Ckyc PWC Mu PDF

Ckyc PWC Mu PDF

You might also like

- Juan J. Linz - Alfred Stepan - Jaun J. Linz - Problems of Democratic Transition and Consolidation - Southern Europe, South America, and Post-Communist Europe-Johns Hopkins University Press (1996) PDFDocument502 pagesJuan J. Linz - Alfred Stepan - Jaun J. Linz - Problems of Democratic Transition and Consolidation - Southern Europe, South America, and Post-Communist Europe-Johns Hopkins University Press (1996) PDFBoavida Simia Penicela100% (5)

- Waldo Case SolDocument3 pagesWaldo Case Solvishal nigam100% (2)

- Bi1000541546 8100183438MHC12021 10012021 1448Document1 pageBi1000541546 8100183438MHC12021 10012021 1448Yuna SyNo ratings yet

- Pega Ds Know Your Customer Kyc FrameworkDocument2 pagesPega Ds Know Your Customer Kyc FrameworkAnuragNo ratings yet

- EXIM INDIA BlockchainDocument18 pagesEXIM INDIA BlockchainKrish GopalakrishnanNo ratings yet

- Transforming The Know Your Customer (KYC) Process Using BlockchainDocument5 pagesTransforming The Know Your Customer (KYC) Process Using BlockchainHarshal DahatNo ratings yet

- Digital KYC Digitals Next FrontierDocument8 pagesDigital KYC Digitals Next Frontiersaramoujit131521No ratings yet

- Digital KYC Utility For UAE Concept PaperDocument12 pagesDigital KYC Utility For UAE Concept PaperRay deeNo ratings yet

- Week2 Kyc Blockchain White PaperDocument14 pagesWeek2 Kyc Blockchain White Paperkv55ggnhxvNo ratings yet

- The Heart of The MatterDocument10 pagesThe Heart of The MattermedellincolombiaNo ratings yet

- Hackcelerator Problem StatementsDocument72 pagesHackcelerator Problem StatementsVenp Pe100% (1)

- Optimization of KYC ProcessesDocument12 pagesOptimization of KYC ProcessesTrina KundiNo ratings yet

- WE GOT This.: Tackle Specialized Training Needs With ACFCS Custom Live Online LearningDocument2 pagesWE GOT This.: Tackle Specialized Training Needs With ACFCS Custom Live Online LearningArtur GolbanNo ratings yet

- Know Your Client (Kyc) Compliance: Practical Considerations For Capital Markets ParticipantsDocument8 pagesKnow Your Client (Kyc) Compliance: Practical Considerations For Capital Markets ParticipantsshriyankaNo ratings yet

- How To Better Understand Your Customers Using ContextDocument20 pagesHow To Better Understand Your Customers Using ContextAmitNo ratings yet

- KYCDocument6 pagesKYCShounak BafnaNo ratings yet

- Guide-To-Digital-Identity-Verification-Report 9Document1 pageGuide-To-Digital-Identity-Verification-Report 9Роман КунькоNo ratings yet

- Efficient Client Onboarding The Key To Empowering Banks PDFDocument9 pagesEfficient Client Onboarding The Key To Empowering Banks PDFsaumilshuklaNo ratings yet

- Central KYC: What It Means For Investors and InstitutionsDocument8 pagesCentral KYC: What It Means For Investors and InstitutionsAmrut SuryawanshiNo ratings yet

- PB 24 - KYC Practices in IndonesiaDocument14 pagesPB 24 - KYC Practices in IndonesiaBabe GueNo ratings yet

- Blockchain in Fin-Tech Sector.Document9 pagesBlockchain in Fin-Tech Sector.Himanshu SinghNo ratings yet

- 15.217+Blockchain+Lab MAS+KYC+Final+ReportDocument23 pages15.217+Blockchain+Lab MAS+KYC+Final+ReportHariprasath GanapathiNo ratings yet

- KYC - DM - Presentation - AmendedDocument104 pagesKYC - DM - Presentation - AmendedBarisa IbrahimNo ratings yet

