BF 220 Test One Practice

BF 220 Test One Practice

You might also like

- B7AF102 Financial Accounting May 2023Document11 pagesB7AF102 Financial Accounting May 2023gerlaniamelgacoNo ratings yet

- International Taxation OutlineDocument138 pagesInternational Taxation OutlineMa FajardoNo ratings yet

- FAR210 - July 2023 - QDocument8 pagesFAR210 - July 2023 - QafiqahNo ratings yet

- IAS 1 MAC LTDDocument2 pagesIAS 1 MAC LTDvuchiduc.contactNo ratings yet

- Faculty - Accountancy - 2022 - Session 1 - Diploma - Far210Document8 pagesFaculty - Accountancy - 2022 - Session 1 - Diploma - Far210Bil hutNo ratings yet

- Bs 320 TutorialDocument4 pagesBs 320 TutorialPrince Daniels TutorNo ratings yet

- FAR210 - Feb 2022 - QDocument8 pagesFAR210 - Feb 2022 - Qqh2mtyprq8No ratings yet

- Bs 320 - 30th AprilDocument2 pagesBs 320 - 30th AprilPrince Daniels TutorNo ratings yet

- FA Dec 2022Document8 pagesFA Dec 2022Shawn LiewNo ratings yet

- Far210 Fe Feb23Document8 pagesFar210 Fe Feb23ediza adhaNo ratings yet

- BS 320Document3 pagesBS 320Prince Daniels TutorNo ratings yet

- Cuac208 Tests and AssignmentsDocument8 pagesCuac208 Tests and AssignmentsInnocent GwangwaraNo ratings yet

- Final Assessment Far210 Feb2021Document8 pagesFinal Assessment Far210 Feb2021Lampard AimanNo ratings yet

- MC 4 - Deferred Tax - A231Document4 pagesMC 4 - Deferred Tax - A231Patricia TangNo ratings yet

- MAN1068 Exam Paper 2021-22Document16 pagesMAN1068 Exam Paper 2021-22Praveena RavishankerNo ratings yet

- Bac 2211 Cat&assignment Sep 2023Document5 pagesBac 2211 Cat&assignment Sep 2023toniruii98No ratings yet

- Final FAR-2 Mock Q. PaperDocument6 pagesFinal FAR-2 Mock Q. PaperAli OptimisticNo ratings yet

- Test Series: March 2023 Mock Test Paper 1 Intermediate: Group - I Paper - 1: AccountingDocument75 pagesTest Series: March 2023 Mock Test Paper 1 Intermediate: Group - I Paper - 1: AccountingKartik GuptaNo ratings yet

- Far270 July2022Document8 pagesFar270 July2022Nur Fatin AmirahNo ratings yet

- Assignment FarDocument5 pagesAssignment FarALIESYA FARHANA ALI HUSSAIN GHAZALINo ratings yet

- UOL ExamDocument11 pagesUOL ExamThant Hayman ThwayNo ratings yet

- BBF 313 Financial Reporting, Analysis and Planning: Code of The Name of The Module Date of Exam Time of Exam SetDocument4 pagesBBF 313 Financial Reporting, Analysis and Planning: Code of The Name of The Module Date of Exam Time of Exam Setkp107416No ratings yet

- 73507bos59335 Inter p1qDocument7 pages73507bos59335 Inter p1qRaish QURESHINo ratings yet

- Far270 February 22 FaDocument8 pagesFar270 February 22 FarumaisyaNo ratings yet

- Test Series: April 2023 Mock Test Paper - 2 Intermediate: Group - I Paper - 1: AccountingDocument7 pagesTest Series: April 2023 Mock Test Paper - 2 Intermediate: Group - I Paper - 1: AccountingKartik GuptaNo ratings yet

- 1 2 3 4 5 6 7 8 MergedDocument78 pages1 2 3 4 5 6 7 8 MergedKartik GuptaNo ratings yet

- CPA 1 - Financial Accounting - Paper 1dec 2022Document9 pagesCPA 1 - Financial Accounting - Paper 1dec 2022Asaba GloriaNo ratings yet

- MTP 3 14 Questions 1680520270Document7 pagesMTP 3 14 Questions 1680520270Umar MalikNo ratings yet

- CPA Paper 1 Financial Accounting 2Document9 pagesCPA Paper 1 Financial Accounting 2philipisingomaNo ratings yet

