SBR合并报表题草稿

SBR合并报表题草稿

You might also like

- BUA4002 - Assignment - Part - 3Document23 pagesBUA4002 - Assignment - Part - 3julenjoe2No ratings yet

- DanitaCronkhite1 MT 482 Assignment Unit 7Document10 pagesDanitaCronkhite1 MT 482 Assignment Unit 7leeyaa aNo ratings yet

- Enago Recuitment HandbookDocument19 pagesEnago Recuitment Handbookgreg232No ratings yet

- Case 50 Flinder Valves and Controls IncDocument24 pagesCase 50 Flinder Valves and Controls IncBlatta Orientalis0% (1)

- Socialized Housing in The Philippines IsDocument33 pagesSocialized Housing in The Philippines IsReigneth VillenaNo ratings yet

- PWCFinancialDocument92 pagesPWCFinancialgshearod2uNo ratings yet

- Zach WeinerSmith Polystate v7Document73 pagesZach WeinerSmith Polystate v7Matthew HutchinsNo ratings yet

- Ey Aarsrapport 2021 22 12Document1 pageEy Aarsrapport 2021 22 12Ronald RunruilNo ratings yet

- Ey Aarsrapport 2021 22 12Document1 pageEy Aarsrapport 2021 22 12Ronald RunruilNo ratings yet

- Kel Annual AccountsDocument14 pagesKel Annual AccountsmrordinaryNo ratings yet

- Acc319 - Take-Home Act - Financial ModelDocument24 pagesAcc319 - Take-Home Act - Financial Modeljpalisoc204No ratings yet

- Ermenegildo Zegna N.V. (ZGN)Document2 pagesErmenegildo Zegna N.V. (ZGN)Carlos Suárez MatosNo ratings yet

- Britannia X Ls XDocument15 pagesBritannia X Ls Xshubham9308No ratings yet

- Spreadsheet 9M21Document14 pagesSpreadsheet 9M21Salah HusseinNo ratings yet

- Asian Paints Ltd. (India) : SourceDocument6 pagesAsian Paints Ltd. (India) : SourceDivyagarapatiNo ratings yet

- Asian PaintsDocument6 pagesAsian PaintsDivyagarapatiNo ratings yet

- Financial Statement Analysis Group-3Document19 pagesFinancial Statement Analysis Group-3MostakNo ratings yet

- Resus Energy PLC: Interim Report 01st Quarter 2022-2023Document13 pagesResus Energy PLC: Interim Report 01st Quarter 2022-2023w.chathura nuwan ranasingheNo ratings yet

- SBR Excel PracticeDocument8 pagesSBR Excel PracticeMD SAIFUL ISLAMNo ratings yet

- 5 URD 2023 - Consolidated Financial StatementsDocument80 pages5 URD 2023 - Consolidated Financial Statementschaimae bejjaNo ratings yet

- Industry Segment of Bajaj CompanyDocument4 pagesIndustry Segment of Bajaj CompanysantunusorenNo ratings yet

- Marico BSDocument2 pagesMarico BSAbhay Kumar SinghNo ratings yet

- American Airlines Group IncDocument5 pagesAmerican Airlines Group IncMyka Mabs MagbanuaNo ratings yet

- This Spreadsheet Supports The Analysis of The Case "Flinder Valves and Controls Inc." (Case 43)Document17 pagesThis Spreadsheet Supports The Analysis of The Case "Flinder Valves and Controls Inc." (Case 43)Lalang PalambangNo ratings yet

- UBL Consolidated Finanical Statements 2021Document91 pagesUBL Consolidated Finanical Statements 2021Aftab JamilNo ratings yet

- 8 - Procter GambalDocument40 pages8 - Procter GambalPranali SanasNo ratings yet

- UBL Annual Consolidated Financial Statments 2022Document92 pagesUBL Annual Consolidated Financial Statments 2022abdullahazaim55No ratings yet

- Assets FY 2075/76 FY 2074/75 FY 2073/74 FY 2072/73 FY 2071/72Document1 pageAssets FY 2075/76 FY 2074/75 FY 2073/74 FY 2072/73 FY 2071/72Girja AutomotiveNo ratings yet

