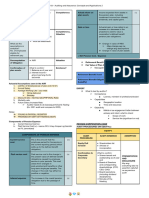

C3 - Intangible Assets

C3 - Intangible Assets

You might also like

- Audit Programs 21-3, 21-4, and 21-5Document3 pagesAudit Programs 21-3, 21-4, and 21-5Faaiz YousafNo ratings yet

- TN 34 The WM Wrigley JR Company Capital Structure Valuation and Cost of CapitalDocument108 pagesTN 34 The WM Wrigley JR Company Capital Structure Valuation and Cost of CapitalStanisla Lee0% (2)

- Nciii Bookkeeping PDFDocument28 pagesNciii Bookkeeping PDFStephanie Cruz100% (10)

- FABM2 Q1 Mod1 Statement-of-Financial-Position v2Document24 pagesFABM2 Q1 Mod1 Statement-of-Financial-Position v2randy magbudhi93% (15)

- 19h (12-00) Develop The Audit Program - Accrued Liabilities and Deferred IncomeDocument2 pages19h (12-00) Develop The Audit Program - Accrued Liabilities and Deferred IncomeTran AnhNo ratings yet

- Oceanview Marine Company Audit Programs 30-3, 30-4, 30-5Document3 pagesOceanview Marine Company Audit Programs 30-3, 30-4, 30-5rebecca0% (2)

- Accountant TestDocument3 pagesAccountant TestMax SuperNo ratings yet

- C1 PpeDocument14 pagesC1 Ppebanomehar524No ratings yet

- C1 - Property, Plant and Equipment 2017Document36 pagesC1 - Property, Plant and Equipment 2017banomehar524No ratings yet

- D11 - Cash and BankDocument12 pagesD11 - Cash and Bankbanomehar524No ratings yet

- D4 - Trade Debts 2018Document13 pagesD4 - Trade Debts 2018banomehar524No ratings yet

- Audit Programme Tangible Fixed AssetDocument8 pagesAudit Programme Tangible Fixed AssetfaheemNo ratings yet

- Rizwan & Co. Chartered Accountants: Completed by Schedule Reviewed by (SPS/AM) Reviewed by (Partner)Document3 pagesRizwan & Co. Chartered Accountants: Completed by Schedule Reviewed by (SPS/AM) Reviewed by (Partner)faheemNo ratings yet

- WP Asset B - Trade ReceivablesDocument15 pagesWP Asset B - Trade ReceivablesDikdikNo ratings yet

- Rizwan & Co. Chartered Accountants: Completed by Schedule Reviewed by (SPS/AM) Reviewed by (Partner)Document2 pagesRizwan & Co. Chartered Accountants: Completed by Schedule Reviewed by (SPS/AM) Reviewed by (Partner)faheemNo ratings yet

- Advances - Deposits - and - Prepayments - Audit - Program - TODDocument20 pagesAdvances - Deposits - and - Prepayments - Audit - Program - TODShohag RaihanNo ratings yet

- 19l (12-00) Develop The Audit Program - RevenuesDocument2 pages19l (12-00) Develop The Audit Program - RevenuesAnh Tuấn TrầnNo ratings yet

- 3082advances, Deposits and Prepayments-Audit Program - TODDocument20 pages3082advances, Deposits and Prepayments-Audit Program - TODNiloy NeogiNo ratings yet

- 01 Property, Plant - EquipmentsDocument21 pages01 Property, Plant - EquipmentsRuwan GunarathnaNo ratings yet

- Audit Programme Long Term LoanDocument5 pagesAudit Programme Long Term LoanfaheemNo ratings yet

- PT - Cash and Cash Equivalents Period Ended - Audit ObjectivesDocument32 pagesPT - Cash and Cash Equivalents Period Ended - Audit ObjectivesVera Magdalena HutaurukNo ratings yet

- 02 Trade PayableDocument14 pages02 Trade PayableRuwan GunarathnaNo ratings yet

- 19b (12-00) Develop The Audit Program - Accounts ReceivableDocument3 pages19b (12-00) Develop The Audit Program - Accounts ReceivableTran AnhNo ratings yet

- Trade and Other PayablesDocument54 pagesTrade and Other Payablesemaan fatimaNo ratings yet

