6.03 Market Efficiency - Answers

6.03 Market Efficiency - Answers

You might also like

- CMT Curriculum 2021 LEVEL II Wiley FINALDocument14 pagesCMT Curriculum 2021 LEVEL II Wiley FINALJamesMc114433% (3)

- Corporate FinanceDocument13 pagesCorporate FinanceNguyễn Thanh LâmNo ratings yet

- Ema Ge Berk CF 2GE SG 23Document12 pagesEma Ge Berk CF 2GE SG 23Sascha SaschaNo ratings yet

- CFA Level III 2010 Exam AnswersDocument67 pagesCFA Level III 2010 Exam AnswersAkash KumarNo ratings yet

- A Game Theoretic Framework of TrustDocument13 pagesA Game Theoretic Framework of TrustBaasit ShariefNo ratings yet

- Financial Management - Grinblatt and TitmanDocument68 pagesFinancial Management - Grinblatt and TitmanLuis Daniel Malavé RojasNo ratings yet

- Topic 2 - Equity 1 AnsDocument6 pagesTopic 2 - Equity 1 AnsGaba RieleNo ratings yet

- Topic 3 - Equity 2 Ans 2019-20Document6 pagesTopic 3 - Equity 2 Ans 2019-20Gaba RieleNo ratings yet

- Chapter 4 FIDocument7 pagesChapter 4 FIsitina.at.lunarNo ratings yet

- Chapter 13. Market EfficiencyDocument3 pagesChapter 13. Market EfficiencyHastings KapalaNo ratings yet

- Bachelor of Business Administration-BBA: Semester 5 BB0022 Capital and Money Market - 4 Credits Assignment (60 Marks)Document8 pagesBachelor of Business Administration-BBA: Semester 5 BB0022 Capital and Money Market - 4 Credits Assignment (60 Marks)Devlean Bhowal100% (1)

- Efficient Capital MarketDocument3 pagesEfficient Capital MarketTaimoorKhanNo ratings yet

- Dissertation ReportDocument53 pagesDissertation ReportPriyanka GroverNo ratings yet

- Proportional To Shares OwnedDocument6 pagesProportional To Shares OwnedArham KothariNo ratings yet

- Management of Financial Institutions - BUP - Lecture 06Document30 pagesManagement of Financial Institutions - BUP - Lecture 06Kaniz Fatama MimNo ratings yet

- Buy Back of SharesDocument10 pagesBuy Back of SharesRajgor ShrushtiNo ratings yet

- Chapter 4 FIDocument7 pagesChapter 4 FISeid KassawNo ratings yet

- Unit 1: Understanding Equity: Public Equity Vs Private EquityDocument10 pagesUnit 1: Understanding Equity: Public Equity Vs Private EquityPulkit AggarwalNo ratings yet

- Oneliners P1Document4 pagesOneliners P1Nirvana BoyNo ratings yet

- Financial Matter1 PDFDocument42 pagesFinancial Matter1 PDFDrNaveed Ul HaqNo ratings yet

- Stock Market Efficiency & Stock ValuationDocument23 pagesStock Market Efficiency & Stock ValuationKaila SalemNo ratings yet

- Current Stock Market Scenario-Delisting OffersDocument4 pagesCurrent Stock Market Scenario-Delisting OffersSNo ratings yet

- Merger & Acquisition: Defences Against Unwelcome TakeoversDocument22 pagesMerger & Acquisition: Defences Against Unwelcome TakeoversViraj GawandeNo ratings yet

- Chapter 3: Stock Valuation Methods and Efficient Market HypothesisDocument5 pagesChapter 3: Stock Valuation Methods and Efficient Market HypothesisPablo EkskobaNo ratings yet

- BM 204 2020 Module Investment ApprochesDocument36 pagesBM 204 2020 Module Investment ApprochesPhebieon MukwenhaNo ratings yet

- S A A I M: Ecurity Nalysis ND Nvestment AnagementDocument38 pagesS A A I M: Ecurity Nalysis ND Nvestment AnagementghanshyamvarshneyjiNo ratings yet

