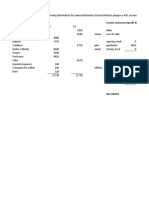

Financial Statements

Financial Statements

You might also like

- IWT Conscious Spending Plan 2023Document12 pagesIWT Conscious Spending Plan 2023GEO654No ratings yet

- Ia Vol 3 Valix 2019 SolmanDocument105 pagesIa Vol 3 Valix 2019 Solmanxeth agas86% (7)

- Intermediate Accounting 2: a QuickStudy Digital Reference GuideFrom EverandIntermediate Accounting 2: a QuickStudy Digital Reference GuideNo ratings yet

- This Study Resource WasDocument4 pagesThis Study Resource WasRizquita DhindaNo ratings yet

- 2020 Beximco and Renata Ratio AnalysisDocument18 pages2020 Beximco and Renata Ratio AnalysisRahi Mun100% (2)

- Cash FlowDocument9 pagesCash Flowshreyanshi sharmaNo ratings yet

- Unit 10 - Cash Flow AnalysisDocument26 pagesUnit 10 - Cash Flow Analysisqwertyytrewq12No ratings yet

- Cahs Flow StatementDocument18 pagesCahs Flow Statementtaniya17No ratings yet

- Cash Flow StatementDocument11 pagesCash Flow StatementPranay SinghNo ratings yet

- Statement of Cash FlowDocument24 pagesStatement of Cash FlowMylene Santiago100% (1)

- Unit Ii Accounting PDFDocument11 pagesUnit Ii Accounting PDFMo ToNo ratings yet

- Statement of Changes in Financial Position: Cash Flow StatementDocument25 pagesStatement of Changes in Financial Position: Cash Flow StatementCharu Arora100% (1)

- Section 7Document30 pagesSection 7Abata BageyuNo ratings yet

- Accounting Assignment 2Document4 pagesAccounting Assignment 2Laddie LMNo ratings yet

- Cash Flow StatementDocument17 pagesCash Flow StatementSwapnil ManeNo ratings yet

- 4 Statement of Cash FlowsDocument13 pages4 Statement of Cash FlowsNabi ParkNo ratings yet

- SCF - 3rd YrDocument27 pagesSCF - 3rd YrA.J. Chua100% (1)

- Cash Follow Statement (1) - 2Document17 pagesCash Follow Statement (1) - 2Gkgolam KibriaNo ratings yet

- Cash Flow Statement NotesDocument8 pagesCash Flow Statement NotesAbdullahNo ratings yet

- Chapter 13 PowerPointDocument89 pagesChapter 13 PowerPointcheuleee100% (1)

- CTRL Vol4Document19 pagesCTRL Vol4Roberto SanchezNo ratings yet

- Pas 7Document11 pagesPas 7Princess Jullyn ClaudioNo ratings yet

- Cash Flow StatementDocument24 pagesCash Flow StatementSHENUNo ratings yet

- Finacc 2 IvDocument36 pagesFinacc 2 IvMarielle De LeonNo ratings yet

- Understanding Cash Flow StatementDocument3 pagesUnderstanding Cash Flow StatementImran IdrisNo ratings yet

- Statement of Cash FlowsDocument26 pagesStatement of Cash Flowslascona.christinerheaNo ratings yet

- Chapter 4-Statement of Cash FlowsDocument3 pagesChapter 4-Statement of Cash FlowsDan GalvezNo ratings yet

- CASH FLOW StudentsDocument14 pagesCASH FLOW StudentsJirehJohnG.ArafolNo ratings yet

- Statement of Cash FlowsDocument84 pagesStatement of Cash Flowsknarfylunjas15No ratings yet

- AFM Unit 4 CASH FLOW TheoryDocument5 pagesAFM Unit 4 CASH FLOW TheoryMr. N. KARTHIKEYAN Asst Prof MBANo ratings yet

- Cash Flow AnalysisDocument15 pagesCash Flow AnalysisElvie Abulencia-BagsicNo ratings yet

- Finacial Statement Analysis Cash Flow Statement and Its AnalysisDocument8 pagesFinacial Statement Analysis Cash Flow Statement and Its AnalysisLeomarc LavaNo ratings yet

- Unit 4 Cash Flow StatementDocument26 pagesUnit 4 Cash Flow Statementjatin4verma-2No ratings yet

