Fringe Benefits 2

Fringe Benefits 2

You might also like

- Chapter 6Document24 pagesChapter 6jake doinog88% (16)

- Land Economics - Lecture 1aDocument18 pagesLand Economics - Lecture 1aSixd WaznineNo ratings yet

- Buckwold 21e - CH 4 Selected SolutionsDocument18 pagesBuckwold 21e - CH 4 Selected SolutionsLucy50% (2)

- Fringe Benefits 1Document56 pagesFringe Benefits 1mattnoowinNo ratings yet

- Gross Income: Learning ObjectivesDocument12 pagesGross Income: Learning ObjectivesClaire BarbaNo ratings yet

- Unit 2 SalaryDocument131 pagesUnit 2 SalaryRekha BansalNo ratings yet

- TAX 228 2023 - Special InclusionsDocument29 pagesTAX 228 2023 - Special InclusionsedwardsyaameenNo ratings yet

- Gross Income Regular Tax: MARCH 2019Document57 pagesGross Income Regular Tax: MARCH 2019tyineNo ratings yet

- Gross Income Regular TaxDocument51 pagesGross Income Regular TaxElizalen MacarilayNo ratings yet

- 6.0 INDIVIDUALS PART 3 Fringe Benefit Tax and de Minimis BenefitsDocument41 pages6.0 INDIVIDUALS PART 3 Fringe Benefit Tax and de Minimis BenefitsAllan BacudioNo ratings yet

- 06 Gross IncomeDocument103 pages06 Gross IncomeJSNo ratings yet

- Is The Higher BetweenDocument4 pagesIs The Higher Betweenleshz zynNo ratings yet

- For Session DTD 5th Sep by CA Alok Garg PDFDocument46 pagesFor Session DTD 5th Sep by CA Alok Garg PDFLakshmi Narayana Murthy KapavarapuNo ratings yet

- Chapter 3 Employment Income A 202Document79 pagesChapter 3 Employment Income A 202ateen rizalmanNo ratings yet

- Inclusion and Exclusion of Gross IncomeDocument70 pagesInclusion and Exclusion of Gross IncomeEnola HeitsgerNo ratings yet

- Fringe Benefits TaxDocument11 pagesFringe Benefits Taxkenshin sclanimirNo ratings yet

- Taxation Granada LaynoDocument13 pagesTaxation Granada LaynosimpatheticoNo ratings yet

- Special Allowable Itemized DeductionsDocument6 pagesSpecial Allowable Itemized DeductionsChristine RaizNo ratings yet

- Tax Chapter 10, 11, 12Document13 pagesTax Chapter 10, 11, 12Sheraldine MendozaNo ratings yet

- Limitations: Interest Expense For Passenger Vehicle:$300. Leasing Cost of Passenger Vehicle:$800. Capital Cost of Auto: $30000Document1 pageLimitations: Interest Expense For Passenger Vehicle:$300. Leasing Cost of Passenger Vehicle:$800. Capital Cost of Auto: $30000f6linNo ratings yet

- Chapter 8 Fringe Benefits 220816140606 B881b1ceDocument37 pagesChapter 8 Fringe Benefits 220816140606 B881b1ceCPAREVIEWNo ratings yet

- Salary Tax CalculatorDocument7 pagesSalary Tax Calculatorbecito6195No ratings yet

- TAX 327 Employment Benefits Part 1 2021 - 1Document22 pagesTAX 327 Employment Benefits Part 1 2021 - 1mamitjasNo ratings yet

- EVR Withholding Tax & Other Common Tax Liabilities For Coops PDFDocument148 pagesEVR Withholding Tax & Other Common Tax Liabilities For Coops PDFTagrit TagritNo ratings yet

- ACCT604 Week 7 Lecture SlidesDocument29 pagesACCT604 Week 7 Lecture SlidesBuddika PrasannaNo ratings yet

- Bam031 Income Taxation P2 NotesDocument8 pagesBam031 Income Taxation P2 NotesRyan Malanum AbrioNo ratings yet

- Income From The Head "Salary"Document29 pagesIncome From The Head "Salary"Sahitya Kumar SheeNo ratings yet

- TOPIC 4b - EMPLOYMENT INCOME-typesDocument40 pagesTOPIC 4b - EMPLOYMENT INCOME-typesAgnesNo ratings yet

- Income Exclusion TAXDocument5 pagesIncome Exclusion TAXcamille howarthNo ratings yet