- Spring 2024 - MGT401 - 1Document3 pagesSpring 2024 - MGT401 - 1Wahab AftabNo ratings yet

- AccrDocument2 pagesAccrlearningcantstop561No ratings yet

- Case StudyDocument3 pagesCase Study203560No ratings yet

- Midterm - Far2 - AmendedDocument2 pagesMidterm - Far2 - AmendedmellNo ratings yet

- FA Dec 2021Document8 pagesFA Dec 2021Shawn LiewNo ratings yet

- FAR460 Jan 24Document8 pagesFAR460 Jan 24wan idharNo ratings yet

- Faculty Accountancy 2022 Session 1 - Diploma Far210Document8 pagesFaculty Accountancy 2022 Session 1 - Diploma Far210nafisah rahmanNo ratings yet

- MC 3 Topic 4 Def Tax Question A232Document4 pagesMC 3 Topic 4 Def Tax Question A232thanusri0103No ratings yet

- WP contentuploads202302FINANCIAL ACCOUNTING PAPER 1.1 Dec 2023 PDFDocument22 pagesWP contentuploads202302FINANCIAL ACCOUNTING PAPER 1.1 Dec 2023 PDFProsperity Thēë BwøyNo ratings yet

- Final Exam July 2021 QQDocument8 pagesFinal Exam July 2021 QQLampard AimanNo ratings yet

- FAR460 - JAN 2023 Group Assignment B Published Financial Statements Instructions To StudentsDocument5 pagesFAR460 - JAN 2023 Group Assignment B Published Financial Statements Instructions To StudentsAmniNo ratings yet

- Mba ZC415 Ec-3r First Sem 2022-2023Document4 pagesMba ZC415 Ec-3r First Sem 2022-2023Ravi KaviNo ratings yet

- Control Test 1 - March 2022Document4 pagesControl Test 1 - March 2022yandisaNo ratings yet

- Q Far270 July2021 - Set 1Document8 pagesQ Far270 July2021 - Set 1nafisah rahmanNo ratings yet

- B7AF102 2021 OMD1 First Sitting Exam PaperDocument10 pagesB7AF102 2021 OMD1 First Sitting Exam PaperAZLEA BINTI SYED HUSSIN (BG)No ratings yet

- University of Bradford Financial Accounting, Afe5008-B Final ExaminationDocument9 pagesUniversity of Bradford Financial Accounting, Afe5008-B Final ExaminationDiana TuckerNo ratings yet

- 2022 Grade 10 Controlled Test 3 QP EngDocument5 pages2022 Grade 10 Controlled Test 3 QP EngkellzylesediNo ratings yet

- Assignment Financial 2024 18TH MarchDocument6 pagesAssignment Financial 2024 18TH MarchBen Noah EuroNo ratings yet

- CAF 1 FAR1 Autumn 2022Document6 pagesCAF 1 FAR1 Autumn 2022QasimNo ratings yet

- Poa T - 12Document4 pagesPoa T - 12SHEVENA A/P VIJIANNo ratings yet

- FR Day 1Document9 pagesFR Day 1Fun DietNo ratings yet

- Corporate Reporting Nd-2022 QuestionDocument7 pagesCorporate Reporting Nd-2022 QuestionMDSadeq-ulIslamNo ratings yet

- 21NDocument22 pages21NWinnie GNo ratings yet

- Socw - 1263543589Document7 pagesSocw - 1263543589dolevov652No ratings yet

- (EN) Problem Mojakoe AK1Document11 pages(EN) Problem Mojakoe AK1gebbyNo ratings yet

- CAF 1 FAR1 Autumn 2023Document6 pagesCAF 1 FAR1 Autumn 2023z8qcsqfj8dNo ratings yet

- FAC612S - Test 3 2023Document5 pagesFAC612S - Test 3 2023simaneka.shilongoNo ratings yet

- Financial Accounting 2A Final OSA PDFDocument5 pagesFinancial Accounting 2A Final OSA PDFdamian.levendalNo ratings yet

- Shareholders' Equity p21 28Document19 pagesShareholders' Equity p21 28Rizalito SisonNo ratings yet

- Finance Assignment Due MarchDocument19 pagesFinance Assignment Due MarchJeenika S SingaravaluNo ratings yet

- CA Inter Adv Accounts Suggested Answer May 2022Document30 pagesCA Inter Adv Accounts Suggested Answer May 2022BILLU-YTNo ratings yet