- Cash Flow StatementDocument26 pagesCash Flow StatementADITI BISWASNo ratings yet

- Cash Flow Analysis ExcercisesDocument6 pagesCash Flow Analysis Excercisesmax zeneNo ratings yet

- Chap 11cash FlowDocument6 pagesChap 11cash FlowAlton D'silvaNo ratings yet

- Flow of Costs: Module 2 Introducing The Fin Statements, and Transaction Analysis. Start by Looking atDocument36 pagesFlow of Costs: Module 2 Introducing The Fin Statements, and Transaction Analysis. Start by Looking atLong NguyenNo ratings yet

- CashDocument37 pagesCashanand chawanNo ratings yet

- Fundamentals of Accountancy, Business, and ManagementDocument16 pagesFundamentals of Accountancy, Business, and ManagementAraNo ratings yet

- Unit 1Document23 pagesUnit 1Katlego ThaboNo ratings yet

- Cash Flow Statement Wit SumDocument27 pagesCash Flow Statement Wit SumSunay KhaireNo ratings yet

- IAS 7-Statements of Cash FlowsDocument41 pagesIAS 7-Statements of Cash Flowstmandikutse04No ratings yet

- Statement of Cash FlowsDocument9 pagesStatement of Cash FlowsNini yaludNo ratings yet

- Cash and Fund Flow StatementDocument6 pagesCash and Fund Flow StatementAsma SaeedNo ratings yet

- Chapter: - 8Document16 pagesChapter: - 8Kanu SubramanianNo ratings yet

- Cash Flow Statement AnalysisDocument29 pagesCash Flow Statement AnalysisCASAQUIT, IRA LORAINENo ratings yet

- Cash Flow ReportingDocument90 pagesCash Flow Reportingkristane ingrid arcayeraNo ratings yet

- Cash Flow AnalysisDocument7 pagesCash Flow AnalysisDeepalaxmi BhatNo ratings yet

- Chapter 6 Satatement of Cash FlowsDocument28 pagesChapter 6 Satatement of Cash FlowsCabdiraxmaan GeeldoonNo ratings yet

- Cash Flow Statements: by CA. Pramod Prabhu. S.HDocument17 pagesCash Flow Statements: by CA. Pramod Prabhu. S.HsonibijuNo ratings yet

- Satish FinalDocument79 pagesSatish FinalAnonymous MhCdtwxQINo ratings yet

- Financial Accounting - Information For Decisions - Session 9 - Chapter 11 PPT HmugGnI6jbDocument41 pagesFinancial Accounting - Information For Decisions - Session 9 - Chapter 11 PPT HmugGnI6jbmukul3087_305865623No ratings yet

- Analusis of Financial StatementDocument28 pagesAnalusis of Financial StatementAjaykumar MauryaNo ratings yet

- Analysis of Financial Statements Cash Flow Analysis: Prof. Priyanka Oza Mms Sem IiDocument21 pagesAnalysis of Financial Statements Cash Flow Analysis: Prof. Priyanka Oza Mms Sem IiSujit AdulkarNo ratings yet

- International Accounting Standard 7 Statement of Cash FlowsDocument8 pagesInternational Accounting Standard 7 Statement of Cash Flowsইবনুল মাইজভাণ্ডারীNo ratings yet

- 2022 Sem 1 ACC10007 Topic 3Document45 pages2022 Sem 1 ACC10007 Topic 3JordanNo ratings yet

- 21 Ch. 21 - Statement of Cash Flows - S2015Document27 pages21 Ch. 21 - Statement of Cash Flows - S2015zhouzhu211100% (1)

- Of Cash and Which Are Subject To An Insignificant Risk of Changes in ValueDocument2 pagesOf Cash and Which Are Subject To An Insignificant Risk of Changes in ValueJMClosedNo ratings yet

- Atp 106 LPM Accounting - Topic 5 - Statement of Cash FlowsDocument17 pagesAtp 106 LPM Accounting - Topic 5 - Statement of Cash FlowsTwain JonesNo ratings yet

- Cash Flow Statement Direct MethodDocument20 pagesCash Flow Statement Direct MethodMidsy De la Cruz100% (1)