- Group AssignmentDocument4 pagesGroup Assignment1954032027cucNo ratings yet

- Análisis Fundamental: USD in Millions Except Per Share Data. 2014 2015 2016 2017 2018Document8 pagesAnálisis Fundamental: USD in Millions Except Per Share Data. 2014 2015 2016 2017 2018andusotoNo ratings yet

- Wipro Ltd. (India) : SourceDocument6 pagesWipro Ltd. (India) : SourceDivyagarapatiNo ratings yet

- Dr. Reddy's Laboratories Ltd. (India) : SourceDocument6 pagesDr. Reddy's Laboratories Ltd. (India) : SourceDivyagarapatiNo ratings yet

- Balance Sheet & P & LDocument3 pagesBalance Sheet & P & LSatish WagholeNo ratings yet

- Balance Sheet of Gujarat Alkalies and ChemicalsDocument8 pagesBalance Sheet of Gujarat Alkalies and ChemicalsrotiNo ratings yet

- Guj AlkaliDocument8 pagesGuj AlkalirotiNo ratings yet

- Guj AlkaliDocument8 pagesGuj AlkalirotiNo ratings yet

- 566647370.xls - R15.1 DvorakDocument9 pages566647370.xls - R15.1 DvorakleuleuNo ratings yet

- CapitaLand Limited SGX C31 Financials Income StatementDocument3 pagesCapitaLand Limited SGX C31 Financials Income StatementElvin TanNo ratings yet

- Business ForecastingDocument6 pagesBusiness ForecastingRahat Mahmud ShoebNo ratings yet

- GRP Balance Sheet Structure Merck Ar23Document1 pageGRP Balance Sheet Structure Merck Ar23HA NGUYEN THUYNo ratings yet

- Financial Summary: Annual Report 2076/77Document1 pageFinancial Summary: Annual Report 2076/77Panchakanya SaccosNo ratings yet

- Adani Green Balance SheetDocument2 pagesAdani Green Balance SheetTaksh DhamiNo ratings yet

- Financials 1620828-23.03.25Document6 pagesFinancials 1620828-23.03.25Levin OliverNo ratings yet

- BookDocument4 pagesBookspj1962001No ratings yet

- Financial Report Krishnapalsinh-20Document11 pagesFinancial Report Krishnapalsinh-20Mansi GoelNo ratings yet

- Wassim Zhani Texas Roadhouse Financial Statements 2006-2009Document14 pagesWassim Zhani Texas Roadhouse Financial Statements 2006-2009wassim zhaniNo ratings yet

- Gujarat Narmada Valley Fertilizers & ChemicalsDocument14 pagesGujarat Narmada Valley Fertilizers & ChemicalsPrashant TiwariNo ratings yet

- StateHouse Holdings Inc - Form Interim Financial Statements (Nov-22-2022)Document60 pagesStateHouse Holdings Inc - Form Interim Financial Statements (Nov-22-2022)ScridbyNo ratings yet

- FMDocument8 pagesFMesmailkarimi456No ratings yet

- BRD - 20230208074925 - BRD IFRS December 2022 ENDocument3 pagesBRD - 20230208074925 - BRD IFRS December 2022 ENteoxysNo ratings yet

- Financial Ratio Analysis: (AIA Engineering LTD.)Document14 pagesFinancial Ratio Analysis: (AIA Engineering LTD.)kalathiadhavalNo ratings yet

- Sample FS Schedule 3 Tool For CompaniesDocument20 pagesSample FS Schedule 3 Tool For CompaniesGirish HNo ratings yet

- UPL Ltd. (India) : SourceDocument6 pagesUPL Ltd. (India) : SourceDivyagarapatiNo ratings yet

- HCL Technologies LTD (HCLT IN) - StandardizedDocument6 pagesHCL Technologies LTD (HCLT IN) - StandardizedAswini Kumar BhuyanNo ratings yet

- DCF ModelDocument5 pagesDCF Modelibs56225No ratings yet

- Trần Đức Thái AssignmentDocument38 pagesTrần Đức Thái AssignmentThái TranNo ratings yet

- ClairantDocument2 pagesClairantABHAY KUMAR SINGHNo ratings yet

- Acc 1Document3 pagesAcc 1Mayank RelanNo ratings yet

- 9539 MUH QR 2023-06-30 MUHQ420230630Result 71098896Document15 pages9539 MUH QR 2023-06-30 MUHQ420230630Result 71098896Eugene OngNo ratings yet