- Chapter 13 The Stock MarketDocument7 pagesChapter 13 The Stock Marketlasha KachkachishviliNo ratings yet

- Chapter 6: Answers To Concepts in Review: Fundamentals of Investing, by Gitman and JoehnkDocument6 pagesChapter 6: Answers To Concepts in Review: Fundamentals of Investing, by Gitman and JoehnkLouina YnciertoNo ratings yet

- Learning Module #3 Investment and Portfolio Management: Participating, and Cumulative and ParticipatingDocument6 pagesLearning Module #3 Investment and Portfolio Management: Participating, and Cumulative and ParticipatingAira AbigailNo ratings yet

- Imbalances Created Because of Structured Products in India Equity MarketsDocument8 pagesImbalances Created Because of Structured Products in India Equity MarketsManmohan BhartiaNo ratings yet

- T FDocument3 pagesT Faquarius21012003No ratings yet

- Describe The Nature of The Stock MarketDocument4 pagesDescribe The Nature of The Stock MarketJerbert JesalvaNo ratings yet

- Unit 8Document4 pagesUnit 8Loan NguyễnNo ratings yet

- The Efficient Market HypothesisDocument6 pagesThe Efficient Market HypothesisSeemaNo ratings yet

- Stock Market LearningDocument7 pagesStock Market LearningD P ChatterjeeNo ratings yet

- Chapter 6Document24 pagesChapter 6sdfklmjsdlklskfjd100% (2)

- Security Structures and Determining Enterprise Values FocusDocument24 pagesSecurity Structures and Determining Enterprise Values FocusMuhammad Qasim A20D047FNo ratings yet

- General Mathematics Basic Concepts of Stocks and BondsDocument5 pagesGeneral Mathematics Basic Concepts of Stocks and BondsGyle Contawe Garcia86% (7)

- BD Job Traning Session 4Document58 pagesBD Job Traning Session 4Mamun ReturnNo ratings yet

- Silo - Tips - Chapter 10 Stocks and Their Valuation Answers To End of Chapter QuestionsDocument19 pagesSilo - Tips - Chapter 10 Stocks and Their Valuation Answers To End of Chapter QuestionsBeatrice ReynanciaNo ratings yet

- Stock Market I. What Are Stocks?Document9 pagesStock Market I. What Are Stocks?JehannahBaratNo ratings yet

- Common Stocks: SummaryDocument5 pagesCommon Stocks: SummaryZain MughalNo ratings yet

- Project On Reliance BuybackDocument17 pagesProject On Reliance Buybackamin pattaniNo ratings yet

- Equity QUIZDocument8 pagesEquity QUIZSaYeD SeeDooNo ratings yet

- Investing in Stocks and BondsDocument89 pagesInvesting in Stocks and BondsLimSiEianNo ratings yet

- BFC5935 - Tutorial 4 SolutionsDocument6 pagesBFC5935 - Tutorial 4 SolutionsXue XuNo ratings yet

- D - Tutorial 9 (Solutions)Document13 pagesD - Tutorial 9 (Solutions)AlfieNo ratings yet

- 2023 Financial Eco Chapters 11 and 12 Lecture SlidesDocument49 pages2023 Financial Eco Chapters 11 and 12 Lecture SlidesmrsmasandaNo ratings yet

- Chap 14 SolutionsDocument10 pagesChap 14 SolutionsMiftahudin Miftahudin100% (1)

- Chapter 12 - PART 2Document11 pagesChapter 12 - PART 2Maya RamadhaniyatiNo ratings yet

- Sources of Finance (Equity)Document10 pagesSources of Finance (Equity)Dayaan ANo ratings yet

- Buy-Side M&ADocument8 pagesBuy-Side M&ALeonardoNo ratings yet

- Lesson 6. Equity MarketDocument12 pagesLesson 6. Equity Markethoneymaetreseni26No ratings yet

- Essay Question For Final ExamDocument5 pagesEssay Question For Final ExamKhoa LêNo ratings yet

