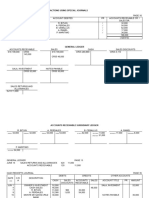

Partnership Handout Week 3

Partnership Handout Week 3

You might also like

- Unit Test 4 Answer KeyDocument1 pageUnit Test 4 Answer Keyalesenan0% (1)

- Fedex AssignmentDocument20 pagesFedex AssignmentAibak Irshad100% (2)

- Chapter 8: Admission of Partner: Rohit AgarwalDocument3 pagesChapter 8: Admission of Partner: Rohit AgarwalbcomNo ratings yet

- Ncert Sol Class 12 Accountancy Chapter 3 PDFDocument66 pagesNcert Sol Class 12 Accountancy Chapter 3 PDFAnupam DasNo ratings yet

- Module 3 - Partnership DissolutionDocument54 pagesModule 3 - Partnership DissolutionMaluDyNo ratings yet

- NCERT Solutions For Class 12 Accountancy Partnership Accounts Chapter 2Document70 pagesNCERT Solutions For Class 12 Accountancy Partnership Accounts Chapter 2ROo SonNo ratings yet

- Profit & Loss Appropriation Account, Admission, Retirement and Death of A Partner, and Dissolution of A Partnership FirmDocument10 pagesProfit & Loss Appropriation Account, Admission, Retirement and Death of A Partner, and Dissolution of A Partnership Firmd-fbuser-65596417No ratings yet

- 23 PartnershiptheoryDocument10 pages23 PartnershiptheorySanjeev MiglaniNo ratings yet

- NCERT Solutions For Class 12 Accountancy Partnership Accounts Chapter 2Document70 pagesNCERT Solutions For Class 12 Accountancy Partnership Accounts Chapter 2The stuff unlimitedNo ratings yet

- Unit V PartnershipDocument11 pagesUnit V PartnershipMUDITSAHANINo ratings yet

- Hsslive-CHAPTER 3.2 Admission of A Partner - NotesDocument8 pagesHsslive-CHAPTER 3.2 Admission of A Partner - NotesPES FOOTBALLNo ratings yet

- Accounting For Partnerships 2Document35 pagesAccounting For Partnerships 2Lazarus Henga100% (1)

- Ncert Solutions For Class 12 Accountancy 22 May Chapter 3 Reconstruction of A Partnership Firm Admission of A PartnerDocument86 pagesNcert Solutions For Class 12 Accountancy 22 May Chapter 3 Reconstruction of A Partnership Firm Admission of A PartnerHome Grown CreationNo ratings yet

- Partnership NotesDocument10 pagesPartnership NotesannabellNo ratings yet

- Accounting For Partnership - Basic ConceptsDocument19 pagesAccounting For Partnership - Basic ConceptsAashutosh PatodiaNo ratings yet

- Key Terms and Chapter Summary-3Document3 pagesKey Terms and Chapter Summary-3AbhiNo ratings yet

- Fundamantal of Partnership PPT As On 21 12 2020Document50 pagesFundamantal of Partnership PPT As On 21 12 2020jeevan varma100% (1)

- NCERT Solutions For Class 12 Accountancy Chapter 3 - Reconstitution of A Partnership Firm - Admission of A Partner - 69pDocument69 pagesNCERT Solutions For Class 12 Accountancy Chapter 3 - Reconstitution of A Partnership Firm - Admission of A Partner - 69pshanmugam PalaniappanNo ratings yet

- Detailed Handouts in Partnership DissolutionDocument14 pagesDetailed Handouts in Partnership DissolutionVinz Ray PitargueNo ratings yet

- Chapter 3 Chapter 3.admission of A Partner-1599071940612Document9 pagesChapter 3 Chapter 3.admission of A Partner-1599071940612gyannibaba2007No ratings yet

- Accountancy Chap 3 Theory NotesDocument17 pagesAccountancy Chap 3 Theory NotesRevati MenghaniNo ratings yet

- Admission of A Partner Assignment 3Document9 pagesAdmission of A Partner Assignment 3Arun KCNo ratings yet

- Accountancy Notes PDF Class 12 Chapter 3Document5 pagesAccountancy Notes PDF Class 12 Chapter 3Rishi ShibdatNo ratings yet

- 12 AccountancyDocument4 pages12 AccountancygattulokhandeNo ratings yet

- A. Retirement Notes 2023Document4 pagesA. Retirement Notes 2023Nishtha GargNo ratings yet

