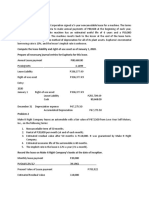

Activity Lease Part 2 A

Activity Lease Part 2 A

You might also like

- Chapter 02 Outline - Modern Real Estate Practice, 18th EditionDocument4 pagesChapter 02 Outline - Modern Real Estate Practice, 18th Editionmyname1015100% (1)

- 07 Special Liabilities - Leases: Intermediate Accounting 2 - Bernadette L. BaulDocument5 pages07 Special Liabilities - Leases: Intermediate Accounting 2 - Bernadette L. Baulkrisha millo50% (2)

- Answer: C - 465,000Document9 pagesAnswer: C - 465,000kyle G50% (2)

- Example Exercise Lease Acctg With AnsDocument28 pagesExample Exercise Lease Acctg With AnsPrince Avena AquinoNo ratings yet

- SPQ 003 Employee Benefits, Leases, and Other LiabilitiesDocument3 pagesSPQ 003 Employee Benefits, Leases, and Other LiabilitiesmarygraceomacNo ratings yet

- Orca Share Media1577676523240Document4 pagesOrca Share Media1577676523240Jayr BVNo ratings yet

- Accounting ForDocument18 pagesAccounting ForKriztleKateMontealtoGelogoNo ratings yet

- WeWork Pitch Deck Series D PDFDocument51 pagesWeWork Pitch Deck Series D PDFdont-wantNo ratings yet

- Compressed Notes On SPP & Architect's GuidelinesDocument65 pagesCompressed Notes On SPP & Architect's GuidelinesManny Inocencio100% (12)

- Activity Lease Part 1Document1 pageActivity Lease Part 1Eric GuapinNo ratings yet

- Assignment Problems On LeasesDocument4 pagesAssignment Problems On LeasesEllah Sharielle SantosNo ratings yet

- On January 1, 2-WPS OfficeDocument4 pagesOn January 1, 2-WPS OfficeSanta-ana Jerald JuanoNo ratings yet

- Rayos, Lyka Mae A - Ia3 CompilationsDocument7 pagesRayos, Lyka Mae A - Ia3 CompilationsKayeNo ratings yet

- IA2 AssignmentDocument2 pagesIA2 AssignmentJobelle Marie MahNo ratings yet

- SEATWORK - Chapter 11 - 16Document8 pagesSEATWORK - Chapter 11 - 16Kheajoy99 KimNo ratings yet

- MODULE 1 Midterm FAR 3 LeasesDocument31 pagesMODULE 1 Midterm FAR 3 LeasesKezNo ratings yet

- Lobrigas Unit5 Topic1 AssessmentDocument3 pagesLobrigas Unit5 Topic1 AssessmentClaudine LobrigasNo ratings yet

- Lessee Accounting: Right To Control The Use of An AssetDocument33 pagesLessee Accounting: Right To Control The Use of An AssetJohn Mark FernandoNo ratings yet

- Accounting For LeasesDocument6 pagesAccounting For LeasesJohn Ferd M. FerminNo ratings yet

- Far Project PrefiDocument16 pagesFar Project PrefiMarjorie PagsinuhinNo ratings yet

- Lessor Sample ProbDocument24 pagesLessor Sample ProbCzarina Jean ConopioNo ratings yet

- Case 1Document10 pagesCase 1Shawn VerzalesNo ratings yet

- Finance Lease LesseeDocument11 pagesFinance Lease LesseeAngel Queen Marino SamoragaNo ratings yet

- Chapter 10 Lease AccountingDocument6 pagesChapter 10 Lease AccountingCasinas Kyana LouisseNo ratings yet

- Intermediate Accounting 2 Finals SolvingsDocument24 pagesIntermediate Accounting 2 Finals SolvingsColeen BiocalesNo ratings yet