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisFrom EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisNo ratings yet

- Benefit Illustration For HDFC Life Sanchay Par AdvantageDocument3 pagesBenefit Illustration For HDFC Life Sanchay Par AdvantageVamsi Krishna BNo ratings yet

- IRCTC E-Catering - Order Booked #36108741Document1 pageIRCTC E-Catering - Order Booked #36108741Debopriyo MukherjiNo ratings yet

- Shoe Factory Plant Manager: Gross Salary ElementsDocument2 pagesShoe Factory Plant Manager: Gross Salary ElementsSukaina SalmanNo ratings yet

- OD225537427076154000Document1 pageOD225537427076154000Sandipan BiswasNo ratings yet

- Price List For Fiesta Homes by SJR PrimecorpDocument1 pagePrice List For Fiesta Homes by SJR PrimecorpAswath FarookNo ratings yet

- Trial Balance Ud Mudah HasilDocument1 pageTrial Balance Ud Mudah HasilSani SausanNo ratings yet

- AssignmentDocument3 pagesAssignmentDùķe HPNo ratings yet

- Invoice 197Document2 pagesInvoice 197miroljubNo ratings yet

- Basic Principles - Taxn01bDocument28 pagesBasic Principles - Taxn01bJericho PedragosaNo ratings yet

- Taxation Short Questions AnswersDocument4 pagesTaxation Short Questions AnswersSheetal IyerNo ratings yet

- Uttar Pradesh Budget Analysis 2019-20Document6 pagesUttar Pradesh Budget Analysis 2019-20AdNo ratings yet

- The VAT GuideDocument195 pagesThe VAT Guidestingray2No ratings yet

- New Tax Rates (TRAIN LAW) PDFDocument1 pageNew Tax Rates (TRAIN LAW) PDFphoebemariealhambra1475No ratings yet

- Bar Examination 2006 - TaxationlawDocument7 pagesBar Examination 2006 - TaxationlawLyraNo ratings yet

- Godrej Prana Price SheetDocument10 pagesGodrej Prana Price Sheetbigdealsin14No ratings yet

- Formst 1Document3 pagesFormst 1arulantonyNo ratings yet

- Chapter 16 Practice Problems Solution Manual 2020Document29 pagesChapter 16 Practice Problems Solution Manual 2020James SeelosNo ratings yet

- Transfer Pricing Country Profile BulgariaDocument16 pagesTransfer Pricing Country Profile BulgariaIoanna ZlatevaNo ratings yet

- Osmena vs. OrbosDocument2 pagesOsmena vs. OrbosDana Denisse RicaplazaNo ratings yet

- Od 225991033389305000Document1 pageOd 225991033389305000Iqbal khanNo ratings yet

- Synopsis of Project GSTDocument4 pagesSynopsis of Project GSTamarjeet singhNo ratings yet

- Circular CGST 199Document4 pagesCircular CGST 199Jaipur-B Gr-2No ratings yet

- Chapter 3 Charge Under GSTDocument10 pagesChapter 3 Charge Under GSTabhay javiyaNo ratings yet

- Paper4 - Taxation - MTP - All Attempts - May23Document335 pagesPaper4 - Taxation - MTP - All Attempts - May23devaaNo ratings yet

- Quote: 2215 Paseo de Las Americas Suite # 29 San Diego, CA 92154 PH# (858) 513-7748 FX# (858) 513-7757Document1 pageQuote: 2215 Paseo de Las Americas Suite # 29 San Diego, CA 92154 PH# (858) 513-7748 FX# (858) 513-7757Armenta EdwinNo ratings yet

- US Internal Revenue Service: I1040se - 1997Document5 pagesUS Internal Revenue Service: I1040se - 1997IRSNo ratings yet

- Respondent: Raja Benoy Kumar Sahas RoyDocument3 pagesRespondent: Raja Benoy Kumar Sahas RoysontineniNo ratings yet

- Complete Taxation PrelimDocument59 pagesComplete Taxation PrelimJOSHUA M. ESCOTONo ratings yet

- DATE: 19.12.2021 JOB NO: 192-9203-000 Invoice No.: 192-9203-FPC-191221Document1 pageDATE: 19.12.2021 JOB NO: 192-9203-000 Invoice No.: 192-9203-FPC-191221Mohammad MudassarNo ratings yet

