Download as pdf or txt

You might also like

- 5008S Fresenuis Service ManualDocument318 pages5008S Fresenuis Service ManualEslam Karam100% (10)

- List of Government WebsitesDocument1 pageList of Government Websitessumit-7No ratings yet

- Role of Sebi Under Takeover CodeDocument27 pagesRole of Sebi Under Takeover CodeSAHAL SHAJAHANNo ratings yet

- BMA Consultation PaperDocument72 pagesBMA Consultation PaperAnonymous UpWci5No ratings yet

- Reviewing The Ambit of Control' Apropos To The Objective of Mandatory Bids': An Analysis Under The Takeover RegulationsDocument32 pagesReviewing The Ambit of Control' Apropos To The Objective of Mandatory Bids': An Analysis Under The Takeover Regulationsyarramsetty geethanjaliNo ratings yet

- Utkarsh FinalDocument32 pagesUtkarsh FinalSunit ShandilyaNo ratings yet

- ProCorp FinalDocument21 pagesProCorp FinalShivamNo ratings yet

- Corporate Law 2 ProjDocument11 pagesCorporate Law 2 ProjhimanshuNo ratings yet

- Corporate ReconstructionDocument40 pagesCorporate ReconstructionHemantVermaNo ratings yet

- Akshit Lse InvestmentDocument45 pagesAkshit Lse InvestmentAbhay RanaNo ratings yet

- 2017 - IOSCO - Order Routing Incentives - Final ReportDocument61 pages2017 - IOSCO - Order Routing Incentives - Final ReportsouzajoseNo ratings yet

- Compliance Newsletter - March, 2024Document13 pagesCompliance Newsletter - March, 2024Chiranjibi PandaNo ratings yet

- Legal Regulation 1.editedDocument43 pagesLegal Regulation 1.editedPoetic YatchyNo ratings yet

- 4 Competition LawDocument36 pages4 Competition LawYash KalaNo ratings yet

- Legal Term PaperDocument49 pagesLegal Term PaperAbhi ShresthaNo ratings yet

- Role of Cci in Banking Mergers With Special Reference To Banking Law AmendmentDocument20 pagesRole of Cci in Banking Mergers With Special Reference To Banking Law AmendmentishuNo ratings yet

- Damodaram Sanjivayya National Law UniversityDocument22 pagesDamodaram Sanjivayya National Law UniversityRahaMan ShaikNo ratings yet

- Security Analysis AND Portfolio Management Assignment 2Document9 pagesSecurity Analysis AND Portfolio Management Assignment 2Ankur SharmaNo ratings yet

- Capital Market 2Document22 pagesCapital Market 2rashi bakshNo ratings yet

- Best Practices of IT ProcurementDocument40 pagesBest Practices of IT ProcurementgpppNo ratings yet

- Relevant Research ArticleDocument26 pagesRelevant Research ArticleVedant MaskeNo ratings yet

- Securities Law Research Project - Poorna Poovamma K.M.Document18 pagesSecurities Law Research Project - Poorna Poovamma K.M.parishtiNo ratings yet

- SEBI (Delisting of Equity Shares) Regulations, 2009Document11 pagesSEBI (Delisting of Equity Shares) Regulations, 2009Abhijithsr TvpmNo ratings yet

- Corporate Procurement Policy enDocument7 pagesCorporate Procurement Policy enLele ScarfNo ratings yet

- SebiDocument8 pagesSebiSakshi rayNo ratings yet

- Dr. Ram Manohar Lohia National Law University, LucknowDocument18 pagesDr. Ram Manohar Lohia National Law University, LucknowAbhishek PratapNo ratings yet

- Amendments: Corporate Funding & Listings in Stock ExchangesDocument6 pagesAmendments: Corporate Funding & Listings in Stock ExchangesVSNo ratings yet

- Corporate Strategy and Capital Structure-FullTextThesis PDFDocument299 pagesCorporate Strategy and Capital Structure-FullTextThesis PDFSuharliNo ratings yet

- A Study On Organizational Study in Reliance Securities Ltd.Document48 pagesA Study On Organizational Study in Reliance Securities Ltd.Vidhyashankar IyerNo ratings yet

- TopicDocument10 pagesTopicprawaichal69No ratings yet

- Rbi & SebiDocument14 pagesRbi & SebiAbhijeetNo ratings yet

- Investment and Security LawDocument26 pagesInvestment and Security LawKishalaya PalNo ratings yet

- 7 CCCS Guidelines On Directions RemediesDocument22 pages7 CCCS Guidelines On Directions RemediesSuchiNo ratings yet