- CompiledDocument74 pagesCompiledNeil Richmond RecierdoNo ratings yet

- WP Asset A - Cash On Hand and in BanksDocument7 pagesWP Asset A - Cash On Hand and in BanksDikdikNo ratings yet

- 19l (12-00) Develop The Audit Program - COGSDocument1 page19l (12-00) Develop The Audit Program - COGSAnh Tuấn TrầnNo ratings yet

- Chartered Accountants: Member Crowe GlobalDocument20 pagesChartered Accountants: Member Crowe Globalemaan fatimaNo ratings yet

- Client Balance Date Nature of WPDocument6 pagesClient Balance Date Nature of WPSyazliana KasimNo ratings yet

- N-AP-1 - Accrued MarkupDocument2 pagesN-AP-1 - Accrued MarkupAung Zaw HtweNo ratings yet

- AFAR ProblemDocument14 pagesAFAR ProblemGil Enriquez100% (1)

- Primary Substantive ProceduresDocument9 pagesPrimary Substantive Proceduresmisonim.eNo ratings yet

- H1 - Account Receivables - PT Samcro 2020Document105 pagesH1 - Account Receivables - PT Samcro 2020Siska TriandriyaniNo ratings yet

- Audit of Trade Receivables and Sales BalancesDocument2 pagesAudit of Trade Receivables and Sales BalancesDiane VillarmaNo ratings yet

- Aec64 Audit 2 Notes-22-24Document3 pagesAec64 Audit 2 Notes-22-24Althea RubinNo ratings yet

- Substantive ProceduresDocument19 pagesSubstantive Proceduresمحمد اویسNo ratings yet

- Equity Audit ProgramDocument5 pagesEquity Audit ProgramHarold Dan AcebedoNo ratings yet

- Psa 700Document1 pagePsa 700Mary Grace NaragNo ratings yet

- Client - Year/ Period EndedDocument10 pagesClient - Year/ Period EndedTricia Rozl PimentelNo ratings yet

- Audit Group AssignmentDocument23 pagesAudit Group AssignmentShavi GurugeNo ratings yet

- AUD589 Tutorial Aud of SOPL SOFPDocument4 pagesAUD589 Tutorial Aud of SOPL SOFPRABIATULNAZIHAH NAZRINo ratings yet

- Auditing Notes 4 SWDocument4 pagesAuditing Notes 4 SWDhiraj rahateNo ratings yet

- Client: XYZ Limited Year End: 31-Dec-2014 File No. Ref:F Summary Sheet-Tangible Fixed Assets Planning FinalDocument6 pagesClient: XYZ Limited Year End: 31-Dec-2014 File No. Ref:F Summary Sheet-Tangible Fixed Assets Planning FinalnhbNo ratings yet

- BorrowingsDocument8 pagesBorrowingsStephen Paul EscañoNo ratings yet

- AR and Sales Audit ProgramDocument10 pagesAR and Sales Audit ProgramHarold Dan AcebedoNo ratings yet

- Audit Report 2021-2022Document18 pagesAudit Report 2021-2022Tanvir Ahmed ChowdhuryNo ratings yet

- SUMMARY SHEET - Advance Deposit and Prepayments: Client: Year End: File No. RefDocument2 pagesSUMMARY SHEET - Advance Deposit and Prepayments: Client: Year End: File No. RefShohag RaihanNo ratings yet

- Salaries Asia TADocument24 pagesSalaries Asia TAemaan fatimaNo ratings yet

- 19a (12-00) Develop The Audit Program - CashDocument2 pages19a (12-00) Develop The Audit Program - CashTran AnhNo ratings yet

- Employee Supervisor Payroll Check Cash Disbursements Vendor: Time Card Time Card Time CardDocument2 pagesEmployee Supervisor Payroll Check Cash Disbursements Vendor: Time Card Time Card Time CardAndrea Nicole PalalonNo ratings yet

- 2019 TANGLAW WP A011-V2Document95 pages2019 TANGLAW WP A011-V2Isaac Dominic MacaranasNo ratings yet

