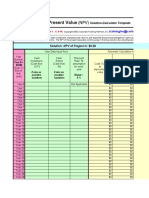

Slides Cash Flow

Slides Cash Flow

You might also like

- Battery Ventures OpenCloud Report 2021Document46 pagesBattery Ventures OpenCloud Report 2021Battery Ventures83% (6)

- Car Wash Marketing PlanDocument17 pagesCar Wash Marketing Plananon-145054100% (2)

- Live Nation PresentationDocument149 pagesLive Nation PresentationFortune100% (6)

- PW Your Money or Your Life PDFDocument8 pagesPW Your Money or Your Life PDFzoranle2363100% (5)

- Sap Cost Center PlanningDocument20 pagesSap Cost Center PlanningDon DonNo ratings yet

- BSC in Financial ServicesDocument16 pagesBSC in Financial ServicesBobby IM SibaraniNo ratings yet

- Pacing Plans For Illiquid Asset Classes: Rhode Island State Investment CommissionDocument15 pagesPacing Plans For Illiquid Asset Classes: Rhode Island State Investment Commissionnyguy06No ratings yet

- Sustainable Finance Review 2022.06Document15 pagesSustainable Finance Review 2022.06karlng167No ratings yet

- Sustainable Finance Review 2021.12Document15 pagesSustainable Finance Review 2021.12karlng167No ratings yet

- FMT05 Invoice - Tracker - AdvancedDocument2 pagesFMT05 Invoice - Tracker - AdvancedHazqanNo ratings yet

- Sustainable Finance Review 2022.12Document15 pagesSustainable Finance Review 2022.12karlng167No ratings yet

- Software Sector Report 1.16.2018Document24 pagesSoftware Sector Report 1.16.2018in_daHouseNo ratings yet

- P1Maths Weekly W41Document5 pagesP1Maths Weekly W41Yet Fong SanNo ratings yet

- Time To Exit & IPOs - PitchBook - 1H - 2016Document14 pagesTime To Exit & IPOs - PitchBook - 1H - 2016Arthur CahuantziNo ratings yet

- Complete The Questions and Answers: My Name Is - How Much Is/are 1 ?Document1 pageComplete The Questions and Answers: My Name Is - How Much Is/are 1 ?Lan Clarice AbabonNo ratings yet

- Classroom Objects FindrbbDocument1 pageClassroom Objects FindrbbNhanhut8xNo ratings yet

- 13 - Airplane Value AnalysisDocument39 pages13 - Airplane Value AnalysisJurandir SanchesNo ratings yet

- Retos Gastos VariablesDocument3 pagesRetos Gastos VariablesYessica RuizNo ratings yet

- Receipts (DailyExpense)Document12 pagesReceipts (DailyExpense)정집은No ratings yet

- Fondos de EmergenciaDocument1 pageFondos de EmergenciaAngie VenusNo ratings yet

- Status 2008 ClamsDocument5 pagesStatus 2008 ClamsGuillaume DentrelleNo ratings yet

- Profit and Loss Statement TemplateDocument2 pagesProfit and Loss Statement TemplateAlisa VisanNo ratings yet

- Part 2 - TKM0844 - 11E - IM - Ch20 PDFDocument18 pagesPart 2 - TKM0844 - 11E - IM - Ch20 PDFdannavillafuenteNo ratings yet

- Sustainable Finance Review 2020.09Document15 pagesSustainable Finance Review 2020.09karlng167No ratings yet

- Profit and Loss Statement TemplateDocument3 pagesProfit and Loss Statement TemplateMervat AboureslanNo ratings yet

- Testing Grant Billing Template 12220Document3 pagesTesting Grant Billing Template 12220Betty HannahNo ratings yet

- Annex B - Financial Proposal TemplateDocument2 pagesAnnex B - Financial Proposal TemplateMohammed YcfssNo ratings yet

- Home Renovation Budget TemplateDocument1 pageHome Renovation Budget TemplateNikunj VaghasiyaNo ratings yet

- Chapter 6 - Introduction To Risk and Return (Compatibility Mode)Document18 pagesChapter 6 - Introduction To Risk and Return (Compatibility Mode)Hanh TranNo ratings yet

- Problem Set 1Document5 pagesProblem Set 1Bocah_eLLekNo ratings yet

- The Global HBI/DRI Market: Outlook For Seaborne DR Grade Pellet SupplyDocument31 pagesThe Global HBI/DRI Market: Outlook For Seaborne DR Grade Pellet SupplyVivek RanganathanNo ratings yet