- Balance Sheet of ZEE NETWORK (Rs in Crores)Document12 pagesBalance Sheet of ZEE NETWORK (Rs in Crores)abid ali khanNo ratings yet

- Accltd.: Balance Sheet Summary: Dec 2010 - Dec 2019: Non-Annualised: Rs. CroreDocument59 pagesAccltd.: Balance Sheet Summary: Dec 2010 - Dec 2019: Non-Annualised: Rs. Crorehardik aroraNo ratings yet

- Standalone Bal SheetDocument2 pagesStandalone Bal SheetvaidyaaadiNo ratings yet

- Book 2Document2 pagesBook 2Piyush JainNo ratings yet

- Chapter 2 & 3 SummaryDocument3 pagesChapter 2 & 3 SummaryIqra 2000No ratings yet

- Islam and Communism PDFDocument0 pagesIslam and Communism PDFAMEEN AKBAR100% (1)

- Couples BudgetDocument6 pagesCouples BudgetIzamar RiveraNo ratings yet

- CV & ResumeDocument9 pagesCV & ResumeNurhidayati KeriyunNo ratings yet

- 4-13B. Wage and Tax Statement: Omni Corporation 4800 River Road Philadelphia, PA 19113-5548Document4 pages4-13B. Wage and Tax Statement: Omni Corporation 4800 River Road Philadelphia, PA 19113-5548KrisnaNo ratings yet

- Income Tax-Atty. CabanDocument4 pagesIncome Tax-Atty. CabanCelyn PalacolNo ratings yet

- Tourism and Environment NepalDocument9 pagesTourism and Environment NepalPrakash KarnNo ratings yet

- InvoiceDocument1 pageInvoicedevanshupal0101No ratings yet

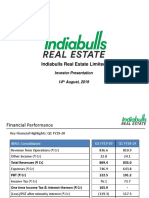

- Indiabulls Real Estate Limited: Investor Presentation 14 August, 2019Document41 pagesIndiabulls Real Estate Limited: Investor Presentation 14 August, 2019slohariNo ratings yet

- 1st and 2nd Batch of Cases CORPORATION LAWDocument132 pages1st and 2nd Batch of Cases CORPORATION LAWToh YangNo ratings yet

- Solutions Manual To Accompany International Corporate Finance 9780073530666Document4 pagesSolutions Manual To Accompany International Corporate Finance 9780073530666JamieBerrypdey100% (52)

- 2016-11 Aeoi Self-Certif SQB Static Indiv. (En) v1Document1 page2016-11 Aeoi Self-Certif SQB Static Indiv. (En) v1AswanTajuddinNo ratings yet

- Land Purchase and Sale Agreement Templates - LegalDocument4 pagesLand Purchase and Sale Agreement Templates - LegalAlekz PicarNo ratings yet

- DonationDocument9 pagesDonationArline B. FuentesNo ratings yet

- Srinivas SAP Withholding TaxDocument3 pagesSrinivas SAP Withholding TaxsrinivasNo ratings yet

- SOAL Kuis Materi UAS Inter 2Document2 pagesSOAL Kuis Materi UAS Inter 2vania 322019087No ratings yet

- Ratio AnalysisDocument6 pagesRatio AnalysisSaswat NandaNo ratings yet

- May 2023 PayslipDocument1 pageMay 2023 Payslipdorcas baduNo ratings yet

- Faisal Cargo Quotation +profileDocument3 pagesFaisal Cargo Quotation +profilekhawjaarslanNo ratings yet

- Certified Wealth ManagerDocument10 pagesCertified Wealth ManagerRicky MartinNo ratings yet

- CFMcorpDocument1 pageCFMcorpnavimala85No ratings yet

- Interpretation of StatuesDocument17 pagesInterpretation of Statuessandeepa koppulaNo ratings yet

- 2016-02 Cvmena Mag #5Document108 pages2016-02 Cvmena Mag #5Connecting Voices MENANo ratings yet

- Remegio Miñoza - January 2024 SoaDocument3 pagesRemegio Miñoza - January 2024 Soaseanrain396No ratings yet

- Prediction of Equity Price in Stock MarketDocument76 pagesPrediction of Equity Price in Stock MarketPrem KumarNo ratings yet

- Chapter 33 PFRS 5 Discontinued OperationsDocument2 pagesChapter 33 PFRS 5 Discontinued OperationsstudentoneNo ratings yet