- KYC Models and Mechanisms Ragnar Toomla SEB May 2019Document22 pagesKYC Models and Mechanisms Ragnar Toomla SEB May 2019Idea HayneNo ratings yet

- Possible Designs of CBDCDocument3 pagesPossible Designs of CBDCSachin ChauhanNo ratings yet

- Way To Manage KYCDocument11 pagesWay To Manage KYCVipul JainNo ratings yet

- Swift Gpi Business Case EbookDocument14 pagesSwift Gpi Business Case EbookBeniamin KohanNo ratings yet

- COTI Overview DocumentDocument40 pagesCOTI Overview DocumentDisneyboi100% (1)

- RBI Circulars March 2023Document8 pagesRBI Circulars March 2023Udya singhNo ratings yet

- The Digital Real: Brazilian CBDCDocument17 pagesThe Digital Real: Brazilian CBDCViviane BocalonNo ratings yet

- Payments 2020Document35 pagesPayments 2020hitesh_urlNo ratings yet

- DT MT Banking Blockchain ApplicationsDocument4 pagesDT MT Banking Blockchain ApplicationsEuber ChaiaNo ratings yet

- TCS Lending and SecuritisationDocument12 pagesTCS Lending and SecuritisationSoumiya MuthurajaNo ratings yet

- Swift Paper Iso20022Document8 pagesSwift Paper Iso20022MaBe Saltos López0% (1)

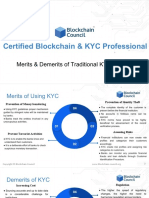

- Merits - Demerits of Traditional KYC Process PDFDocument4 pagesMerits - Demerits of Traditional KYC Process PDFvivxtractNo ratings yet

- Swift MCB Gpi CasestudyDocument2 pagesSwift MCB Gpi Casestudydicky bhaktiNo ratings yet

- Fenergo Remote Account Opening GenericDocument4 pagesFenergo Remote Account Opening GenericTope AjibadeNo ratings yet

- The Best Solution To Business Tasks of KYC, AML and Verification ProcedureDocument22 pagesThe Best Solution To Business Tasks of KYC, AML and Verification ProcedureIndra CiptaNo ratings yet

- Perpetual KycDocument4 pagesPerpetual KycAnjaly Ann JosephNo ratings yet

- Six Sigma in Credit Card OperationsDocument8 pagesSix Sigma in Credit Card Operationsdasguptasamrat26No ratings yet

- Open Banking API FrameworkDocument4 pagesOpen Banking API FrameworkChandra S0% (1)

- Best KYC SoftwareDocument10 pagesBest KYC SoftwareNazish JavedNo ratings yet

- Digital TransformationDocument16 pagesDigital Transformationyogita gore100% (1)

- RiskworkDocument180 pagesRiskworkUmar RajpootNo ratings yet

- Capstone ProjectDocument29 pagesCapstone ProjectPrashant A UNo ratings yet

- Reimagining KYC Blockchain 0716 1Document11 pagesReimagining KYC Blockchain 0716 1Vamsi YsNo ratings yet

- What Did We Cover in This Lecture? Introduced KYC, and Explore The Key Components That Make Up KYCDocument1 pageWhat Did We Cover in This Lecture? Introduced KYC, and Explore The Key Components That Make Up KYCSharadkumar HonakeriNo ratings yet

- Kyc Using Blockchain: Keywords: KYC (Know Your Customer), Block-Chain, Distributed EnvironmentDocument3 pagesKyc Using Blockchain: Keywords: KYC (Know Your Customer), Block-Chain, Distributed Environmentkiranmai AmbatiNo ratings yet

- KYC Verification Using BlockchainDocument7 pagesKYC Verification Using BlockchainIJRASETPublicationsNo ratings yet

- 72825cajournal Feb2023 22Document4 pages72825cajournal Feb2023 22S M SHEKARNo ratings yet

- Implementation of Secure Authentication Technologies For DFS 1 1 PDFDocument66 pagesImplementation of Secure Authentication Technologies For DFS 1 1 PDFdavidNo ratings yet

- PWC CBDC Global Index 1st Edition April 2021Document42 pagesPWC CBDC Global Index 1st Edition April 2021ForkLogNo ratings yet