Download as pdf or txt

You might also like

- B7AF102 Financial Accounting May 2023Document11 pagesB7AF102 Financial Accounting May 2023gerlaniamelgacoNo ratings yet

- International Taxation OutlineDocument138 pagesInternational Taxation OutlineMa FajardoNo ratings yet

- FAR210 - July 2023 - QDocument8 pagesFAR210 - July 2023 - QafiqahNo ratings yet

- IAS 1 MAC LTDDocument2 pagesIAS 1 MAC LTDvuchiduc.contactNo ratings yet

- Faculty - Accountancy - 2022 - Session 1 - Diploma - Far210Document8 pagesFaculty - Accountancy - 2022 - Session 1 - Diploma - Far210Bil hutNo ratings yet

- Bs 320 TutorialDocument4 pagesBs 320 TutorialPrince Daniels TutorNo ratings yet

- FAR210 - Feb 2022 - QDocument8 pagesFAR210 - Feb 2022 - Qqh2mtyprq8No ratings yet

- Bs 320 - 30th AprilDocument2 pagesBs 320 - 30th AprilPrince Daniels TutorNo ratings yet

- FA Dec 2022Document8 pagesFA Dec 2022Shawn LiewNo ratings yet

- Far210 Fe Feb23Document8 pagesFar210 Fe Feb23ediza adhaNo ratings yet

- BS 320Document3 pagesBS 320Prince Daniels TutorNo ratings yet

- Cuac208 Tests and AssignmentsDocument8 pagesCuac208 Tests and AssignmentsInnocent GwangwaraNo ratings yet

- Final Assessment Far210 Feb2021Document8 pagesFinal Assessment Far210 Feb2021Lampard AimanNo ratings yet

- MC 4 - Deferred Tax - A231Document4 pagesMC 4 - Deferred Tax - A231Patricia TangNo ratings yet

- MAN1068 Exam Paper 2021-22Document16 pagesMAN1068 Exam Paper 2021-22Praveena RavishankerNo ratings yet

- Bac 2211 Cat&assignment Sep 2023Document5 pagesBac 2211 Cat&assignment Sep 2023toniruii98No ratings yet

- Final FAR-2 Mock Q. PaperDocument6 pagesFinal FAR-2 Mock Q. PaperAli OptimisticNo ratings yet

- Test Series: March 2023 Mock Test Paper 1 Intermediate: Group - I Paper - 1: AccountingDocument75 pagesTest Series: March 2023 Mock Test Paper 1 Intermediate: Group - I Paper - 1: AccountingKartik GuptaNo ratings yet

- Far270 July2022Document8 pagesFar270 July2022Nur Fatin AmirahNo ratings yet

- Assignment FarDocument5 pagesAssignment FarALIESYA FARHANA ALI HUSSAIN GHAZALINo ratings yet

- UOL ExamDocument11 pagesUOL ExamThant Hayman ThwayNo ratings yet

- BBF 313 Financial Reporting, Analysis and Planning: Code of The Name of The Module Date of Exam Time of Exam SetDocument4 pagesBBF 313 Financial Reporting, Analysis and Planning: Code of The Name of The Module Date of Exam Time of Exam Setkp107416No ratings yet

- 73507bos59335 Inter p1qDocument7 pages73507bos59335 Inter p1qRaish QURESHINo ratings yet

- Far270 February 22 FaDocument8 pagesFar270 February 22 FarumaisyaNo ratings yet

- Test Series: April 2023 Mock Test Paper - 2 Intermediate: Group - I Paper - 1: AccountingDocument7 pagesTest Series: April 2023 Mock Test Paper - 2 Intermediate: Group - I Paper - 1: AccountingKartik GuptaNo ratings yet

- 1 2 3 4 5 6 7 8 MergedDocument78 pages1 2 3 4 5 6 7 8 MergedKartik GuptaNo ratings yet

- CPA 1 - Financial Accounting - Paper 1dec 2022Document9 pagesCPA 1 - Financial Accounting - Paper 1dec 2022Asaba GloriaNo ratings yet

- MTP 3 14 Questions 1680520270Document7 pagesMTP 3 14 Questions 1680520270Umar MalikNo ratings yet

- CPA Paper 1 Financial Accounting 2Document9 pagesCPA Paper 1 Financial Accounting 2philipisingomaNo ratings yet

- Spring 2024 - MGT401 - 1Document3 pagesSpring 2024 - MGT401 - 1Wahab AftabNo ratings yet