- Assignment Ppfrs 16Document3 pagesAssignment Ppfrs 16Joseph DoctoNo ratings yet

- SW-UPDATED-Leases PrintDocument2 pagesSW-UPDATED-Leases PrintMikaela Joy FloraNo ratings yet

- Lease Accounting 2021Document5 pagesLease Accounting 2021Just JhexNo ratings yet

- Leases: Lease Part 1Document10 pagesLeases: Lease Part 1ZyxNo ratings yet

- Problem Set 8. Finance LeaseDocument7 pagesProblem Set 8. Finance LeaseitsBlessedNo ratings yet

- Leases Part 2Document40 pagesLeases Part 2Danica RamosNo ratings yet

- Operating LeaseDocument7 pagesOperating Leasesantosashleymay7No ratings yet

- Problem Solving-LeaseDocument2 pagesProblem Solving-LeasegadingancielomarieNo ratings yet

- 6988 Finance Lease LesseeDocument2 pages6988 Finance Lease LesseeFREE MOVIESNo ratings yet

- Quiz 1 Leases PDFDocument4 pagesQuiz 1 Leases PDFken aysonNo ratings yet

- Lease Problem With SolutionDocument19 pagesLease Problem With SolutionJeane Mae Boo100% (1)

- 21 Finance Lease LesseeDocument3 pages21 Finance Lease LesseeTinNo ratings yet

- FAR QUIZ 1 - ProblemsDocument4 pagesFAR QUIZ 1 - ProblemsAEHYUN YENVYNo ratings yet

- LeasesDocument5 pagesLeasesCamille BacaresNo ratings yet

- 2 - ACG015 - Intermediate Accounting Part 3 - QuestionnaireDocument5 pages2 - ACG015 - Intermediate Accounting Part 3 - Questionnairedavis lizardaNo ratings yet

- Accounting 8 - ReviewerDocument4 pagesAccounting 8 - ReviewerAshley David AligonsaNo ratings yet

- Mary The Queen College of Pampanga Department of Accountancy Intermediate Accounting 2Document5 pagesMary The Queen College of Pampanga Department of Accountancy Intermediate Accounting 2Angela TuazonNo ratings yet

- Leases Part 3 - Other Accounting IssuesDocument33 pagesLeases Part 3 - Other Accounting IssuesDanica RamosNo ratings yet

- Problem 1: True or FalseDocument4 pagesProblem 1: True or FalseJohn Ace Madriaga50% (6)

- FINANCE LEASE-lecture and ExercisesDocument10 pagesFINANCE LEASE-lecture and ExercisesJamie CantubaNo ratings yet

- Quizzes Midterm To Finals OnlyDocument40 pagesQuizzes Midterm To Finals OnlyMikasa MikasaNo ratings yet

- Quiz Far LeaseDocument2 pagesQuiz Far Leasefrancis dungcaNo ratings yet

- Quiz On Pfrs 16 LeaseDocument4 pagesQuiz On Pfrs 16 LeaseCielo Mae Parungo56% (16)

- ACC 211 - Seventh QuizzerDocument1 pageACC 211 - Seventh QuizzerKate FernandezNo ratings yet

- Discussion Problems - Lessor AccountingDocument4 pagesDiscussion Problems - Lessor AccountingangelapearlrNo ratings yet

- Direct Financing Lease-LessorDocument2 pagesDirect Financing Lease-LessororillosachristoperjohnNo ratings yet

- ALL Quiz Ia 3Document29 pagesALL Quiz Ia 3julia4razoNo ratings yet

- Seatwork On LeasesDocument1 pageSeatwork On Leasesmitakumo uwuNo ratings yet

- Act1106-Leased Asset-LesseeDocument2 pagesAct1106-Leased Asset-LesseeorillosachristoperjohnNo ratings yet

- LeasesDocument3 pagesLeasesAngelica Rome EnriquezNo ratings yet

- Chapter 21Document18 pagesChapter 21Ardilla Noor Paramashanti Wirahadikusuma100% (1)