- Future of Digital Currency in India 1694942271Document16 pagesFuture of Digital Currency in India 1694942271KeshavNo ratings yet

- TssDocument3 pagesTssShiv JumaniNo ratings yet

- IBC - Knowledge - CapsuleDocument5 pagesIBC - Knowledge - CapsulemurthyeNo ratings yet

- Blockchain Applications in Banking: Simon Mcnamara, Chief Administrative Officer, RbsDocument2 pagesBlockchain Applications in Banking: Simon Mcnamara, Chief Administrative Officer, Rbsquang NguyenNo ratings yet

- Blockchain App in BankingDocument2 pagesBlockchain App in Bankingrahulverma9No ratings yet

- Top KYC AML Service Providers For Startups and Small BusinessesDocument27 pagesTop KYC AML Service Providers For Startups and Small BusinessesKYC AML GuideNo ratings yet

- Ey How CLM Transformation Is Helping Fis Drive Business Growth Eyg No 003441 19gblDocument11 pagesEy How CLM Transformation Is Helping Fis Drive Business Growth Eyg No 003441 19gblKiranKannanNo ratings yet

- Central Bank Digital Currency:: The Future of Payments For CorporatesDocument29 pagesCentral Bank Digital Currency:: The Future of Payments For CorporatesknwongabNo ratings yet

- Lending Case StudyDocument7 pagesLending Case Studyanon_821676994No ratings yet

- Automate Banking Compliance and Scale InnovationDocument15 pagesAutomate Banking Compliance and Scale InnovationMIGUELNo ratings yet

- Blockchain Technology for Paperless Trade Facilitation in MaldivesFrom EverandBlockchain Technology for Paperless Trade Facilitation in MaldivesNo ratings yet

- Za APCP Brochure Digital-1Document40 pagesZa APCP Brochure Digital-1Obi AgboNo ratings yet

- Borderlands Data Forum and Encyclopaedia Launch Report-FinalDocument17 pagesBorderlands Data Forum and Encyclopaedia Launch Report-FinalObi AgboNo ratings yet

- The State of Identification Systems in AfricaDocument68 pagesThe State of Identification Systems in AfricaObi AgboNo ratings yet

- Visions Thesis - Business Models in Data Ecosystems V2Document48 pagesVisions Thesis - Business Models in Data Ecosystems V2Obi AgboNo ratings yet

- Professional CV ResumeDocument1 pageProfessional CV ResumenetoameNo ratings yet

- Activity 1 FinMaDocument3 pagesActivity 1 FinMaDiomela BionganNo ratings yet

- Analysis Paper On FYRE FestivalDocument3 pagesAnalysis Paper On FYRE Festivalhbfernandez1No ratings yet

- Car Rental AgreementDocument5 pagesCar Rental AgreementRashid JamalNo ratings yet

- Wfvt618 Es - 1000 at 10 Bar VT - Advanced (60hz) KsaDocument152 pagesWfvt618 Es - 1000 at 10 Bar VT - Advanced (60hz) KsaMostafa SharafNo ratings yet

- Committee ChecklistDocument8 pagesCommittee ChecklistAhmad Saiful Ridzwan JaharuddinNo ratings yet

- Pooja 1234Document83 pagesPooja 1234PRIYANo ratings yet

- RVL 2-02-03 Digital Additional PracticeDocument3 pagesRVL 2-02-03 Digital Additional PracticeHajer MannaiNo ratings yet

- Ruigomez OppDocument8 pagesRuigomez OppdefiantdetectiveNo ratings yet

- PHD Thesis Publishers IndiaDocument4 pagesPHD Thesis Publishers Indiaambercarterknoxville100% (2)

- Affidavit of Seller and BuyerDocument2 pagesAffidavit of Seller and BuyerJRMSU Finance OfficeNo ratings yet

- Accounting Information System - Chapter 5 - ReviewerDocument8 pagesAccounting Information System - Chapter 5 - ReviewerSecret LangNo ratings yet

- Final Internship Report - Amber DasDocument19 pagesFinal Internship Report - Amber DasAmber DasNo ratings yet

