Download as pdf or txt

You might also like

- Topographic Maps: Use The Following Hiking Map From Enchanted Rock To Complete The Following QuestionsDocument3 pagesTopographic Maps: Use The Following Hiking Map From Enchanted Rock To Complete The Following QuestionsVinujah Sukumaran50% (4)

- Government Departments Contact Emails/Phone Numbers EtcDocument149 pagesGovernment Departments Contact Emails/Phone Numbers EtcPaul Smith0% (1)

- vxBjICCrQ7eQYyAgq0O3cg - Debit Credit Rules ActivityDocument1 pagevxBjICCrQ7eQYyAgq0O3cg - Debit Credit Rules ActivityAlok PatilNo ratings yet

- 2 Material HandlingDocument218 pages2 Material HandlingJon Blac100% (1)

- Cambridge International AS & A Level: Accounting 9706/21 October/November 2021Document13 pagesCambridge International AS & A Level: Accounting 9706/21 October/November 2021babarmumtaz1962No ratings yet

- Cambridge O Level: Accounting 7707/22 October/November 2021Document15 pagesCambridge O Level: Accounting 7707/22 October/November 2021FarrukhsgNo ratings yet

- Cambridge IGCSE™: Accounting 0452/22 October/November 2021Document15 pagesCambridge IGCSE™: Accounting 0452/22 October/November 2021Mohammed ZakeeNo ratings yet

- Cambridge O Level: Accounting 7707/22 October/November 2022Document16 pagesCambridge O Level: Accounting 7707/22 October/November 2022Marlene BandaNo ratings yet

- Cambridge O Level: Accounting 7707/24 May/June 2021Document17 pagesCambridge O Level: Accounting 7707/24 May/June 2021Hashir ShaheerNo ratings yet

- Cambridge O Level: Accounting 7707/23 October/November 2021Document17 pagesCambridge O Level: Accounting 7707/23 October/November 2021jeetenjsrNo ratings yet

- Cambridge International AS & A Level: Accounting 9706/32 March 2021Document19 pagesCambridge International AS & A Level: Accounting 9706/32 March 2021Ahmed NaserNo ratings yet

- Cambridge O Level: Accounting 7707/23 October/November 2022Document18 pagesCambridge O Level: Accounting 7707/23 October/November 2022FahadNo ratings yet

- Cambridge IGCSE™: Accounting 0452/23 October/November 2021Document17 pagesCambridge IGCSE™: Accounting 0452/23 October/November 2021Mohammed ZakeeNo ratings yet

- Cambridge International AS & A Level: Accounting 9706/31 October/November 2022Document17 pagesCambridge International AS & A Level: Accounting 9706/31 October/November 2022ryan valtrainNo ratings yet

- Cambridge IGCSE ™: Accounting 0452/22 October/November 2022Document16 pagesCambridge IGCSE ™: Accounting 0452/22 October/November 2022Sean RusikeNo ratings yet

- Cambridge International AS & A Level: Accounting 9706/21 May/June 2021Document15 pagesCambridge International AS & A Level: Accounting 9706/21 May/June 2021fa22msmg0011No ratings yet

- Cambridge International AS & A Level: Accounting 9706/32 October/November 2022Document22 pagesCambridge International AS & A Level: Accounting 9706/32 October/November 2022alanmuchenjeNo ratings yet

- Cambridge IGCSE™: Accounting 0452/23 May/June 2021Document16 pagesCambridge IGCSE™: Accounting 0452/23 May/June 2021Sana IbrahimNo ratings yet

- Cambridge IGCSE™: Economics 0455/22 October/November 2021Document24 pagesCambridge IGCSE™: Economics 0455/22 October/November 2021Mohammed ZakeeNo ratings yet

- Cambridge International AS & A Level: Accounting 9706/21 October/November 2022Document17 pagesCambridge International AS & A Level: Accounting 9706/21 October/November 2022damiangoromonziiNo ratings yet

- Cambridge O Level: Economics 2281/22 October/November 2022Document24 pagesCambridge O Level: Economics 2281/22 October/November 2022FahadNo ratings yet