- 22 Finance Lease LessorDocument3 pages22 Finance Lease LessorAllegria AlamoNo ratings yet

- This Study Resource Was: F-ACADL-01Document8 pagesThis Study Resource Was: F-ACADL-01Marjorie PalmaNo ratings yet

- Sales&leasebackDocument15 pagesSales&leasebackeulhiemae arong0% (1)

- Inacct3 Module 3 QuizDocument7 pagesInacct3 Module 3 QuizGemNo ratings yet

- Finals - SeatWorkDocument1 pageFinals - SeatWorkDan RyanNo ratings yet

- Promoting Green Local Currency Bonds for Infrastructure Development in ASEAN+3From EverandPromoting Green Local Currency Bonds for Infrastructure Development in ASEAN+3No ratings yet

- Article 6 of the Paris Agreement: Drawing Lessons from the Joint Crediting MechanismFrom EverandArticle 6 of the Paris Agreement: Drawing Lessons from the Joint Crediting MechanismNo ratings yet

- OM Operation MGT Mod 4 Forecasting and SchedulingDocument5 pagesOM Operation MGT Mod 4 Forecasting and SchedulingEric GuapinNo ratings yet

- OM Operation Management Module Two 2Document6 pagesOM Operation Management Module Two 2Eric GuapinNo ratings yet

- Day 1 - Team BravoDocument13 pagesDay 1 - Team BravoEric GuapinNo ratings yet

- Group Work-Team BravoDocument28 pagesGroup Work-Team BravoEric GuapinNo ratings yet

- Team Bravo-Event TaskDocument7 pagesTeam Bravo-Event TaskEric GuapinNo ratings yet

- Land Title and Deeds ReviewerDocument2 pagesLand Title and Deeds ReviewerPauline Vistan Garcia100% (1)

- Lecture 1Document15 pagesLecture 1Anne AlyasNo ratings yet

- Tenancy Agreement 41 Greenwich Park Street London Se10 9ltDocument26 pagesTenancy Agreement 41 Greenwich Park Street London Se10 9ltw1933194No ratings yet

- Digest 2 Tiosejo vs. AngDocument1 pageDigest 2 Tiosejo vs. AngErvien A. MendozaNo ratings yet

- 1 LIHTC-Form-3-1 1 2021Document19 pages1 LIHTC-Form-3-1 1 2021PawPaul MccoyNo ratings yet

- Balaji Printing Solution ReportDocument10 pagesBalaji Printing Solution ReportYusuf AnsariNo ratings yet

- Fixed Asset Accounting and Management Procedures Manual: Revised December 2005 IDocument164 pagesFixed Asset Accounting and Management Procedures Manual: Revised December 2005 IDessie TarekegnNo ratings yet

- Bit Mesra M.arch SyllabusDocument22 pagesBit Mesra M.arch SyllabusniteshNo ratings yet

- Law On Property ReviewerDocument102 pagesLaw On Property ReviewerELEENAMICHAELA TORRESNo ratings yet

- Rental Listings in Roseville CA - 140 Rentals ZillowDocument1 pageRental Listings in Roseville CA - 140 Rentals ZillowChristine SparksNo ratings yet

- EU Directives SummaryDocument2 pagesEU Directives SummaryAndres HidalgoNo ratings yet

- Carmel Parking CorrespondenceDocument33 pagesCarmel Parking CorrespondenceL. A. PatersonNo ratings yet

- Spa Benchmark Report Full Year 2020Document5 pagesSpa Benchmark Report Full Year 2020Rupsayar DasNo ratings yet

- Specimen Specimen: Tenancy AgreementDocument4 pagesSpecimen Specimen: Tenancy AgreementYawson ElvisNo ratings yet

- What Types of Building Are There in Your City?Document2 pagesWhat Types of Building Are There in Your City?NganNo ratings yet