- Concept Questions - Chapter 19Document2 pagesConcept Questions - Chapter 19husseinNo ratings yet

- RELATIVE VALUATION Theory PDFDocument5 pagesRELATIVE VALUATION Theory PDFPrateek SidharNo ratings yet

- Stock Investment DefinedDocument5 pagesStock Investment DefinedRoger Paul Singidas FuentesNo ratings yet

- A Stock Split or Stock Divide Increases or Decreases The Number of Shares in A PublicDocument11 pagesA Stock Split or Stock Divide Increases or Decreases The Number of Shares in A Publicsanjay mehtaNo ratings yet

- What Is A Stock?: Stock Market Equity MarketDocument3 pagesWhat Is A Stock?: Stock Market Equity MarketJob KurienNo ratings yet

- Module 4Document22 pagesModule 4mohibjahangir01No ratings yet

- Mastering the Market: A Comprehensive Guide to Successful Stock InvestingFrom EverandMastering the Market: A Comprehensive Guide to Successful Stock InvestingNo ratings yet

- Mastering the Markets: Advanced Trading Strategies for Success and Ethical Trading PracticesFrom EverandMastering the Markets: Advanced Trading Strategies for Success and Ethical Trading PracticesNo ratings yet

- 5.09 Analysis of Income Taxes - AnswersDocument38 pages5.09 Analysis of Income Taxes - Answersgustavo eichholzNo ratings yet

- 6.01 Market Organization and Structure - AnswersDocument56 pages6.01 Market Organization and Structure - Answersgustavo eichholzNo ratings yet

- 6.01 Market Organization and StructureDocument13 pages6.01 Market Organization and Structuregustavo eichholzNo ratings yet

- 1.05 Portfolio MathematicsDocument3 pages1.05 Portfolio Mathematicsgustavo eichholzNo ratings yet

- 4.05 Capital Investments and Capital Allocation - AnswersDocument33 pages4.05 Capital Investments and Capital Allocation - Answersgustavo eichholzNo ratings yet

- 4.07 Business ModelsDocument1 page4.07 Business Modelsgustavo eichholzNo ratings yet

- Mock Exam 2023 #4 First Session Ethical and Professional StandardsDocument91 pagesMock Exam 2023 #4 First Session Ethical and Professional Standardsgustavo eichholzNo ratings yet

- 2.06 International Trade - AnswersDocument10 pages2.06 International Trade - Answersgustavo eichholzNo ratings yet

- 1.01 Rates and ReturnsDocument12 pages1.01 Rates and Returnsgustavo eichholzNo ratings yet

- 1.08 Hypothesis TestingDocument7 pages1.08 Hypothesis Testinggustavo eichholzNo ratings yet

- 1.02 The Time Value of Money in FinanceDocument1 page1.02 The Time Value of Money in Financegustavo eichholzNo ratings yet

- 1.08 Hypothesis Testing - AnswersDocument29 pages1.08 Hypothesis Testing - Answersgustavo eichholzNo ratings yet

- 4.02 Investors and Other StakeholdersDocument2 pages4.02 Investors and Other Stakeholdersgustavo eichholzNo ratings yet

- 4.03 Corporate Governance - Conflicts, Mechanisms, Risks, and BenefitsDocument3 pages4.03 Corporate Governance - Conflicts, Mechanisms, Risks, and Benefitsgustavo eichholzNo ratings yet

- 4.07 Business ModelsDocument1 page4.07 Business Modelsgustavo eichholzNo ratings yet

- 15 1391bsacInternationalCenterforLaw&EconomicsandScholarsofLawandEconomicsDocument36 pages15 1391bsacInternationalCenterforLaw&EconomicsandScholarsofLawandEconomicsrobertNo ratings yet

- Impact of Behavioral Finance & Traditional Finance On Financial Decision Making ProcessDocument8 pagesImpact of Behavioral Finance & Traditional Finance On Financial Decision Making ProcessUbaid DarNo ratings yet

- The Oxford Handbook of Ethics and Economics White Ebook Full ChapterDocument51 pagesThe Oxford Handbook of Ethics and Economics White Ebook Full Chapterandrew.glidewell897100% (18)