- Capital GainsDocument6 pagesCapital GainsMuskanDodejaNo ratings yet

- Wala LangDocument5 pagesWala LangHOSPITAL EMERGENCY ROOMNo ratings yet

- Withholding Tax SystemDocument73 pagesWithholding Tax SystemrickmortyNo ratings yet

- Chapter 3 Taxation Part 1Document28 pagesChapter 3 Taxation Part 1Alhysa Rosales CatapangNo ratings yet

- TaxationDocument12 pagesTaxationJames CasiaNo ratings yet

- Withholding Tax OverviewDocument16 pagesWithholding Tax OverviewMa. Corazon CaramalesNo ratings yet

- Fringe Benefit DeminimisDocument12 pagesFringe Benefit DeminimisMa. Angelica Celina MoralesNo ratings yet

- Notes To Income Tax (Compensation Income)Document1 pageNotes To Income Tax (Compensation Income)Aniza DucayNo ratings yet

- IAS 19 Employee BenefitsDocument22 pagesIAS 19 Employee Benefitsanon_419651076No ratings yet

- 13th Month PayDocument3 pages13th Month PayChristine GalsimNo ratings yet

- IAS 19 Employee Benefits (2021)Document6 pagesIAS 19 Employee Benefits (2021)Tawanda Tatenda Herbert100% (1)

- Week 8 Inclusions and Exclusions From The Gross Income 2023 24 1Document102 pagesWeek 8 Inclusions and Exclusions From The Gross Income 2023 24 1Arellano Rhovic R.No ratings yet

- Chapter 10 Compensation IncomeDocument6 pagesChapter 10 Compensation IncomeMary Jane Pabroa100% (2)

- Chapter 3: Fringe Benefits Tax and de Minimis Benefits Fringe BenefitDocument8 pagesChapter 3: Fringe Benefits Tax and de Minimis Benefits Fringe BenefitMARIA BELEN GUTIERREZNo ratings yet

- Business Income NotesDocument10 pagesBusiness Income NotesGODBARNo ratings yet

- The Withholding Tax SystemDocument191 pagesThe Withholding Tax SystemDa Yani ChristeeneNo ratings yet

- Chapter 8 Exclusions From Gross IncomeDocument4 pagesChapter 8 Exclusions From Gross IncomeMary Jane PabroaNo ratings yet

- Fringe Benefits: Paragraph 6 (1) (A)Document11 pagesFringe Benefits: Paragraph 6 (1) (A)takundaNo ratings yet

- Fringe Benefit GuideDocument91 pagesFringe Benefit GuideJeff MartinsonNo ratings yet

- Tax Proof Submission Document 2022-23Document7 pagesTax Proof Submission Document 2022-23Jagadeesh DatlaNo ratings yet

- Lecture Notes - IAS 19Document14 pagesLecture Notes - IAS 19Muhammed NaqiNo ratings yet

- Exclusion of Gross IncomeDocument16 pagesExclusion of Gross IncomeAce ReytaNo ratings yet

- Review Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020Document28 pagesReview Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020AB CloydNo ratings yet

- Gifts Distinguished From ExchangeDocument7 pagesGifts Distinguished From ExchangedailydoseoflawNo ratings yet

- IND AS 19 Employee BenefitsDocument9 pagesIND AS 19 Employee BenefitsPavan Kumar PurohitNo ratings yet

- Taxable Fringe Benefit Guide: Federal, State, and Local Governments The Internal Revenue ServiceDocument91 pagesTaxable Fringe Benefit Guide: Federal, State, and Local Governments The Internal Revenue ServiceJoseph ThompsonNo ratings yet

- Ias 19 Employee BenefitsDocument43 pagesIas 19 Employee BenefitsHasan Ali BokhariNo ratings yet

- SalaryDocument11 pagesSalaryshreshthasethi05No ratings yet

- FS2122-INCOMETAX-02: BSA 1202 Atty. F. R. SorianoDocument11 pagesFS2122-INCOMETAX-02: BSA 1202 Atty. F. R. SorianoKatring O.No ratings yet

- Tax 327 Fringe Benefits PART 2 - 2021Document37 pagesTax 327 Fringe Benefits PART 2 - 2021mamitjasNo ratings yet

- PGDM Seniors: Tax Planning and Financial ManagementDocument12 pagesPGDM Seniors: Tax Planning and Financial Managementbanerjee arupNo ratings yet

- Assignment Semester 1 Cycle 6 ( (Fa) )Document135 pagesAssignment Semester 1 Cycle 6 ( (Fa) )Sumaya100% (1)