- Sublease AgreementDocument15 pagesSublease AgreementJoebell VillanuevaNo ratings yet

- Efr Vol 57 No 4 December 2019 Addressing Housing Deficit in Nigeria Issues, Challenges and Prospects Moore BEAUTYDocument22 pagesEfr Vol 57 No 4 December 2019 Addressing Housing Deficit in Nigeria Issues, Challenges and Prospects Moore BEAUTYjonathanNo ratings yet

- #Plumeria - GodrejWoods - Tower PlansDocument13 pages#Plumeria - GodrejWoods - Tower Plansprateek scrubingNo ratings yet

- Comparison..pledge, Mortgage, AntichresisDocument2 pagesComparison..pledge, Mortgage, AntichresisElfin Kenneth Puentespina0% (1)

- Hand Book For Civil EngineersDocument171 pagesHand Book For Civil EngineersWahid MarwatNo ratings yet

- Finding An Apartment ProjectDocument3 pagesFinding An Apartment Projectapi-288395661No ratings yet

- HS 330 1-1Document231 pagesHS 330 1-1MCP MarkNo ratings yet

- Caveat On Kyadondo Block 189 Plot 761Document3 pagesCaveat On Kyadondo Block 189 Plot 761SimonPrinceSemagandaNo ratings yet

- 31 PNB Vs CA, Et Al., G.R. No. 66715, Sept 18, 1990Document2 pages31 PNB Vs CA, Et Al., G.R. No. 66715, Sept 18, 1990RubenNo ratings yet

- December 2023 HomeLet Rental Index ReportDocument18 pagesDecember 2023 HomeLet Rental Index ReportjohnbullasNo ratings yet

- Pigao v. Rabanillo, 488 SCRA 547 (2006)Document9 pagesPigao v. Rabanillo, 488 SCRA 547 (2006)Carie LawyerrNo ratings yet

- 2023 Geronimo Delos Reyes OctoberDocument8 pages2023 Geronimo Delos Reyes Octoberウォーカー スカイラーNo ratings yet

Download as pdf or txt

You might also like

- Chapter 02 Outline - Modern Real Estate Practice, 18th EditionDocument4 pagesChapter 02 Outline - Modern Real Estate Practice, 18th Editionmyname1015100% (1)

- 07 Special Liabilities - Leases: Intermediate Accounting 2 - Bernadette L. BaulDocument5 pages07 Special Liabilities - Leases: Intermediate Accounting 2 - Bernadette L. Baulkrisha millo50% (2)

- Answer: C - 465,000Document9 pagesAnswer: C - 465,000kyle G50% (2)

- Example Exercise Lease Acctg With AnsDocument28 pagesExample Exercise Lease Acctg With AnsPrince Avena AquinoNo ratings yet

- SPQ 003 Employee Benefits, Leases, and Other LiabilitiesDocument3 pagesSPQ 003 Employee Benefits, Leases, and Other LiabilitiesmarygraceomacNo ratings yet

- Orca Share Media1577676523240Document4 pagesOrca Share Media1577676523240Jayr BVNo ratings yet

- Accounting ForDocument18 pagesAccounting ForKriztleKateMontealtoGelogoNo ratings yet

- WeWork Pitch Deck Series D PDFDocument51 pagesWeWork Pitch Deck Series D PDFdont-wantNo ratings yet

- Compressed Notes On SPP & Architect's GuidelinesDocument65 pagesCompressed Notes On SPP & Architect's GuidelinesManny Inocencio100% (12)

- Activity Lease Part 1Document1 pageActivity Lease Part 1Eric GuapinNo ratings yet

- Assignment Problems On LeasesDocument4 pagesAssignment Problems On LeasesEllah Sharielle SantosNo ratings yet

- On January 1, 2-WPS OfficeDocument4 pagesOn January 1, 2-WPS OfficeSanta-ana Jerald JuanoNo ratings yet