- Partnership Accounts PDFDocument12 pagesPartnership Accounts PDFDecereen Pineda RodriguezaNo ratings yet

- Chapterwise Theory Accounts by Sunil Panda - 240227 - 171656Document191 pagesChapterwise Theory Accounts by Sunil Panda - 240227 - 171656kawaljeetsingh121666No ratings yet

- Study MaterialDocument187 pagesStudy MaterialTanisha Tibrewal100% (1)

- Amalgamation & AbsorptionDocument11 pagesAmalgamation & AbsorptionSubhra DasNo ratings yet

- 20 Admission of PartnerDocument12 pages20 Admission of PartnerNadeem Manzoor100% (1)

- Introduction To Partnership AccountsDocument88 pagesIntroduction To Partnership Accountssaheer100% (1)

- Admission of A PartnerDocument23 pagesAdmission of A PartnerMohd Arman50% (2)

- कार्य करेंDocument199 pagesकार्य करेंkushvverma2003No ratings yet

- Document (2) AccountsDocument6 pagesDocument (2) Accountsabhishekmu95No ratings yet

- HTFA Exam 1 (Spring 2023) 2Document12 pagesHTFA Exam 1 (Spring 2023) 2AruzhanNo ratings yet

- Mediocre Non-Profit OrganizationDocument12 pagesMediocre Non-Profit OrganizationveenaNo ratings yet

- ACCOUNTANCY (CA) Answer Key Kerala +2 Annual Exam March 2020Document7 pagesACCOUNTANCY (CA) Answer Key Kerala +2 Annual Exam March 2020soumyabibin573No ratings yet

- Admission of A PartnerDocument27 pagesAdmission of A PartnerKumarNo ratings yet

- ch2 Slides InstructorDocument52 pagesch2 Slides Instructorakshitnagpal9119No ratings yet

- Accounting For: Presentation OnDocument24 pagesAccounting For: Presentation OnMonir Ahmmed Ovi50% (2)

- 12 AccountancyDocument6 pages12 AccountancygattulokhandeNo ratings yet

- POA Section 8 PartnershipsDocument26 pagesPOA Section 8 Partnershipskxng ultimateNo ratings yet

- Session 2 - Income Statement and Transaction AnalysisDocument42 pagesSession 2 - Income Statement and Transaction Analysishieucaiminh155No ratings yet

- Post Test. A12Document5 pagesPost Test. A12GICHA FEARL GIPALANo ratings yet

- Admission of PartnersDocument11 pagesAdmission of Partnerssneha sasidharanNo ratings yet

- Accounting For: Presentation OnDocument24 pagesAccounting For: Presentation OnDas ApurboNo ratings yet

- Partnership AccountsDocument4 pagesPartnership AccountsManoj Kumar GeldaNo ratings yet

- 2022 9 27 Q Merged - PagenumberDocument11 pages2022 9 27 Q Merged - PagenumberMike HKNo ratings yet

- AFAR - Partnership DissolutionDocument36 pagesAFAR - Partnership DissolutionReginald ValenciaNo ratings yet

- M.No.9818168085 Reconstitution of Partnership:: Notes On Admission of Partner Prepared By: VINEET RAJANDocument5 pagesM.No.9818168085 Reconstitution of Partnership:: Notes On Admission of Partner Prepared By: VINEET RAJANvineet_rajan100% (2)

- Lect 5 ReceivablesDocument40 pagesLect 5 Receivablesjoeltan111No ratings yet

- The Accounting Treatment of DividendsDocument5 pagesThe Accounting Treatment of DividendsVictor SantiagoNo ratings yet

- Designed Partnership Deed PresentationDocument13 pagesDesigned Partnership Deed Presentationjindalmehul03No ratings yet

- GoodwillDocument14 pagesGoodwillsandeep44% (9)

- Admission of A Partner, Class 12, CbseDocument13 pagesAdmission of A Partner, Class 12, CbseTULIP DAHIYANo ratings yet

- Accounting Olevel Theory NotesDocument7 pagesAccounting Olevel Theory NotesMujahid AmanNo ratings yet

- Nandha AccountancyDocument7 pagesNandha Accountancyrangasamibanumathi1950No ratings yet

- Unit 4 Admission of New PartnerDocument5 pagesUnit 4 Admission of New PartnerNeelabh KumarNo ratings yet

- Chapter 4 Chapter 4 Retirement or Death of A Partner 1599071952606Document10 pagesChapter 4 Chapter 4 Retirement or Death of A Partner 1599071952606gyannibaba2007No ratings yet

