Download as pdf or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5820)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (845)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Baylosis Vs Chavez, GR No 95136Document27 pagesBaylosis Vs Chavez, GR No 95136Add AllNo ratings yet

- Exec Summ Recorded Votes 082610Document1 pageExec Summ Recorded Votes 082610Steve CouncilNo ratings yet

- Exec Summ Shorten The Session 082610Document1 pageExec Summ Shorten The Session 082610Steve CouncilNo ratings yet

- Chapter 10Document24 pagesChapter 10Steve CouncilNo ratings yet

- Chapter 1Document14 pagesChapter 1Steve CouncilNo ratings yet

- Workforce Development Requires Educational Reform: by L. Brooke ConawayDocument14 pagesWorkforce Development Requires Educational Reform: by L. Brooke ConawaySteve CouncilNo ratings yet

- Chapter 8Document22 pagesChapter 8Steve CouncilNo ratings yet

- Fact Sheet: Which Counties Spend The Most of Your Tax Dollars?Document7 pagesFact Sheet: Which Counties Spend The Most of Your Tax Dollars?Steve CouncilNo ratings yet

- Chapter 6Document19 pagesChapter 6Steve CouncilNo ratings yet

- Mployment Security Organization of Southern StatesDocument6 pagesMployment Security Organization of Southern StatesSteve CouncilNo ratings yet

- Chapter 2Document28 pagesChapter 2Steve CouncilNo ratings yet

- Chapter 3Document22 pagesChapter 3Steve CouncilNo ratings yet

- Chapter 7Document20 pagesChapter 7Steve CouncilNo ratings yet

- Chapter 5Document21 pagesChapter 5Steve CouncilNo ratings yet

- 4478 Fact Sheet 061010Document4 pages4478 Fact Sheet 061010Steve CouncilNo ratings yet

- Best Worst 2011Document20 pagesBest Worst 2011Steve CouncilNo ratings yet

- Best/Worst of 2010: South Carolina Policy CouncilDocument47 pagesBest/Worst of 2010: South Carolina Policy CouncilSteve CouncilNo ratings yet

- The $21 Billion State Budget: South Carolina's Three Spending CategoriesDocument25 pagesThe $21 Billion State Budget: South Carolina's Three Spending CategoriesSteve CouncilNo ratings yet

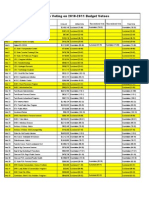

- Senate Budget Veto VotingDocument2 pagesSenate Budget Veto VotingSteve CouncilNo ratings yet

- BudgetWatchObesityMandate 052710Document2 pagesBudgetWatchObesityMandate 052710Steve CouncilNo ratings yet

- Aiken Fact SheetDocument2 pagesAiken Fact SheetSteve CouncilNo ratings yet

- Budget Watch I95 052510Document3 pagesBudget Watch I95 052510Steve CouncilNo ratings yet

- HealthcareDocument2 pagesHealthcareSteve CouncilNo ratings yet

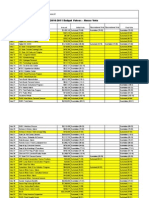

- House Budget Veto VotingDocument3 pagesHouse Budget Veto VotingSteve CouncilNo ratings yet

- Budget Veto HouseDocument4 pagesBudget Veto HouseSteve CouncilNo ratings yet

- BudgetDocument2 pagesBudgetSteve CouncilNo ratings yet

- Sat Scores Report 091010Document5 pagesSat Scores Report 091010Steve CouncilNo ratings yet

- UpdateDocument1 pageUpdateSteve CouncilNo ratings yet

- Juan Padilla Lambert, A055 860 485 (BIA Aug. 23, 2016) PDFDocument14 pagesJuan Padilla Lambert, A055 860 485 (BIA Aug. 23, 2016) PDFImmigrant & Refugee Appellate Center, LLCNo ratings yet

- Course Outline For Agrarian Reform Law and Social Legislation EuDocument5 pagesCourse Outline For Agrarian Reform Law and Social Legislation EuFraicess GonzalesNo ratings yet

- Correctional Institution For WomenDocument2 pagesCorrectional Institution For WomenNam KcalbNo ratings yet

