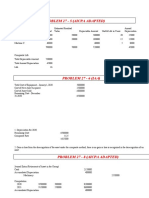

624977550-30-5-to-30-6-Depletion-Intermediate-Accounting-Volume-1-2021-Edition-Valix

624977550-30-5-to-30-6-Depletion-Intermediate-Accounting-Volume-1-2021-Edition-Valix

You might also like

- SPC 3rd Edition EnglishDocument233 pagesSPC 3rd Edition Englishdhillon63No ratings yet

- Opm TQM Course Syllabus Bsa BsaisDocument9 pagesOpm TQM Course Syllabus Bsa BsaisPeachyNo ratings yet

- Accounting Part 2: Problem SolvingDocument10 pagesAccounting Part 2: Problem Solvingnd555No ratings yet

- PPE Government Grant Borrowing Cost Intangible AssetsDocument7 pagesPPE Government Grant Borrowing Cost Intangible AssetsLian Garl100% (4)

- Intermediate Accounting 1 - Chapter 15, Financial Assets at Fair ValueDocument8 pagesIntermediate Accounting 1 - Chapter 15, Financial Assets at Fair ValueAndrei FajardoNo ratings yet

- Chapter 18 - Investment in Associate 2 PDFDocument15 pagesChapter 18 - Investment in Associate 2 PDFTurksNo ratings yet

- Problem 23-7 and 23-8Document2 pagesProblem 23-7 and 23-8Maria LicuananNo ratings yet

- Intacc FinalsDocument81 pagesIntacc FinalsargoNo ratings yet

- 7 3 BuenaventuraDocument2 pages7 3 BuenaventuraAnonnNo ratings yet

- Chapter 13 - Gross Profit MethodDocument2 pagesChapter 13 - Gross Profit MethodBena CubillasNo ratings yet

- IA 1 Valix 2020 Ver. Problem 27-5 - Problem 27-7Document2 pagesIA 1 Valix 2020 Ver. Problem 27-5 - Problem 27-7Ariean Joy DequiñaNo ratings yet

- Ppe Borrowing Cost July 12 SummerDocument12 pagesPpe Borrowing Cost July 12 SummerJelyn RuazolNo ratings yet

- Sol. Man. - Chapter 17 - Depletion of Mineral Resources - Ia Part 1BDocument3 pagesSol. Man. - Chapter 17 - Depletion of Mineral Resources - Ia Part 1BMahasia MANDIGANNo ratings yet

- Test - Financial PlanningDocument3 pagesTest - Financial PlanningMasTer PanDaNo ratings yet

- Revaluation-Accounting CompressDocument13 pagesRevaluation-Accounting CompressEunice Buenaventura100% (1)

- 21 Financial Assets at Fair Value: Solution 21-1 Answer CDocument30 pages21 Financial Assets at Fair Value: Solution 21-1 Answer CLayNo ratings yet

- Chapter 33Document7 pagesChapter 33Shane Ivory ClaudioNo ratings yet

- Group 1 - Chapter 16Document8 pagesGroup 1 - Chapter 16Cherie Soriano AnanayoNo ratings yet

- Depletion 5Document1 pageDepletion 5Paula Mae DacanayNo ratings yet

- ACC 102.key Answer - Quiz 1.inventoriesDocument5 pagesACC 102.key Answer - Quiz 1.inventoriesMa. Lou Erika BALITENo ratings yet

- Charisma Company Required 1 Date Interest Received Interest Income Discount Amortization Carrying AmountDocument2 pagesCharisma Company Required 1 Date Interest Received Interest Income Discount Amortization Carrying AmountAnonnNo ratings yet

- Seatwork Module 10Document3 pagesSeatwork Module 10Marjorie PalmaNo ratings yet

- Flexible Company Debit Credit 2020Document1 pageFlexible Company Debit Credit 2020AnonnNo ratings yet