- Barclays Wealth InsightsDocument32 pagesBarclays Wealth Insightsnarayan.mitNo ratings yet

- Data Mentah18 Desember 2020Document23 pagesData Mentah18 Desember 2020fathur abrarNo ratings yet

- Module 5.1. Market Anomalies - Behavioural.psychological - FactorsDocument30 pagesModule 5.1. Market Anomalies - Behavioural.psychological - FactorsakwoviahNo ratings yet

- K Kiran Kumar: Any Questions? Behavioral Finance, Netscape IPO, ReviewDocument33 pagesK Kiran Kumar: Any Questions? Behavioral Finance, Netscape IPO, ReviewJohn DoeNo ratings yet

- 1 - Introduction Behavioral EconomicsDocument3 pages1 - Introduction Behavioral EconomicsPyan AminNo ratings yet

- Rational Expectation Theory Assingment by Naseer AhmadDocument12 pagesRational Expectation Theory Assingment by Naseer AhmadNaseerNo ratings yet

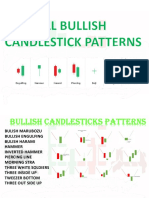

- All Bullish Candlestick Pattern by Optrading00 Telegram Optrading00Document25 pagesAll Bullish Candlestick Pattern by Optrading00 Telegram Optrading00Samitm TamhankarNo ratings yet

- Alchian - Incertidumbre, Evolución y Teoría EconómicaDocument19 pagesAlchian - Incertidumbre, Evolución y Teoría EconómicaKatherineNo ratings yet

- Psychological Biases, Main Factors of Financial Behaviour - A Literature ReviewDocument11 pagesPsychological Biases, Main Factors of Financial Behaviour - A Literature ReviewNi Wayan Radha MaharseniNo ratings yet

- Indian Stock MarketDocument197 pagesIndian Stock Marketdeepsam88No ratings yet

- Fullpaper Icopss2017 PDFDocument1,095 pagesFullpaper Icopss2017 PDFNurul AidaNo ratings yet

- The Dynamics of Financial Markets: Fibonacci Numbers, Elliott Waves, and SolitonsDocument27 pagesThe Dynamics of Financial Markets: Fibonacci Numbers, Elliott Waves, and SolitonsCPV994No ratings yet

- Behavioral FinanceDocument115 pagesBehavioral FinancekenNo ratings yet

- Behavioural Biases Theories 2nd ChapterDocument26 pagesBehavioural Biases Theories 2nd Chaptersadhana gawade/AwateNo ratings yet

- Revue AERES HCERES Mars2016Document727 pagesRevue AERES HCERES Mars2016Emy des JardinsNo ratings yet

- Role of Behavioral Finance in Investment Decision - A Study of Investment Behavior in IndiaDocument12 pagesRole of Behavioral Finance in Investment Decision - A Study of Investment Behavior in IndiaVishal ShimpiNo ratings yet

- Dan Ariely - The Upside of IrrationalityDocument11 pagesDan Ariely - The Upside of IrrationalityJasvinder TanejaNo ratings yet

- Week 4 Concept of Behavioural BiasesDocument11 pagesWeek 4 Concept of Behavioural BiasesShirin RazdanNo ratings yet

- Big Data in FinannceDocument14 pagesBig Data in FinannceTrần Thị Thuỷ TiênNo ratings yet

- Hum1046 PPT (17543)Document329 pagesHum1046 PPT (17543)shri shubhamNo ratings yet

- Coronavirus Crisis and Behavioural EconomicsDocument36 pagesCoronavirus Crisis and Behavioural Economicsrakesh khuranaNo ratings yet

- Reading 52 - Behavioral Biases of IndividualsDocument12 pagesReading 52 - Behavioral Biases of IndividualsAllen AravindanNo ratings yet

- MCQ - Behavioural EconomicsDocument12 pagesMCQ - Behavioural EconomicsMelaku GemedaNo ratings yet