- Cash Flow StatementDocument2 pagesCash Flow Statementmark_torreonNo ratings yet

- Cash Flow StatementDocument8 pagesCash Flow StatementHemant kumar JhaNo ratings yet

- Theory - CASH FLOW ANALYSISDocument7 pagesTheory - CASH FLOW ANALYSISShahina KhanNo ratings yet

- Group8 Stone Container Corporation Final PDFDocument7 pagesGroup8 Stone Container Corporation Final PDFRahul BhatiaNo ratings yet

- KK KKKKKDocument14 pagesKK KKKKKCarlo VillanNo ratings yet

- Part Two: Financial Accounting: An IntroductionDocument139 pagesPart Two: Financial Accounting: An IntroductionRobel Habtamu100% (1)

- Chapter 10 Accounting Cycle of A Merchandising BusinessDocument40 pagesChapter 10 Accounting Cycle of A Merchandising BusinessOmelkhair YahyaNo ratings yet

- 2011 Bar Examination Questionnaire For Commercial Law Set ADocument37 pages2011 Bar Examination Questionnaire For Commercial Law Set Achiji chzzzmeowNo ratings yet

- Dhanuka Laboratories LimitedDocument8 pagesDhanuka Laboratories LimitedDarshanNo ratings yet

- The Oriental Insurance Company LTDDocument7 pagesThe Oriental Insurance Company LTDSri KamalNo ratings yet

- CMA MCQ MergedDocument224 pagesCMA MCQ Mergedsaikat karmakarNo ratings yet

- Sebenta Inglês AplicadoDocument30 pagesSebenta Inglês AplicadoJoana PimentelNo ratings yet

- Accounting Adjustments 1Document71 pagesAccounting Adjustments 1vukicevic.ivan5No ratings yet

- Portfolio For Personal FinanceDocument7 pagesPortfolio For Personal FinanceSharon SagerNo ratings yet

- Cma ProjectDocument14 pagesCma ProjectAbhishek SaravananNo ratings yet

- Credit Analysis-Medlife: 1. Description of The LoanDocument20 pagesCredit Analysis-Medlife: 1. Description of The LoanAlexandraNo ratings yet

- LAPORAN KEUANGAN PT Unilever Indonesia TBKDocument12 pagesLAPORAN KEUANGAN PT Unilever Indonesia TBKNesya NandaNo ratings yet

- Lending in Finance WorldDocument18 pagesLending in Finance WorldMeesam NaqviNo ratings yet

- Discussions On Chapter 2Document13 pagesDiscussions On Chapter 2Norren Thea VlogsNo ratings yet

- Solution Manual For Macroeconomics 5 e 5th Edition Stephen D WilliamsonDocument8 pagesSolution Manual For Macroeconomics 5 e 5th Edition Stephen D WilliamsonRalphLaneifrte100% (85)

- 12 Indemnity & Guarantee Bailment & PledgeDocument38 pages12 Indemnity & Guarantee Bailment & PledgeMUHMMAD ARSALAN 13728No ratings yet

- Topic 4Document7 pagesTopic 4mintchoco98No ratings yet

- Audit of ReceivablesDocument5 pagesAudit of ReceivablesandreamrieNo ratings yet

- S Pinkerton Statement of Financial PositionDocument6 pagesS Pinkerton Statement of Financial PositionFindley MaringkaNo ratings yet

- Bank/Financial Instituion/ Company: Process Flow Chart of Asset SecuritisationDocument1 pageBank/Financial Instituion/ Company: Process Flow Chart of Asset Securitisationsudhir.kochhar3530No ratings yet

- Investment in Equity SecuritiesDocument11 pagesInvestment in Equity SecuritiesnikNo ratings yet

- Islamic Financial Accounting Standard-2 Ijarah: Interpretation and ImplementationDocument23 pagesIslamic Financial Accounting Standard-2 Ijarah: Interpretation and Implementationhammad067No ratings yet

- Ch02 Financial Statements, Taxes, and Cash FlowsDocument34 pagesCh02 Financial Statements, Taxes, and Cash FlowsAndrew BruceNo ratings yet

- DK Goel Solutions Class 11 Accountancy Chapter 23 - Accounts From Incomplete RecordsDocument67 pagesDK Goel Solutions Class 11 Accountancy Chapter 23 - Accounts From Incomplete RecordsPython The SnakeNo ratings yet