- Ical 01Document1 pageIcal 01Rizhal MuinNo ratings yet

- Business Kpi Dashboard Showing Average Revenue and CLV WDDocument6 pagesBusiness Kpi Dashboard Showing Average Revenue and CLV WDHimanshu ChavanNo ratings yet

- Sustainable Finance Review 2020.12Document15 pagesSustainable Finance Review 2020.12karlng167No ratings yet

- Time Consuming Challeneges Hours Per Week Your BLUE Number Total WeeklyDocument2 pagesTime Consuming Challeneges Hours Per Week Your BLUE Number Total WeeklyAnonymous ukxCpzXoNo ratings yet

- Net Present Value: $0.00 Solution: NPV of Project IsDocument4 pagesNet Present Value: $0.00 Solution: NPV of Project IspmanerkarNo ratings yet

- Money MonsterDocument20 pagesMoney MonstertinhhoanghonNo ratings yet

- Setup Costs (Incl GST)Document2 pagesSetup Costs (Incl GST)IswichNo ratings yet

- Hotel Cap Rates Hold Steady - Values Under PressureDocument10 pagesHotel Cap Rates Hold Steady - Values Under PressureManvinderNo ratings yet

- Coin Monkey 3Document1 pageCoin Monkey 3A TomNo ratings yet

- Venture Capital 2016 - Some Upfront Views: Mark SusterDocument37 pagesVenture Capital 2016 - Some Upfront Views: Mark Susteruzairkutti jagooNo ratings yet

- CARTA GRANDE La Provincia - Octubre 2023Document2 pagesCARTA GRANDE La Provincia - Octubre 2023francy covaledaNo ratings yet

- Franking Account WorkpaperDocument6 pagesFranking Account WorkpaperCarol YaoNo ratings yet

- HRM Kpi-DashboardDocument10 pagesHRM Kpi-DashboardMahmud MorshedNo ratings yet

- Nyb 20100707Document2 pagesNyb 20100707andrewbloggerNo ratings yet

- OriginalDocument36 pagesOriginalXiaochen TangNo ratings yet

- Sustainable Finance Review 2020.06Document14 pagesSustainable Finance Review 2020.06karlng167No ratings yet

- UMA House May'22 CheckbookDocument8 pagesUMA House May'22 CheckbookqgenerNo ratings yet

- 04/03/2017 06.07.30 D:/Eagle7.1.0/sensor Bloodseeker - BRDDocument1 page04/03/2017 06.07.30 D:/Eagle7.1.0/sensor Bloodseeker - BRDMsaNo ratings yet

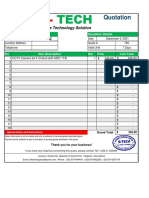

- Quotation: Reliable Technology SolutionDocument1 pageQuotation: Reliable Technology SolutionKHALIDNo ratings yet

- Donation LogDocument2 pagesDonation LogmommyyammieNo ratings yet

- CartaDocument2 pagesCartaLuis Antonio Carrera RoblesNo ratings yet

- Jefferies-Global Secondary Market Review-January 2023Document10 pagesJefferies-Global Secondary Market Review-January 2023Chuan JiNo ratings yet

- #1 Data Science Course Pune: Gross Profit Multiple AxesDocument1 page#1 Data Science Course Pune: Gross Profit Multiple AxesAmlan PandaNo ratings yet

- Venture Capital Update: Andy White Analysis ManagerDocument21 pagesVenture Capital Update: Andy White Analysis Managermarcmyomyint1663No ratings yet

- Farm AccountingDocument14 pagesFarm Accountingrobert.delasernaNo ratings yet

- DCF-ROPI ValuationDocument15 pagesDCF-ROPI ValuationRimpy SondhNo ratings yet

- Nyse NNN 2022Document112 pagesNyse NNN 2022Ngqabutho NdlovuNo ratings yet

- Money FlashcardsDocument5 pagesMoney Flashcardswinda meilia anggrainiNo ratings yet

- Consolidation ModelDocument19 pagesConsolidation ModelYAUHANo ratings yet

- Cost-Benefit Analysis TemplateDocument4 pagesCost-Benefit Analysis TemplateGeorgios PalaiologosNo ratings yet

- BAF 67 Summative ExaminationDocument3 pagesBAF 67 Summative ExaminationJastinNo ratings yet