- Vodafone PortugalDocument15 pagesVodafone PortugalMica DGNo ratings yet

- G.R. No. 200274. April 20, 2016. Melecio Domingo, Petitioner, vs. Spouses Genaro MOLINA and ELENA B. MOLINA, Substituted by ESTER MOLINA, RespondentsDocument17 pagesG.R. No. 200274. April 20, 2016. Melecio Domingo, Petitioner, vs. Spouses Genaro MOLINA and ELENA B. MOLINA, Substituted by ESTER MOLINA, RespondentsLalaNo ratings yet

- Mattel V FranciscoDocument2 pagesMattel V FranciscoMichael Enad100% (1)

- Supreme Court: J. Solano Reyes, For Petitioner. Cleofe B. Villar-Verzola For RespondentsDocument4 pagesSupreme Court: J. Solano Reyes, For Petitioner. Cleofe B. Villar-Verzola For Respondentsgem_mataNo ratings yet

- Labor RelationsDocument299 pagesLabor Relationsmtabcao100% (1)

- City of Manila vs. Judge Laguio Gr. No. 118127Document29 pagesCity of Manila vs. Judge Laguio Gr. No. 118127Hanelizan Ert RoadNo ratings yet

- Order Dismissing Kurt Huy Pham's Lawsuit Against His Employer Chase Investment Services 02-20-2013Document10 pagesOrder Dismissing Kurt Huy Pham's Lawsuit Against His Employer Chase Investment Services 02-20-2013FrankBulNo ratings yet

- Perez v. HagonoyDocument2 pagesPerez v. HagonoyJessa F. Austria-CalderonNo ratings yet

- Cyber Crime Investigation in IndiaDocument13 pagesCyber Crime Investigation in IndiaAanika AeryNo ratings yet

- Federalism Class 10 Notes Social Science Civics Chapter 2Document4 pagesFederalism Class 10 Notes Social Science Civics Chapter 2ParthuNo ratings yet

- Whitey by Dick Lehr and Gerard O'Neill - ExcerptDocument15 pagesWhitey by Dick Lehr and Gerard O'Neill - ExcerptCrown Publishing GroupNo ratings yet

- Motion To Attend Wedding Ceremony of DaughterDocument2 pagesMotion To Attend Wedding Ceremony of DaughterMeybs D. DimaanoNo ratings yet

- Jamil V ComelecDocument46 pagesJamil V Comelecpiarodriguez88No ratings yet

- ESMILLA - Heirs of Ramiro V Spouses BacaronDocument3 pagesESMILLA - Heirs of Ramiro V Spouses BacaronJohnny A. Esmilla Jr.No ratings yet

- LAWSUIT: Hagedorn Family Filing Against Jennifer CarnahanDocument5 pagesLAWSUIT: Hagedorn Family Filing Against Jennifer CarnahanFluenceMediaNo ratings yet

- Law 124 Crimpro OcDocument25 pagesLaw 124 Crimpro OcAgent BlueNo ratings yet

- Avera v. Garcia and RodriguezDocument3 pagesAvera v. Garcia and RodriguezGlenz LagunaNo ratings yet

- GFGHFHDocument8 pagesGFGHFHAcuxii PamNo ratings yet

- LEgal Ethics Latest JurisDocument6 pagesLEgal Ethics Latest JurisdyosaNo ratings yet

- Musa v. MosonDocument8 pagesMusa v. MosonTon RiveraNo ratings yet

- Icls Training Materials Sec 2 What Is Intl Law2Document26 pagesIcls Training Materials Sec 2 What Is Intl Law2Dustin NitroNo ratings yet

- Assignement 3 - 20 Mobilia Products Inc v. DemecilioDocument1 pageAssignement 3 - 20 Mobilia Products Inc v. DemeciliopatrickNo ratings yet

- Memorial On Behalf of Respondent (Team Code - LLDC - 087)Document31 pagesMemorial On Behalf of Respondent (Team Code - LLDC - 087)AYUSH R MENON 1850408No ratings yet

- Denoso vs. CADocument3 pagesDenoso vs. CAMarie Nickie BolosNo ratings yet

- CRIMPRO 012 People Vs ValdezDocument5 pagesCRIMPRO 012 People Vs ValdezEm Asiddao-DeonaNo ratings yet

- United States v. Milwaukee Refrigerator Transit Co. 142 F. 247Document7 pagesUnited States v. Milwaukee Refrigerator Transit Co. 142 F. 247Jayvee RobiasNo ratings yet