- Cambridge O Level: Commerce 7100/21 October/November 2021Document18 pagesCambridge O Level: Commerce 7100/21 October/November 2021Abu IbrahimNo ratings yet

- Cambridge IGCSE ™: Accounting 0452/21 October/November 2022Document18 pagesCambridge IGCSE ™: Accounting 0452/21 October/November 2022Muhammad AhmadNo ratings yet

- Cambridge IGCSE™: Accounting 0452/21 May/June 2021Document20 pagesCambridge IGCSE™: Accounting 0452/21 May/June 2021nokutenda zindereNo ratings yet

- Cambridge IGCSE™: Business Studies 0450/13 October/November 2021Document24 pagesCambridge IGCSE™: Business Studies 0450/13 October/November 2021econearthNo ratings yet

- Cambridge International AS & A Level: EconomicsDocument15 pagesCambridge International AS & A Level: EconomicsAndrew BadgerNo ratings yet

- Cambridge O Level: Economics 2281/21 May/June 2021Document26 pagesCambridge O Level: Economics 2281/21 May/June 2021FahadNo ratings yet

- Paper 1 Marking SchemeDocument22 pagesPaper 1 Marking SchemeHussain ShaikhNo ratings yet

- Cambridge O Level: Commerce 7100/22 October/November 2021Document19 pagesCambridge O Level: Commerce 7100/22 October/November 2021Sadia afrinNo ratings yet

- Cambridge International AS & A Level: Economics 9708/23 October/November 2022Document15 pagesCambridge International AS & A Level: Economics 9708/23 October/November 2022Andrew BadgerNo ratings yet

- Cambridge IGCSE™: Accounting 0452/23 October/November 2021Document17 pagesCambridge IGCSE™: Accounting 0452/23 October/November 2021Iron OneNo ratings yet

- Cambridge IGCSE ™: Business Studies 0450/12 October/November 2022Document21 pagesCambridge IGCSE ™: Business Studies 0450/12 October/November 2022Katlego MedupeNo ratings yet

- Cambridge IGCSE™: Accounting 0452/22 February/March 2022Document17 pagesCambridge IGCSE™: Accounting 0452/22 February/March 2022Janvi JainNo ratings yet

- Cambridge O Level: Accounting 7707/22 May/June 2022Document16 pagesCambridge O Level: Accounting 7707/22 May/June 2022Kutwaroo GayetreeNo ratings yet

- Cambridge O Level: Business Studies 7115/12 October/November 2022Document21 pagesCambridge O Level: Business Studies 7115/12 October/November 2022MsuBrainBoxNo ratings yet

- Cambridge International AS & A Level: Economics 9708/22 February/March 2022Document12 pagesCambridge International AS & A Level: Economics 9708/22 February/March 2022Andrew BadgerNo ratings yet

- Cambridge O Level: Commerce 7100/22 October/November 2022Document24 pagesCambridge O Level: Commerce 7100/22 October/November 2022Tapiwa MT (N1c3isH)No ratings yet

- Cambridge International AS & A Level: Economics 9708/21 May/June 2021Document14 pagesCambridge International AS & A Level: Economics 9708/21 May/June 2021Đoàn DũngNo ratings yet

- Cambridge International AS & A Level: Global Perspectives and Research 9239/11 May/June 2021Document21 pagesCambridge International AS & A Level: Global Perspectives and Research 9239/11 May/June 2021Hassan AsadullahNo ratings yet

- Cambridge IGCSE™: Economics 0455/23 October/November 2021Document28 pagesCambridge IGCSE™: Economics 0455/23 October/November 2021Mohammed ZakeeNo ratings yet

- Cambridge IGCSE™: Business Studies 0450/11 October/November 2021Document22 pagesCambridge IGCSE™: Business Studies 0450/11 October/November 2021Callum BirdNo ratings yet

- Feb March 2021 (22) - ADocument12 pagesFeb March 2021 (22) - AMarie Xavier - FelixNo ratings yet

