Download as pdf or txt

You might also like

- Strategies Wells Fargo Can Use To GROW From A Billion Dollar Company To A Trillion Dollar CompanyDocument4 pagesStrategies Wells Fargo Can Use To GROW From A Billion Dollar Company To A Trillion Dollar CompanyEnock TareNo ratings yet

- Flipkart Project (Arindam Dutta)Document47 pagesFlipkart Project (Arindam Dutta)Music & Art80% (5)

- An Investigation On Efficient Loan and Advances of Karnataka BankDocument56 pagesAn Investigation On Efficient Loan and Advances of Karnataka BankNithin GowdaNo ratings yet

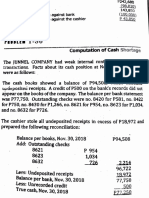

- Manarang Auto Repair Shop Journal by The Month of January 2019Document9 pagesManarang Auto Repair Shop Journal by The Month of January 2019Renz MoralesNo ratings yet

- IGCSE Edexcel Business Studies NotesDocument30 pagesIGCSE Edexcel Business Studies NotesEllie Housen100% (1)

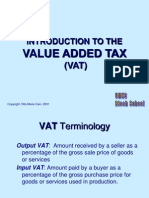

- Pre-Week Notes On Vat: Prepared by Dr. Jeannie P. LimDocument11 pagesPre-Week Notes On Vat: Prepared by Dr. Jeannie P. LimMark MagnoNo ratings yet

- Problem 2Document4 pagesProblem 2redassdawn100% (1)

- Lecture Slides - Lecture 01 - VAT (Part 1)Document6 pagesLecture Slides - Lecture 01 - VAT (Part 1)nkosinathiNo ratings yet

- Taxation Report2Document22 pagesTaxation Report2Ritchelyn ArbonNo ratings yet

- Vat Zero Rated SuppliesDocument2 pagesVat Zero Rated SuppliesPrecy B BinwagNo ratings yet

- EH403 TAXATION MIDTERMS VAT - EditedDocument12 pagesEH403 TAXATION MIDTERMS VAT - Editedethel hyugaNo ratings yet

- Final PaperDocument20 pagesFinal PaperLaila PaleyanNo ratings yet

- Gruba Tax 2 NotesDocument13 pagesGruba Tax 2 NotesPJezrael Arreza FrondozoNo ratings yet

- Corporate Income TaxDocument70 pagesCorporate Income TaxNhung HồngNo ratings yet

- Value Added Tax NotesDocument12 pagesValue Added Tax NotesAimeeNo ratings yet

- Lecture On VAT Output Vat PDFDocument7 pagesLecture On VAT Output Vat PDFCarl's Aeto DomingoNo ratings yet

- ICAEW Principles of Taxation CH 11-13Document30 pagesICAEW Principles of Taxation CH 11-13ITALIANO hohNo ratings yet

- GNotes2 VAT 2018 With TRAIN AmendmentsDocument31 pagesGNotes2 VAT 2018 With TRAIN AmendmentsKristine Bucu100% (4)

- Sales Tax - VATDocument6 pagesSales Tax - VATSAJNo ratings yet

- 1 Basics of Value Added TaxDocument58 pages1 Basics of Value Added TaxHazel Andrea Garduque LopezNo ratings yet

- Tax Session I - VATDocument32 pagesTax Session I - VATbrightkeysNo ratings yet

- Business TaxationDocument6 pagesBusiness TaxationPATRICK JAMES BALOGBOG ROSARIONo ratings yet

- VAT Presentation - Staff.Document36 pagesVAT Presentation - Staff.zubairNo ratings yet

- Value Added TaxDocument29 pagesValue Added TaxSNLTNo ratings yet

- Other TaxesDocument51 pagesOther Taxesmbandamanathan22No ratings yet

- Unit 6: Value Added Tax (Proclamation 285/2002 Regulation 79/2002 Proclamation 609/2008)Document23 pagesUnit 6: Value Added Tax (Proclamation 285/2002 Regulation 79/2002 Proclamation 609/2008)Bizu AtnafuNo ratings yet