- Chapter 16Document10 pagesChapter 16GONZALES, MICA ANGEL A.No ratings yet

- Land and BuildingDocument5 pagesLand and BuildingDianna DayawonNo ratings yet

- Chapter 7Document18 pagesChapter 7Raven Vargas DayritNo ratings yet

- Investment in Equity Securities - Problem 16-2, 16-3, 16-10. and 16-11Document6 pagesInvestment in Equity Securities - Problem 16-2, 16-3, 16-10. and 16-11Jessie Dela CruzNo ratings yet

- Financial Asset at Amortized CostDocument4 pagesFinancial Asset at Amortized CostXNo ratings yet

- IA 2 Chapter 5 ActivitiesDocument12 pagesIA 2 Chapter 5 ActivitiesShaina TorraineNo ratings yet

- AC13 Provisions, Contingencies and Other Liabilities Additional Guide ProblemsDocument2 pagesAC13 Provisions, Contingencies and Other Liabilities Additional Guide ProblemsDianaNo ratings yet

- Intermediate Accounting Chapter 23 To 35Document101 pagesIntermediate Accounting Chapter 23 To 35Blue SkyNo ratings yet

- This Study Resource Was Shared Via: Solution 23-2 Answer DDocument5 pagesThis Study Resource Was Shared Via: Solution 23-2 Answer DDummy GoogleNo ratings yet

- Chapter 48: ProvisionDocument8 pagesChapter 48: ProvisionjsemlpzNo ratings yet

- Padernal BSA 1A SW Problem 3 11Document1 pagePadernal BSA 1A SW Problem 3 11Fly ThoughtsNo ratings yet

- Problem 2 8Document6 pagesProblem 2 8Carl Jaime Dela CruzNo ratings yet

- Machinery VergaraDocument10 pagesMachinery VergaraDarlianne Klyne BayerNo ratings yet

- Chapter 18Document34 pagesChapter 18Christine Marie T. RamirezNo ratings yet

- ASC Partnership Schedule of Safe PaymentsDocument3 pagesASC Partnership Schedule of Safe PaymentsMayaNo ratings yet

- Pre2 Module-Intangible Assets: Learning ObjectivesDocument9 pagesPre2 Module-Intangible Assets: Learning ObjectivesCyrine Grace DucogNo ratings yet

- Practice Set Review - Current LiabilitiesDocument12 pagesPractice Set Review - Current LiabilitiesKayla MirandaNo ratings yet

- Chapter 20Document13 pagesChapter 20Bella RonahNo ratings yet

- Group Activity Mina HanDocument4 pagesGroup Activity Mina HanLevi's DishwasherNo ratings yet

- Borrowing Cost (PAS 23)Document6 pagesBorrowing Cost (PAS 23)CharléNo ratings yet

- Precious Grace Ann R. Loja IA1 April 13, 2020: Initial Measurement of Loan ReceivableDocument6 pagesPrecious Grace Ann R. Loja IA1 April 13, 2020: Initial Measurement of Loan Receivableprecious2lojaNo ratings yet

- Basic Concepts Revenue Cycle: List Price, Trade Discount, Prepaid Freight, Cash DiscountDocument50 pagesBasic Concepts Revenue Cycle: List Price, Trade Discount, Prepaid Freight, Cash DiscountJean MaeNo ratings yet

- IA2 Worksheet-BONDS PAYABLE - 101010Document11 pagesIA2 Worksheet-BONDS PAYABLE - 101010aehy lznuscrfbjNo ratings yet

- Lobrigas Unit3 Topic1 AssessmentDocument9 pagesLobrigas Unit3 Topic1 AssessmentClaudine LobrigasNo ratings yet

- T-Test One SampleDocument5 pagesT-Test One SampleJessa Delos SantosNo ratings yet

- Problem 7 - 6 & 7Document2 pagesProblem 7 - 6 & 7Micah April SabularseNo ratings yet

- 1Document20 pages1Denver AcenasNo ratings yet

- EXAMINATION ON INVENTORY MaDocument5 pagesEXAMINATION ON INVENTORY Macriszel4sobejanaNo ratings yet

- ACC 121 Chapter 55Document4 pagesACC 121 Chapter 55Mohammad saripNo ratings yet