- Report On Portfolio Management BusinessDocument20 pagesReport On Portfolio Management BusinessLouis NoronhaNo ratings yet

- Master Circular For ESG Rating Providers (ERPs) by SEBIDocument60 pagesMaster Circular For ESG Rating Providers (ERPs) by SEBIArchisman DeyNo ratings yet

- Project Towards Partial Fulfilment of The CA3 Assessment in Banking and FinanceDocument16 pagesProject Towards Partial Fulfilment of The CA3 Assessment in Banking and FinanceRichik DadhichNo ratings yet

- Labour LawDocument13 pagesLabour LawYashmeetNo ratings yet

- Manual For Procurement of Goods - 1Document289 pagesManual For Procurement of Goods - 1Hire ViewNo ratings yet

- Consultive Paper On InsiderTradingDocument10 pagesConsultive Paper On InsiderTradingAKS_RSNo ratings yet

- PMS Master CircularDocument100 pagesPMS Master CircularLouis NoronhaNo ratings yet

- IOSCOPD638 Suitability and Distribution of Complex Financial ProductsDocument37 pagesIOSCOPD638 Suitability and Distribution of Complex Financial ProductsKevin SantosNo ratings yet

- Recommendations Concerning Remuneration and Hours of Work For Articled StudentsDocument17 pagesRecommendations Concerning Remuneration and Hours of Work For Articled StudentsanjeeNo ratings yet

- Corporate Restructuring PDFDocument26 pagesCorporate Restructuring PDFAbhishek GuptaNo ratings yet

- GLP Letter To ShareholdersDocument7 pagesGLP Letter To ShareholdersIosiasNo ratings yet

- Final Pronouncement The Restructured Code - 0Document200 pagesFinal Pronouncement The Restructured Code - 0Juvêncio ChigonaNo ratings yet

- Objectives and Principles of Securities RegulationDocument68 pagesObjectives and Principles of Securities Regulation11black2No ratings yet

- Competition LawDocument19 pagesCompetition LawSreelekhaNo ratings yet

- SFA FAA PhaseII Policy ConsultationDocument60 pagesSFA FAA PhaseII Policy ConsultationHarpott GhantaNo ratings yet

- FFDocument718 pagesFFashok kumarNo ratings yet

- Manual For Procurement of Consultancy & Other Services - 0Document214 pagesManual For Procurement of Consultancy & Other Services - 0achuusNo ratings yet

- WINS August Newsletter 2023Document68 pagesWINS August Newsletter 2023suhitaNo ratings yet

- Dewan Standar Akuntansi Keuangan: Mr. Hans HoogervorstDocument3 pagesDewan Standar Akuntansi Keuangan: Mr. Hans HoogervorstSarah FauziaNo ratings yet

- Corporate LawsDocument17 pagesCorporate LawsMayank TripathiNo ratings yet

- Regulation of Combinations Under The Competition LDocument30 pagesRegulation of Combinations Under The Competition LDileep ChowdaryNo ratings yet

- Implications of Korea's Recent Measures To Improve Asset-Backed Securities MarketDocument7 pagesImplications of Korea's Recent Measures To Improve Asset-Backed Securities MarketminhphuongNo ratings yet

- General Framework of Revenue Requirement Determination MethodologyDocument35 pagesGeneral Framework of Revenue Requirement Determination MethodologyRaul FenrandezNo ratings yet

- SEBI Takeover Code - Detailed Analysis - Taxguru - inDocument27 pagesSEBI Takeover Code - Detailed Analysis - Taxguru - insumeet sheokandNo ratings yet

- Research Report: Listing Regime Reforms For Dual-Class Share Structure and Biotech IndustryDocument22 pagesResearch Report: Listing Regime Reforms For Dual-Class Share Structure and Biotech IndustrySean Ng Jun JieNo ratings yet

- SEBI and Primary MarketDocument7 pagesSEBI and Primary Marketशुभम डिमरीNo ratings yet

- Mutual Funds in India: Structure, Performance and UndercurrentsFrom EverandMutual Funds in India: Structure, Performance and UndercurrentsNo ratings yet

- Emergence of National Law Universities ADocument28 pagesEmergence of National Law Universities AAnushriNo ratings yet

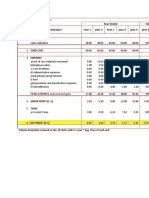

- All Values in INR CRDocument1 pageAll Values in INR CRAnushriNo ratings yet

- CONSTi Summary NotesDocument91 pagesCONSTi Summary NotesAnushriNo ratings yet

- Affidavit For Declaration of Ownership of Immovable Property Held in IndiaDocument1 pageAffidavit For Declaration of Ownership of Immovable Property Held in IndiaAnushriNo ratings yet