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 3.5 out of 5 stars3.5/5 (2)

- Liaison Officer Bookeeper Signature Over Printed Name/Date SignedDocument51 pagesLiaison Officer Bookeeper Signature Over Printed Name/Date SignedArmando LlidoNo ratings yet

- QHSE Audit Schedule: SL No Date Time Auditor Auditee DepartmentDocument2 pagesQHSE Audit Schedule: SL No Date Time Auditor Auditee DepartmentMuthusamy AyyanapillaiNo ratings yet

- Bfar Chapter 9 Answer KeyDocument2 pagesBfar Chapter 9 Answer KeyNow OnwooNo ratings yet

- Group4 PFRS15FocusnotesDocument10 pagesGroup4 PFRS15FocusnotesJohanna Nina UyNo ratings yet

- Chapter10 Solutions Hansen6eDocument17 pagesChapter10 Solutions Hansen6etccl polder39No ratings yet

- Subject Name: Business Strategy Topic Name(s) : Case Study Lecture No: 18Document11 pagesSubject Name: Business Strategy Topic Name(s) : Case Study Lecture No: 18SANKET GANDHINo ratings yet

- World Home Decor Market - Opportunities and Forecasts, 2014 - 2020Document5 pagesWorld Home Decor Market - Opportunities and Forecasts, 2014 - 2020api-311896562No ratings yet

- Module 5-Distribution MGTDocument21 pagesModule 5-Distribution MGTRevenlie GalapinNo ratings yet

- Tugas 12 - B.ING - B - WidyaNovitaDocument2 pagesTugas 12 - B.ING - B - WidyaNovitaWidya NovitaNo ratings yet

- (Ebook PDF) (Ebook PDF) Strategic Management and Competitive Advantage: Concepts and Cases Global Edition 6th Edition All ChapterDocument43 pages(Ebook PDF) (Ebook PDF) Strategic Management and Competitive Advantage: Concepts and Cases Global Edition 6th Edition All Chapterrokkiknaub100% (8)

- Pincon Spirit Limited: 37th Annual ReportDocument66 pagesPincon Spirit Limited: 37th Annual ReportSiddharth ShekharNo ratings yet

- Ifrs 15 QuestionsDocument2 pagesIfrs 15 QuestionsTata MgpNo ratings yet

- HCA PerformanceDocument9 pagesHCA PerformanceDead EyeNo ratings yet

- Asmamaw Module Edit 11 FontDocument155 pagesAsmamaw Module Edit 11 FontEdlamu AlemieNo ratings yet

- Admas University: Individual Assignment Prepare Financial ReportDocument7 pagesAdmas University: Individual Assignment Prepare Financial ReportephaNo ratings yet

- MKTG2 - Mod 1Document2 pagesMKTG2 - Mod 1ShanseaaNo ratings yet

- Accounting Applications - Part 4 - Lecture 2Document7 pagesAccounting Applications - Part 4 - Lecture 2Ahmed Mostafa ElmowafyNo ratings yet

- Porter Five (5) Forces Model: Home Writing ServicesDocument10 pagesPorter Five (5) Forces Model: Home Writing ServicesJaylen Del RosarioNo ratings yet

- Asm2 Slide BriefDocument26 pagesAsm2 Slide Briefhoattkbh01255No ratings yet

- Data Visualization Dashboard CreationDocument12 pagesData Visualization Dashboard CreationSamuel GitongaNo ratings yet

- Set B Instructions: Choose The BEST Answer For Each of The Following Items. Mark Only OneDocument15 pagesSet B Instructions: Choose The BEST Answer For Each of The Following Items. Mark Only OnePamela SantosNo ratings yet

- BPS - 5 Level of StrategiesDocument6 pagesBPS - 5 Level of StrategiesAniket YadavNo ratings yet

- Research PaperDocument33 pagesResearch PaperEnock HangwemuNo ratings yet

- Business Plan 2Document4 pagesBusiness Plan 2Zainab AshrafNo ratings yet

- 07 Franchise AccountingDocument5 pages07 Franchise AccountingAllegria AlamoNo ratings yet

- Audit of EquityDocument1 pageAudit of EquityChristine Bandigan TaladuaNo ratings yet

- Caselet - Logistics PerformaceDocument6 pagesCaselet - Logistics PerformaceNitin ShankarNo ratings yet

- Tugas Mandiri Lab. Ak. Meng 1 - PersediaanDocument9 pagesTugas Mandiri Lab. Ak. Meng 1 - PersediaanZachra MeirizaNo ratings yet

