Download as pdf or txt

You might also like

- Change Signatories ResolutionDocument2 pagesChange Signatories ResolutionJ J. Lamita93% (29)

- Pac All CAF Mocks With Solutions Compiled by Saboor AhmadDocument144 pagesPac All CAF Mocks With Solutions Compiled by Saboor AhmadRao Ali CA100% (2)

- Auditing The Control EnvironmentDocument37 pagesAuditing The Control Environmentsofyan timotyNo ratings yet

- Trust Receipt SampleDocument2 pagesTrust Receipt SampleCecil MaquirangNo ratings yet

- Rangkuman Pertemuan Auditing 1Document54 pagesRangkuman Pertemuan Auditing 1bangkutubuNo ratings yet

- Assurance Chapter-5 (04-09-2018)Document9 pagesAssurance Chapter-5 (04-09-2018)Shahid MahmudNo ratings yet

- Narrative: You Will Need A Copy of The Book As Future Reference Material For This PresentationDocument33 pagesNarrative: You Will Need A Copy of The Book As Future Reference Material For This PresentationRoifah AmeliaNo ratings yet

- P1-09 Management Control SystemsDocument24 pagesP1-09 Management Control Systemsmagnetbox8No ratings yet

- Chapter 4 - Internal ControlDocument60 pagesChapter 4 - Internal Controlyebegashet100% (1)

- Tests of ControlsDocument40 pagesTests of ControlsMuhammad SaqibNo ratings yet

- Imprest ReportDocument12 pagesImprest ReportRanjanNo ratings yet

- Internal Audit Training - 011948Document170 pagesInternal Audit Training - 011948aassweNo ratings yet

- Entity Level Controls in Internal AuditingDocument9 pagesEntity Level Controls in Internal Auditingmahmudtoha100% (1)

- PowerPoint PresentationDocument15 pagesPowerPoint PresentationMOHAMAD AMIRUL AINAN BIN BASHIR AHMAD MoeNo ratings yet

- INS3116 - CHAPTER 2 - Internal Control Framework - COSODocument25 pagesINS3116 - CHAPTER 2 - Internal Control Framework - COSOThuỳ Linh Bùi100% (1)

- APELOAD - Module 1Document7 pagesAPELOAD - Module 1Hermoine GrangerNo ratings yet

- Chapter 2 ControlDocument11 pagesChapter 2 ControlArizal Zul Lathiif0% (1)

- Larrys Cheat Sheet Auditing TechniquesDocument2 pagesLarrys Cheat Sheet Auditing TechniquesMay Chen100% (1)

- Assessing System of Internal ControlsDocument2 pagesAssessing System of Internal ControlsastiningrumdamayantiNo ratings yet

- Int Aud Chapter 9Document23 pagesInt Aud Chapter 9atiah zakariaNo ratings yet

- Assessing System of Internal ControlsDocument2 pagesAssessing System of Internal ControlsMary MwansaNo ratings yet

- Risk Assessment and Internal Control: CA Inter - Auditing and Assurance Additional Questions For Practice (Chapter 4)Document4 pagesRisk Assessment and Internal Control: CA Inter - Auditing and Assurance Additional Questions For Practice (Chapter 4)Annu DuaNo ratings yet

- 1 - Overview of AuditingDocument13 pages1 - Overview of AuditingZooeyNo ratings yet

- Control Environment Governance Audit 1585631025Document4 pagesControl Environment Governance Audit 1585631025Mohammed OsmanNo ratings yet

- MGT 209 - Overview of Internal ControlDocument8 pagesMGT 209 - Overview of Internal ControlCrystelNo ratings yet

- Review Questions: Chapter 21 - Internal, Operational, and Compliance AuditingDocument13 pagesReview Questions: Chapter 21 - Internal, Operational, and Compliance AuditingHeeyNo ratings yet

- Week 7 Audit Risk Assessment CanvasDocument61 pagesWeek 7 Audit Risk Assessment CanvasdelulublinkNo ratings yet

- Deloitte Uk Gif Internal Control and The Board November 2019Document8 pagesDeloitte Uk Gif Internal Control and The Board November 2019ahamidianNo ratings yet

- Lesson 1-Fundamental Principles of Operations AuditDocument9 pagesLesson 1-Fundamental Principles of Operations AuditLuiNo ratings yet

- ACCA SBL Chapter 12 Internal ControlDocument15 pagesACCA SBL Chapter 12 Internal ControlSeng Cheong KhorNo ratings yet

- Internal Audit RoleDocument12 pagesInternal Audit RoleBobbyD.ResjaNo ratings yet

- Acco 360 NotesDocument41 pagesAcco 360 NotesJessica HadzurikNo ratings yet

- Isa 315 GermicDocument3 pagesIsa 315 GermicDanica Christele AlfaroNo ratings yet