- Assignment For Linear RegressionDocument1 pageAssignment For Linear RegressionJastinNo ratings yet

- CHAPTER 6 (Other Reference)Document35 pagesCHAPTER 6 (Other Reference)JastinNo ratings yet

- Chap 002Document25 pagesChap 002JastinNo ratings yet

- Chapter 6 PresentationDocument21 pagesChapter 6 PresentationJastinNo ratings yet

- Financial Stability FrameworkDocument46 pagesFinancial Stability FrameworkJastinNo ratings yet

- G5 Monitoring and Identifying Risks and Intervention ToolsDocument70 pagesG5 Monitoring and Identifying Risks and Intervention ToolsJastinNo ratings yet

- Working Capital Management SscEDocument38 pagesWorking Capital Management SscEJastinNo ratings yet

- Thesis Midterm Defense - Uniform PresentationDocument3 pagesThesis Midterm Defense - Uniform PresentationJastinNo ratings yet

- Financing Education As Administrative FunctionDocument27 pagesFinancing Education As Administrative Function0717 CartNo ratings yet

- ME Problem Set-6Document5 pagesME Problem Set-6Akash Deep100% (1)

- National Income and Related Aggregates: Dr. Roopali Srivastava Department of Management ITS, GhaziabadDocument30 pagesNational Income and Related Aggregates: Dr. Roopali Srivastava Department of Management ITS, GhaziabadniteshNo ratings yet

- Bba 407 - Management AccountingDocument10 pagesBba 407 - Management AccountingSimanta KalitaNo ratings yet

- Manual For Preparing Terms of ReferenceDocument23 pagesManual For Preparing Terms of Referencesofianina05100% (1)

- Employment NewsDocument40 pagesEmployment NewsVinod100% (1)

- Guingona v. CaragueDocument2 pagesGuingona v. CaragueArahbellsNo ratings yet

- Brewer Chapter 6Document8 pagesBrewer Chapter 6Sivakumar KanchirajuNo ratings yet

- Case #3Document2 pagesCase #3Atharva IngleNo ratings yet

- Home ManagementDocument15 pagesHome ManagementGian Ronell LaurenariaNo ratings yet

- 23 Gujarat PPP BhattacharyaDocument24 pages23 Gujarat PPP BhattacharyaSwapneel VaijanapurkarNo ratings yet

- BAB - Strategic Planning in EducationDocument11 pagesBAB - Strategic Planning in EducationAlamsyah NursehaNo ratings yet

- Activity-Based Costing Relevant To Acca Qualification Paper F5Document9 pagesActivity-Based Costing Relevant To Acca Qualification Paper F5Faizan Ahmed KiyaniNo ratings yet

- Budget Lines and Indifference CurvesDocument5 pagesBudget Lines and Indifference CurvesSalim AckbarNo ratings yet

- Budgeting in HealthcareDocument10 pagesBudgeting in Healthcarepurity NgasiNo ratings yet

- Job Description - Staff AccountantDocument1 pageJob Description - Staff AccountantFlordeliza SalvadorNo ratings yet

- A New World of Gold An SilverDocument365 pagesA New World of Gold An SilverSantiago Robledo100% (2)

- Incremental Analysis and Capital Budgeting: Learning ObjectivesDocument74 pagesIncremental Analysis and Capital Budgeting: Learning ObjectivesHanifah OktarizaNo ratings yet

- Goods and Service TaxDocument12 pagesGoods and Service Taxshourima mishraNo ratings yet

- Local Fiscal Administration ReportDocument18 pagesLocal Fiscal Administration ReportOliver Santos100% (3)

- CH 07 TifDocument39 pagesCH 07 TifFerdinand FernandoNo ratings yet

- Ocean Carriers Case Group 5Document27 pagesOcean Carriers Case Group 5HarveyNo ratings yet

- Evaluating Front Office OperationsDocument9 pagesEvaluating Front Office Operationsmehedi hasanNo ratings yet

- Test Questions - Com Test QuestionsDocument3 pagesTest Questions - Com Test QuestionsΈνκινουαν Κόγκ ΑδάμουNo ratings yet

- Corporate Budget Circular No. 26Document7 pagesCorporate Budget Circular No. 26DBM-CAR Feliza AlosNo ratings yet