Download as docx, pdf, or txt

You might also like

- Unit Test 4 Answer KeyDocument1 pageUnit Test 4 Answer Keyalesenan0% (1)

- Fedex AssignmentDocument20 pagesFedex AssignmentAibak Irshad100% (2)

- Chapter 8: Admission of Partner: Rohit AgarwalDocument3 pagesChapter 8: Admission of Partner: Rohit AgarwalbcomNo ratings yet

- Ncert Sol Class 12 Accountancy Chapter 3 PDFDocument66 pagesNcert Sol Class 12 Accountancy Chapter 3 PDFAnupam DasNo ratings yet

- Module 3 - Partnership DissolutionDocument54 pagesModule 3 - Partnership DissolutionMaluDyNo ratings yet

- NCERT Solutions For Class 12 Accountancy Partnership Accounts Chapter 2Document70 pagesNCERT Solutions For Class 12 Accountancy Partnership Accounts Chapter 2ROo SonNo ratings yet

- Profit & Loss Appropriation Account, Admission, Retirement and Death of A Partner, and Dissolution of A Partnership FirmDocument10 pagesProfit & Loss Appropriation Account, Admission, Retirement and Death of A Partner, and Dissolution of A Partnership Firmd-fbuser-65596417No ratings yet

- 23 PartnershiptheoryDocument10 pages23 PartnershiptheorySanjeev MiglaniNo ratings yet

- NCERT Solutions For Class 12 Accountancy Partnership Accounts Chapter 2Document70 pagesNCERT Solutions For Class 12 Accountancy Partnership Accounts Chapter 2The stuff unlimitedNo ratings yet

- Unit V PartnershipDocument11 pagesUnit V PartnershipMUDITSAHANINo ratings yet

- Hsslive-CHAPTER 3.2 Admission of A Partner - NotesDocument8 pagesHsslive-CHAPTER 3.2 Admission of A Partner - NotesPES FOOTBALLNo ratings yet

- Accounting For Partnerships 2Document35 pagesAccounting For Partnerships 2Lazarus Henga100% (1)

- Ncert Solutions For Class 12 Accountancy 22 May Chapter 3 Reconstruction of A Partnership Firm Admission of A PartnerDocument86 pagesNcert Solutions For Class 12 Accountancy 22 May Chapter 3 Reconstruction of A Partnership Firm Admission of A PartnerHome Grown CreationNo ratings yet

- Partnership NotesDocument10 pagesPartnership NotesannabellNo ratings yet

- Accounting For Partnership - Basic ConceptsDocument19 pagesAccounting For Partnership - Basic ConceptsAashutosh PatodiaNo ratings yet

- Key Terms and Chapter Summary-3Document3 pagesKey Terms and Chapter Summary-3AbhiNo ratings yet

- Fundamantal of Partnership PPT As On 21 12 2020Document50 pagesFundamantal of Partnership PPT As On 21 12 2020jeevan varma100% (1)

- NCERT Solutions For Class 12 Accountancy Chapter 3 - Reconstitution of A Partnership Firm - Admission of A Partner - 69pDocument69 pagesNCERT Solutions For Class 12 Accountancy Chapter 3 - Reconstitution of A Partnership Firm - Admission of A Partner - 69pshanmugam PalaniappanNo ratings yet

- Detailed Handouts in Partnership DissolutionDocument14 pagesDetailed Handouts in Partnership DissolutionVinz Ray PitargueNo ratings yet

- Chapter 3 Chapter 3.admission of A Partner-1599071940612Document9 pagesChapter 3 Chapter 3.admission of A Partner-1599071940612gyannibaba2007No ratings yet

- Accountancy Chap 3 Theory NotesDocument17 pagesAccountancy Chap 3 Theory NotesRevati MenghaniNo ratings yet

- Admission of A Partner Assignment 3Document9 pagesAdmission of A Partner Assignment 3Arun KCNo ratings yet

- Accountancy Notes PDF Class 12 Chapter 3Document5 pagesAccountancy Notes PDF Class 12 Chapter 3Rishi ShibdatNo ratings yet

- 12 AccountancyDocument4 pages12 AccountancygattulokhandeNo ratings yet

- A. Retirement Notes 2023Document4 pagesA. Retirement Notes 2023Nishtha GargNo ratings yet

- Partnership Accounts PDFDocument12 pagesPartnership Accounts PDFDecereen Pineda RodriguezaNo ratings yet