- 8VATDocument70 pages8VATNoelNo ratings yet

- Value Added Tax (Cap 476)Document15 pagesValue Added Tax (Cap 476)Triila manillaNo ratings yet

- TAXATION 2 Chapter 13 Input VATDocument2 pagesTAXATION 2 Chapter 13 Input VATKim Cristian MaañoNo ratings yet

- VAT AnnotatedDocument46 pagesVAT AnnotatedDr SafaNo ratings yet

- Explanatory Notes For The Completion of Vat Return FormDocument3 pagesExplanatory Notes For The Completion of Vat Return FormTendai ZamangweNo ratings yet

- VatDocument50 pagesVatnikolaevnavalentinaNo ratings yet

- BSTX Reviewer (Midterm)Document7 pagesBSTX Reviewer (Midterm)alaine daphneNo ratings yet

- Tax - Vat GuidenotesDocument13 pagesTax - Vat GuidenotesNardz AndananNo ratings yet

- Vat Full Set PowerpointDocument79 pagesVat Full Set PowerpointthamsanqamanciNo ratings yet

- 05 Input TaxesDocument4 pages05 Input TaxesJaneLayugCabacunganNo ratings yet

- UAE VAT InfoCircularDocument3 pagesUAE VAT InfoCircularMohammadNo ratings yet

- Value Added Tax - VatDocument37 pagesValue Added Tax - VatTimoth MbwiloNo ratings yet

- 07 Business Tax and VATDocument5 pages07 Business Tax and VATlemvin121003No ratings yet

- Tax.3213-7 Output Input and Vat PayableDocument11 pagesTax.3213-7 Output Input and Vat PayableMira Louise HernandezNo ratings yet

- Value Added TaxDocument17 pagesValue Added TaxkirigofortunateNo ratings yet

- TAXATION II KMA PREFINALS VAT EditedDocument14 pagesTAXATION II KMA PREFINALS VAT Editedethel hyuga0% (1)

- Lecture 01 VAT - Lecture SlidesDocument9 pagesLecture 01 VAT - Lecture Slideslameck noah zuluNo ratings yet

- Input Vat: Prepared By: Mrs. Nelia I. Tomas, CPA, LPTDocument28 pagesInput Vat: Prepared By: Mrs. Nelia I. Tomas, CPA, LPTAjey MendiolaNo ratings yet

- Vat System and OptDocument15 pagesVat System and Optlyra21No ratings yet

- Value Added Tax: Scope of ApplicationsDocument5 pagesValue Added Tax: Scope of ApplicationsNguyen Duy Khanh QP0073No ratings yet

- Administration of Value Added Tax-VatDocument13 pagesAdministration of Value Added Tax-VatRuth NyawiraNo ratings yet

- Input Taxes SummaryDocument8 pagesInput Taxes SummaryMichael AquinoNo ratings yet

- 07 Chap 15 16 Mamalateo 2019 Tax BookDocument19 pages07 Chap 15 16 Mamalateo 2019 Tax BookJeremias CusayNo ratings yet

- Value Added TaxDocument9 pagesValue Added TaxĴõ ĔĺNo ratings yet

- Tax 2 Reviewer Atty. Bolivar NotesDocument66 pagesTax 2 Reviewer Atty. Bolivar NotesMaree BajamundeNo ratings yet

- VAT Output TaxesDocument7 pagesVAT Output TaxesJocelyn Verbo-AyubanNo ratings yet

- Value Added TaxesDocument75 pagesValue Added TaxesLEILALYN NICOLAS100% (1)

- WTS Dhruva VAT Handbook PDFDocument40 pagesWTS Dhruva VAT Handbook PDFFaraz AkhtarNo ratings yet

- Implementing VAT in Your Business: E-ServicesDocument1 pageImplementing VAT in Your Business: E-ServicesSalman YousufNo ratings yet

- Value Added TaxDocument15 pagesValue Added TaxJoshua PeraltaNo ratings yet

- Value Added Tax (VAT) : TaxesDocument8 pagesValue Added Tax (VAT) : TaxesattiqullahmalikNo ratings yet