Download as xlsx, pdf, or txt

You might also like

- BUA4002 - Assignment - Part - 3Document23 pagesBUA4002 - Assignment - Part - 3julenjoe2No ratings yet

- DanitaCronkhite1 MT 482 Assignment Unit 7Document10 pagesDanitaCronkhite1 MT 482 Assignment Unit 7leeyaa aNo ratings yet

- Enago Recuitment HandbookDocument19 pagesEnago Recuitment Handbookgreg232No ratings yet

- Case 50 Flinder Valves and Controls IncDocument24 pagesCase 50 Flinder Valves and Controls IncBlatta Orientalis0% (1)

- Socialized Housing in The Philippines IsDocument33 pagesSocialized Housing in The Philippines IsReigneth VillenaNo ratings yet

- PWCFinancialDocument92 pagesPWCFinancialgshearod2uNo ratings yet

- Zach WeinerSmith Polystate v7Document73 pagesZach WeinerSmith Polystate v7Matthew HutchinsNo ratings yet

- Ey Aarsrapport 2021 22 12Document1 pageEy Aarsrapport 2021 22 12Ronald RunruilNo ratings yet

- Ey Aarsrapport 2021 22 12Document1 pageEy Aarsrapport 2021 22 12Ronald RunruilNo ratings yet

- Kel Annual AccountsDocument14 pagesKel Annual AccountsmrordinaryNo ratings yet

- Acc319 - Take-Home Act - Financial ModelDocument24 pagesAcc319 - Take-Home Act - Financial Modeljpalisoc204No ratings yet

- Ermenegildo Zegna N.V. (ZGN)Document2 pagesErmenegildo Zegna N.V. (ZGN)Carlos Suárez MatosNo ratings yet

- Britannia X Ls XDocument15 pagesBritannia X Ls Xshubham9308No ratings yet

- Spreadsheet 9M21Document14 pagesSpreadsheet 9M21Salah HusseinNo ratings yet

- Asian Paints Ltd. (India) : SourceDocument6 pagesAsian Paints Ltd. (India) : SourceDivyagarapatiNo ratings yet

- Asian PaintsDocument6 pagesAsian PaintsDivyagarapatiNo ratings yet

- Financial Statement Analysis Group-3Document19 pagesFinancial Statement Analysis Group-3MostakNo ratings yet

- Resus Energy PLC: Interim Report 01st Quarter 2022-2023Document13 pagesResus Energy PLC: Interim Report 01st Quarter 2022-2023w.chathura nuwan ranasingheNo ratings yet

- SBR Excel PracticeDocument8 pagesSBR Excel PracticeMD SAIFUL ISLAMNo ratings yet

- 5 URD 2023 - Consolidated Financial StatementsDocument80 pages5 URD 2023 - Consolidated Financial Statementschaimae bejjaNo ratings yet

- Industry Segment of Bajaj CompanyDocument4 pagesIndustry Segment of Bajaj CompanysantunusorenNo ratings yet

- Marico BSDocument2 pagesMarico BSAbhay Kumar SinghNo ratings yet

- American Airlines Group IncDocument5 pagesAmerican Airlines Group IncMyka Mabs MagbanuaNo ratings yet

- This Spreadsheet Supports The Analysis of The Case "Flinder Valves and Controls Inc." (Case 43)Document17 pagesThis Spreadsheet Supports The Analysis of The Case "Flinder Valves and Controls Inc." (Case 43)Lalang PalambangNo ratings yet

- UBL Consolidated Finanical Statements 2021Document91 pagesUBL Consolidated Finanical Statements 2021Aftab JamilNo ratings yet

- 8 - Procter GambalDocument40 pages8 - Procter GambalPranali SanasNo ratings yet

- UBL Annual Consolidated Financial Statments 2022Document92 pagesUBL Annual Consolidated Financial Statments 2022abdullahazaim55No ratings yet

- Assets FY 2075/76 FY 2074/75 FY 2073/74 FY 2072/73 FY 2071/72Document1 pageAssets FY 2075/76 FY 2074/75 FY 2073/74 FY 2072/73 FY 2071/72Girja AutomotiveNo ratings yet