- Psychologys Factors of Stock Buying and PDFDocument12 pagesPsychologys Factors of Stock Buying and PDFGabrė FrancisNo ratings yet

Download as pdf or txt

You might also like

- CMT Curriculum 2021 LEVEL II Wiley FINALDocument14 pagesCMT Curriculum 2021 LEVEL II Wiley FINALJamesMc114433% (3)

- Corporate FinanceDocument13 pagesCorporate FinanceNguyễn Thanh LâmNo ratings yet

- Ema Ge Berk CF 2GE SG 23Document12 pagesEma Ge Berk CF 2GE SG 23Sascha SaschaNo ratings yet

- CFA Level III 2010 Exam AnswersDocument67 pagesCFA Level III 2010 Exam AnswersAkash KumarNo ratings yet

- A Game Theoretic Framework of TrustDocument13 pagesA Game Theoretic Framework of TrustBaasit ShariefNo ratings yet

- Financial Management - Grinblatt and TitmanDocument68 pagesFinancial Management - Grinblatt and TitmanLuis Daniel Malavé RojasNo ratings yet

- Topic 2 - Equity 1 AnsDocument6 pagesTopic 2 - Equity 1 AnsGaba RieleNo ratings yet

- Topic 3 - Equity 2 Ans 2019-20Document6 pagesTopic 3 - Equity 2 Ans 2019-20Gaba RieleNo ratings yet

- Chapter 4 FIDocument7 pagesChapter 4 FIsitina.at.lunarNo ratings yet

- Chapter 13. Market EfficiencyDocument3 pagesChapter 13. Market EfficiencyHastings KapalaNo ratings yet

- Bachelor of Business Administration-BBA: Semester 5 BB0022 Capital and Money Market - 4 Credits Assignment (60 Marks)Document8 pagesBachelor of Business Administration-BBA: Semester 5 BB0022 Capital and Money Market - 4 Credits Assignment (60 Marks)Devlean Bhowal100% (1)

- Efficient Capital MarketDocument3 pagesEfficient Capital MarketTaimoorKhanNo ratings yet

- Dissertation ReportDocument53 pagesDissertation ReportPriyanka GroverNo ratings yet

- Proportional To Shares OwnedDocument6 pagesProportional To Shares OwnedArham KothariNo ratings yet

- Management of Financial Institutions - BUP - Lecture 06Document30 pagesManagement of Financial Institutions - BUP - Lecture 06Kaniz Fatama MimNo ratings yet

- Buy Back of SharesDocument10 pagesBuy Back of SharesRajgor ShrushtiNo ratings yet

- Chapter 4 FIDocument7 pagesChapter 4 FISeid KassawNo ratings yet

- Unit 1: Understanding Equity: Public Equity Vs Private EquityDocument10 pagesUnit 1: Understanding Equity: Public Equity Vs Private EquityPulkit AggarwalNo ratings yet

- Oneliners P1Document4 pagesOneliners P1Nirvana BoyNo ratings yet

- Financial Matter1 PDFDocument42 pagesFinancial Matter1 PDFDrNaveed Ul HaqNo ratings yet

- Stock Market Efficiency & Stock ValuationDocument23 pagesStock Market Efficiency & Stock ValuationKaila SalemNo ratings yet

- Current Stock Market Scenario-Delisting OffersDocument4 pagesCurrent Stock Market Scenario-Delisting OffersSNo ratings yet

- Merger & Acquisition: Defences Against Unwelcome TakeoversDocument22 pagesMerger & Acquisition: Defences Against Unwelcome TakeoversViraj GawandeNo ratings yet

- Chapter 3: Stock Valuation Methods and Efficient Market HypothesisDocument5 pagesChapter 3: Stock Valuation Methods and Efficient Market HypothesisPablo EkskobaNo ratings yet

- BM 204 2020 Module Investment ApprochesDocument36 pagesBM 204 2020 Module Investment ApprochesPhebieon MukwenhaNo ratings yet

- S A A I M: Ecurity Nalysis ND Nvestment AnagementDocument38 pagesS A A I M: Ecurity Nalysis ND Nvestment AnagementghanshyamvarshneyjiNo ratings yet