- Grievance MachineryDocument19 pagesGrievance MachineryDlos ProNo ratings yet

- Email TemplatesDocument5 pagesEmail TemplatesSanjay KumarNo ratings yet

- Dev Package 2023-24 MarchDocument464 pagesDev Package 2023-24 MarchApp SoulsNo ratings yet

- Local Government Property Rules, 2003Document26 pagesLocal Government Property Rules, 2003Rizwan Shabbir100% (1)

- Indian Railway: A Research Paper ONDocument33 pagesIndian Railway: A Research Paper ONGourav RanaNo ratings yet

- Introduction To Consumer BehaviourDocument24 pagesIntroduction To Consumer BehaviourSatish ChandraNo ratings yet

- TD365 Tom FishingDocument19 pagesTD365 Tom Fishing100pjwNo ratings yet

- Agrarian Reform: ACRONYM/Spell Out Era/Period/Year ObjectivesDocument2 pagesAgrarian Reform: ACRONYM/Spell Out Era/Period/Year ObjectivesChelsy SantosNo ratings yet

- Options Futures and Other Derivatives Global 9th Edition Hull Test BankDocument35 pagesOptions Futures and Other Derivatives Global 9th Edition Hull Test Bankfranciscocarlsonkpyoz2100% (23)

- Fairfax's Investment Banking TermsDocument2 pagesFairfax's Investment Banking TermsDavid HundeyinNo ratings yet

- Supplier Registration Form: ChecklistDocument12 pagesSupplier Registration Form: ChecklistBùi Duy TâyNo ratings yet

- 7453 RSA Data Discovery For Archer - Customer Presentation v4Document19 pages7453 RSA Data Discovery For Archer - Customer Presentation v4Tarpan Stefan AlexandruNo ratings yet

- Chapter - 1 Economics The Story of Village Palampur: Portal For CBSE Notes, Test Papers, Sample Papers, Tips and TricksDocument2 pagesChapter - 1 Economics The Story of Village Palampur: Portal For CBSE Notes, Test Papers, Sample Papers, Tips and TricksRamya BNo ratings yet

Download as pdf or txt

You might also like

- Juan J. Linz - Alfred Stepan - Jaun J. Linz - Problems of Democratic Transition and Consolidation - Southern Europe, South America, and Post-Communist Europe-Johns Hopkins University Press (1996) PDFDocument502 pagesJuan J. Linz - Alfred Stepan - Jaun J. Linz - Problems of Democratic Transition and Consolidation - Southern Europe, South America, and Post-Communist Europe-Johns Hopkins University Press (1996) PDFBoavida Simia Penicela100% (5)

- Waldo Case SolDocument3 pagesWaldo Case Solvishal nigam100% (2)

- Bi1000541546 8100183438MHC12021 10012021 1448Document1 pageBi1000541546 8100183438MHC12021 10012021 1448Yuna SyNo ratings yet

- Pega Ds Know Your Customer Kyc FrameworkDocument2 pagesPega Ds Know Your Customer Kyc FrameworkAnuragNo ratings yet

- EXIM INDIA BlockchainDocument18 pagesEXIM INDIA BlockchainKrish GopalakrishnanNo ratings yet

- Transforming The Know Your Customer (KYC) Process Using BlockchainDocument5 pagesTransforming The Know Your Customer (KYC) Process Using BlockchainHarshal DahatNo ratings yet

- Digital KYC Digitals Next FrontierDocument8 pagesDigital KYC Digitals Next Frontiersaramoujit131521No ratings yet

- Digital KYC Utility For UAE Concept PaperDocument12 pagesDigital KYC Utility For UAE Concept PaperRay deeNo ratings yet

- Week2 Kyc Blockchain White PaperDocument14 pagesWeek2 Kyc Blockchain White Paperkv55ggnhxvNo ratings yet

- The Heart of The MatterDocument10 pagesThe Heart of The MattermedellincolombiaNo ratings yet

- Hackcelerator Problem StatementsDocument72 pagesHackcelerator Problem StatementsVenp Pe100% (1)