- California Long-Term Care Programs: Recommendations To Improve Access For CaliforniansDocument329 pagesCalifornia Long-Term Care Programs: Recommendations To Improve Access For CaliforniansLeslie HendricksonNo ratings yet

Download as pdf or txt

You might also like

- Battery Ventures OpenCloud Report 2021Document46 pagesBattery Ventures OpenCloud Report 2021Battery Ventures83% (6)

- Car Wash Marketing PlanDocument17 pagesCar Wash Marketing Plananon-145054100% (2)

- Live Nation PresentationDocument149 pagesLive Nation PresentationFortune100% (6)

- PW Your Money or Your Life PDFDocument8 pagesPW Your Money or Your Life PDFzoranle2363100% (5)

- Sap Cost Center PlanningDocument20 pagesSap Cost Center PlanningDon DonNo ratings yet

- BSC in Financial ServicesDocument16 pagesBSC in Financial ServicesBobby IM SibaraniNo ratings yet

- Pacing Plans For Illiquid Asset Classes: Rhode Island State Investment CommissionDocument15 pagesPacing Plans For Illiquid Asset Classes: Rhode Island State Investment Commissionnyguy06No ratings yet

- Sustainable Finance Review 2022.06Document15 pagesSustainable Finance Review 2022.06karlng167No ratings yet

- Sustainable Finance Review 2021.12Document15 pagesSustainable Finance Review 2021.12karlng167No ratings yet

- FMT05 Invoice - Tracker - AdvancedDocument2 pagesFMT05 Invoice - Tracker - AdvancedHazqanNo ratings yet

- Sustainable Finance Review 2022.12Document15 pagesSustainable Finance Review 2022.12karlng167No ratings yet

- Software Sector Report 1.16.2018Document24 pagesSoftware Sector Report 1.16.2018in_daHouseNo ratings yet

- P1Maths Weekly W41Document5 pagesP1Maths Weekly W41Yet Fong SanNo ratings yet

- Time To Exit & IPOs - PitchBook - 1H - 2016Document14 pagesTime To Exit & IPOs - PitchBook - 1H - 2016Arthur CahuantziNo ratings yet

- Complete The Questions and Answers: My Name Is - How Much Is/are 1 ?Document1 pageComplete The Questions and Answers: My Name Is - How Much Is/are 1 ?Lan Clarice AbabonNo ratings yet

- Classroom Objects FindrbbDocument1 pageClassroom Objects FindrbbNhanhut8xNo ratings yet

- 13 - Airplane Value AnalysisDocument39 pages13 - Airplane Value AnalysisJurandir SanchesNo ratings yet

- Retos Gastos VariablesDocument3 pagesRetos Gastos VariablesYessica RuizNo ratings yet

- Receipts (DailyExpense)Document12 pagesReceipts (DailyExpense)정집은No ratings yet

- Fondos de EmergenciaDocument1 pageFondos de EmergenciaAngie VenusNo ratings yet

- Status 2008 ClamsDocument5 pagesStatus 2008 ClamsGuillaume DentrelleNo ratings yet

- Profit and Loss Statement TemplateDocument2 pagesProfit and Loss Statement TemplateAlisa VisanNo ratings yet

- Part 2 - TKM0844 - 11E - IM - Ch20 PDFDocument18 pagesPart 2 - TKM0844 - 11E - IM - Ch20 PDFdannavillafuenteNo ratings yet

- Sustainable Finance Review 2020.09Document15 pagesSustainable Finance Review 2020.09karlng167No ratings yet

- Profit and Loss Statement TemplateDocument3 pagesProfit and Loss Statement TemplateMervat AboureslanNo ratings yet

- Testing Grant Billing Template 12220Document3 pagesTesting Grant Billing Template 12220Betty HannahNo ratings yet

- Annex B - Financial Proposal TemplateDocument2 pagesAnnex B - Financial Proposal TemplateMohammed YcfssNo ratings yet

- Home Renovation Budget TemplateDocument1 pageHome Renovation Budget TemplateNikunj VaghasiyaNo ratings yet

- Chapter 6 - Introduction To Risk and Return (Compatibility Mode)Document18 pagesChapter 6 - Introduction To Risk and Return (Compatibility Mode)Hanh TranNo ratings yet

- Problem Set 1Document5 pagesProblem Set 1Bocah_eLLekNo ratings yet

- The Global HBI/DRI Market: Outlook For Seaborne DR Grade Pellet SupplyDocument31 pagesThe Global HBI/DRI Market: Outlook For Seaborne DR Grade Pellet SupplyVivek RanganathanNo ratings yet