- Group AssignmentDocument4 pagesGroup Assignment1954032027cucNo ratings yet

- Análisis Fundamental: USD in Millions Except Per Share Data. 2014 2015 2016 2017 2018Document8 pagesAnálisis Fundamental: USD in Millions Except Per Share Data. 2014 2015 2016 2017 2018andusotoNo ratings yet

- Wipro Ltd. (India) : SourceDocument6 pagesWipro Ltd. (India) : SourceDivyagarapatiNo ratings yet

- Dr. Reddy's Laboratories Ltd. (India) : SourceDocument6 pagesDr. Reddy's Laboratories Ltd. (India) : SourceDivyagarapatiNo ratings yet

- Balance Sheet & P & LDocument3 pagesBalance Sheet & P & LSatish WagholeNo ratings yet

- Balance Sheet of Gujarat Alkalies and ChemicalsDocument8 pagesBalance Sheet of Gujarat Alkalies and ChemicalsrotiNo ratings yet

- Guj AlkaliDocument8 pagesGuj AlkalirotiNo ratings yet

- Guj AlkaliDocument8 pagesGuj AlkalirotiNo ratings yet

- 566647370.xls - R15.1 DvorakDocument9 pages566647370.xls - R15.1 DvorakleuleuNo ratings yet

- CapitaLand Limited SGX C31 Financials Income StatementDocument3 pagesCapitaLand Limited SGX C31 Financials Income StatementElvin TanNo ratings yet

- Business ForecastingDocument6 pagesBusiness ForecastingRahat Mahmud ShoebNo ratings yet

- GRP Balance Sheet Structure Merck Ar23Document1 pageGRP Balance Sheet Structure Merck Ar23HA NGUYEN THUYNo ratings yet

- Financial Summary: Annual Report 2076/77Document1 pageFinancial Summary: Annual Report 2076/77Panchakanya SaccosNo ratings yet

- Adani Green Balance SheetDocument2 pagesAdani Green Balance SheetTaksh DhamiNo ratings yet

- Financials 1620828-23.03.25Document6 pagesFinancials 1620828-23.03.25Levin OliverNo ratings yet

- BookDocument4 pagesBookspj1962001No ratings yet

- Financial Report Krishnapalsinh-20Document11 pagesFinancial Report Krishnapalsinh-20Mansi GoelNo ratings yet

- Wassim Zhani Texas Roadhouse Financial Statements 2006-2009Document14 pagesWassim Zhani Texas Roadhouse Financial Statements 2006-2009wassim zhaniNo ratings yet

- Gujarat Narmada Valley Fertilizers & ChemicalsDocument14 pagesGujarat Narmada Valley Fertilizers & ChemicalsPrashant TiwariNo ratings yet

- StateHouse Holdings Inc - Form Interim Financial Statements (Nov-22-2022)Document60 pagesStateHouse Holdings Inc - Form Interim Financial Statements (Nov-22-2022)ScridbyNo ratings yet

- FMDocument8 pagesFMesmailkarimi456No ratings yet

- BRD - 20230208074925 - BRD IFRS December 2022 ENDocument3 pagesBRD - 20230208074925 - BRD IFRS December 2022 ENteoxysNo ratings yet

- Financial Ratio Analysis: (AIA Engineering LTD.)Document14 pagesFinancial Ratio Analysis: (AIA Engineering LTD.)kalathiadhavalNo ratings yet

- Sample FS Schedule 3 Tool For CompaniesDocument20 pagesSample FS Schedule 3 Tool For CompaniesGirish HNo ratings yet

- UPL Ltd. (India) : SourceDocument6 pagesUPL Ltd. (India) : SourceDivyagarapatiNo ratings yet

- HCL Technologies LTD (HCLT IN) - StandardizedDocument6 pagesHCL Technologies LTD (HCLT IN) - StandardizedAswini Kumar BhuyanNo ratings yet

- DCF ModelDocument5 pagesDCF Modelibs56225No ratings yet

- Trần Đức Thái AssignmentDocument38 pagesTrần Đức Thái AssignmentThái TranNo ratings yet

- ClairantDocument2 pagesClairantABHAY KUMAR SINGHNo ratings yet

- Acc 1Document3 pagesAcc 1Mayank RelanNo ratings yet

- 9539 MUH QR 2023-06-30 MUHQ420230630Result 71098896Document15 pages9539 MUH QR 2023-06-30 MUHQ420230630Result 71098896Eugene OngNo ratings yet