- Rayos, Lyka Mae A - Ia3 CompilationsDocument7 pagesRayos, Lyka Mae A - Ia3 CompilationsKayeNo ratings yet

- IA2 AssignmentDocument2 pagesIA2 AssignmentJobelle Marie MahNo ratings yet

- SEATWORK - Chapter 11 - 16Document8 pagesSEATWORK - Chapter 11 - 16Kheajoy99 KimNo ratings yet

- MODULE 1 Midterm FAR 3 LeasesDocument31 pagesMODULE 1 Midterm FAR 3 LeasesKezNo ratings yet

- Lobrigas Unit5 Topic1 AssessmentDocument3 pagesLobrigas Unit5 Topic1 AssessmentClaudine LobrigasNo ratings yet

- Lessee Accounting: Right To Control The Use of An AssetDocument33 pagesLessee Accounting: Right To Control The Use of An AssetJohn Mark FernandoNo ratings yet

- Accounting For LeasesDocument6 pagesAccounting For LeasesJohn Ferd M. FerminNo ratings yet

- Far Project PrefiDocument16 pagesFar Project PrefiMarjorie PagsinuhinNo ratings yet

- Lessor Sample ProbDocument24 pagesLessor Sample ProbCzarina Jean ConopioNo ratings yet

- Case 1Document10 pagesCase 1Shawn VerzalesNo ratings yet

- Finance Lease LesseeDocument11 pagesFinance Lease LesseeAngel Queen Marino SamoragaNo ratings yet

- Chapter 10 Lease AccountingDocument6 pagesChapter 10 Lease AccountingCasinas Kyana LouisseNo ratings yet

- Intermediate Accounting 2 Finals SolvingsDocument24 pagesIntermediate Accounting 2 Finals SolvingsColeen BiocalesNo ratings yet

- Assignment Ppfrs 16Document3 pagesAssignment Ppfrs 16Joseph DoctoNo ratings yet

- SW-UPDATED-Leases PrintDocument2 pagesSW-UPDATED-Leases PrintMikaela Joy FloraNo ratings yet

- Lease Accounting 2021Document5 pagesLease Accounting 2021Just JhexNo ratings yet

- Leases: Lease Part 1Document10 pagesLeases: Lease Part 1ZyxNo ratings yet

- Problem Set 8. Finance LeaseDocument7 pagesProblem Set 8. Finance LeaseitsBlessedNo ratings yet

- Leases Part 2Document40 pagesLeases Part 2Danica RamosNo ratings yet

- Operating LeaseDocument7 pagesOperating Leasesantosashleymay7No ratings yet

- Problem Solving-LeaseDocument2 pagesProblem Solving-LeasegadingancielomarieNo ratings yet

- 6988 Finance Lease LesseeDocument2 pages6988 Finance Lease LesseeFREE MOVIESNo ratings yet

- Quiz 1 Leases PDFDocument4 pagesQuiz 1 Leases PDFken aysonNo ratings yet

- Lease Problem With SolutionDocument19 pagesLease Problem With SolutionJeane Mae Boo100% (1)

- 21 Finance Lease LesseeDocument3 pages21 Finance Lease LesseeTinNo ratings yet

- FAR QUIZ 1 - ProblemsDocument4 pagesFAR QUIZ 1 - ProblemsAEHYUN YENVYNo ratings yet

- LeasesDocument5 pagesLeasesCamille BacaresNo ratings yet

- 2 - ACG015 - Intermediate Accounting Part 3 - QuestionnaireDocument5 pages2 - ACG015 - Intermediate Accounting Part 3 - Questionnairedavis lizardaNo ratings yet

- Accounting 8 - ReviewerDocument4 pagesAccounting 8 - ReviewerAshley David AligonsaNo ratings yet

- Mary The Queen College of Pampanga Department of Accountancy Intermediate Accounting 2Document5 pagesMary The Queen College of Pampanga Department of Accountancy Intermediate Accounting 2Angela TuazonNo ratings yet