- Chapter22 BuenaventuraDocument4 pagesChapter22 BuenaventuraAnonnNo ratings yet

- MachineryDocument4 pagesMachineryDianna DayawonNo ratings yet

- Intacc 3 Leases FinalsDocument9 pagesIntacc 3 Leases FinalsDarryl AgustinNo ratings yet

- Sale and LeasebackDocument10 pagesSale and LeasebackShinny Jewel VingnoNo ratings yet

- Chap16 ProblemsDocument20 pagesChap16 ProblemsYen YenNo ratings yet

- Land Building Machinery ProblemsDocument13 pagesLand Building Machinery ProblemsJomerNo ratings yet

- Draft A90Document7 pagesDraft A90Jewel Mae MercadoNo ratings yet

- FAR04-08 - Government Grant & Borrowing CostsDocument7 pagesFAR04-08 - Government Grant & Borrowing CostsAi NatangcopNo ratings yet

- Answer Key For Strategic Cost Management - CompressDocument19 pagesAnswer Key For Strategic Cost Management - CompressMikee RizonNo ratings yet

- CPAR B94 FAR Final PB Exam - Answers - SolutionsDocument8 pagesCPAR B94 FAR Final PB Exam - Answers - SolutionsJazehl ValdezNo ratings yet

- Prof Ed 2 M2, L2Document3 pagesProf Ed 2 M2, L2Away To PonderNo ratings yet

- Edited Module - Docx August 25 2020Document206 pagesEdited Module - Docx August 25 2020Away To PonderNo ratings yet

- ACCT104 Prelim Exam 38 47Document2 pagesACCT104 Prelim Exam 38 47Away To PonderNo ratings yet

- Content No. 07 Bank Reconciliation StatementDocument3 pagesContent No. 07 Bank Reconciliation StatementAway To PonderNo ratings yet

- Content No. 06 Basic Documents and Transactions Related To Bank DepositsDocument3 pagesContent No. 06 Basic Documents and Transactions Related To Bank DepositsAway To PonderNo ratings yet

- Solutions To 2 1 To 2 5Document5 pagesSolutions To 2 1 To 2 5Away To PonderNo ratings yet

- ACCT104 Quizzes SolutionsDocument2 pagesACCT104 Quizzes SolutionsAway To PonderNo ratings yet

- ACCT105 Quiz 02 and 03 Prelim SolutionDocument3 pagesACCT105 Quiz 02 and 03 Prelim SolutionAway To PonderNo ratings yet

- ACCT105 Quizzes and SolutionsDocument8 pagesACCT105 Quizzes and SolutionsAway To PonderNo ratings yet

- 30 1 To 30 4Document2 pages30 1 To 30 4Away To PonderNo ratings yet

- Binalbagan Catholic College: Course Guide Science, Technology and Society (STS)Document5 pagesBinalbagan Catholic College: Course Guide Science, Technology and Society (STS)Away To PonderNo ratings yet

- 31 1 To 31 4Document2 pages31 1 To 31 4Away To PonderNo ratings yet

- GE 5 MODULE 2 - The Structures of GlobalizationDocument7 pagesGE 5 MODULE 2 - The Structures of GlobalizationAway To PonderNo ratings yet

- Week 1 LessonsDocument50 pagesWeek 1 LessonsAway To PonderNo ratings yet

- Module - Week 5 STSDocument8 pagesModule - Week 5 STSAway To PonderNo ratings yet

- Revised Second Module For Purposive CommunicationDocument13 pagesRevised Second Module For Purposive CommunicationAway To PonderNo ratings yet

- Module - Week 6 STSDocument6 pagesModule - Week 6 STSAway To PonderNo ratings yet

- GDP Quiz1Document4 pagesGDP Quiz1Away To PonderNo ratings yet

- 66 - 4 - 1 - Business StudiesDocument23 pages66 - 4 - 1 - Business StudiesbhaiyarakeshNo ratings yet

- Dwnload Full Introduction To Information Systems People Technology and Processes 3rd Edition Wallace Test Bank PDFDocument36 pagesDwnload Full Introduction To Information Systems People Technology and Processes 3rd Edition Wallace Test Bank PDFmellow.duncical.v9vuq100% (16)