- 53rd-55th BPSC Combined Competitive (Main) Exam GENERAL STUDIES Question Paper 2012Document2 pages53rd-55th BPSC Combined Competitive (Main) Exam GENERAL STUDIES Question Paper 2012mevrick_guyNo ratings yet

- Sales Return, Credit, and Debit MemoDocument2 pagesSales Return, Credit, and Debit MemoKnp ChowdaryNo ratings yet

- Accounting, Auditing Audit Com Sec-3Document41 pagesAccounting, Auditing Audit Com Sec-3Sagun Lal AmatyaNo ratings yet

- F9 Acowtancy Notes PDFDocument202 pagesF9 Acowtancy Notes PDFKodwoPNo ratings yet

- GPPB Foreign BiddersDocument9 pagesGPPB Foreign BiddersMi CoNo ratings yet

- Informal Urbanism Dan Layout PerumahanDocument46 pagesInformal Urbanism Dan Layout Perumahanalfariz haidarNo ratings yet

- Oe He Ur NursingDocument78 pagesOe He Ur NursingSA RAINo ratings yet

- Measuring The Success of Strategic InitiativesDocument23 pagesMeasuring The Success of Strategic InitiativesShuhaime IshakNo ratings yet

- Accounting Process of A Services BusinessDocument9 pagesAccounting Process of A Services BusinessFiverr RallNo ratings yet

- Blue Finance Instruments Development Guideline BappenasDocument36 pagesBlue Finance Instruments Development Guideline BappenasDota ImamNo ratings yet

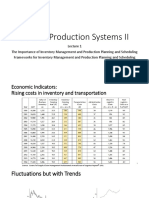

- Chapter 1 Importance of Inventory Management and Production SystemsDocument39 pagesChapter 1 Importance of Inventory Management and Production Systemsjane chahineNo ratings yet

- Tender Document For Purchase Of: Turnkey Project For Supply of STP Tender Number: 6000012984/SAFETY, Dated: 11.05.2019Document51 pagesTender Document For Purchase Of: Turnkey Project For Supply of STP Tender Number: 6000012984/SAFETY, Dated: 11.05.2019aneile liegiseNo ratings yet

- Business Combination: Consolidated Financial StatementsDocument9 pagesBusiness Combination: Consolidated Financial StatementsJuuzuu GearNo ratings yet

- Project For Textile & Apparel Ind. Future Challanges in PAKISTANDocument141 pagesProject For Textile & Apparel Ind. Future Challanges in PAKISTANM.TauqeerNo ratings yet

- Guide To Developing Skatepark FacilitiesDocument17 pagesGuide To Developing Skatepark FacilitiesLucianaNo ratings yet

- 2017 Equipment Leasing & FinanceDocument24 pages2017 Equipment Leasing & FinanceIndranil MandalNo ratings yet

- Challan 431798 02052018 112519 PDFDocument1 pageChallan 431798 02052018 112519 PDFchandrikaNo ratings yet

- Managing FOREX ExposureDocument23 pagesManaging FOREX ExposureCijil Diclause0% (1)

- Is OutriggerDocument4 pagesIs OutriggerSoffia DompreNo ratings yet

- M & A - AssignmentDocument2 pagesM & A - AssignmentrajdeboyNo ratings yet

- Introduction To Quality Management System and Process ImprovementDocument14 pagesIntroduction To Quality Management System and Process Improvementanne pascuaNo ratings yet

- Sample Test For Chapter 1Document40 pagesSample Test For Chapter 1Ha KimNo ratings yet

- XH-IAS 40 Investment Properties - SV-Out-of-class practice-EN NewDocument6 pagesXH-IAS 40 Investment Properties - SV-Out-of-class practice-EN NewHà Mai VõNo ratings yet

- هياكل الاستعانة بمصادر خارجية PDFDocument20 pagesهياكل الاستعانة بمصادر خارجية PDFNamira RefoufiNo ratings yet

- Preface: The 9th International Conference On Global Resource Conservation (ICGRC) and AJI From Ritsumeikan UniversityDocument2 pagesPreface: The 9th International Conference On Global Resource Conservation (ICGRC) and AJI From Ritsumeikan UniversityAdriani HasyimNo ratings yet

- BASF, CD&R Sell Solenis To Platinum Equity For $5.25 BillionDocument4 pagesBASF, CD&R Sell Solenis To Platinum Equity For $5.25 BillionCDI Global IndiaNo ratings yet