- Tudy Buddy: Ias 8 Accounting Policies, Changes in Accounting Estimates and ErrorsDocument2 pagesTudy Buddy: Ias 8 Accounting Policies, Changes in Accounting Estimates and ErrorsAbdullah Al Amin MubinNo ratings yet

- AP and Other Liabilities Audit ProgramDocument7 pagesAP and Other Liabilities Audit ProgramHarold Dan AcebedoNo ratings yet

- Profit or Loss - General and Administrative Expenses DoneDocument42 pagesProfit or Loss - General and Administrative Expenses Donefitriasindiannisya29No ratings yet

- Provisions For Liabilities and ChargesDocument8 pagesProvisions For Liabilities and ChargesStephen Paul EscañoNo ratings yet

- Audit Program - Amusement TaxDocument9 pagesAudit Program - Amusement TaxNanette Rose HaguilingNo ratings yet

- Audit Planning - Analytical ProceduresDocument35 pagesAudit Planning - Analytical ProceduresVenus Lyka LomocsoNo ratings yet

- Chapter 9 (3) : Completing The AuditDocument1 pageChapter 9 (3) : Completing The AuditARMIZAWANI BINTI MOHAMED BUANG BMNo ratings yet

- FABM Chapter 7 Part 1Document12 pagesFABM Chapter 7 Part 1Angel Cyra ObnimagaNo ratings yet

- Audited F/S The Basics: C CCCCC C C CCCC C CCCCCCCCDocument2 pagesAudited F/S The Basics: C CCCCC C C CCCC C CCCCCCCCkyday2No ratings yet

- CH 22Document3 pagesCH 22dedNo ratings yet

- 19f (12-00) Develop The Audit Program - Property, Plant and EquipmentDocument2 pages19f (12-00) Develop The Audit Program - Property, Plant and EquipmentTran AnhNo ratings yet

- FinancialapgDocument2 pagesFinancialapgDivine GraceNo ratings yet

- G6-Other IncomeDocument39 pagesG6-Other Incomebanomehar524No ratings yet

- G8 - Financial ChargesDocument2 pagesG8 - Financial Chargesbanomehar524No ratings yet

- Direct CostDocument26 pagesDirect Costbanomehar524No ratings yet

- F1 - Trade and Other Payables 2018Document24 pagesF1 - Trade and Other Payables 2018banomehar524No ratings yet

- D11 - Cash and BankDocument12 pagesD11 - Cash and Bankbanomehar524No ratings yet

- D5 - Loans and Advances 2018Document14 pagesD5 - Loans and Advances 2018banomehar524No ratings yet

- Lecture 9Document73 pagesLecture 9Zixin GuNo ratings yet

- Modul Xiv Audit Lanjutan Ing, 2020Document20 pagesModul Xiv Audit Lanjutan Ing, 2020Ismail MarzukiNo ratings yet

- Certified College of Accountancy's Mock Exam: PAPER: Financial Accounting (FA)Document10 pagesCertified College of Accountancy's Mock Exam: PAPER: Financial Accounting (FA)Chaiz MineNo ratings yet

- Finman Q2Document14 pagesFinman Q2Rhn SbdNo ratings yet

- Chapter 3 SolutionsDocument100 pagesChapter 3 SolutionssevtenNo ratings yet

- Noesis CFA Level 2 Formula Sheet 2024Document53 pagesNoesis CFA Level 2 Formula Sheet 2024anishloke08No ratings yet

- Societe Generale Ghana PLC 2021 Audited Financial StatementsDocument2 pagesSociete Generale Ghana PLC 2021 Audited Financial StatementsFuaad DodooNo ratings yet

- Paper: Cost Accounting and Financial Management: Raveendranath Kaushik & Associates Cost AccountantDocument13 pagesPaper: Cost Accounting and Financial Management: Raveendranath Kaushik & Associates Cost Accountantrk_rkaushikNo ratings yet

- FM Reviewer MidtermDocument21 pagesFM Reviewer MidtermPablo CoelhoNo ratings yet

- Question 8. T-Account Entries and Balance Sheet PreparationDocument2 pagesQuestion 8. T-Account Entries and Balance Sheet PreparationЭниЭ.No ratings yet