Download as pdf or txt

You might also like

- IWT Conscious Spending Plan 2023Document12 pagesIWT Conscious Spending Plan 2023GEO654No ratings yet

- Ia Vol 3 Valix 2019 SolmanDocument105 pagesIa Vol 3 Valix 2019 Solmanxeth agas86% (7)

- Intermediate Accounting 2: a QuickStudy Digital Reference GuideFrom EverandIntermediate Accounting 2: a QuickStudy Digital Reference GuideNo ratings yet

- This Study Resource WasDocument4 pagesThis Study Resource WasRizquita DhindaNo ratings yet

- 2020 Beximco and Renata Ratio AnalysisDocument18 pages2020 Beximco and Renata Ratio AnalysisRahi Mun100% (2)

- Cash FlowDocument9 pagesCash Flowshreyanshi sharmaNo ratings yet

- Unit 10 - Cash Flow AnalysisDocument26 pagesUnit 10 - Cash Flow Analysisqwertyytrewq12No ratings yet

- Cahs Flow StatementDocument18 pagesCahs Flow Statementtaniya17No ratings yet

- Cash Flow StatementDocument11 pagesCash Flow StatementPranay SinghNo ratings yet

- Statement of Cash FlowDocument24 pagesStatement of Cash FlowMylene Santiago100% (1)

- Unit Ii Accounting PDFDocument11 pagesUnit Ii Accounting PDFMo ToNo ratings yet

- Statement of Changes in Financial Position: Cash Flow StatementDocument25 pagesStatement of Changes in Financial Position: Cash Flow StatementCharu Arora100% (1)

- Section 7Document30 pagesSection 7Abata BageyuNo ratings yet

- Accounting Assignment 2Document4 pagesAccounting Assignment 2Laddie LMNo ratings yet

- Cash Flow StatementDocument17 pagesCash Flow StatementSwapnil ManeNo ratings yet

- 4 Statement of Cash FlowsDocument13 pages4 Statement of Cash FlowsNabi ParkNo ratings yet

- SCF - 3rd YrDocument27 pagesSCF - 3rd YrA.J. Chua100% (1)

- Cash Follow Statement (1) - 2Document17 pagesCash Follow Statement (1) - 2Gkgolam KibriaNo ratings yet

- Cash Flow Statement NotesDocument8 pagesCash Flow Statement NotesAbdullahNo ratings yet

- Chapter 13 PowerPointDocument89 pagesChapter 13 PowerPointcheuleee100% (1)

- CTRL Vol4Document19 pagesCTRL Vol4Roberto SanchezNo ratings yet

- Pas 7Document11 pagesPas 7Princess Jullyn ClaudioNo ratings yet

- Cash Flow StatementDocument24 pagesCash Flow StatementSHENUNo ratings yet

- Finacc 2 IvDocument36 pagesFinacc 2 IvMarielle De LeonNo ratings yet

- Understanding Cash Flow StatementDocument3 pagesUnderstanding Cash Flow StatementImran IdrisNo ratings yet

- Statement of Cash FlowsDocument26 pagesStatement of Cash Flowslascona.christinerheaNo ratings yet

- Chapter 4-Statement of Cash FlowsDocument3 pagesChapter 4-Statement of Cash FlowsDan GalvezNo ratings yet

- CASH FLOW StudentsDocument14 pagesCASH FLOW StudentsJirehJohnG.ArafolNo ratings yet

- Statement of Cash FlowsDocument84 pagesStatement of Cash Flowsknarfylunjas15No ratings yet

- AFM Unit 4 CASH FLOW TheoryDocument5 pagesAFM Unit 4 CASH FLOW TheoryMr. N. KARTHIKEYAN Asst Prof MBANo ratings yet

- Cash Flow AnalysisDocument15 pagesCash Flow AnalysisElvie Abulencia-BagsicNo ratings yet

- Finacial Statement Analysis Cash Flow Statement and Its AnalysisDocument8 pagesFinacial Statement Analysis Cash Flow Statement and Its AnalysisLeomarc LavaNo ratings yet

- Unit 4 Cash Flow StatementDocument26 pagesUnit 4 Cash Flow Statementjatin4verma-2No ratings yet