- Chapter 13 The Stock MarketDocument7 pagesChapter 13 The Stock Marketlasha KachkachishviliNo ratings yet

- Chapter 6: Answers To Concepts in Review: Fundamentals of Investing, by Gitman and JoehnkDocument6 pagesChapter 6: Answers To Concepts in Review: Fundamentals of Investing, by Gitman and JoehnkLouina YnciertoNo ratings yet

- Learning Module #3 Investment and Portfolio Management: Participating, and Cumulative and ParticipatingDocument6 pagesLearning Module #3 Investment and Portfolio Management: Participating, and Cumulative and ParticipatingAira AbigailNo ratings yet

- Imbalances Created Because of Structured Products in India Equity MarketsDocument8 pagesImbalances Created Because of Structured Products in India Equity MarketsManmohan BhartiaNo ratings yet

- T FDocument3 pagesT Faquarius21012003No ratings yet

- Describe The Nature of The Stock MarketDocument4 pagesDescribe The Nature of The Stock MarketJerbert JesalvaNo ratings yet

- Unit 8Document4 pagesUnit 8Loan NguyễnNo ratings yet

- The Efficient Market HypothesisDocument6 pagesThe Efficient Market HypothesisSeemaNo ratings yet

- Stock Market LearningDocument7 pagesStock Market LearningD P ChatterjeeNo ratings yet

- Chapter 6Document24 pagesChapter 6sdfklmjsdlklskfjd100% (2)

- Security Structures and Determining Enterprise Values FocusDocument24 pagesSecurity Structures and Determining Enterprise Values FocusMuhammad Qasim A20D047FNo ratings yet

- General Mathematics Basic Concepts of Stocks and BondsDocument5 pagesGeneral Mathematics Basic Concepts of Stocks and BondsGyle Contawe Garcia86% (7)

- BD Job Traning Session 4Document58 pagesBD Job Traning Session 4Mamun ReturnNo ratings yet

- Silo - Tips - Chapter 10 Stocks and Their Valuation Answers To End of Chapter QuestionsDocument19 pagesSilo - Tips - Chapter 10 Stocks and Their Valuation Answers To End of Chapter QuestionsBeatrice ReynanciaNo ratings yet

- Stock Market I. What Are Stocks?Document9 pagesStock Market I. What Are Stocks?JehannahBaratNo ratings yet

- Common Stocks: SummaryDocument5 pagesCommon Stocks: SummaryZain MughalNo ratings yet

- Project On Reliance BuybackDocument17 pagesProject On Reliance Buybackamin pattaniNo ratings yet

- Equity QUIZDocument8 pagesEquity QUIZSaYeD SeeDooNo ratings yet

- Investing in Stocks and BondsDocument89 pagesInvesting in Stocks and BondsLimSiEianNo ratings yet

- BFC5935 - Tutorial 4 SolutionsDocument6 pagesBFC5935 - Tutorial 4 SolutionsXue XuNo ratings yet

- D - Tutorial 9 (Solutions)Document13 pagesD - Tutorial 9 (Solutions)AlfieNo ratings yet

- 2023 Financial Eco Chapters 11 and 12 Lecture SlidesDocument49 pages2023 Financial Eco Chapters 11 and 12 Lecture SlidesmrsmasandaNo ratings yet

- Chap 14 SolutionsDocument10 pagesChap 14 SolutionsMiftahudin Miftahudin100% (1)

- Chapter 12 - PART 2Document11 pagesChapter 12 - PART 2Maya RamadhaniyatiNo ratings yet

- Sources of Finance (Equity)Document10 pagesSources of Finance (Equity)Dayaan ANo ratings yet

- Buy-Side M&ADocument8 pagesBuy-Side M&ALeonardoNo ratings yet

- Lesson 6. Equity MarketDocument12 pagesLesson 6. Equity Markethoneymaetreseni26No ratings yet

- Essay Question For Final ExamDocument5 pagesEssay Question For Final ExamKhoa LêNo ratings yet