- 6int 2008 Dec ADocument6 pages6int 2008 Dec ACharles_Leong_3417No ratings yet

- EXAM About INTANGIBLE ASSETS 2Document3 pagesEXAM About INTANGIBLE ASSETS 2BLACKPINKLisaRoseJisooJennieNo ratings yet

- IRM Section B Group 1Document12 pagesIRM Section B Group 1Keshav GoelNo ratings yet

- ACCO 20103 Intermediate Accounting 3Document5 pagesACCO 20103 Intermediate Accounting 3glcpa100% (1)

- CMA Part I PDFDocument173 pagesCMA Part I PDFNicolai AquinoNo ratings yet

- Lecture - 5 - CFI-3-statement-model-completeDocument37 pagesLecture - 5 - CFI-3-statement-model-completeshreyasNo ratings yet

- Test Finance and AccountingDocument5 pagesTest Finance and AccountingKarachi Tuitions GroupNo ratings yet

- Free Acc 205 Week One Exercise AssignmentDocument17 pagesFree Acc 205 Week One Exercise AssignmentRachel Landrum100% (2)

- 2nd Quiz Aud ProbDocument4 pages2nd Quiz Aud ProbJohn Patrick Lazaro AndresNo ratings yet

- Equity Invest - MC Quest.w AnsDocument3 pagesEquity Invest - MC Quest.w AnsElaineJrV-Igot0% (1)

- Why Do We Subtract Cash and Add Debt When Calculating The Enterprise Value of A Firm - QuoraDocument10 pagesWhy Do We Subtract Cash and Add Debt When Calculating The Enterprise Value of A Firm - QuoraLester OrtegaNo ratings yet

- Lecture 09Document42 pagesLecture 09Hoda AmrNo ratings yet

- Basic Concepts and ConventionsDocument12 pagesBasic Concepts and ConventionsAnandi SarkarNo ratings yet

- Chapter 1 - Statement From Tabular AnalysisDocument3 pagesChapter 1 - Statement From Tabular AnalysisBracu 2023No ratings yet

- ACC 3003-Revision For Test 1Document7 pagesACC 3003-Revision For Test 1falnuaimi001No ratings yet

- MBAC1003Document7 pagesMBAC1003SwaathiNo ratings yet

Download as xlsx, pdf, or txt

You might also like

- Audit Programs 21-3, 21-4, and 21-5Document3 pagesAudit Programs 21-3, 21-4, and 21-5Faaiz YousafNo ratings yet

- TN 34 The WM Wrigley JR Company Capital Structure Valuation and Cost of CapitalDocument108 pagesTN 34 The WM Wrigley JR Company Capital Structure Valuation and Cost of CapitalStanisla Lee0% (2)

- Nciii Bookkeeping PDFDocument28 pagesNciii Bookkeeping PDFStephanie Cruz100% (10)

- FABM2 Q1 Mod1 Statement-of-Financial-Position v2Document24 pagesFABM2 Q1 Mod1 Statement-of-Financial-Position v2randy magbudhi93% (15)

- 19h (12-00) Develop The Audit Program - Accrued Liabilities and Deferred IncomeDocument2 pages19h (12-00) Develop The Audit Program - Accrued Liabilities and Deferred IncomeTran AnhNo ratings yet

- Oceanview Marine Company Audit Programs 30-3, 30-4, 30-5Document3 pagesOceanview Marine Company Audit Programs 30-3, 30-4, 30-5rebecca0% (2)

- Accountant TestDocument3 pagesAccountant TestMax SuperNo ratings yet

- C1 PpeDocument14 pagesC1 Ppebanomehar524No ratings yet

- C1 - Property, Plant and Equipment 2017Document36 pagesC1 - Property, Plant and Equipment 2017banomehar524No ratings yet

- D11 - Cash and BankDocument12 pagesD11 - Cash and Bankbanomehar524No ratings yet

- D4 - Trade Debts 2018Document13 pagesD4 - Trade Debts 2018banomehar524No ratings yet

- Audit Programme Tangible Fixed AssetDocument8 pagesAudit Programme Tangible Fixed AssetfaheemNo ratings yet