- Cambridge O Level: Business Studies 7115/14 October/November 2022Document22 pagesCambridge O Level: Business Studies 7115/14 October/November 2022Adeela WaqasNo ratings yet

- Cambridge IGCSE™: Accounting 0452/22 March 2021Document19 pagesCambridge IGCSE™: Accounting 0452/22 March 2021Farrukhsg50% (2)

- Cambridge IGCSE™: Business Studies 0450/11 May/June 2021Document21 pagesCambridge IGCSE™: Business Studies 0450/11 May/June 2021Imran Ali100% (1)

- Cambridge O Level: Business Studies 7115/11 May/June 2021Document21 pagesCambridge O Level: Business Studies 7115/11 May/June 2021nayna sharminNo ratings yet

- Cambridge International AS & A Level: Mathematics 9709/13 October/November 2021Document15 pagesCambridge International AS & A Level: Mathematics 9709/13 October/November 2021Robert mukwekweNo ratings yet

- Cambridge International AS & A Level: Accounting 9706/31 October/November 2021Document16 pagesCambridge International AS & A Level: Accounting 9706/31 October/November 2021AB YUNo ratings yet

- Cambridge International AS & A Level: Mathematics 9709/61 October/November 2021Document11 pagesCambridge International AS & A Level: Mathematics 9709/61 October/November 2021Mubashir AsifNo ratings yet

- 9708 w22 Ms 41 PDFDocument16 pages9708 w22 Ms 41 PDFTawanda MakombeNo ratings yet

- November 2021 (v1) MSDocument15 pagesNovember 2021 (v1) MSJesmond TayNo ratings yet

- Cambridge International AS & A Level: Physics 9702/43 October/November 2021Document15 pagesCambridge International AS & A Level: Physics 9702/43 October/November 2021pvaidehi9826No ratings yet

- Cambridge International A Level: Mathematics 9709/31 October/November 2022Document17 pagesCambridge International A Level: Mathematics 9709/31 October/November 2022Wilber TuryasiimaNo ratings yet

- Cambridge IGCSE™: Accounting 0452/23 May/June 2022Document16 pagesCambridge IGCSE™: Accounting 0452/23 May/June 2022Lavanya GoleNo ratings yet

- Cambridge IGCSE™: Business Studies 0450/12 March 2021Document24 pagesCambridge IGCSE™: Business Studies 0450/12 March 2021Wilfred BryanNo ratings yet

- Cambridge IGCSE™: Business Studies 0450/12 March 2021Document24 pagesCambridge IGCSE™: Business Studies 0450/12 March 2021Kausika ThanarajNo ratings yet

- Cambridge International AS & A Level: BusinessDocument21 pagesCambridge International AS & A Level: BusinessEldo PappuNo ratings yet

- Cambridge International AS & A Level: Further Mathematics 9231/41 October/November 2021Document14 pagesCambridge International AS & A Level: Further Mathematics 9231/41 October/November 2021Areeba ImranNo ratings yet

- Cambridge International A Level: Further Mathematics 9231/23 October/November 2020Document15 pagesCambridge International A Level: Further Mathematics 9231/23 October/November 2020Shehzad AslamNo ratings yet

- Cambridge International AS & A Level: Business 9609/22 March 2021Document16 pagesCambridge International AS & A Level: Business 9609/22 March 2021LisaNo ratings yet

- Cambridge International AS & A Level: Mathematics 9709/12 March 2021Document14 pagesCambridge International AS & A Level: Mathematics 9709/12 March 2021JuanaNo ratings yet

- Cambridge International AS & A Level: Mathematics 9709/11 October/November 2021Document19 pagesCambridge International AS & A Level: Mathematics 9709/11 October/November 2021JuniorNo ratings yet

- Cambridge IGCSE ™ (9-1) : Business Studies 0986/21 October/November 2022Document22 pagesCambridge IGCSE ™ (9-1) : Business Studies 0986/21 October/November 2022YahiaNo ratings yet