- Chapterwise Theory Accounts by Sunil Panda - 240227 - 171656Document191 pagesChapterwise Theory Accounts by Sunil Panda - 240227 - 171656kawaljeetsingh121666No ratings yet

- Study MaterialDocument187 pagesStudy MaterialTanisha Tibrewal100% (1)

- Amalgamation & AbsorptionDocument11 pagesAmalgamation & AbsorptionSubhra DasNo ratings yet

- 20 Admission of PartnerDocument12 pages20 Admission of PartnerNadeem Manzoor100% (1)

- Introduction To Partnership AccountsDocument88 pagesIntroduction To Partnership Accountssaheer100% (1)

- Admission of A PartnerDocument23 pagesAdmission of A PartnerMohd Arman50% (2)

- कार्य करेंDocument199 pagesकार्य करेंkushvverma2003No ratings yet

- Document (2) AccountsDocument6 pagesDocument (2) Accountsabhishekmu95No ratings yet

- HTFA Exam 1 (Spring 2023) 2Document12 pagesHTFA Exam 1 (Spring 2023) 2AruzhanNo ratings yet

- Mediocre Non-Profit OrganizationDocument12 pagesMediocre Non-Profit OrganizationveenaNo ratings yet

- ACCOUNTANCY (CA) Answer Key Kerala +2 Annual Exam March 2020Document7 pagesACCOUNTANCY (CA) Answer Key Kerala +2 Annual Exam March 2020soumyabibin573No ratings yet

- Admission of A PartnerDocument27 pagesAdmission of A PartnerKumarNo ratings yet

- ch2 Slides InstructorDocument52 pagesch2 Slides Instructorakshitnagpal9119No ratings yet

- Accounting For: Presentation OnDocument24 pagesAccounting For: Presentation OnMonir Ahmmed Ovi50% (2)

- 12 AccountancyDocument6 pages12 AccountancygattulokhandeNo ratings yet

- POA Section 8 PartnershipsDocument26 pagesPOA Section 8 Partnershipskxng ultimateNo ratings yet

- Session 2 - Income Statement and Transaction AnalysisDocument42 pagesSession 2 - Income Statement and Transaction Analysishieucaiminh155No ratings yet

- Post Test. A12Document5 pagesPost Test. A12GICHA FEARL GIPALANo ratings yet

- Admission of PartnersDocument11 pagesAdmission of Partnerssneha sasidharanNo ratings yet

- Accounting For: Presentation OnDocument24 pagesAccounting For: Presentation OnDas ApurboNo ratings yet

- Partnership AccountsDocument4 pagesPartnership AccountsManoj Kumar GeldaNo ratings yet

- 2022 9 27 Q Merged - PagenumberDocument11 pages2022 9 27 Q Merged - PagenumberMike HKNo ratings yet

- AFAR - Partnership DissolutionDocument36 pagesAFAR - Partnership DissolutionReginald ValenciaNo ratings yet

- M.No.9818168085 Reconstitution of Partnership:: Notes On Admission of Partner Prepared By: VINEET RAJANDocument5 pagesM.No.9818168085 Reconstitution of Partnership:: Notes On Admission of Partner Prepared By: VINEET RAJANvineet_rajan100% (2)

- Lect 5 ReceivablesDocument40 pagesLect 5 Receivablesjoeltan111No ratings yet

- The Accounting Treatment of DividendsDocument5 pagesThe Accounting Treatment of DividendsVictor SantiagoNo ratings yet

- Designed Partnership Deed PresentationDocument13 pagesDesigned Partnership Deed Presentationjindalmehul03No ratings yet

- GoodwillDocument14 pagesGoodwillsandeep44% (9)

- Admission of A Partner, Class 12, CbseDocument13 pagesAdmission of A Partner, Class 12, CbseTULIP DAHIYANo ratings yet

- Accounting Olevel Theory NotesDocument7 pagesAccounting Olevel Theory NotesMujahid AmanNo ratings yet

- Nandha AccountancyDocument7 pagesNandha Accountancyrangasamibanumathi1950No ratings yet

- Unit 4 Admission of New PartnerDocument5 pagesUnit 4 Admission of New PartnerNeelabh KumarNo ratings yet

- Chapter 4 Chapter 4 Retirement or Death of A Partner 1599071952606Document10 pagesChapter 4 Chapter 4 Retirement or Death of A Partner 1599071952606gyannibaba2007No ratings yet

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 3.5 out of 5 stars3.5/5 (2)