- Concept Questions - Chapter 19Document2 pagesConcept Questions - Chapter 19husseinNo ratings yet

- RELATIVE VALUATION Theory PDFDocument5 pagesRELATIVE VALUATION Theory PDFPrateek SidharNo ratings yet

- Stock Investment DefinedDocument5 pagesStock Investment DefinedRoger Paul Singidas FuentesNo ratings yet

- A Stock Split or Stock Divide Increases or Decreases The Number of Shares in A PublicDocument11 pagesA Stock Split or Stock Divide Increases or Decreases The Number of Shares in A Publicsanjay mehtaNo ratings yet

- What Is A Stock?: Stock Market Equity MarketDocument3 pagesWhat Is A Stock?: Stock Market Equity MarketJob KurienNo ratings yet

- Module 4Document22 pagesModule 4mohibjahangir01No ratings yet

- Mastering the Market: A Comprehensive Guide to Successful Stock InvestingFrom EverandMastering the Market: A Comprehensive Guide to Successful Stock InvestingNo ratings yet

- Mastering the Markets: Advanced Trading Strategies for Success and Ethical Trading PracticesFrom EverandMastering the Markets: Advanced Trading Strategies for Success and Ethical Trading PracticesNo ratings yet

- 5.09 Analysis of Income Taxes - AnswersDocument38 pages5.09 Analysis of Income Taxes - Answersgustavo eichholzNo ratings yet

- 6.01 Market Organization and Structure - AnswersDocument56 pages6.01 Market Organization and Structure - Answersgustavo eichholzNo ratings yet

- 6.01 Market Organization and StructureDocument13 pages6.01 Market Organization and Structuregustavo eichholzNo ratings yet

- 1.05 Portfolio MathematicsDocument3 pages1.05 Portfolio Mathematicsgustavo eichholzNo ratings yet

- 4.05 Capital Investments and Capital Allocation - AnswersDocument33 pages4.05 Capital Investments and Capital Allocation - Answersgustavo eichholzNo ratings yet

- 4.07 Business ModelsDocument1 page4.07 Business Modelsgustavo eichholzNo ratings yet

- Mock Exam 2023 #4 First Session Ethical and Professional StandardsDocument91 pagesMock Exam 2023 #4 First Session Ethical and Professional Standardsgustavo eichholzNo ratings yet

- 2.06 International Trade - AnswersDocument10 pages2.06 International Trade - Answersgustavo eichholzNo ratings yet

- 1.01 Rates and ReturnsDocument12 pages1.01 Rates and Returnsgustavo eichholzNo ratings yet

- 1.08 Hypothesis TestingDocument7 pages1.08 Hypothesis Testinggustavo eichholzNo ratings yet

- 1.02 The Time Value of Money in FinanceDocument1 page1.02 The Time Value of Money in Financegustavo eichholzNo ratings yet

- 1.08 Hypothesis Testing - AnswersDocument29 pages1.08 Hypothesis Testing - Answersgustavo eichholzNo ratings yet

- 4.02 Investors and Other StakeholdersDocument2 pages4.02 Investors and Other Stakeholdersgustavo eichholzNo ratings yet

- 4.03 Corporate Governance - Conflicts, Mechanisms, Risks, and BenefitsDocument3 pages4.03 Corporate Governance - Conflicts, Mechanisms, Risks, and Benefitsgustavo eichholzNo ratings yet

- 4.07 Business ModelsDocument1 page4.07 Business Modelsgustavo eichholzNo ratings yet

- 15 1391bsacInternationalCenterforLaw&EconomicsandScholarsofLawandEconomicsDocument36 pages15 1391bsacInternationalCenterforLaw&EconomicsandScholarsofLawandEconomicsrobertNo ratings yet

- Impact of Behavioral Finance & Traditional Finance On Financial Decision Making ProcessDocument8 pagesImpact of Behavioral Finance & Traditional Finance On Financial Decision Making ProcessUbaid DarNo ratings yet

- The Oxford Handbook of Ethics and Economics White Ebook Full ChapterDocument51 pagesThe Oxford Handbook of Ethics and Economics White Ebook Full Chapterandrew.glidewell897100% (18)