- Leases Part 3 - Other Accounting IssuesDocument33 pagesLeases Part 3 - Other Accounting IssuesDanica RamosNo ratings yet

- Problem 1: True or FalseDocument4 pagesProblem 1: True or FalseJohn Ace Madriaga50% (6)

- FINANCE LEASE-lecture and ExercisesDocument10 pagesFINANCE LEASE-lecture and ExercisesJamie CantubaNo ratings yet

- Quizzes Midterm To Finals OnlyDocument40 pagesQuizzes Midterm To Finals OnlyMikasa MikasaNo ratings yet

- Quiz Far LeaseDocument2 pagesQuiz Far Leasefrancis dungcaNo ratings yet

- Quiz On Pfrs 16 LeaseDocument4 pagesQuiz On Pfrs 16 LeaseCielo Mae Parungo56% (16)

- ACC 211 - Seventh QuizzerDocument1 pageACC 211 - Seventh QuizzerKate FernandezNo ratings yet

- Discussion Problems - Lessor AccountingDocument4 pagesDiscussion Problems - Lessor AccountingangelapearlrNo ratings yet

- Direct Financing Lease-LessorDocument2 pagesDirect Financing Lease-LessororillosachristoperjohnNo ratings yet

- ALL Quiz Ia 3Document29 pagesALL Quiz Ia 3julia4razoNo ratings yet

- Seatwork On LeasesDocument1 pageSeatwork On Leasesmitakumo uwuNo ratings yet

- Act1106-Leased Asset-LesseeDocument2 pagesAct1106-Leased Asset-LesseeorillosachristoperjohnNo ratings yet

- LeasesDocument3 pagesLeasesAngelica Rome EnriquezNo ratings yet

- Chapter 21Document18 pagesChapter 21Ardilla Noor Paramashanti Wirahadikusuma100% (1)

- 22 Finance Lease LessorDocument3 pages22 Finance Lease LessorAllegria AlamoNo ratings yet

- This Study Resource Was: F-ACADL-01Document8 pagesThis Study Resource Was: F-ACADL-01Marjorie PalmaNo ratings yet

- Sales&leasebackDocument15 pagesSales&leasebackeulhiemae arong0% (1)

- Inacct3 Module 3 QuizDocument7 pagesInacct3 Module 3 QuizGemNo ratings yet

- Finals - SeatWorkDocument1 pageFinals - SeatWorkDan RyanNo ratings yet

- Promoting Green Local Currency Bonds for Infrastructure Development in ASEAN+3From EverandPromoting Green Local Currency Bonds for Infrastructure Development in ASEAN+3No ratings yet

- Article 6 of the Paris Agreement: Drawing Lessons from the Joint Crediting MechanismFrom EverandArticle 6 of the Paris Agreement: Drawing Lessons from the Joint Crediting MechanismNo ratings yet

- OM Operation MGT Mod 4 Forecasting and SchedulingDocument5 pagesOM Operation MGT Mod 4 Forecasting and SchedulingEric GuapinNo ratings yet

- OM Operation Management Module Two 2Document6 pagesOM Operation Management Module Two 2Eric GuapinNo ratings yet

- Day 1 - Team BravoDocument13 pagesDay 1 - Team BravoEric GuapinNo ratings yet

- Group Work-Team BravoDocument28 pagesGroup Work-Team BravoEric GuapinNo ratings yet

- Team Bravo-Event TaskDocument7 pagesTeam Bravo-Event TaskEric GuapinNo ratings yet

- Land Title and Deeds ReviewerDocument2 pagesLand Title and Deeds ReviewerPauline Vistan Garcia100% (1)

- Lecture 1Document15 pagesLecture 1Anne AlyasNo ratings yet

- Tenancy Agreement 41 Greenwich Park Street London Se10 9ltDocument26 pagesTenancy Agreement 41 Greenwich Park Street London Se10 9ltw1933194No ratings yet