- Cash Flow StatementDocument26 pagesCash Flow StatementADITI BISWASNo ratings yet

- Cash Flow Analysis ExcercisesDocument6 pagesCash Flow Analysis Excercisesmax zeneNo ratings yet

- Chap 11cash FlowDocument6 pagesChap 11cash FlowAlton D'silvaNo ratings yet

- Flow of Costs: Module 2 Introducing The Fin Statements, and Transaction Analysis. Start by Looking atDocument36 pagesFlow of Costs: Module 2 Introducing The Fin Statements, and Transaction Analysis. Start by Looking atLong NguyenNo ratings yet

- CashDocument37 pagesCashanand chawanNo ratings yet

- Fundamentals of Accountancy, Business, and ManagementDocument16 pagesFundamentals of Accountancy, Business, and ManagementAraNo ratings yet

- Unit 1Document23 pagesUnit 1Katlego ThaboNo ratings yet

- Cash Flow Statement Wit SumDocument27 pagesCash Flow Statement Wit SumSunay KhaireNo ratings yet

- IAS 7-Statements of Cash FlowsDocument41 pagesIAS 7-Statements of Cash Flowstmandikutse04No ratings yet

- Statement of Cash FlowsDocument9 pagesStatement of Cash FlowsNini yaludNo ratings yet

- Cash and Fund Flow StatementDocument6 pagesCash and Fund Flow StatementAsma SaeedNo ratings yet

- Chapter: - 8Document16 pagesChapter: - 8Kanu SubramanianNo ratings yet

- Cash Flow Statement AnalysisDocument29 pagesCash Flow Statement AnalysisCASAQUIT, IRA LORAINENo ratings yet

- Cash Flow ReportingDocument90 pagesCash Flow Reportingkristane ingrid arcayeraNo ratings yet

- Cash Flow AnalysisDocument7 pagesCash Flow AnalysisDeepalaxmi BhatNo ratings yet

- Chapter 6 Satatement of Cash FlowsDocument28 pagesChapter 6 Satatement of Cash FlowsCabdiraxmaan GeeldoonNo ratings yet

- Cash Flow Statements: by CA. Pramod Prabhu. S.HDocument17 pagesCash Flow Statements: by CA. Pramod Prabhu. S.HsonibijuNo ratings yet

- Satish FinalDocument79 pagesSatish FinalAnonymous MhCdtwxQINo ratings yet

- Financial Accounting - Information For Decisions - Session 9 - Chapter 11 PPT HmugGnI6jbDocument41 pagesFinancial Accounting - Information For Decisions - Session 9 - Chapter 11 PPT HmugGnI6jbmukul3087_305865623No ratings yet

- Analusis of Financial StatementDocument28 pagesAnalusis of Financial StatementAjaykumar MauryaNo ratings yet

- Analysis of Financial Statements Cash Flow Analysis: Prof. Priyanka Oza Mms Sem IiDocument21 pagesAnalysis of Financial Statements Cash Flow Analysis: Prof. Priyanka Oza Mms Sem IiSujit AdulkarNo ratings yet

- International Accounting Standard 7 Statement of Cash FlowsDocument8 pagesInternational Accounting Standard 7 Statement of Cash Flowsইবনুল মাইজভাণ্ডারীNo ratings yet

- 2022 Sem 1 ACC10007 Topic 3Document45 pages2022 Sem 1 ACC10007 Topic 3JordanNo ratings yet

- 21 Ch. 21 - Statement of Cash Flows - S2015Document27 pages21 Ch. 21 - Statement of Cash Flows - S2015zhouzhu211100% (1)

- Of Cash and Which Are Subject To An Insignificant Risk of Changes in ValueDocument2 pagesOf Cash and Which Are Subject To An Insignificant Risk of Changes in ValueJMClosedNo ratings yet

- Atp 106 LPM Accounting - Topic 5 - Statement of Cash FlowsDocument17 pagesAtp 106 LPM Accounting - Topic 5 - Statement of Cash FlowsTwain JonesNo ratings yet

- Cash Flow Statement Direct MethodDocument20 pagesCash Flow Statement Direct MethodMidsy De la Cruz100% (1)

- Cash Flow StatementDocument2 pagesCash Flow Statementmark_torreonNo ratings yet