- Lecture 2 - Ms - Hong An - Incoterms (Revised 02 Mar 2019)Document51 pagesLecture 2 - Ms - Hong An - Incoterms (Revised 02 Mar 2019)Tâm Lê Hồ HỒNGNo ratings yet

- 12th BM Paper - 1 - HL (Set - C)Document3 pages12th BM Paper - 1 - HL (Set - C)Mohd Bilal TariqNo ratings yet

- Letter of Agreement 01Document3 pagesLetter of Agreement 01Anonymous w53hOKdRoINo ratings yet

- Inventory ControlDocument52 pagesInventory Controlaafanshahid180No ratings yet

- HIlbro SurgicalDocument70 pagesHIlbro Surgicalshazay_7733% (3)

- Consulting Civil EngineerDocument4 pagesConsulting Civil Engineerhabtu tesemaNo ratings yet

- Managerial Accounting Asia Pacific 1St Edition Mowen Solutions Manual Full Chapter PDFDocument32 pagesManagerial Accounting Asia Pacific 1St Edition Mowen Solutions Manual Full Chapter PDFjohnjohnsondpybkqsfct100% (14)

- PV4 Milestone 4Document26 pagesPV4 Milestone 4Milo MiloNo ratings yet

- Work Portfolio - Eng. Neagu GeorgianDocument21 pagesWork Portfolio - Eng. Neagu GeorgianGeorgian NeaguNo ratings yet

- Strategic Supply Chain Management: Syed Abdul Rehman KhanDocument2 pagesStrategic Supply Chain Management: Syed Abdul Rehman KhanrockyssssNo ratings yet

- Ammar Ahmad: Welding InspectorDocument4 pagesAmmar Ahmad: Welding InspectorAdilMunirNo ratings yet

- Lecture - 11 - Rate Analysis - Estimation and Costing - AmiteshDocument15 pagesLecture - 11 - Rate Analysis - Estimation and Costing - AmiteshSupriya DasNo ratings yet

- Web Class8Document19 pagesWeb Class8Christos MaiNo ratings yet

- 07 CBM RigsDocument5 pages07 CBM RigsRahesa Wahyu NalendraNo ratings yet

- Republic of Kenya: County Government of BusiaDocument94 pagesRepublic of Kenya: County Government of BusiaSolidr ArchitectsNo ratings yet

- Agg Innov - Business PlanDocument16 pagesAgg Innov - Business Planshankarjmc7407No ratings yet

- Group No-15 - Section-B - Fin1104Document6 pagesGroup No-15 - Section-B - Fin1104Aswath ChandrasekarNo ratings yet

- Spare Part Designation S40.1 S50.1 S63.1 S80.1: N/a N/aDocument3 pagesSpare Part Designation S40.1 S50.1 S63.1 S80.1: N/a N/aeli saNo ratings yet

- Brisbane Land ValuationsDocument8 pagesBrisbane Land ValuationsW Martin Canales AyalaNo ratings yet

- Government of Andhra Pradesh Municipal Administration DepartmentDocument6 pagesGovernment of Andhra Pradesh Municipal Administration Departmentuttamreddy8244266No ratings yet

- Annex IV Intertek Facility Integrity Acknowledgment and Declaration Form V0010Document3 pagesAnnex IV Intertek Facility Integrity Acknowledgment and Declaration Form V0010muadzzulkar9No ratings yet

- Institute of Management Science: (Shepa) Nibia, Bachchaon, VRM Bypass Varanasi - 221001Document79 pagesInstitute of Management Science: (Shepa) Nibia, Bachchaon, VRM Bypass Varanasi - 221001dctarang50% (4)

- Cost Management of Engineering ProjectsDocument2 pagesCost Management of Engineering ProjectsAadhilNo ratings yet

- Dear respondent-WPS OfficeDocument3 pagesDear respondent-WPS OfficeJohn Ezra SajulNo ratings yet

- Corporate Governance in IndiaDocument29 pagesCorporate Governance in IndiaMH PHOTO CREATIVENo ratings yet