- Balance Sheet of ZEE NETWORK (Rs in Crores)Document12 pagesBalance Sheet of ZEE NETWORK (Rs in Crores)abid ali khanNo ratings yet

- Accltd.: Balance Sheet Summary: Dec 2010 - Dec 2019: Non-Annualised: Rs. CroreDocument59 pagesAccltd.: Balance Sheet Summary: Dec 2010 - Dec 2019: Non-Annualised: Rs. Crorehardik aroraNo ratings yet

- Standalone Bal SheetDocument2 pagesStandalone Bal SheetvaidyaaadiNo ratings yet

- Book 2Document2 pagesBook 2Piyush JainNo ratings yet

- Chapter 2 & 3 SummaryDocument3 pagesChapter 2 & 3 SummaryIqra 2000No ratings yet

- Islam and Communism PDFDocument0 pagesIslam and Communism PDFAMEEN AKBAR100% (1)

- Couples BudgetDocument6 pagesCouples BudgetIzamar RiveraNo ratings yet

- CV & ResumeDocument9 pagesCV & ResumeNurhidayati KeriyunNo ratings yet

- 4-13B. Wage and Tax Statement: Omni Corporation 4800 River Road Philadelphia, PA 19113-5548Document4 pages4-13B. Wage and Tax Statement: Omni Corporation 4800 River Road Philadelphia, PA 19113-5548KrisnaNo ratings yet

- Income Tax-Atty. CabanDocument4 pagesIncome Tax-Atty. CabanCelyn PalacolNo ratings yet

- Tourism and Environment NepalDocument9 pagesTourism and Environment NepalPrakash KarnNo ratings yet

- InvoiceDocument1 pageInvoicedevanshupal0101No ratings yet

- Indiabulls Real Estate Limited: Investor Presentation 14 August, 2019Document41 pagesIndiabulls Real Estate Limited: Investor Presentation 14 August, 2019slohariNo ratings yet

- 1st and 2nd Batch of Cases CORPORATION LAWDocument132 pages1st and 2nd Batch of Cases CORPORATION LAWToh YangNo ratings yet

- Solutions Manual To Accompany International Corporate Finance 9780073530666Document4 pagesSolutions Manual To Accompany International Corporate Finance 9780073530666JamieBerrypdey100% (52)

- 2016-11 Aeoi Self-Certif SQB Static Indiv. (En) v1Document1 page2016-11 Aeoi Self-Certif SQB Static Indiv. (En) v1AswanTajuddinNo ratings yet

- Land Purchase and Sale Agreement Templates - LegalDocument4 pagesLand Purchase and Sale Agreement Templates - LegalAlekz PicarNo ratings yet

- DonationDocument9 pagesDonationArline B. FuentesNo ratings yet

- Srinivas SAP Withholding TaxDocument3 pagesSrinivas SAP Withholding TaxsrinivasNo ratings yet

- SOAL Kuis Materi UAS Inter 2Document2 pagesSOAL Kuis Materi UAS Inter 2vania 322019087No ratings yet

- Ratio AnalysisDocument6 pagesRatio AnalysisSaswat NandaNo ratings yet

- May 2023 PayslipDocument1 pageMay 2023 Payslipdorcas baduNo ratings yet

- Faisal Cargo Quotation +profileDocument3 pagesFaisal Cargo Quotation +profilekhawjaarslanNo ratings yet

- Certified Wealth ManagerDocument10 pagesCertified Wealth ManagerRicky MartinNo ratings yet

- CFMcorpDocument1 pageCFMcorpnavimala85No ratings yet

- Interpretation of StatuesDocument17 pagesInterpretation of Statuessandeepa koppulaNo ratings yet

- 2016-02 Cvmena Mag #5Document108 pages2016-02 Cvmena Mag #5Connecting Voices MENANo ratings yet

- Remegio Miñoza - January 2024 SoaDocument3 pagesRemegio Miñoza - January 2024 Soaseanrain396No ratings yet

- Prediction of Equity Price in Stock MarketDocument76 pagesPrediction of Equity Price in Stock MarketPrem KumarNo ratings yet

- Chapter 33 PFRS 5 Discontinued OperationsDocument2 pagesChapter 33 PFRS 5 Discontinued OperationsstudentoneNo ratings yet