- Barclays Wealth InsightsDocument32 pagesBarclays Wealth Insightsnarayan.mitNo ratings yet

- Data Mentah18 Desember 2020Document23 pagesData Mentah18 Desember 2020fathur abrarNo ratings yet

- Module 5.1. Market Anomalies - Behavioural.psychological - FactorsDocument30 pagesModule 5.1. Market Anomalies - Behavioural.psychological - FactorsakwoviahNo ratings yet

- K Kiran Kumar: Any Questions? Behavioral Finance, Netscape IPO, ReviewDocument33 pagesK Kiran Kumar: Any Questions? Behavioral Finance, Netscape IPO, ReviewJohn DoeNo ratings yet

- 1 - Introduction Behavioral EconomicsDocument3 pages1 - Introduction Behavioral EconomicsPyan AminNo ratings yet

- Rational Expectation Theory Assingment by Naseer AhmadDocument12 pagesRational Expectation Theory Assingment by Naseer AhmadNaseerNo ratings yet

- All Bullish Candlestick Pattern by Optrading00 Telegram Optrading00Document25 pagesAll Bullish Candlestick Pattern by Optrading00 Telegram Optrading00Samitm TamhankarNo ratings yet

- Alchian - Incertidumbre, Evolución y Teoría EconómicaDocument19 pagesAlchian - Incertidumbre, Evolución y Teoría EconómicaKatherineNo ratings yet

- Psychological Biases, Main Factors of Financial Behaviour - A Literature ReviewDocument11 pagesPsychological Biases, Main Factors of Financial Behaviour - A Literature ReviewNi Wayan Radha MaharseniNo ratings yet

- Indian Stock MarketDocument197 pagesIndian Stock Marketdeepsam88No ratings yet

- Fullpaper Icopss2017 PDFDocument1,095 pagesFullpaper Icopss2017 PDFNurul AidaNo ratings yet

- The Dynamics of Financial Markets: Fibonacci Numbers, Elliott Waves, and SolitonsDocument27 pagesThe Dynamics of Financial Markets: Fibonacci Numbers, Elliott Waves, and SolitonsCPV994No ratings yet

- Behavioral FinanceDocument115 pagesBehavioral FinancekenNo ratings yet

- Behavioural Biases Theories 2nd ChapterDocument26 pagesBehavioural Biases Theories 2nd Chaptersadhana gawade/AwateNo ratings yet

- Revue AERES HCERES Mars2016Document727 pagesRevue AERES HCERES Mars2016Emy des JardinsNo ratings yet

- Role of Behavioral Finance in Investment Decision - A Study of Investment Behavior in IndiaDocument12 pagesRole of Behavioral Finance in Investment Decision - A Study of Investment Behavior in IndiaVishal ShimpiNo ratings yet

- Dan Ariely - The Upside of IrrationalityDocument11 pagesDan Ariely - The Upside of IrrationalityJasvinder TanejaNo ratings yet

- Week 4 Concept of Behavioural BiasesDocument11 pagesWeek 4 Concept of Behavioural BiasesShirin RazdanNo ratings yet

- Big Data in FinannceDocument14 pagesBig Data in FinannceTrần Thị Thuỷ TiênNo ratings yet

- Hum1046 PPT (17543)Document329 pagesHum1046 PPT (17543)shri shubhamNo ratings yet

- Coronavirus Crisis and Behavioural EconomicsDocument36 pagesCoronavirus Crisis and Behavioural Economicsrakesh khuranaNo ratings yet

- Reading 52 - Behavioral Biases of IndividualsDocument12 pagesReading 52 - Behavioral Biases of IndividualsAllen AravindanNo ratings yet

- MCQ - Behavioural EconomicsDocument12 pagesMCQ - Behavioural EconomicsMelaku GemedaNo ratings yet

- Psychologys Factors of Stock Buying and PDFDocument12 pagesPsychologys Factors of Stock Buying and PDFGabrė FrancisNo ratings yet