- CEBA45 - Group ActivityDocument11 pagesCEBA45 - Group ActivityShivneel Kunaal KaranNo ratings yet

Download as pdf or txt

You might also like

- SPC 3rd Edition EnglishDocument233 pagesSPC 3rd Edition Englishdhillon63No ratings yet

- Opm TQM Course Syllabus Bsa BsaisDocument9 pagesOpm TQM Course Syllabus Bsa BsaisPeachyNo ratings yet

- Accounting Part 2: Problem SolvingDocument10 pagesAccounting Part 2: Problem Solvingnd555No ratings yet

- PPE Government Grant Borrowing Cost Intangible AssetsDocument7 pagesPPE Government Grant Borrowing Cost Intangible AssetsLian Garl100% (4)

- Intermediate Accounting 1 - Chapter 15, Financial Assets at Fair ValueDocument8 pagesIntermediate Accounting 1 - Chapter 15, Financial Assets at Fair ValueAndrei FajardoNo ratings yet

- Chapter 18 - Investment in Associate 2 PDFDocument15 pagesChapter 18 - Investment in Associate 2 PDFTurksNo ratings yet

- Problem 23-7 and 23-8Document2 pagesProblem 23-7 and 23-8Maria LicuananNo ratings yet

- Intacc FinalsDocument81 pagesIntacc FinalsargoNo ratings yet

- 7 3 BuenaventuraDocument2 pages7 3 BuenaventuraAnonnNo ratings yet

- Chapter 13 - Gross Profit MethodDocument2 pagesChapter 13 - Gross Profit MethodBena CubillasNo ratings yet

- IA 1 Valix 2020 Ver. Problem 27-5 - Problem 27-7Document2 pagesIA 1 Valix 2020 Ver. Problem 27-5 - Problem 27-7Ariean Joy DequiñaNo ratings yet

- Ppe Borrowing Cost July 12 SummerDocument12 pagesPpe Borrowing Cost July 12 SummerJelyn RuazolNo ratings yet

- Sol. Man. - Chapter 17 - Depletion of Mineral Resources - Ia Part 1BDocument3 pagesSol. Man. - Chapter 17 - Depletion of Mineral Resources - Ia Part 1BMahasia MANDIGANNo ratings yet

- Test - Financial PlanningDocument3 pagesTest - Financial PlanningMasTer PanDaNo ratings yet

- Revaluation-Accounting CompressDocument13 pagesRevaluation-Accounting CompressEunice Buenaventura100% (1)

- 21 Financial Assets at Fair Value: Solution 21-1 Answer CDocument30 pages21 Financial Assets at Fair Value: Solution 21-1 Answer CLayNo ratings yet

- Chapter 33Document7 pagesChapter 33Shane Ivory ClaudioNo ratings yet

- Group 1 - Chapter 16Document8 pagesGroup 1 - Chapter 16Cherie Soriano AnanayoNo ratings yet

- Depletion 5Document1 pageDepletion 5Paula Mae DacanayNo ratings yet

- ACC 102.key Answer - Quiz 1.inventoriesDocument5 pagesACC 102.key Answer - Quiz 1.inventoriesMa. Lou Erika BALITENo ratings yet

- Charisma Company Required 1 Date Interest Received Interest Income Discount Amortization Carrying AmountDocument2 pagesCharisma Company Required 1 Date Interest Received Interest Income Discount Amortization Carrying AmountAnonnNo ratings yet

- Seatwork Module 10Document3 pagesSeatwork Module 10Marjorie PalmaNo ratings yet

- Flexible Company Debit Credit 2020Document1 pageFlexible Company Debit Credit 2020AnonnNo ratings yet

- Chapter 16Document10 pagesChapter 16GONZALES, MICA ANGEL A.No ratings yet

- Land and BuildingDocument5 pagesLand and BuildingDianna DayawonNo ratings yet

- Chapter 7Document18 pagesChapter 7Raven Vargas DayritNo ratings yet

- Investment in Equity Securities - Problem 16-2, 16-3, 16-10. and 16-11Document6 pagesInvestment in Equity Securities - Problem 16-2, 16-3, 16-10. and 16-11Jessie Dela CruzNo ratings yet