- Rizwan & Co. Chartered Accountants: Completed by Schedule Reviewed by (SPS/AM) Reviewed by (Partner)Document3 pagesRizwan & Co. Chartered Accountants: Completed by Schedule Reviewed by (SPS/AM) Reviewed by (Partner)faheemNo ratings yet

- WP Asset B - Trade ReceivablesDocument15 pagesWP Asset B - Trade ReceivablesDikdikNo ratings yet

- Rizwan & Co. Chartered Accountants: Completed by Schedule Reviewed by (SPS/AM) Reviewed by (Partner)Document2 pagesRizwan & Co. Chartered Accountants: Completed by Schedule Reviewed by (SPS/AM) Reviewed by (Partner)faheemNo ratings yet

- Advances - Deposits - and - Prepayments - Audit - Program - TODDocument20 pagesAdvances - Deposits - and - Prepayments - Audit - Program - TODShohag RaihanNo ratings yet

- 19l (12-00) Develop The Audit Program - RevenuesDocument2 pages19l (12-00) Develop The Audit Program - RevenuesAnh Tuấn TrầnNo ratings yet

- 3082advances, Deposits and Prepayments-Audit Program - TODDocument20 pages3082advances, Deposits and Prepayments-Audit Program - TODNiloy NeogiNo ratings yet

- 01 Property, Plant - EquipmentsDocument21 pages01 Property, Plant - EquipmentsRuwan GunarathnaNo ratings yet

- Audit Programme Long Term LoanDocument5 pagesAudit Programme Long Term LoanfaheemNo ratings yet

- PT - Cash and Cash Equivalents Period Ended - Audit ObjectivesDocument32 pagesPT - Cash and Cash Equivalents Period Ended - Audit ObjectivesVera Magdalena HutaurukNo ratings yet

- 02 Trade PayableDocument14 pages02 Trade PayableRuwan GunarathnaNo ratings yet

- 19b (12-00) Develop The Audit Program - Accounts ReceivableDocument3 pages19b (12-00) Develop The Audit Program - Accounts ReceivableTran AnhNo ratings yet

- Trade and Other PayablesDocument54 pagesTrade and Other Payablesemaan fatimaNo ratings yet

- CompiledDocument74 pagesCompiledNeil Richmond RecierdoNo ratings yet

- WP Asset A - Cash On Hand and in BanksDocument7 pagesWP Asset A - Cash On Hand and in BanksDikdikNo ratings yet

- 19l (12-00) Develop The Audit Program - COGSDocument1 page19l (12-00) Develop The Audit Program - COGSAnh Tuấn TrầnNo ratings yet

- Chartered Accountants: Member Crowe GlobalDocument20 pagesChartered Accountants: Member Crowe Globalemaan fatimaNo ratings yet

- Client Balance Date Nature of WPDocument6 pagesClient Balance Date Nature of WPSyazliana KasimNo ratings yet

- N-AP-1 - Accrued MarkupDocument2 pagesN-AP-1 - Accrued MarkupAung Zaw HtweNo ratings yet

- AFAR ProblemDocument14 pagesAFAR ProblemGil Enriquez100% (1)

- Primary Substantive ProceduresDocument9 pagesPrimary Substantive Proceduresmisonim.eNo ratings yet

- H1 - Account Receivables - PT Samcro 2020Document105 pagesH1 - Account Receivables - PT Samcro 2020Siska TriandriyaniNo ratings yet

- Audit of Trade Receivables and Sales BalancesDocument2 pagesAudit of Trade Receivables and Sales BalancesDiane VillarmaNo ratings yet

- Aec64 Audit 2 Notes-22-24Document3 pagesAec64 Audit 2 Notes-22-24Althea RubinNo ratings yet

- Substantive ProceduresDocument19 pagesSubstantive Proceduresمحمد اویسNo ratings yet

- Equity Audit ProgramDocument5 pagesEquity Audit ProgramHarold Dan AcebedoNo ratings yet

- Psa 700Document1 pagePsa 700Mary Grace NaragNo ratings yet

- Client - Year/ Period EndedDocument10 pagesClient - Year/ Period EndedTricia Rozl PimentelNo ratings yet

- Audit Group AssignmentDocument23 pagesAudit Group AssignmentShavi GurugeNo ratings yet