- Digest 2 Tiosejo vs. AngDocument1 pageDigest 2 Tiosejo vs. AngErvien A. MendozaNo ratings yet

- 1 LIHTC-Form-3-1 1 2021Document19 pages1 LIHTC-Form-3-1 1 2021PawPaul MccoyNo ratings yet

- Balaji Printing Solution ReportDocument10 pagesBalaji Printing Solution ReportYusuf AnsariNo ratings yet

- Fixed Asset Accounting and Management Procedures Manual: Revised December 2005 IDocument164 pagesFixed Asset Accounting and Management Procedures Manual: Revised December 2005 IDessie TarekegnNo ratings yet

- Bit Mesra M.arch SyllabusDocument22 pagesBit Mesra M.arch SyllabusniteshNo ratings yet

- Law On Property ReviewerDocument102 pagesLaw On Property ReviewerELEENAMICHAELA TORRESNo ratings yet

- Rental Listings in Roseville CA - 140 Rentals ZillowDocument1 pageRental Listings in Roseville CA - 140 Rentals ZillowChristine SparksNo ratings yet

- EU Directives SummaryDocument2 pagesEU Directives SummaryAndres HidalgoNo ratings yet

- Carmel Parking CorrespondenceDocument33 pagesCarmel Parking CorrespondenceL. A. PatersonNo ratings yet

- Spa Benchmark Report Full Year 2020Document5 pagesSpa Benchmark Report Full Year 2020Rupsayar DasNo ratings yet

- Specimen Specimen: Tenancy AgreementDocument4 pagesSpecimen Specimen: Tenancy AgreementYawson ElvisNo ratings yet

- What Types of Building Are There in Your City?Document2 pagesWhat Types of Building Are There in Your City?NganNo ratings yet

- Sublease AgreementDocument15 pagesSublease AgreementJoebell VillanuevaNo ratings yet

- Efr Vol 57 No 4 December 2019 Addressing Housing Deficit in Nigeria Issues, Challenges and Prospects Moore BEAUTYDocument22 pagesEfr Vol 57 No 4 December 2019 Addressing Housing Deficit in Nigeria Issues, Challenges and Prospects Moore BEAUTYjonathanNo ratings yet

- #Plumeria - GodrejWoods - Tower PlansDocument13 pages#Plumeria - GodrejWoods - Tower Plansprateek scrubingNo ratings yet

- Comparison..pledge, Mortgage, AntichresisDocument2 pagesComparison..pledge, Mortgage, AntichresisElfin Kenneth Puentespina0% (1)

- Hand Book For Civil EngineersDocument171 pagesHand Book For Civil EngineersWahid MarwatNo ratings yet

- Finding An Apartment ProjectDocument3 pagesFinding An Apartment Projectapi-288395661No ratings yet

- HS 330 1-1Document231 pagesHS 330 1-1MCP MarkNo ratings yet

- Caveat On Kyadondo Block 189 Plot 761Document3 pagesCaveat On Kyadondo Block 189 Plot 761SimonPrinceSemagandaNo ratings yet

- 31 PNB Vs CA, Et Al., G.R. No. 66715, Sept 18, 1990Document2 pages31 PNB Vs CA, Et Al., G.R. No. 66715, Sept 18, 1990RubenNo ratings yet

- December 2023 HomeLet Rental Index ReportDocument18 pagesDecember 2023 HomeLet Rental Index ReportjohnbullasNo ratings yet

- Pigao v. Rabanillo, 488 SCRA 547 (2006)Document9 pagesPigao v. Rabanillo, 488 SCRA 547 (2006)Carie LawyerrNo ratings yet

- 2023 Geronimo Delos Reyes OctoberDocument8 pages2023 Geronimo Delos Reyes Octoberウォーカー スカイラーNo ratings yet