Download as pdf or txt

You might also like

- 2018 INT Fraud Examiners ManualDocument14 pages2018 INT Fraud Examiners ManualKalaiyalagan Karuppiah33% (3)

- CSR and Sustainability Policy - New PDFDocument10 pagesCSR and Sustainability Policy - New PDFNaniNo ratings yet

- ASSIGNMENT LAW 2 (TASK 1) (2) BBBDocument4 pagesASSIGNMENT LAW 2 (TASK 1) (2) BBBChong Kai MingNo ratings yet

- Basic Principles of A Sound Tax SystemDocument5 pagesBasic Principles of A Sound Tax SystemCharity Joy Manayod LemieuxNo ratings yet

- CSR NotesDocument14 pagesCSR NotesMallik SVNo ratings yet

- CSR Laws and GuidelinesDocument4 pagesCSR Laws and Guidelinesanishvijay23No ratings yet

- Company CSR Policy As Per Section 135 (4) - 17012020Document5 pagesCompany CSR Policy As Per Section 135 (4) - 17012020rajesh uluwatuNo ratings yet

- CSR PolicyDocument5 pagesCSR Policyshivangicroissance2024No ratings yet

- CSR - A Panoramic View - DR Bhasker ChatterjiDocument39 pagesCSR - A Panoramic View - DR Bhasker ChatterjicodemakitNo ratings yet

- Company CSR Policy As Per Section 135 (4) - 24072018Document6 pagesCompany CSR Policy As Per Section 135 (4) - 24072018rajesh uluwatuNo ratings yet

- Corporate Social Responsibility PolicyDocument5 pagesCorporate Social Responsibility PolicyRaaj SinghNo ratings yet

- spring energyDocument6 pagesspring energyShivansh SharmaNo ratings yet

- Corporate Social ResponsibilityDocument24 pagesCorporate Social ResponsibilityNaveen MettaNo ratings yet

- CSR PPTDocument70 pagesCSR PPTbhardwajparul321No ratings yet

- Timken - Corporate-Social-Responsibility-PolicyDocument5 pagesTimken - Corporate-Social-Responsibility-Policyadi.arrow7No ratings yet

- Rar Unit 4Document12 pagesRar Unit 4raval123690No ratings yet

- ApplicabilityDocument4 pagesApplicabilityvasantharaoNo ratings yet

- Section 135 of Companies Act For Corporate Social Responsibility - TDocument3 pagesSection 135 of Companies Act For Corporate Social Responsibility - TVivek ANo ratings yet

- CSR Policy 2023-2024Document10 pagesCSR Policy 2023-2024keshnathjnpNo ratings yet

- Corporate Social Responsibility Policy: Page 1 of 9Document9 pagesCorporate Social Responsibility Policy: Page 1 of 9Darshan KannurNo ratings yet

- CSR-PPT-29 01 2020Document44 pagesCSR-PPT-29 01 2020Acs Kailash TyagiNo ratings yet

- Franklin India CSR PolicyDocument7 pagesFranklin India CSR PolicyBhomik J ShahNo ratings yet

- Corporate Social ResponsibilityDocument3 pagesCorporate Social ResponsibilityabcNo ratings yet

- Corporate Social Responsibility Under Section 135 of Companies Act 2013Document14 pagesCorporate Social Responsibility Under Section 135 of Companies Act 2013Rahul BarmanNo ratings yet

- CSR PolicyDocument12 pagesCSR Policyshivam singhNo ratings yet

- CSR PolicyDocument5 pagesCSR PolicyRitik SinghalNo ratings yet

- CSR-PPT-29 01 2020Document44 pagesCSR-PPT-29 01 2020Acs Kailash TyagiNo ratings yet

- Law Relating To Corporate Social ResponsibilityDocument12 pagesLaw Relating To Corporate Social ResponsibilityShivam RazorNo ratings yet

- 0016 Avantika Tijare Assignment 2Document4 pages0016 Avantika Tijare Assignment 2AKSHAT SINGHNo ratings yet

- 0205 - Pragati - Verma - Assignment - 2 - Pragati VermaDocument6 pages0205 - Pragati - Verma - Assignment - 2 - Pragati VermaAKSHAT SINGHNo ratings yet

- Chapter 3Document16 pagesChapter 3Mayank SenNo ratings yet

- MSL / Note On CSR (Inclusion Provisions of All Amendments Till Date) From: Secretarial & Legal Department / 11 March 2021Document11 pagesMSL / Note On CSR (Inclusion Provisions of All Amendments Till Date) From: Secretarial & Legal Department / 11 March 2021mgsalunke108No ratings yet

- Corporate Social Responsibility (Section-135) : by Akhil Kodam 20464Document24 pagesCorporate Social Responsibility (Section-135) : by Akhil Kodam 20464Kodam AkhilNo ratings yet