- Ical 01Document1 pageIcal 01Rizhal MuinNo ratings yet

- Business Kpi Dashboard Showing Average Revenue and CLV WDDocument6 pagesBusiness Kpi Dashboard Showing Average Revenue and CLV WDHimanshu ChavanNo ratings yet

- Sustainable Finance Review 2020.12Document15 pagesSustainable Finance Review 2020.12karlng167No ratings yet

- Time Consuming Challeneges Hours Per Week Your BLUE Number Total WeeklyDocument2 pagesTime Consuming Challeneges Hours Per Week Your BLUE Number Total WeeklyAnonymous ukxCpzXoNo ratings yet

- Net Present Value: $0.00 Solution: NPV of Project IsDocument4 pagesNet Present Value: $0.00 Solution: NPV of Project IspmanerkarNo ratings yet

- Money MonsterDocument20 pagesMoney MonstertinhhoanghonNo ratings yet

- Setup Costs (Incl GST)Document2 pagesSetup Costs (Incl GST)IswichNo ratings yet

- Hotel Cap Rates Hold Steady - Values Under PressureDocument10 pagesHotel Cap Rates Hold Steady - Values Under PressureManvinderNo ratings yet

- Coin Monkey 3Document1 pageCoin Monkey 3A TomNo ratings yet

- Venture Capital 2016 - Some Upfront Views: Mark SusterDocument37 pagesVenture Capital 2016 - Some Upfront Views: Mark Susteruzairkutti jagooNo ratings yet

- CARTA GRANDE La Provincia - Octubre 2023Document2 pagesCARTA GRANDE La Provincia - Octubre 2023francy covaledaNo ratings yet

- Franking Account WorkpaperDocument6 pagesFranking Account WorkpaperCarol YaoNo ratings yet

- HRM Kpi-DashboardDocument10 pagesHRM Kpi-DashboardMahmud MorshedNo ratings yet

- Nyb 20100707Document2 pagesNyb 20100707andrewbloggerNo ratings yet

- OriginalDocument36 pagesOriginalXiaochen TangNo ratings yet

- Sustainable Finance Review 2020.06Document14 pagesSustainable Finance Review 2020.06karlng167No ratings yet

- UMA House May'22 CheckbookDocument8 pagesUMA House May'22 CheckbookqgenerNo ratings yet

- 04/03/2017 06.07.30 D:/Eagle7.1.0/sensor Bloodseeker - BRDDocument1 page04/03/2017 06.07.30 D:/Eagle7.1.0/sensor Bloodseeker - BRDMsaNo ratings yet

- Quotation: Reliable Technology SolutionDocument1 pageQuotation: Reliable Technology SolutionKHALIDNo ratings yet

- Donation LogDocument2 pagesDonation LogmommyyammieNo ratings yet

- CartaDocument2 pagesCartaLuis Antonio Carrera RoblesNo ratings yet

- Jefferies-Global Secondary Market Review-January 2023Document10 pagesJefferies-Global Secondary Market Review-January 2023Chuan JiNo ratings yet

- #1 Data Science Course Pune: Gross Profit Multiple AxesDocument1 page#1 Data Science Course Pune: Gross Profit Multiple AxesAmlan PandaNo ratings yet

- Venture Capital Update: Andy White Analysis ManagerDocument21 pagesVenture Capital Update: Andy White Analysis Managermarcmyomyint1663No ratings yet

- Farm AccountingDocument14 pagesFarm Accountingrobert.delasernaNo ratings yet

- DCF-ROPI ValuationDocument15 pagesDCF-ROPI ValuationRimpy SondhNo ratings yet

- Nyse NNN 2022Document112 pagesNyse NNN 2022Ngqabutho NdlovuNo ratings yet

- Money FlashcardsDocument5 pagesMoney Flashcardswinda meilia anggrainiNo ratings yet

- Consolidation ModelDocument19 pagesConsolidation ModelYAUHANo ratings yet

- Cost-Benefit Analysis TemplateDocument4 pagesCost-Benefit Analysis TemplateGeorgios PalaiologosNo ratings yet

- BAF 67 Summative ExaminationDocument3 pagesBAF 67 Summative ExaminationJastinNo ratings yet

- Assignment For Linear RegressionDocument1 pageAssignment For Linear RegressionJastinNo ratings yet