- Content ServerDocument26 pagesContent Serverdepiwos852No ratings yet

Download as pdf or txt

You might also like

- Chapter 6Document24 pagesChapter 6jake doinog88% (16)

- Land Economics - Lecture 1aDocument18 pagesLand Economics - Lecture 1aSixd WaznineNo ratings yet

- Buckwold 21e - CH 4 Selected SolutionsDocument18 pagesBuckwold 21e - CH 4 Selected SolutionsLucy50% (2)

- Fringe Benefits 1Document56 pagesFringe Benefits 1mattnoowinNo ratings yet

- Gross Income: Learning ObjectivesDocument12 pagesGross Income: Learning ObjectivesClaire BarbaNo ratings yet

- Unit 2 SalaryDocument131 pagesUnit 2 SalaryRekha BansalNo ratings yet

- TAX 228 2023 - Special InclusionsDocument29 pagesTAX 228 2023 - Special InclusionsedwardsyaameenNo ratings yet

- Gross Income Regular Tax: MARCH 2019Document57 pagesGross Income Regular Tax: MARCH 2019tyineNo ratings yet

- Gross Income Regular TaxDocument51 pagesGross Income Regular TaxElizalen MacarilayNo ratings yet

- 6.0 INDIVIDUALS PART 3 Fringe Benefit Tax and de Minimis BenefitsDocument41 pages6.0 INDIVIDUALS PART 3 Fringe Benefit Tax and de Minimis BenefitsAllan BacudioNo ratings yet

- 06 Gross IncomeDocument103 pages06 Gross IncomeJSNo ratings yet

- Is The Higher BetweenDocument4 pagesIs The Higher Betweenleshz zynNo ratings yet

- For Session DTD 5th Sep by CA Alok Garg PDFDocument46 pagesFor Session DTD 5th Sep by CA Alok Garg PDFLakshmi Narayana Murthy KapavarapuNo ratings yet

- Chapter 3 Employment Income A 202Document79 pagesChapter 3 Employment Income A 202ateen rizalmanNo ratings yet

- Inclusion and Exclusion of Gross IncomeDocument70 pagesInclusion and Exclusion of Gross IncomeEnola HeitsgerNo ratings yet

- Fringe Benefits TaxDocument11 pagesFringe Benefits Taxkenshin sclanimirNo ratings yet

- Taxation Granada LaynoDocument13 pagesTaxation Granada LaynosimpatheticoNo ratings yet

- Special Allowable Itemized DeductionsDocument6 pagesSpecial Allowable Itemized DeductionsChristine RaizNo ratings yet

- Tax Chapter 10, 11, 12Document13 pagesTax Chapter 10, 11, 12Sheraldine MendozaNo ratings yet

- Limitations: Interest Expense For Passenger Vehicle:$300. Leasing Cost of Passenger Vehicle:$800. Capital Cost of Auto: $30000Document1 pageLimitations: Interest Expense For Passenger Vehicle:$300. Leasing Cost of Passenger Vehicle:$800. Capital Cost of Auto: $30000f6linNo ratings yet

- Chapter 8 Fringe Benefits 220816140606 B881b1ceDocument37 pagesChapter 8 Fringe Benefits 220816140606 B881b1ceCPAREVIEWNo ratings yet

- Salary Tax CalculatorDocument7 pagesSalary Tax Calculatorbecito6195No ratings yet

- TAX 327 Employment Benefits Part 1 2021 - 1Document22 pagesTAX 327 Employment Benefits Part 1 2021 - 1mamitjasNo ratings yet

- EVR Withholding Tax & Other Common Tax Liabilities For Coops PDFDocument148 pagesEVR Withholding Tax & Other Common Tax Liabilities For Coops PDFTagrit TagritNo ratings yet

- ACCT604 Week 7 Lecture SlidesDocument29 pagesACCT604 Week 7 Lecture SlidesBuddika PrasannaNo ratings yet

- Bam031 Income Taxation P2 NotesDocument8 pagesBam031 Income Taxation P2 NotesRyan Malanum AbrioNo ratings yet

- Income From The Head "Salary"Document29 pagesIncome From The Head "Salary"Sahitya Kumar SheeNo ratings yet

- TOPIC 4b - EMPLOYMENT INCOME-typesDocument40 pagesTOPIC 4b - EMPLOYMENT INCOME-typesAgnesNo ratings yet

- Income Exclusion TAXDocument5 pagesIncome Exclusion TAXcamille howarthNo ratings yet