- Competency-Based Accounting Education, Training, and Certification: An Implementation GuideFrom EverandCompetency-Based Accounting Education, Training, and Certification: An Implementation GuideNo ratings yet

- Self - Assessment Guide: Can I? YES NODocument3 pagesSelf - Assessment Guide: Can I? YES NOJohn Castillo100% (1)

- Business Law Cpa Board Exam Lecture Notes: I. (CO, NO)Document27 pagesBusiness Law Cpa Board Exam Lecture Notes: I. (CO, NO)Shin MelodyNo ratings yet

- HahayysDocument30 pagesHahayys2BGrp3Plaza, Anna MaeNo ratings yet

- The Impact of Different Political Beliefs On The Family Relationship of College-StudentsDocument16 pagesThe Impact of Different Political Beliefs On The Family Relationship of College-Studentshue sandovalNo ratings yet

- Mesina V Meer PDFDocument3 pagesMesina V Meer PDFColee StiflerNo ratings yet

- Complete ModuleDocument99 pagesComplete ModuleMhel DemabogteNo ratings yet

- Answer: The Measure of The Central Angles of An Equilateral TriangleDocument4 pagesAnswer: The Measure of The Central Angles of An Equilateral Trianglesunil_ibmNo ratings yet

- For StatDocument47 pagesFor StatLyn VeaNo ratings yet

- Input Filter Design by EricksonDocument49 pagesInput Filter Design by EricksonshrikrisNo ratings yet

- Law and IT Assignment SEM IXDocument18 pagesLaw and IT Assignment SEM IXrenu tomarNo ratings yet

- PethaDocument4 pagesPethaJeet RajNo ratings yet

- Database Teach IctDocument3 pagesDatabase Teach IctMushawatuNo ratings yet

- Zxdaw 3Document56 pagesZxdaw 3kingNo ratings yet

- Computer Information SystemDocument5 pagesComputer Information SystemAmandaNo ratings yet

- Magnetic Systems Specific Heat$Document13 pagesMagnetic Systems Specific Heat$andres arizaNo ratings yet

- Ebook Contemporary Issues in Accounting 2Nd Edition Rankin Solutions Manual Full Chapter PDFDocument53 pagesEbook Contemporary Issues in Accounting 2Nd Edition Rankin Solutions Manual Full Chapter PDFfideliamaximilian7pjjf100% (11)

- Care of Dying and DeadDocument10 pagesCare of Dying and Deadd1choosenNo ratings yet

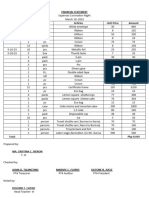

- Financial Statement Coronation NightDocument8 pagesFinancial Statement Coronation NightRuel Gapuz ManzanoNo ratings yet

- 1 A-2 Mann - Concept of Infrastructural PowerDocument11 pages1 A-2 Mann - Concept of Infrastructural Powerrichiflowers11gmail.comNo ratings yet

- Mathematics: Quarter 3 - Module 5: Independent & Dependent EventsDocument19 pagesMathematics: Quarter 3 - Module 5: Independent & Dependent EventsAlexis Jon NaingueNo ratings yet

- Boreal Forests Canadian Shield Tundra Arctic Canadian Rockies Coast Mountains Prairies Great Lakes St. Lawrence RiverDocument2 pagesBoreal Forests Canadian Shield Tundra Arctic Canadian Rockies Coast Mountains Prairies Great Lakes St. Lawrence Riversaikiran100No ratings yet

- Quasi JudicialDocument2 pagesQuasi JudicialMich Angeles100% (1)

- Palanca vs. CADocument16 pagesPalanca vs. CASherwin Anoba CabutijaNo ratings yet

- Lap Trình KeyenceDocument676 pagesLap Trình Keyencetuand1No ratings yet

- Week 8 Assignment SiriDocument8 pagesWeek 8 Assignment SiriSiri ReddyNo ratings yet

- Weight Tracking Chartv2 365days WeeklyDocument20 pagesWeight Tracking Chartv2 365days WeeklyozgegizemNo ratings yet