- 45 Shivi HalDocument4 pages45 Shivi HalKunal KaushalNo ratings yet

- CSR Project MergedDocument7 pagesCSR Project Mergedsyedsabafatima220No ratings yet

- Microsoft Word - Compliance 2021 - DSL - RevisedDocument7 pagesMicrosoft Word - Compliance 2021 - DSL - RevisedSaikatmondalNo ratings yet

- Intex Tech India LTD-CSR PolicyDocument2 pagesIntex Tech India LTD-CSR PolicyBhomik J ShahNo ratings yet

- Unitile, India - CSRDocument9 pagesUnitile, India - CSRHakimuddin GheewalaNo ratings yet

- Corporate Social ResponsibilityDocument33 pagesCorporate Social ResponsibilitySharma VishnuNo ratings yet

- DsdsdsdsdsDocument2 pagesDsdsdsdsdssuvendu beheraNo ratings yet

- CSR PolicyDocument14 pagesCSR PolicyJilla Vishwas100% (1)

- CSR Policy - BilingualDocument15 pagesCSR Policy - BilingualRanjeet DongreNo ratings yet

- CSR PolicyDocument7 pagesCSR PolicyShhanya Madan BhatiaNo ratings yet

- Preamble: Corporate Social Responsibility (CSR) Policy of Anik Industries LimitedDocument4 pagesPreamble: Corporate Social Responsibility (CSR) Policy of Anik Industries LimitedSeshangNo ratings yet

- CSR PolicyDocument8 pagesCSR PolicyKaranNo ratings yet

- CSRDocument4 pagesCSRRISHAV CHOPRANo ratings yet

- CORPORATE-SOCIAL-RESPONSIBILITY-AND-SUSTAINABILITY-POLICY-2021 Balmer LawrieDocument13 pagesCORPORATE-SOCIAL-RESPONSIBILITY-AND-SUSTAINABILITY-POLICY-2021 Balmer Lawriekusum2016thadaNo ratings yet

- Twinings CSR PolicyDocument5 pagesTwinings CSR PolicyPyramid BalerNo ratings yet

- AzureviewDocument6 pagesAzureviewshubham2904365No ratings yet

- Corporate Social Responsibility 2013Document8 pagesCorporate Social Responsibility 2013sanjeevseshannaNo ratings yet

- Warner Bros. Pictures (India) Private LimitedDocument8 pagesWarner Bros. Pictures (India) Private Limitedsaurav singhNo ratings yet

- Corporate Social Responsibility RevisedDocument12 pagesCorporate Social Responsibility RevisedVipul NarwalNo ratings yet

- Aarav CSRDocument64 pagesAarav CSRAbhay Singh ParmarNo ratings yet

- Corporate Social Responsibility PolicyDocument4 pagesCorporate Social Responsibility PolicyOMKAR PARULEKARNo ratings yet

- CSR MariottDocument7 pagesCSR MariottPrasanth KumarNo ratings yet

- CSR Policy ContentsDocument7 pagesCSR Policy Contentsvtejas842No ratings yet

- CSR Policy FinalDocument4 pagesCSR Policy FinalNaresh khandelwalNo ratings yet

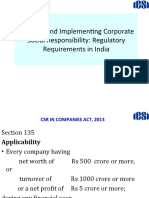

- Planning and Implementing Corporate Social Responsibility: Regulatory Requirements in IndiaDocument23 pagesPlanning and Implementing Corporate Social Responsibility: Regulatory Requirements in IndiaMuskan ManchandaNo ratings yet

- CSR Policy PDFDocument12 pagesCSR Policy PDFAkanksha DhandareNo ratings yet

- Company Law CIA III CSRDocument6 pagesCompany Law CIA III CSRVedant GoswamiNo ratings yet

- Corporate Social Responsibility - Companies Act 2013Document11 pagesCorporate Social Responsibility - Companies Act 2013Gaurav GargNo ratings yet

- rupanugabhajanashram.com-Bhagavad Gita2Document3 pagesrupanugabhajanashram.com-Bhagavad Gita2PushkarajNo ratings yet

- Highlights of (Corporate Social Responsibility Policy) Amendment Rules, 2021- taxguru.inDocument3 pagesHighlights of (Corporate Social Responsibility Policy) Amendment Rules, 2021- taxguru.inPushkarajNo ratings yet

- Form CSR-1 & related ROC Compliance- taxguru.inDocument4 pagesForm CSR-1 & related ROC Compliance- taxguru.inPushkarajNo ratings yet

- DevSectorWiseReportDocument4 pagesDevSectorWiseReportPushkarajNo ratings yet

- A brief history of Indian CSR - Gateway HouseDocument2 pagesA brief history of Indian CSR - Gateway HousePushkarajNo ratings yet