- AUD589 Tutorial Aud of SOPL SOFPDocument4 pagesAUD589 Tutorial Aud of SOPL SOFPRABIATULNAZIHAH NAZRINo ratings yet

- Auditing Notes 4 SWDocument4 pagesAuditing Notes 4 SWDhiraj rahateNo ratings yet

- Client: XYZ Limited Year End: 31-Dec-2014 File No. Ref:F Summary Sheet-Tangible Fixed Assets Planning FinalDocument6 pagesClient: XYZ Limited Year End: 31-Dec-2014 File No. Ref:F Summary Sheet-Tangible Fixed Assets Planning FinalnhbNo ratings yet

- BorrowingsDocument8 pagesBorrowingsStephen Paul EscañoNo ratings yet

- AR and Sales Audit ProgramDocument10 pagesAR and Sales Audit ProgramHarold Dan AcebedoNo ratings yet

- Audit Report 2021-2022Document18 pagesAudit Report 2021-2022Tanvir Ahmed ChowdhuryNo ratings yet

- SUMMARY SHEET - Advance Deposit and Prepayments: Client: Year End: File No. RefDocument2 pagesSUMMARY SHEET - Advance Deposit and Prepayments: Client: Year End: File No. RefShohag RaihanNo ratings yet

- Salaries Asia TADocument24 pagesSalaries Asia TAemaan fatimaNo ratings yet

- 19a (12-00) Develop The Audit Program - CashDocument2 pages19a (12-00) Develop The Audit Program - CashTran AnhNo ratings yet

- Employee Supervisor Payroll Check Cash Disbursements Vendor: Time Card Time Card Time CardDocument2 pagesEmployee Supervisor Payroll Check Cash Disbursements Vendor: Time Card Time Card Time CardAndrea Nicole PalalonNo ratings yet

- 2019 TANGLAW WP A011-V2Document95 pages2019 TANGLAW WP A011-V2Isaac Dominic MacaranasNo ratings yet

- Tudy Buddy: Ias 8 Accounting Policies, Changes in Accounting Estimates and ErrorsDocument2 pagesTudy Buddy: Ias 8 Accounting Policies, Changes in Accounting Estimates and ErrorsAbdullah Al Amin MubinNo ratings yet

- AP and Other Liabilities Audit ProgramDocument7 pagesAP and Other Liabilities Audit ProgramHarold Dan AcebedoNo ratings yet

- Profit or Loss - General and Administrative Expenses DoneDocument42 pagesProfit or Loss - General and Administrative Expenses Donefitriasindiannisya29No ratings yet

- Provisions For Liabilities and ChargesDocument8 pagesProvisions For Liabilities and ChargesStephen Paul EscañoNo ratings yet

- Audit Program - Amusement TaxDocument9 pagesAudit Program - Amusement TaxNanette Rose HaguilingNo ratings yet

- Audit Planning - Analytical ProceduresDocument35 pagesAudit Planning - Analytical ProceduresVenus Lyka LomocsoNo ratings yet

- Chapter 9 (3) : Completing The AuditDocument1 pageChapter 9 (3) : Completing The AuditARMIZAWANI BINTI MOHAMED BUANG BMNo ratings yet

- FABM Chapter 7 Part 1Document12 pagesFABM Chapter 7 Part 1Angel Cyra ObnimagaNo ratings yet

- Audited F/S The Basics: C CCCCC C C CCCC C CCCCCCCCDocument2 pagesAudited F/S The Basics: C CCCCC C C CCCC C CCCCCCCCkyday2No ratings yet

- CH 22Document3 pagesCH 22dedNo ratings yet

- 19f (12-00) Develop The Audit Program - Property, Plant and EquipmentDocument2 pages19f (12-00) Develop The Audit Program - Property, Plant and EquipmentTran AnhNo ratings yet

- FinancialapgDocument2 pagesFinancialapgDivine GraceNo ratings yet

- G6-Other IncomeDocument39 pagesG6-Other Incomebanomehar524No ratings yet

- G8 - Financial ChargesDocument2 pagesG8 - Financial Chargesbanomehar524No ratings yet

- Direct CostDocument26 pagesDirect Costbanomehar524No ratings yet

- F1 - Trade and Other Payables 2018Document24 pagesF1 - Trade and Other Payables 2018banomehar524No ratings yet