- Applicability of Hindu LawDocument31 pagesApplicability of Hindu LawAnushriNo ratings yet

- Divorce Under Hindu LawDocument21 pagesDivorce Under Hindu LawAnushriNo ratings yet

- 84501-9200-9L-008 Rev-0 Technical Inspection Services Company Final Documentation RequirementsDocument7 pages84501-9200-9L-008 Rev-0 Technical Inspection Services Company Final Documentation RequirementsPeni M. SaptoargoNo ratings yet

- Georgina Smith - Resume 1Document3 pagesGeorgina Smith - Resume 1api-559062488No ratings yet

- Experiencing Postsocialist CapitalismDocument251 pagesExperiencing Postsocialist CapitalismjelisNo ratings yet

- The Laws On Local Governments SyllabusDocument4 pagesThe Laws On Local Governments SyllabusJohn Kevin ArtuzNo ratings yet

- HD Consumer Behavior AssignmentDocument9 pagesHD Consumer Behavior AssignmentAishwaryaNo ratings yet

- API BasicsDocument6 pagesAPI BasicsSrinivas BathulaNo ratings yet

- Ebook Digital Marketing PDF Full Chapter PDFDocument67 pagesEbook Digital Marketing PDF Full Chapter PDFamy.farley40997% (33)

- Kalsi® Building Board Cladding: Kalsi® Clad Standard DimensionsDocument1 pageKalsi® Building Board Cladding: Kalsi® Clad Standard DimensionsDenis AkingbasoNo ratings yet

- Safety Manual (B-80687EN 10)Document35 pagesSafety Manual (B-80687EN 10)Jander Luiz TomaziNo ratings yet

- The Body Productive Rethinking Capitalism Work and The Body Steffan Blayney Full ChapterDocument67 pagesThe Body Productive Rethinking Capitalism Work and The Body Steffan Blayney Full Chaptersharon.tuttle380100% (6)

- Conceptual FrameworkDocument4 pagesConceptual FrameworkEustass KiddNo ratings yet

- BNVD Eaufrance Metadonnees Vente 20230130Document16 pagesBNVD Eaufrance Metadonnees Vente 20230130moussaouiNo ratings yet

- Different Kinds of Meat ProductsDocument7 pagesDifferent Kinds of Meat ProductsYam MuhiNo ratings yet

- Philippine Statistics Authority: Date (2021)Document9 pagesPhilippine Statistics Authority: Date (2021)Nah ReeNo ratings yet

- LPPDocument35 pagesLPPommprakashpanda15scribdNo ratings yet

- 1231.322 323 MSDS Sabroe 1507-100 MSDSDocument6 pages1231.322 323 MSDS Sabroe 1507-100 MSDSzhyhhNo ratings yet

- Policy Copy 3005 314095178 00 000Document3 pagesPolicy Copy 3005 314095178 00 000alagardharshan2No ratings yet

- 2011 C1 CoMe ORGMIDocument8 pages2011 C1 CoMe ORGMIADJ ADJNo ratings yet

- William Gann Method PDFDocument1 pageWilliam Gann Method PDFchandra widjajaNo ratings yet

- SAILOR 6081 Power Supply Unit and Charger: Installation ManualDocument72 pagesSAILOR 6081 Power Supply Unit and Charger: Installation ManualMariosNo ratings yet

- BitBox CarList 2022 10 28Document97 pagesBitBox CarList 2022 10 28marcos hernandezNo ratings yet

- Lienard EquationDocument9 pagesLienard EquationmenguemengueNo ratings yet

- File Handling in JavaDocument8 pagesFile Handling in JavaDipendra KmNo ratings yet

- Full Chapter Embracing Modern C Safely 1St Edition Lakos PDFDocument53 pagesFull Chapter Embracing Modern C Safely 1St Edition Lakos PDFjeffery.rosseau147No ratings yet

- List of TradeMark Forms & Therein PDFDocument17 pagesList of TradeMark Forms & Therein PDFShreeneetRathiNo ratings yet

- Beginner's Guide To SoloDocument12 pagesBeginner's Guide To SoloTiurNo ratings yet

- JF 2 14 PDFDocument32 pagesJF 2 14 PDFIoannis GaridasNo ratings yet

- DX-790-960-65-16.5i-M Model: A79451600v02: Antenna SpecificationsDocument2 pagesDX-790-960-65-16.5i-M Model: A79451600v02: Antenna SpecificationsakiselNo ratings yet