- Optimization of KYC ProcessesDocument12 pagesOptimization of KYC ProcessesTrina KundiNo ratings yet

- WE GOT This.: Tackle Specialized Training Needs With ACFCS Custom Live Online LearningDocument2 pagesWE GOT This.: Tackle Specialized Training Needs With ACFCS Custom Live Online LearningArtur GolbanNo ratings yet

- Know Your Client (Kyc) Compliance: Practical Considerations For Capital Markets ParticipantsDocument8 pagesKnow Your Client (Kyc) Compliance: Practical Considerations For Capital Markets ParticipantsshriyankaNo ratings yet

- How To Better Understand Your Customers Using ContextDocument20 pagesHow To Better Understand Your Customers Using ContextAmitNo ratings yet

- KYCDocument6 pagesKYCShounak BafnaNo ratings yet

- Guide-To-Digital-Identity-Verification-Report 9Document1 pageGuide-To-Digital-Identity-Verification-Report 9Роман КунькоNo ratings yet

- Efficient Client Onboarding The Key To Empowering Banks PDFDocument9 pagesEfficient Client Onboarding The Key To Empowering Banks PDFsaumilshuklaNo ratings yet

- Central KYC: What It Means For Investors and InstitutionsDocument8 pagesCentral KYC: What It Means For Investors and InstitutionsAmrut SuryawanshiNo ratings yet

- PB 24 - KYC Practices in IndonesiaDocument14 pagesPB 24 - KYC Practices in IndonesiaBabe GueNo ratings yet

- Blockchain in Fin-Tech Sector.Document9 pagesBlockchain in Fin-Tech Sector.Himanshu SinghNo ratings yet

- 15.217+Blockchain+Lab MAS+KYC+Final+ReportDocument23 pages15.217+Blockchain+Lab MAS+KYC+Final+ReportHariprasath GanapathiNo ratings yet

- KYC - DM - Presentation - AmendedDocument104 pagesKYC - DM - Presentation - AmendedBarisa IbrahimNo ratings yet

- KYC Models and Mechanisms Ragnar Toomla SEB May 2019Document22 pagesKYC Models and Mechanisms Ragnar Toomla SEB May 2019Idea HayneNo ratings yet

- Possible Designs of CBDCDocument3 pagesPossible Designs of CBDCSachin ChauhanNo ratings yet

- Way To Manage KYCDocument11 pagesWay To Manage KYCVipul JainNo ratings yet

- Swift Gpi Business Case EbookDocument14 pagesSwift Gpi Business Case EbookBeniamin KohanNo ratings yet

- COTI Overview DocumentDocument40 pagesCOTI Overview DocumentDisneyboi100% (1)

- RBI Circulars March 2023Document8 pagesRBI Circulars March 2023Udya singhNo ratings yet

- The Digital Real: Brazilian CBDCDocument17 pagesThe Digital Real: Brazilian CBDCViviane BocalonNo ratings yet

- Payments 2020Document35 pagesPayments 2020hitesh_urlNo ratings yet

- DT MT Banking Blockchain ApplicationsDocument4 pagesDT MT Banking Blockchain ApplicationsEuber ChaiaNo ratings yet

- TCS Lending and SecuritisationDocument12 pagesTCS Lending and SecuritisationSoumiya MuthurajaNo ratings yet

- Swift Paper Iso20022Document8 pagesSwift Paper Iso20022MaBe Saltos López0% (1)

- Merits - Demerits of Traditional KYC Process PDFDocument4 pagesMerits - Demerits of Traditional KYC Process PDFvivxtractNo ratings yet

- Swift MCB Gpi CasestudyDocument2 pagesSwift MCB Gpi Casestudydicky bhaktiNo ratings yet

- Fenergo Remote Account Opening GenericDocument4 pagesFenergo Remote Account Opening GenericTope AjibadeNo ratings yet

- The Best Solution To Business Tasks of KYC, AML and Verification ProcedureDocument22 pagesThe Best Solution To Business Tasks of KYC, AML and Verification ProcedureIndra CiptaNo ratings yet