- AccrDocument2 pagesAccrlearningcantstop561No ratings yet

- Case StudyDocument3 pagesCase Study203560No ratings yet

- Midterm - Far2 - AmendedDocument2 pagesMidterm - Far2 - AmendedmellNo ratings yet

- FA Dec 2021Document8 pagesFA Dec 2021Shawn LiewNo ratings yet

- FAR460 Jan 24Document8 pagesFAR460 Jan 24wan idharNo ratings yet

- Faculty Accountancy 2022 Session 1 - Diploma Far210Document8 pagesFaculty Accountancy 2022 Session 1 - Diploma Far210nafisah rahmanNo ratings yet

- MC 3 Topic 4 Def Tax Question A232Document4 pagesMC 3 Topic 4 Def Tax Question A232thanusri0103No ratings yet

- WP contentuploads202302FINANCIAL ACCOUNTING PAPER 1.1 Dec 2023 PDFDocument22 pagesWP contentuploads202302FINANCIAL ACCOUNTING PAPER 1.1 Dec 2023 PDFProsperity Thēë BwøyNo ratings yet

- Final Exam July 2021 QQDocument8 pagesFinal Exam July 2021 QQLampard AimanNo ratings yet

- FAR460 - JAN 2023 Group Assignment B Published Financial Statements Instructions To StudentsDocument5 pagesFAR460 - JAN 2023 Group Assignment B Published Financial Statements Instructions To StudentsAmniNo ratings yet

- Mba ZC415 Ec-3r First Sem 2022-2023Document4 pagesMba ZC415 Ec-3r First Sem 2022-2023Ravi KaviNo ratings yet

- Control Test 1 - March 2022Document4 pagesControl Test 1 - March 2022yandisaNo ratings yet

- Q Far270 July2021 - Set 1Document8 pagesQ Far270 July2021 - Set 1nafisah rahmanNo ratings yet

- B7AF102 2021 OMD1 First Sitting Exam PaperDocument10 pagesB7AF102 2021 OMD1 First Sitting Exam PaperAZLEA BINTI SYED HUSSIN (BG)No ratings yet

- University of Bradford Financial Accounting, Afe5008-B Final ExaminationDocument9 pagesUniversity of Bradford Financial Accounting, Afe5008-B Final ExaminationDiana TuckerNo ratings yet

- 2022 Grade 10 Controlled Test 3 QP EngDocument5 pages2022 Grade 10 Controlled Test 3 QP EngkellzylesediNo ratings yet

- Assignment Financial 2024 18TH MarchDocument6 pagesAssignment Financial 2024 18TH MarchBen Noah EuroNo ratings yet

- CAF 1 FAR1 Autumn 2022Document6 pagesCAF 1 FAR1 Autumn 2022QasimNo ratings yet

- Poa T - 12Document4 pagesPoa T - 12SHEVENA A/P VIJIANNo ratings yet

- FR Day 1Document9 pagesFR Day 1Fun DietNo ratings yet

- Corporate Reporting Nd-2022 QuestionDocument7 pagesCorporate Reporting Nd-2022 QuestionMDSadeq-ulIslamNo ratings yet

- 21NDocument22 pages21NWinnie GNo ratings yet

- Socw - 1263543589Document7 pagesSocw - 1263543589dolevov652No ratings yet

- (EN) Problem Mojakoe AK1Document11 pages(EN) Problem Mojakoe AK1gebbyNo ratings yet

- CAF 1 FAR1 Autumn 2023Document6 pagesCAF 1 FAR1 Autumn 2023z8qcsqfj8dNo ratings yet

- FAC612S - Test 3 2023Document5 pagesFAC612S - Test 3 2023simaneka.shilongoNo ratings yet

- Financial Accounting 2A Final OSA PDFDocument5 pagesFinancial Accounting 2A Final OSA PDFdamian.levendalNo ratings yet

- Shareholders' Equity p21 28Document19 pagesShareholders' Equity p21 28Rizalito SisonNo ratings yet

- Finance Assignment Due MarchDocument19 pagesFinance Assignment Due MarchJeenika S SingaravaluNo ratings yet

- CA Inter Adv Accounts Suggested Answer May 2022Document30 pagesCA Inter Adv Accounts Suggested Answer May 2022BILLU-YTNo ratings yet

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisFrom EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisNo ratings yet