- Capital GainsDocument6 pagesCapital GainsMuskanDodejaNo ratings yet

- Wala LangDocument5 pagesWala LangHOSPITAL EMERGENCY ROOMNo ratings yet

- Withholding Tax SystemDocument73 pagesWithholding Tax SystemrickmortyNo ratings yet

- Chapter 3 Taxation Part 1Document28 pagesChapter 3 Taxation Part 1Alhysa Rosales CatapangNo ratings yet

- TaxationDocument12 pagesTaxationJames CasiaNo ratings yet

- Withholding Tax OverviewDocument16 pagesWithholding Tax OverviewMa. Corazon CaramalesNo ratings yet

- Fringe Benefit DeminimisDocument12 pagesFringe Benefit DeminimisMa. Angelica Celina MoralesNo ratings yet

- Notes To Income Tax (Compensation Income)Document1 pageNotes To Income Tax (Compensation Income)Aniza DucayNo ratings yet

- IAS 19 Employee BenefitsDocument22 pagesIAS 19 Employee Benefitsanon_419651076No ratings yet

- 13th Month PayDocument3 pages13th Month PayChristine GalsimNo ratings yet

- IAS 19 Employee Benefits (2021)Document6 pagesIAS 19 Employee Benefits (2021)Tawanda Tatenda Herbert100% (1)

- Week 8 Inclusions and Exclusions From The Gross Income 2023 24 1Document102 pagesWeek 8 Inclusions and Exclusions From The Gross Income 2023 24 1Arellano Rhovic R.No ratings yet

- Chapter 10 Compensation IncomeDocument6 pagesChapter 10 Compensation IncomeMary Jane Pabroa100% (2)

- Chapter 3: Fringe Benefits Tax and de Minimis Benefits Fringe BenefitDocument8 pagesChapter 3: Fringe Benefits Tax and de Minimis Benefits Fringe BenefitMARIA BELEN GUTIERREZNo ratings yet

- Business Income NotesDocument10 pagesBusiness Income NotesGODBARNo ratings yet

- The Withholding Tax SystemDocument191 pagesThe Withholding Tax SystemDa Yani ChristeeneNo ratings yet

- Chapter 8 Exclusions From Gross IncomeDocument4 pagesChapter 8 Exclusions From Gross IncomeMary Jane PabroaNo ratings yet

- Fringe Benefits: Paragraph 6 (1) (A)Document11 pagesFringe Benefits: Paragraph 6 (1) (A)takundaNo ratings yet

- Fringe Benefit GuideDocument91 pagesFringe Benefit GuideJeff MartinsonNo ratings yet

- Tax Proof Submission Document 2022-23Document7 pagesTax Proof Submission Document 2022-23Jagadeesh DatlaNo ratings yet

- Lecture Notes - IAS 19Document14 pagesLecture Notes - IAS 19Muhammed NaqiNo ratings yet

- Exclusion of Gross IncomeDocument16 pagesExclusion of Gross IncomeAce ReytaNo ratings yet

- Review Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020Document28 pagesReview Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020AB CloydNo ratings yet

- Gifts Distinguished From ExchangeDocument7 pagesGifts Distinguished From ExchangedailydoseoflawNo ratings yet

- IND AS 19 Employee BenefitsDocument9 pagesIND AS 19 Employee BenefitsPavan Kumar PurohitNo ratings yet

- Taxable Fringe Benefit Guide: Federal, State, and Local Governments The Internal Revenue ServiceDocument91 pagesTaxable Fringe Benefit Guide: Federal, State, and Local Governments The Internal Revenue ServiceJoseph ThompsonNo ratings yet

- Ias 19 Employee BenefitsDocument43 pagesIas 19 Employee BenefitsHasan Ali BokhariNo ratings yet

- SalaryDocument11 pagesSalaryshreshthasethi05No ratings yet

- FS2122-INCOMETAX-02: BSA 1202 Atty. F. R. SorianoDocument11 pagesFS2122-INCOMETAX-02: BSA 1202 Atty. F. R. SorianoKatring O.No ratings yet

- Tax 327 Fringe Benefits PART 2 - 2021Document37 pagesTax 327 Fringe Benefits PART 2 - 2021mamitjasNo ratings yet

- PGDM Seniors: Tax Planning and Financial ManagementDocument12 pagesPGDM Seniors: Tax Planning and Financial Managementbanerjee arupNo ratings yet