- Perpetual KycDocument4 pagesPerpetual KycAnjaly Ann JosephNo ratings yet

- Six Sigma in Credit Card OperationsDocument8 pagesSix Sigma in Credit Card Operationsdasguptasamrat26No ratings yet

- Open Banking API FrameworkDocument4 pagesOpen Banking API FrameworkChandra S0% (1)

- Best KYC SoftwareDocument10 pagesBest KYC SoftwareNazish JavedNo ratings yet

- Digital TransformationDocument16 pagesDigital Transformationyogita gore100% (1)

- RiskworkDocument180 pagesRiskworkUmar RajpootNo ratings yet

- Capstone ProjectDocument29 pagesCapstone ProjectPrashant A UNo ratings yet

- Reimagining KYC Blockchain 0716 1Document11 pagesReimagining KYC Blockchain 0716 1Vamsi YsNo ratings yet

- What Did We Cover in This Lecture? Introduced KYC, and Explore The Key Components That Make Up KYCDocument1 pageWhat Did We Cover in This Lecture? Introduced KYC, and Explore The Key Components That Make Up KYCSharadkumar HonakeriNo ratings yet

- Kyc Using Blockchain: Keywords: KYC (Know Your Customer), Block-Chain, Distributed EnvironmentDocument3 pagesKyc Using Blockchain: Keywords: KYC (Know Your Customer), Block-Chain, Distributed Environmentkiranmai AmbatiNo ratings yet

- KYC Verification Using BlockchainDocument7 pagesKYC Verification Using BlockchainIJRASETPublicationsNo ratings yet

- 72825cajournal Feb2023 22Document4 pages72825cajournal Feb2023 22S M SHEKARNo ratings yet

- Implementation of Secure Authentication Technologies For DFS 1 1 PDFDocument66 pagesImplementation of Secure Authentication Technologies For DFS 1 1 PDFdavidNo ratings yet

- PWC CBDC Global Index 1st Edition April 2021Document42 pagesPWC CBDC Global Index 1st Edition April 2021ForkLogNo ratings yet

- Future of Digital Currency in India 1694942271Document16 pagesFuture of Digital Currency in India 1694942271KeshavNo ratings yet

- TssDocument3 pagesTssShiv JumaniNo ratings yet

- IBC - Knowledge - CapsuleDocument5 pagesIBC - Knowledge - CapsulemurthyeNo ratings yet

- Blockchain Applications in Banking: Simon Mcnamara, Chief Administrative Officer, RbsDocument2 pagesBlockchain Applications in Banking: Simon Mcnamara, Chief Administrative Officer, Rbsquang NguyenNo ratings yet

- Blockchain App in BankingDocument2 pagesBlockchain App in Bankingrahulverma9No ratings yet

- Top KYC AML Service Providers For Startups and Small BusinessesDocument27 pagesTop KYC AML Service Providers For Startups and Small BusinessesKYC AML GuideNo ratings yet

- Ey How CLM Transformation Is Helping Fis Drive Business Growth Eyg No 003441 19gblDocument11 pagesEy How CLM Transformation Is Helping Fis Drive Business Growth Eyg No 003441 19gblKiranKannanNo ratings yet

- Central Bank Digital Currency:: The Future of Payments For CorporatesDocument29 pagesCentral Bank Digital Currency:: The Future of Payments For CorporatesknwongabNo ratings yet

- Lending Case StudyDocument7 pagesLending Case Studyanon_821676994No ratings yet

- Automate Banking Compliance and Scale InnovationDocument15 pagesAutomate Banking Compliance and Scale InnovationMIGUELNo ratings yet

- Blockchain Technology for Paperless Trade Facilitation in MaldivesFrom EverandBlockchain Technology for Paperless Trade Facilitation in MaldivesNo ratings yet

- Za APCP Brochure Digital-1Document40 pagesZa APCP Brochure Digital-1Obi AgboNo ratings yet

- Borderlands Data Forum and Encyclopaedia Launch Report-FinalDocument17 pagesBorderlands Data Forum and Encyclopaedia Launch Report-FinalObi AgboNo ratings yet