- Benefit Illustration For HDFC Life Sanchay Par AdvantageDocument3 pagesBenefit Illustration For HDFC Life Sanchay Par AdvantageVamsi Krishna BNo ratings yet

- IRCTC E-Catering - Order Booked #36108741Document1 pageIRCTC E-Catering - Order Booked #36108741Debopriyo MukherjiNo ratings yet

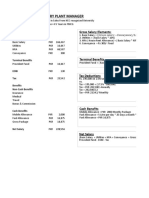

- Shoe Factory Plant Manager: Gross Salary ElementsDocument2 pagesShoe Factory Plant Manager: Gross Salary ElementsSukaina SalmanNo ratings yet

- OD225537427076154000Document1 pageOD225537427076154000Sandipan BiswasNo ratings yet

- Price List For Fiesta Homes by SJR PrimecorpDocument1 pagePrice List For Fiesta Homes by SJR PrimecorpAswath FarookNo ratings yet

- Trial Balance Ud Mudah HasilDocument1 pageTrial Balance Ud Mudah HasilSani SausanNo ratings yet

- AssignmentDocument3 pagesAssignmentDùķe HPNo ratings yet

- Invoice 197Document2 pagesInvoice 197miroljubNo ratings yet

- Basic Principles - Taxn01bDocument28 pagesBasic Principles - Taxn01bJericho PedragosaNo ratings yet

- Taxation Short Questions AnswersDocument4 pagesTaxation Short Questions AnswersSheetal IyerNo ratings yet

- Uttar Pradesh Budget Analysis 2019-20Document6 pagesUttar Pradesh Budget Analysis 2019-20AdNo ratings yet

- The VAT GuideDocument195 pagesThe VAT Guidestingray2No ratings yet

- New Tax Rates (TRAIN LAW) PDFDocument1 pageNew Tax Rates (TRAIN LAW) PDFphoebemariealhambra1475No ratings yet

- Bar Examination 2006 - TaxationlawDocument7 pagesBar Examination 2006 - TaxationlawLyraNo ratings yet

- Godrej Prana Price SheetDocument10 pagesGodrej Prana Price Sheetbigdealsin14No ratings yet

- Formst 1Document3 pagesFormst 1arulantonyNo ratings yet

- Chapter 16 Practice Problems Solution Manual 2020Document29 pagesChapter 16 Practice Problems Solution Manual 2020James SeelosNo ratings yet

- Transfer Pricing Country Profile BulgariaDocument16 pagesTransfer Pricing Country Profile BulgariaIoanna ZlatevaNo ratings yet

- Osmena vs. OrbosDocument2 pagesOsmena vs. OrbosDana Denisse RicaplazaNo ratings yet

- Od 225991033389305000Document1 pageOd 225991033389305000Iqbal khanNo ratings yet

- Synopsis of Project GSTDocument4 pagesSynopsis of Project GSTamarjeet singhNo ratings yet

- Circular CGST 199Document4 pagesCircular CGST 199Jaipur-B Gr-2No ratings yet

- Chapter 3 Charge Under GSTDocument10 pagesChapter 3 Charge Under GSTabhay javiyaNo ratings yet

- Paper4 - Taxation - MTP - All Attempts - May23Document335 pagesPaper4 - Taxation - MTP - All Attempts - May23devaaNo ratings yet

- Quote: 2215 Paseo de Las Americas Suite # 29 San Diego, CA 92154 PH# (858) 513-7748 FX# (858) 513-7757Document1 pageQuote: 2215 Paseo de Las Americas Suite # 29 San Diego, CA 92154 PH# (858) 513-7748 FX# (858) 513-7757Armenta EdwinNo ratings yet

- US Internal Revenue Service: I1040se - 1997Document5 pagesUS Internal Revenue Service: I1040se - 1997IRSNo ratings yet

- Respondent: Raja Benoy Kumar Sahas RoyDocument3 pagesRespondent: Raja Benoy Kumar Sahas RoysontineniNo ratings yet

- Complete Taxation PrelimDocument59 pagesComplete Taxation PrelimJOSHUA M. ESCOTONo ratings yet

- DATE: 19.12.2021 JOB NO: 192-9203-000 Invoice No.: 192-9203-FPC-191221Document1 pageDATE: 19.12.2021 JOB NO: 192-9203-000 Invoice No.: 192-9203-FPC-191221Mohammad MudassarNo ratings yet