- Assignment Semester 1 Cycle 6 ( (Fa) )Document135 pagesAssignment Semester 1 Cycle 6 ( (Fa) )Sumaya100% (1)

- 53rd-55th BPSC Combined Competitive (Main) Exam GENERAL STUDIES Question Paper 2012Document2 pages53rd-55th BPSC Combined Competitive (Main) Exam GENERAL STUDIES Question Paper 2012mevrick_guyNo ratings yet

- Sales Return, Credit, and Debit MemoDocument2 pagesSales Return, Credit, and Debit MemoKnp ChowdaryNo ratings yet

- Accounting, Auditing Audit Com Sec-3Document41 pagesAccounting, Auditing Audit Com Sec-3Sagun Lal AmatyaNo ratings yet

- F9 Acowtancy Notes PDFDocument202 pagesF9 Acowtancy Notes PDFKodwoPNo ratings yet

- GPPB Foreign BiddersDocument9 pagesGPPB Foreign BiddersMi CoNo ratings yet

- Informal Urbanism Dan Layout PerumahanDocument46 pagesInformal Urbanism Dan Layout Perumahanalfariz haidarNo ratings yet

- Oe He Ur NursingDocument78 pagesOe He Ur NursingSA RAINo ratings yet

- Measuring The Success of Strategic InitiativesDocument23 pagesMeasuring The Success of Strategic InitiativesShuhaime IshakNo ratings yet

- Accounting Process of A Services BusinessDocument9 pagesAccounting Process of A Services BusinessFiverr RallNo ratings yet

- Blue Finance Instruments Development Guideline BappenasDocument36 pagesBlue Finance Instruments Development Guideline BappenasDota ImamNo ratings yet

- Chapter 1 Importance of Inventory Management and Production SystemsDocument39 pagesChapter 1 Importance of Inventory Management and Production Systemsjane chahineNo ratings yet

- Tender Document For Purchase Of: Turnkey Project For Supply of STP Tender Number: 6000012984/SAFETY, Dated: 11.05.2019Document51 pagesTender Document For Purchase Of: Turnkey Project For Supply of STP Tender Number: 6000012984/SAFETY, Dated: 11.05.2019aneile liegiseNo ratings yet

- Business Combination: Consolidated Financial StatementsDocument9 pagesBusiness Combination: Consolidated Financial StatementsJuuzuu GearNo ratings yet

- Project For Textile & Apparel Ind. Future Challanges in PAKISTANDocument141 pagesProject For Textile & Apparel Ind. Future Challanges in PAKISTANM.TauqeerNo ratings yet

- Guide To Developing Skatepark FacilitiesDocument17 pagesGuide To Developing Skatepark FacilitiesLucianaNo ratings yet

- 2017 Equipment Leasing & FinanceDocument24 pages2017 Equipment Leasing & FinanceIndranil MandalNo ratings yet

- Challan 431798 02052018 112519 PDFDocument1 pageChallan 431798 02052018 112519 PDFchandrikaNo ratings yet

- Managing FOREX ExposureDocument23 pagesManaging FOREX ExposureCijil Diclause0% (1)

- Is OutriggerDocument4 pagesIs OutriggerSoffia DompreNo ratings yet

- M & A - AssignmentDocument2 pagesM & A - AssignmentrajdeboyNo ratings yet

- Introduction To Quality Management System and Process ImprovementDocument14 pagesIntroduction To Quality Management System and Process Improvementanne pascuaNo ratings yet

- Sample Test For Chapter 1Document40 pagesSample Test For Chapter 1Ha KimNo ratings yet

- XH-IAS 40 Investment Properties - SV-Out-of-class practice-EN NewDocument6 pagesXH-IAS 40 Investment Properties - SV-Out-of-class practice-EN NewHà Mai VõNo ratings yet

- هياكل الاستعانة بمصادر خارجية PDFDocument20 pagesهياكل الاستعانة بمصادر خارجية PDFNamira RefoufiNo ratings yet

- Preface: The 9th International Conference On Global Resource Conservation (ICGRC) and AJI From Ritsumeikan UniversityDocument2 pagesPreface: The 9th International Conference On Global Resource Conservation (ICGRC) and AJI From Ritsumeikan UniversityAdriani HasyimNo ratings yet

- BASF, CD&R Sell Solenis To Platinum Equity For $5.25 BillionDocument4 pagesBASF, CD&R Sell Solenis To Platinum Equity For $5.25 BillionCDI Global IndiaNo ratings yet

- Content ServerDocument26 pagesContent Serverdepiwos852No ratings yet