- The State of Identification Systems in AfricaDocument68 pagesThe State of Identification Systems in AfricaObi AgboNo ratings yet

- Visions Thesis - Business Models in Data Ecosystems V2Document48 pagesVisions Thesis - Business Models in Data Ecosystems V2Obi AgboNo ratings yet

- Professional CV ResumeDocument1 pageProfessional CV ResumenetoameNo ratings yet

- Activity 1 FinMaDocument3 pagesActivity 1 FinMaDiomela BionganNo ratings yet

- Analysis Paper On FYRE FestivalDocument3 pagesAnalysis Paper On FYRE Festivalhbfernandez1No ratings yet

- Car Rental AgreementDocument5 pagesCar Rental AgreementRashid JamalNo ratings yet

- Wfvt618 Es - 1000 at 10 Bar VT - Advanced (60hz) KsaDocument152 pagesWfvt618 Es - 1000 at 10 Bar VT - Advanced (60hz) KsaMostafa SharafNo ratings yet

- Committee ChecklistDocument8 pagesCommittee ChecklistAhmad Saiful Ridzwan JaharuddinNo ratings yet

- Pooja 1234Document83 pagesPooja 1234PRIYANo ratings yet

- RVL 2-02-03 Digital Additional PracticeDocument3 pagesRVL 2-02-03 Digital Additional PracticeHajer MannaiNo ratings yet

- Ruigomez OppDocument8 pagesRuigomez OppdefiantdetectiveNo ratings yet

- PHD Thesis Publishers IndiaDocument4 pagesPHD Thesis Publishers Indiaambercarterknoxville100% (2)

- Affidavit of Seller and BuyerDocument2 pagesAffidavit of Seller and BuyerJRMSU Finance OfficeNo ratings yet

- Accounting Information System - Chapter 5 - ReviewerDocument8 pagesAccounting Information System - Chapter 5 - ReviewerSecret LangNo ratings yet

- Final Internship Report - Amber DasDocument19 pagesFinal Internship Report - Amber DasAmber DasNo ratings yet

- Grievance MachineryDocument19 pagesGrievance MachineryDlos ProNo ratings yet

- Email TemplatesDocument5 pagesEmail TemplatesSanjay KumarNo ratings yet

- Dev Package 2023-24 MarchDocument464 pagesDev Package 2023-24 MarchApp SoulsNo ratings yet

- Local Government Property Rules, 2003Document26 pagesLocal Government Property Rules, 2003Rizwan Shabbir100% (1)

- Indian Railway: A Research Paper ONDocument33 pagesIndian Railway: A Research Paper ONGourav RanaNo ratings yet

- Introduction To Consumer BehaviourDocument24 pagesIntroduction To Consumer BehaviourSatish ChandraNo ratings yet

- TD365 Tom FishingDocument19 pagesTD365 Tom Fishing100pjwNo ratings yet

- Agrarian Reform: ACRONYM/Spell Out Era/Period/Year ObjectivesDocument2 pagesAgrarian Reform: ACRONYM/Spell Out Era/Period/Year ObjectivesChelsy SantosNo ratings yet

- Options Futures and Other Derivatives Global 9th Edition Hull Test BankDocument35 pagesOptions Futures and Other Derivatives Global 9th Edition Hull Test Bankfranciscocarlsonkpyoz2100% (23)

- Fairfax's Investment Banking TermsDocument2 pagesFairfax's Investment Banking TermsDavid HundeyinNo ratings yet

- Supplier Registration Form: ChecklistDocument12 pagesSupplier Registration Form: ChecklistBùi Duy TâyNo ratings yet

- 7453 RSA Data Discovery For Archer - Customer Presentation v4Document19 pages7453 RSA Data Discovery For Archer - Customer Presentation v4Tarpan Stefan AlexandruNo ratings yet

- Chapter - 1 Economics The Story of Village Palampur: Portal For CBSE Notes, Test Papers, Sample Papers, Tips and TricksDocument2 pagesChapter - 1 Economics The Story of Village Palampur: Portal For CBSE Notes, Test Papers, Sample Papers, Tips and TricksRamya BNo ratings yet