- CSR registration for Trusts _ Form CSR-1- Apply Online, FeesDocument13 pagesCSR registration for Trusts _ Form CSR-1- Apply Online, FeesPushkarajNo ratings yet

- 3.timespro.com-A Guide On How To Become A Professional Trader In India In 2024Document6 pages3.timespro.com-A Guide On How To Become A Professional Trader In India In 2024PushkarajNo ratings yet

- Food-Processing TRDocument12 pagesFood-Processing TRS on the GoNo ratings yet

- Available Commodities Listing - Feb - Kingdom Trade Group LLC, Usa - RFQDocument18 pagesAvailable Commodities Listing - Feb - Kingdom Trade Group LLC, Usa - RFQlhiuahauNo ratings yet

- 02 Munawaroh 88-99 (Fiks)Document12 pages02 Munawaroh 88-99 (Fiks)8421yahhoNo ratings yet

- American Capitalism. Running Head: Title: American Capitlism 1Document20 pagesAmerican Capitalism. Running Head: Title: American Capitlism 1ghalibhasnainNo ratings yet

- An Assessment of The Operations of Affirmative Action Reports in Namibia From 2014 To 2018Document64 pagesAn Assessment of The Operations of Affirmative Action Reports in Namibia From 2014 To 2018David MpunwaNo ratings yet

- Packing List For UCS-FI-6332 PDFDocument2 pagesPacking List For UCS-FI-6332 PDFsuperthangNo ratings yet

- Field Visit Report - CHUBASASHIDocument6 pagesField Visit Report - CHUBASASHITruth FeetNo ratings yet

- Forbes V Chuoco Tiaco and Crossfield, 16 Phil 534 1910 Civil ActionDocument2 pagesForbes V Chuoco Tiaco and Crossfield, 16 Phil 534 1910 Civil ActionRukmini Dasi Rosemary GuevaraNo ratings yet

- Law Express International Law (Stephen Allen)Document347 pagesLaw Express International Law (Stephen Allen)MujjuatharNo ratings yet

- Quiz Mas 4Document2 pagesQuiz Mas 4Cheese ButterNo ratings yet

- MSW SocialWorkCAS Professional Transcript Entry OverviewDocument1 pageMSW SocialWorkCAS Professional Transcript Entry OverviewfatimaNo ratings yet

- Dokumen - Tips 78636068 Memory Aid LaborDocument81 pagesDokumen - Tips 78636068 Memory Aid LaborRusty NomadNo ratings yet

- IMSLP532140-PMLP215828-Latour Sonatina No. 1Document7 pagesIMSLP532140-PMLP215828-Latour Sonatina No. 1Jamille MesquitaNo ratings yet

- Bhavesh's ResumeDocument1 pageBhavesh's Resumeभावेश मंगला संजय पवारNo ratings yet

- 07 Standards of Professional Conduct & Guidance-Conflicts of Interest PDFDocument11 pages07 Standards of Professional Conduct & Guidance-Conflicts of Interest PDFSardonna FongNo ratings yet

- Forms of Business OwnershipDocument26 pagesForms of Business OwnershipRitesh yadavNo ratings yet

- Class Presentation-Hire Purchase-2019-BBA-HCMDocument11 pagesClass Presentation-Hire Purchase-2019-BBA-HCMManish NepaliNo ratings yet

- Holding Period Return Formula Excel TemplateDocument3 pagesHolding Period Return Formula Excel TemplateSri VastavNo ratings yet

- Invoice - HitDocument1 pageInvoice - HitAnkit MaheshwariNo ratings yet

- (BS EN 932-5 - 2000) - Tests For General Properties of Aggregates. Common Equipment and CalibrationDocument18 pages(BS EN 932-5 - 2000) - Tests For General Properties of Aggregates. Common Equipment and CalibrationAdelNo ratings yet

- Ebook - CISSP - Domain - 01 - Security and Risk ManagementDocument202 pagesEbook - CISSP - Domain - 01 - Security and Risk ManagementroyNo ratings yet

- G.R. No. 26708 - People v. ResabalDocument4 pagesG.R. No. 26708 - People v. ResabalPam MiraflorNo ratings yet

- CON321Document4 pagesCON321Marianne CelociaNo ratings yet

- SITXFSA004-Develop and Implement A Food Safety Program - Assessment V2.0Document10 pagesSITXFSA004-Develop and Implement A Food Safety Program - Assessment V2.0sandeep kesar0% (1)

- Not Economy But Politics Is A Key To Success PDFDocument7 pagesNot Economy But Politics Is A Key To Success PDFumeerzNo ratings yet

- Virtual Work Integration TableDocument1 pageVirtual Work Integration Tablefloi dNo ratings yet

- Alabama - Interstate 65 Northbound - Cross Country RoadsDocument10 pagesAlabama - Interstate 65 Northbound - Cross Country RoadschefchadsmithNo ratings yet