- BUSLAW3 C1 (Notes On Business Taxes)Document7 pagesBUSLAW3 C1 (Notes On Business Taxes)Brad Stevens1911No ratings yet

- VATDocument11 pagesVATSaurav KumarNo ratings yet

- HANDOUT FOR VAT-NewDocument25 pagesHANDOUT FOR VAT-NewCristian RenatusNo ratings yet

- Value Added Tax2Document28 pagesValue Added Tax2biburaNo ratings yet

- Bustax Chapter 9Document10 pagesBustax Chapter 9Pineda, Paula MarieNo ratings yet

- Very Awkward Tax: A bite-size guide to VAT for small businessFrom EverandVery Awkward Tax: A bite-size guide to VAT for small businessNo ratings yet

- TD Bank StatementDocument1 pageTD Bank Statementnurulamin00023No ratings yet

- Statement Bank MARCH Just White LLC 7d68313aa6Document8 pagesStatement Bank MARCH Just White LLC 7d68313aa6Madelyn VasquezNo ratings yet

- LeanCor Capabilities Presentation - The Lean Logistics Operations ProviderDocument12 pagesLeanCor Capabilities Presentation - The Lean Logistics Operations ProviderLeanCorNo ratings yet

- Project in FinAccDocument15 pagesProject in FinAccBrod Lee SantosNo ratings yet

- Reading in Philippine History - Learning Activity 2 GOLDEN AGEDocument1 pageReading in Philippine History - Learning Activity 2 GOLDEN AGEClaro M. GarchitorenaNo ratings yet

- Capacity PROBLEMSDocument3 pagesCapacity PROBLEMSJustNo ratings yet

- Marketing Metrics - Chapter 3Document28 pagesMarketing Metrics - Chapter 3Hoang Yen NhiNo ratings yet

- 2023-24 Planning CalendarDocument3 pages2023-24 Planning CalendarvesotiktokizazovNo ratings yet

- BillDocument1 pageBillTabrez AhamadNo ratings yet

- Qdoc - Tips - Database of Big BrandsDocument33 pagesQdoc - Tips - Database of Big BrandsUday kumarNo ratings yet

- Business Law 34 Marks Revision - CTC ClassesDocument36 pagesBusiness Law 34 Marks Revision - CTC ClassesThe Real BNo ratings yet

- Doddy Bicara InvestasiDocument34 pagesDoddy Bicara InvestasiAmri RijalNo ratings yet

- Training Report - Abhishek SharmaDocument46 pagesTraining Report - Abhishek SharmaHeena KaushalNo ratings yet

- Lecture 1A - Introduction, Agency and Financial MarketsDocument54 pagesLecture 1A - Introduction, Agency and Financial MarketsJackieNo ratings yet

- 空调维修已付款凭证Document3 pages空调维修已付款凭证william6703No ratings yet

- Importance of Entrepreneur ShipDocument23 pagesImportance of Entrepreneur ShipXiet JimenezNo ratings yet

- Test 1 - 2022 08 17Document3 pagesTest 1 - 2022 08 17MiclczeeNo ratings yet

- Unemployment A Menace To National EconomyDocument8 pagesUnemployment A Menace To National EconomyMan BhaiNo ratings yet

- Case Study:: Department of International Business ManagementDocument29 pagesCase Study:: Department of International Business ManagementTak BunleangNo ratings yet

- Instructions To Bidder ITB - Rev.01Document20 pagesInstructions To Bidder ITB - Rev.01stegenNo ratings yet

- AppendicesDocument7 pagesAppendicesKrishna ShresthaNo ratings yet

- Documents For UploadDocument12 pagesDocuments For UploadMilind GoplaniNo ratings yet

- Neo - Classical School of Economics: Leading Economists: Alfred Marshall (English), Knut Wicksell (Swedish)Document18 pagesNeo - Classical School of Economics: Leading Economists: Alfred Marshall (English), Knut Wicksell (Swedish)Ishrat Jahan DiaNo ratings yet

- Client's Guide On Forms - Policy Change Request FormDocument14 pagesClient's Guide On Forms - Policy Change Request FormJulienne Mhae ReyesNo ratings yet