- Financial Asset at Amortized CostDocument4 pagesFinancial Asset at Amortized CostXNo ratings yet

- IA 2 Chapter 5 ActivitiesDocument12 pagesIA 2 Chapter 5 ActivitiesShaina TorraineNo ratings yet

- AC13 Provisions, Contingencies and Other Liabilities Additional Guide ProblemsDocument2 pagesAC13 Provisions, Contingencies and Other Liabilities Additional Guide ProblemsDianaNo ratings yet

- Intermediate Accounting Chapter 23 To 35Document101 pagesIntermediate Accounting Chapter 23 To 35Blue SkyNo ratings yet

- This Study Resource Was Shared Via: Solution 23-2 Answer DDocument5 pagesThis Study Resource Was Shared Via: Solution 23-2 Answer DDummy GoogleNo ratings yet

- Chapter 48: ProvisionDocument8 pagesChapter 48: ProvisionjsemlpzNo ratings yet

- Padernal BSA 1A SW Problem 3 11Document1 pagePadernal BSA 1A SW Problem 3 11Fly ThoughtsNo ratings yet

- Problem 2 8Document6 pagesProblem 2 8Carl Jaime Dela CruzNo ratings yet

- Machinery VergaraDocument10 pagesMachinery VergaraDarlianne Klyne BayerNo ratings yet

- Chapter 18Document34 pagesChapter 18Christine Marie T. RamirezNo ratings yet

- ASC Partnership Schedule of Safe PaymentsDocument3 pagesASC Partnership Schedule of Safe PaymentsMayaNo ratings yet

- Pre2 Module-Intangible Assets: Learning ObjectivesDocument9 pagesPre2 Module-Intangible Assets: Learning ObjectivesCyrine Grace DucogNo ratings yet

- Practice Set Review - Current LiabilitiesDocument12 pagesPractice Set Review - Current LiabilitiesKayla MirandaNo ratings yet

- Chapter 20Document13 pagesChapter 20Bella RonahNo ratings yet

- Group Activity Mina HanDocument4 pagesGroup Activity Mina HanLevi's DishwasherNo ratings yet

- Borrowing Cost (PAS 23)Document6 pagesBorrowing Cost (PAS 23)CharléNo ratings yet

- Precious Grace Ann R. Loja IA1 April 13, 2020: Initial Measurement of Loan ReceivableDocument6 pagesPrecious Grace Ann R. Loja IA1 April 13, 2020: Initial Measurement of Loan Receivableprecious2lojaNo ratings yet

- Basic Concepts Revenue Cycle: List Price, Trade Discount, Prepaid Freight, Cash DiscountDocument50 pagesBasic Concepts Revenue Cycle: List Price, Trade Discount, Prepaid Freight, Cash DiscountJean MaeNo ratings yet

- IA2 Worksheet-BONDS PAYABLE - 101010Document11 pagesIA2 Worksheet-BONDS PAYABLE - 101010aehy lznuscrfbjNo ratings yet

- Lobrigas Unit3 Topic1 AssessmentDocument9 pagesLobrigas Unit3 Topic1 AssessmentClaudine LobrigasNo ratings yet

- T-Test One SampleDocument5 pagesT-Test One SampleJessa Delos SantosNo ratings yet

- Problem 7 - 6 & 7Document2 pagesProblem 7 - 6 & 7Micah April SabularseNo ratings yet

- 1Document20 pages1Denver AcenasNo ratings yet

- EXAMINATION ON INVENTORY MaDocument5 pagesEXAMINATION ON INVENTORY Macriszel4sobejanaNo ratings yet

- ACC 121 Chapter 55Document4 pagesACC 121 Chapter 55Mohammad saripNo ratings yet

- Chapter22 BuenaventuraDocument4 pagesChapter22 BuenaventuraAnonnNo ratings yet

- MachineryDocument4 pagesMachineryDianna DayawonNo ratings yet

- Intacc 3 Leases FinalsDocument9 pagesIntacc 3 Leases FinalsDarryl AgustinNo ratings yet