- Liaison Officer Bookeeper Signature Over Printed Name/Date SignedDocument51 pagesLiaison Officer Bookeeper Signature Over Printed Name/Date SignedArmando LlidoNo ratings yet

- QHSE Audit Schedule: SL No Date Time Auditor Auditee DepartmentDocument2 pagesQHSE Audit Schedule: SL No Date Time Auditor Auditee DepartmentMuthusamy AyyanapillaiNo ratings yet

- Bfar Chapter 9 Answer KeyDocument2 pagesBfar Chapter 9 Answer KeyNow OnwooNo ratings yet

- Group4 PFRS15FocusnotesDocument10 pagesGroup4 PFRS15FocusnotesJohanna Nina UyNo ratings yet

- Chapter10 Solutions Hansen6eDocument17 pagesChapter10 Solutions Hansen6etccl polder39No ratings yet

- Subject Name: Business Strategy Topic Name(s) : Case Study Lecture No: 18Document11 pagesSubject Name: Business Strategy Topic Name(s) : Case Study Lecture No: 18SANKET GANDHINo ratings yet

- World Home Decor Market - Opportunities and Forecasts, 2014 - 2020Document5 pagesWorld Home Decor Market - Opportunities and Forecasts, 2014 - 2020api-311896562No ratings yet

- Module 5-Distribution MGTDocument21 pagesModule 5-Distribution MGTRevenlie GalapinNo ratings yet

- Tugas 12 - B.ING - B - WidyaNovitaDocument2 pagesTugas 12 - B.ING - B - WidyaNovitaWidya NovitaNo ratings yet

- (Ebook PDF) (Ebook PDF) Strategic Management and Competitive Advantage: Concepts and Cases Global Edition 6th Edition All ChapterDocument43 pages(Ebook PDF) (Ebook PDF) Strategic Management and Competitive Advantage: Concepts and Cases Global Edition 6th Edition All Chapterrokkiknaub100% (8)

- Pincon Spirit Limited: 37th Annual ReportDocument66 pagesPincon Spirit Limited: 37th Annual ReportSiddharth ShekharNo ratings yet

- Ifrs 15 QuestionsDocument2 pagesIfrs 15 QuestionsTata MgpNo ratings yet

- HCA PerformanceDocument9 pagesHCA PerformanceDead EyeNo ratings yet

- Asmamaw Module Edit 11 FontDocument155 pagesAsmamaw Module Edit 11 FontEdlamu AlemieNo ratings yet

- Admas University: Individual Assignment Prepare Financial ReportDocument7 pagesAdmas University: Individual Assignment Prepare Financial ReportephaNo ratings yet

- MKTG2 - Mod 1Document2 pagesMKTG2 - Mod 1ShanseaaNo ratings yet

- Accounting Applications - Part 4 - Lecture 2Document7 pagesAccounting Applications - Part 4 - Lecture 2Ahmed Mostafa ElmowafyNo ratings yet

- Porter Five (5) Forces Model: Home Writing ServicesDocument10 pagesPorter Five (5) Forces Model: Home Writing ServicesJaylen Del RosarioNo ratings yet

- Asm2 Slide BriefDocument26 pagesAsm2 Slide Briefhoattkbh01255No ratings yet

- Data Visualization Dashboard CreationDocument12 pagesData Visualization Dashboard CreationSamuel GitongaNo ratings yet

- Set B Instructions: Choose The BEST Answer For Each of The Following Items. Mark Only OneDocument15 pagesSet B Instructions: Choose The BEST Answer For Each of The Following Items. Mark Only OnePamela SantosNo ratings yet

- BPS - 5 Level of StrategiesDocument6 pagesBPS - 5 Level of StrategiesAniket YadavNo ratings yet

- Research PaperDocument33 pagesResearch PaperEnock HangwemuNo ratings yet

- Business Plan 2Document4 pagesBusiness Plan 2Zainab AshrafNo ratings yet

- 07 Franchise AccountingDocument5 pages07 Franchise AccountingAllegria AlamoNo ratings yet

- Audit of EquityDocument1 pageAudit of EquityChristine Bandigan TaladuaNo ratings yet

- Caselet - Logistics PerformaceDocument6 pagesCaselet - Logistics PerformaceNitin ShankarNo ratings yet

- Tugas Mandiri Lab. Ak. Meng 1 - PersediaanDocument9 pagesTugas Mandiri Lab. Ak. Meng 1 - PersediaanZachra MeirizaNo ratings yet