- D11 - Cash and BankDocument12 pagesD11 - Cash and Bankbanomehar524No ratings yet

- D5 - Loans and Advances 2018Document14 pagesD5 - Loans and Advances 2018banomehar524No ratings yet

- Lecture 9Document73 pagesLecture 9Zixin GuNo ratings yet

- Modul Xiv Audit Lanjutan Ing, 2020Document20 pagesModul Xiv Audit Lanjutan Ing, 2020Ismail MarzukiNo ratings yet

- Certified College of Accountancy's Mock Exam: PAPER: Financial Accounting (FA)Document10 pagesCertified College of Accountancy's Mock Exam: PAPER: Financial Accounting (FA)Chaiz MineNo ratings yet

- Finman Q2Document14 pagesFinman Q2Rhn SbdNo ratings yet

- Chapter 3 SolutionsDocument100 pagesChapter 3 SolutionssevtenNo ratings yet

- Noesis CFA Level 2 Formula Sheet 2024Document53 pagesNoesis CFA Level 2 Formula Sheet 2024anishloke08No ratings yet

- Societe Generale Ghana PLC 2021 Audited Financial StatementsDocument2 pagesSociete Generale Ghana PLC 2021 Audited Financial StatementsFuaad DodooNo ratings yet

- Paper: Cost Accounting and Financial Management: Raveendranath Kaushik & Associates Cost AccountantDocument13 pagesPaper: Cost Accounting and Financial Management: Raveendranath Kaushik & Associates Cost Accountantrk_rkaushikNo ratings yet

- FM Reviewer MidtermDocument21 pagesFM Reviewer MidtermPablo CoelhoNo ratings yet

- Question 8. T-Account Entries and Balance Sheet PreparationDocument2 pagesQuestion 8. T-Account Entries and Balance Sheet PreparationЭниЭ.No ratings yet

- 6int 2008 Dec ADocument6 pages6int 2008 Dec ACharles_Leong_3417No ratings yet

- EXAM About INTANGIBLE ASSETS 2Document3 pagesEXAM About INTANGIBLE ASSETS 2BLACKPINKLisaRoseJisooJennieNo ratings yet

- IRM Section B Group 1Document12 pagesIRM Section B Group 1Keshav GoelNo ratings yet

- ACCO 20103 Intermediate Accounting 3Document5 pagesACCO 20103 Intermediate Accounting 3glcpa100% (1)

- CMA Part I PDFDocument173 pagesCMA Part I PDFNicolai AquinoNo ratings yet

- Lecture - 5 - CFI-3-statement-model-completeDocument37 pagesLecture - 5 - CFI-3-statement-model-completeshreyasNo ratings yet

- Test Finance and AccountingDocument5 pagesTest Finance and AccountingKarachi Tuitions GroupNo ratings yet

- Free Acc 205 Week One Exercise AssignmentDocument17 pagesFree Acc 205 Week One Exercise AssignmentRachel Landrum100% (2)

- 2nd Quiz Aud ProbDocument4 pages2nd Quiz Aud ProbJohn Patrick Lazaro AndresNo ratings yet

- Equity Invest - MC Quest.w AnsDocument3 pagesEquity Invest - MC Quest.w AnsElaineJrV-Igot0% (1)

- Why Do We Subtract Cash and Add Debt When Calculating The Enterprise Value of A Firm - QuoraDocument10 pagesWhy Do We Subtract Cash and Add Debt When Calculating The Enterprise Value of A Firm - QuoraLester OrtegaNo ratings yet

- Lecture 09Document42 pagesLecture 09Hoda AmrNo ratings yet

- Basic Concepts and ConventionsDocument12 pagesBasic Concepts and ConventionsAnandi SarkarNo ratings yet

- Chapter 1 - Statement From Tabular AnalysisDocument3 pagesChapter 1 - Statement From Tabular AnalysisBracu 2023No ratings yet

- ACC 3003-Revision For Test 1Document7 pagesACC 3003-Revision For Test 1falnuaimi001No ratings yet

- MBAC1003Document7 pagesMBAC1003SwaathiNo ratings yet