- CHAPTER 6 (Other Reference)Document35 pagesCHAPTER 6 (Other Reference)JastinNo ratings yet

- Chap 002Document25 pagesChap 002JastinNo ratings yet

- Chapter 6 PresentationDocument21 pagesChapter 6 PresentationJastinNo ratings yet

- Financial Stability FrameworkDocument46 pagesFinancial Stability FrameworkJastinNo ratings yet

- G5 Monitoring and Identifying Risks and Intervention ToolsDocument70 pagesG5 Monitoring and Identifying Risks and Intervention ToolsJastinNo ratings yet

- Working Capital Management SscEDocument38 pagesWorking Capital Management SscEJastinNo ratings yet

- Thesis Midterm Defense - Uniform PresentationDocument3 pagesThesis Midterm Defense - Uniform PresentationJastinNo ratings yet

- Financing Education As Administrative FunctionDocument27 pagesFinancing Education As Administrative Function0717 CartNo ratings yet

- ME Problem Set-6Document5 pagesME Problem Set-6Akash Deep100% (1)

- National Income and Related Aggregates: Dr. Roopali Srivastava Department of Management ITS, GhaziabadDocument30 pagesNational Income and Related Aggregates: Dr. Roopali Srivastava Department of Management ITS, GhaziabadniteshNo ratings yet

- Bba 407 - Management AccountingDocument10 pagesBba 407 - Management AccountingSimanta KalitaNo ratings yet

- Manual For Preparing Terms of ReferenceDocument23 pagesManual For Preparing Terms of Referencesofianina05100% (1)

- Employment NewsDocument40 pagesEmployment NewsVinod100% (1)

- Guingona v. CaragueDocument2 pagesGuingona v. CaragueArahbellsNo ratings yet

- Brewer Chapter 6Document8 pagesBrewer Chapter 6Sivakumar KanchirajuNo ratings yet

- Case #3Document2 pagesCase #3Atharva IngleNo ratings yet

- Home ManagementDocument15 pagesHome ManagementGian Ronell LaurenariaNo ratings yet

- 23 Gujarat PPP BhattacharyaDocument24 pages23 Gujarat PPP BhattacharyaSwapneel VaijanapurkarNo ratings yet

- BAB - Strategic Planning in EducationDocument11 pagesBAB - Strategic Planning in EducationAlamsyah NursehaNo ratings yet

- Activity-Based Costing Relevant To Acca Qualification Paper F5Document9 pagesActivity-Based Costing Relevant To Acca Qualification Paper F5Faizan Ahmed KiyaniNo ratings yet

- Budget Lines and Indifference CurvesDocument5 pagesBudget Lines and Indifference CurvesSalim AckbarNo ratings yet

- Budgeting in HealthcareDocument10 pagesBudgeting in Healthcarepurity NgasiNo ratings yet

- Job Description - Staff AccountantDocument1 pageJob Description - Staff AccountantFlordeliza SalvadorNo ratings yet

- A New World of Gold An SilverDocument365 pagesA New World of Gold An SilverSantiago Robledo100% (2)

- Incremental Analysis and Capital Budgeting: Learning ObjectivesDocument74 pagesIncremental Analysis and Capital Budgeting: Learning ObjectivesHanifah OktarizaNo ratings yet

- Goods and Service TaxDocument12 pagesGoods and Service Taxshourima mishraNo ratings yet

- Local Fiscal Administration ReportDocument18 pagesLocal Fiscal Administration ReportOliver Santos100% (3)

- CH 07 TifDocument39 pagesCH 07 TifFerdinand FernandoNo ratings yet

- Ocean Carriers Case Group 5Document27 pagesOcean Carriers Case Group 5HarveyNo ratings yet

- Evaluating Front Office OperationsDocument9 pagesEvaluating Front Office Operationsmehedi hasanNo ratings yet

- Test Questions - Com Test QuestionsDocument3 pagesTest Questions - Com Test QuestionsΈνκινουαν Κόγκ ΑδάμουNo ratings yet

- Corporate Budget Circular No. 26Document7 pagesCorporate Budget Circular No. 26DBM-CAR Feliza AlosNo ratings yet

- California Long-Term Care Programs: Recommendations To Improve Access For CaliforniansDocument329 pagesCalifornia Long-Term Care Programs: Recommendations To Improve Access For CaliforniansLeslie HendricksonNo ratings yet