- Sale and LeasebackDocument10 pagesSale and LeasebackShinny Jewel VingnoNo ratings yet

- Chap16 ProblemsDocument20 pagesChap16 ProblemsYen YenNo ratings yet

- Land Building Machinery ProblemsDocument13 pagesLand Building Machinery ProblemsJomerNo ratings yet

- Draft A90Document7 pagesDraft A90Jewel Mae MercadoNo ratings yet

- FAR04-08 - Government Grant & Borrowing CostsDocument7 pagesFAR04-08 - Government Grant & Borrowing CostsAi NatangcopNo ratings yet

- Answer Key For Strategic Cost Management - CompressDocument19 pagesAnswer Key For Strategic Cost Management - CompressMikee RizonNo ratings yet

- CPAR B94 FAR Final PB Exam - Answers - SolutionsDocument8 pagesCPAR B94 FAR Final PB Exam - Answers - SolutionsJazehl ValdezNo ratings yet

- Prof Ed 2 M2, L2Document3 pagesProf Ed 2 M2, L2Away To PonderNo ratings yet

- Edited Module - Docx August 25 2020Document206 pagesEdited Module - Docx August 25 2020Away To PonderNo ratings yet

- ACCT104 Prelim Exam 38 47Document2 pagesACCT104 Prelim Exam 38 47Away To PonderNo ratings yet

- Content No. 07 Bank Reconciliation StatementDocument3 pagesContent No. 07 Bank Reconciliation StatementAway To PonderNo ratings yet

- Content No. 06 Basic Documents and Transactions Related To Bank DepositsDocument3 pagesContent No. 06 Basic Documents and Transactions Related To Bank DepositsAway To PonderNo ratings yet

- Solutions To 2 1 To 2 5Document5 pagesSolutions To 2 1 To 2 5Away To PonderNo ratings yet

- ACCT104 Quizzes SolutionsDocument2 pagesACCT104 Quizzes SolutionsAway To PonderNo ratings yet

- ACCT105 Quiz 02 and 03 Prelim SolutionDocument3 pagesACCT105 Quiz 02 and 03 Prelim SolutionAway To PonderNo ratings yet

- ACCT105 Quizzes and SolutionsDocument8 pagesACCT105 Quizzes and SolutionsAway To PonderNo ratings yet

- 30 1 To 30 4Document2 pages30 1 To 30 4Away To PonderNo ratings yet

- Binalbagan Catholic College: Course Guide Science, Technology and Society (STS)Document5 pagesBinalbagan Catholic College: Course Guide Science, Technology and Society (STS)Away To PonderNo ratings yet

- 31 1 To 31 4Document2 pages31 1 To 31 4Away To PonderNo ratings yet

- GE 5 MODULE 2 - The Structures of GlobalizationDocument7 pagesGE 5 MODULE 2 - The Structures of GlobalizationAway To PonderNo ratings yet

- Week 1 LessonsDocument50 pagesWeek 1 LessonsAway To PonderNo ratings yet

- Module - Week 5 STSDocument8 pagesModule - Week 5 STSAway To PonderNo ratings yet

- Revised Second Module For Purposive CommunicationDocument13 pagesRevised Second Module For Purposive CommunicationAway To PonderNo ratings yet

- Module - Week 6 STSDocument6 pagesModule - Week 6 STSAway To PonderNo ratings yet

- GDP Quiz1Document4 pagesGDP Quiz1Away To PonderNo ratings yet

- 66 - 4 - 1 - Business StudiesDocument23 pages66 - 4 - 1 - Business StudiesbhaiyarakeshNo ratings yet

- Dwnload Full Introduction To Information Systems People Technology and Processes 3rd Edition Wallace Test Bank PDFDocument36 pagesDwnload Full Introduction To Information Systems People Technology and Processes 3rd Edition Wallace Test Bank PDFmellow.duncical.v9vuq100% (16)