- Cash Flow StatementDocument8 pagesCash Flow StatementHemant kumar JhaNo ratings yet

- Theory - CASH FLOW ANALYSISDocument7 pagesTheory - CASH FLOW ANALYSISShahina KhanNo ratings yet

- Group8 Stone Container Corporation Final PDFDocument7 pagesGroup8 Stone Container Corporation Final PDFRahul BhatiaNo ratings yet

- KK KKKKKDocument14 pagesKK KKKKKCarlo VillanNo ratings yet

- Part Two: Financial Accounting: An IntroductionDocument139 pagesPart Two: Financial Accounting: An IntroductionRobel Habtamu100% (1)

- Chapter 10 Accounting Cycle of A Merchandising BusinessDocument40 pagesChapter 10 Accounting Cycle of A Merchandising BusinessOmelkhair YahyaNo ratings yet

- 2011 Bar Examination Questionnaire For Commercial Law Set ADocument37 pages2011 Bar Examination Questionnaire For Commercial Law Set Achiji chzzzmeowNo ratings yet

- Dhanuka Laboratories LimitedDocument8 pagesDhanuka Laboratories LimitedDarshanNo ratings yet

- The Oriental Insurance Company LTDDocument7 pagesThe Oriental Insurance Company LTDSri KamalNo ratings yet

- CMA MCQ MergedDocument224 pagesCMA MCQ Mergedsaikat karmakarNo ratings yet

- Sebenta Inglês AplicadoDocument30 pagesSebenta Inglês AplicadoJoana PimentelNo ratings yet

- Accounting Adjustments 1Document71 pagesAccounting Adjustments 1vukicevic.ivan5No ratings yet

- Portfolio For Personal FinanceDocument7 pagesPortfolio For Personal FinanceSharon SagerNo ratings yet

- Cma ProjectDocument14 pagesCma ProjectAbhishek SaravananNo ratings yet

- Credit Analysis-Medlife: 1. Description of The LoanDocument20 pagesCredit Analysis-Medlife: 1. Description of The LoanAlexandraNo ratings yet

- LAPORAN KEUANGAN PT Unilever Indonesia TBKDocument12 pagesLAPORAN KEUANGAN PT Unilever Indonesia TBKNesya NandaNo ratings yet

- Lending in Finance WorldDocument18 pagesLending in Finance WorldMeesam NaqviNo ratings yet

- Discussions On Chapter 2Document13 pagesDiscussions On Chapter 2Norren Thea VlogsNo ratings yet

- Solution Manual For Macroeconomics 5 e 5th Edition Stephen D WilliamsonDocument8 pagesSolution Manual For Macroeconomics 5 e 5th Edition Stephen D WilliamsonRalphLaneifrte100% (85)

- 12 Indemnity & Guarantee Bailment & PledgeDocument38 pages12 Indemnity & Guarantee Bailment & PledgeMUHMMAD ARSALAN 13728No ratings yet

- Topic 4Document7 pagesTopic 4mintchoco98No ratings yet

- Audit of ReceivablesDocument5 pagesAudit of ReceivablesandreamrieNo ratings yet

- S Pinkerton Statement of Financial PositionDocument6 pagesS Pinkerton Statement of Financial PositionFindley MaringkaNo ratings yet

- Bank/Financial Instituion/ Company: Process Flow Chart of Asset SecuritisationDocument1 pageBank/Financial Instituion/ Company: Process Flow Chart of Asset Securitisationsudhir.kochhar3530No ratings yet

- Investment in Equity SecuritiesDocument11 pagesInvestment in Equity SecuritiesnikNo ratings yet

- Islamic Financial Accounting Standard-2 Ijarah: Interpretation and ImplementationDocument23 pagesIslamic Financial Accounting Standard-2 Ijarah: Interpretation and Implementationhammad067No ratings yet

- Ch02 Financial Statements, Taxes, and Cash FlowsDocument34 pagesCh02 Financial Statements, Taxes, and Cash FlowsAndrew BruceNo ratings yet

- DK Goel Solutions Class 11 Accountancy Chapter 23 - Accounts From Incomplete RecordsDocument67 pagesDK Goel Solutions Class 11 Accountancy Chapter 23 - Accounts From Incomplete RecordsPython The SnakeNo ratings yet