- Lecture 2 - Ms - Hong An - Incoterms (Revised 02 Mar 2019)Document51 pagesLecture 2 - Ms - Hong An - Incoterms (Revised 02 Mar 2019)Tâm Lê Hồ HỒNGNo ratings yet

- 12th BM Paper - 1 - HL (Set - C)Document3 pages12th BM Paper - 1 - HL (Set - C)Mohd Bilal TariqNo ratings yet

- Letter of Agreement 01Document3 pagesLetter of Agreement 01Anonymous w53hOKdRoINo ratings yet

- Inventory ControlDocument52 pagesInventory Controlaafanshahid180No ratings yet

- HIlbro SurgicalDocument70 pagesHIlbro Surgicalshazay_7733% (3)

- Consulting Civil EngineerDocument4 pagesConsulting Civil Engineerhabtu tesemaNo ratings yet

- Managerial Accounting Asia Pacific 1St Edition Mowen Solutions Manual Full Chapter PDFDocument32 pagesManagerial Accounting Asia Pacific 1St Edition Mowen Solutions Manual Full Chapter PDFjohnjohnsondpybkqsfct100% (14)

- PV4 Milestone 4Document26 pagesPV4 Milestone 4Milo MiloNo ratings yet

- Work Portfolio - Eng. Neagu GeorgianDocument21 pagesWork Portfolio - Eng. Neagu GeorgianGeorgian NeaguNo ratings yet

- Strategic Supply Chain Management: Syed Abdul Rehman KhanDocument2 pagesStrategic Supply Chain Management: Syed Abdul Rehman KhanrockyssssNo ratings yet

- Ammar Ahmad: Welding InspectorDocument4 pagesAmmar Ahmad: Welding InspectorAdilMunirNo ratings yet

- Lecture - 11 - Rate Analysis - Estimation and Costing - AmiteshDocument15 pagesLecture - 11 - Rate Analysis - Estimation and Costing - AmiteshSupriya DasNo ratings yet

- Web Class8Document19 pagesWeb Class8Christos MaiNo ratings yet

- 07 CBM RigsDocument5 pages07 CBM RigsRahesa Wahyu NalendraNo ratings yet

- Republic of Kenya: County Government of BusiaDocument94 pagesRepublic of Kenya: County Government of BusiaSolidr ArchitectsNo ratings yet

- Agg Innov - Business PlanDocument16 pagesAgg Innov - Business Planshankarjmc7407No ratings yet

- Group No-15 - Section-B - Fin1104Document6 pagesGroup No-15 - Section-B - Fin1104Aswath ChandrasekarNo ratings yet

- Spare Part Designation S40.1 S50.1 S63.1 S80.1: N/a N/aDocument3 pagesSpare Part Designation S40.1 S50.1 S63.1 S80.1: N/a N/aeli saNo ratings yet

- Brisbane Land ValuationsDocument8 pagesBrisbane Land ValuationsW Martin Canales AyalaNo ratings yet

- Government of Andhra Pradesh Municipal Administration DepartmentDocument6 pagesGovernment of Andhra Pradesh Municipal Administration Departmentuttamreddy8244266No ratings yet

- Annex IV Intertek Facility Integrity Acknowledgment and Declaration Form V0010Document3 pagesAnnex IV Intertek Facility Integrity Acknowledgment and Declaration Form V0010muadzzulkar9No ratings yet

- Institute of Management Science: (Shepa) Nibia, Bachchaon, VRM Bypass Varanasi - 221001Document79 pagesInstitute of Management Science: (Shepa) Nibia, Bachchaon, VRM Bypass Varanasi - 221001dctarang50% (4)

- Cost Management of Engineering ProjectsDocument2 pagesCost Management of Engineering ProjectsAadhilNo ratings yet

- Dear respondent-WPS OfficeDocument3 pagesDear respondent-WPS OfficeJohn Ezra SajulNo ratings yet

- Corporate Governance in IndiaDocument29 pagesCorporate Governance in IndiaMH PHOTO CREATIVENo ratings yet

- CEBA45 - Group ActivityDocument11 pagesCEBA45 - Group ActivityShivneel Kunaal KaranNo ratings yet