- Australian Beverages OHS FINALDocument41 pagesAustralian Beverages OHS FINALPauline VukiNo ratings yet

- Internal ControlDocument6 pagesInternal ControlVarun jajalNo ratings yet

- Deloitte Uk Audit Internal Controls Whats All The Fuss About June 2021Document8 pagesDeloitte Uk Audit Internal Controls Whats All The Fuss About June 2021Anand RajNo ratings yet

- Item 7aiii Internal Audit Report Is Service DeskDocument6 pagesItem 7aiii Internal Audit Report Is Service DesksamanNo ratings yet

- 05GeneralInternalControl NotesDocument13 pages05GeneralInternalControl NotesMussaNo ratings yet

- Internal Audit: Session 32Document26 pagesInternal Audit: Session 32Abdullah EjazNo ratings yet

- ch1 QADocument10 pagesch1 QARamez RedaNo ratings yet

- Chapter 2.2022 EnglishDocument59 pagesChapter 2.2022 Englishcamnhu622003No ratings yet

- Chapter 2 - Audit Strategy, Planning & Programming: Stages of Audit ExecutionDocument17 pagesChapter 2 - Audit Strategy, Planning & Programming: Stages of Audit Executionmaulesh bhattNo ratings yet

- AI - Modul 7 (INTERNAL CONTROL)Document30 pagesAI - Modul 7 (INTERNAL CONTROL)Lusi NuryantiNo ratings yet

- Pullout II 11 Practices 10 1 and 10 2Document9 pagesPullout II 11 Practices 10 1 and 10 2Ermi ManNo ratings yet

- Audit Part 4Document33 pagesAudit Part 4Florent AlvesNo ratings yet

- MODULE 4 Control FrameworkDocument9 pagesMODULE 4 Control FrameworkEric CauilanNo ratings yet

- Template Presentation - Entrance and Exit MeetingsDocument48 pagesTemplate Presentation - Entrance and Exit MeetingsRheneir MoraNo ratings yet

- AUD Internal ControlDocument11 pagesAUD Internal ControlChrismand CongeNo ratings yet

- Presentation by Mr. Mohammad Abbas Head of Internal Audit EFU Life Assurance LTDDocument134 pagesPresentation by Mr. Mohammad Abbas Head of Internal Audit EFU Life Assurance LTDSahilemariamNo ratings yet

- AU 9 Consideration of ICDocument11 pagesAU 9 Consideration of ICJb MejiaNo ratings yet

- Chapter 3 Risk Assement & Internal ControlDocument54 pagesChapter 3 Risk Assement & Internal ControlRohit Kumar SantukaNo ratings yet

- 8 RiskDocument31 pages8 RiskSadrul Amin SujonNo ratings yet

- Internal Control and RiskDocument9 pagesInternal Control and RiskdominicNo ratings yet

- OM and CourseMaterial of CertificateProgramme On Internal AuditDocument404 pagesOM and CourseMaterial of CertificateProgramme On Internal AuditMRL AccountsNo ratings yet

- Solution Manual For Internal Auditing Assurance and Consulting Services 2nd Edition by RedingDocument9 pagesSolution Manual For Internal Auditing Assurance and Consulting Services 2nd Edition by RedingBrianWelchxqdm100% (42)

- Audit and Assuarance C1Document62 pagesAudit and Assuarance C1Phạm Mình CongNo ratings yet

- Internal Controls PreviousDocument12 pagesInternal Controls PreviousMike dzielakNo ratings yet

- GBERMICDocument3 pagesGBERMICAnnyeong AngeNo ratings yet

- Ai - PPT 7 (Internal Control)Document30 pagesAi - PPT 7 (Internal Control)diana_busrizalti100% (1)

- 2 Aci Assessing System Internal Control Fs Uk v4 LR PDFDocument2 pages2 Aci Assessing System Internal Control Fs Uk v4 LR PDFFira NoverinaNo ratings yet

- Corporate Governance and Internal AuditDocument10 pagesCorporate Governance and Internal AuditItdarareNo ratings yet

- The Sarbanes-Oxley Section 404 Implementation Toolkit: Practice Aids for Managers and AuditorsFrom EverandThe Sarbanes-Oxley Section 404 Implementation Toolkit: Practice Aids for Managers and AuditorsNo ratings yet

- The Art and Science of Auditing: Principles, Practices, and InsightsFrom EverandThe Art and Science of Auditing: Principles, Practices, and InsightsNo ratings yet

- Baker Ab - Az.chap019Document40 pagesBaker Ab - Az.chap019magnetbox8No ratings yet

- Baker Ab - Az.chap014Document40 pagesBaker Ab - Az.chap014magnetbox8No ratings yet

- Financial Reporting Class NoteDocument9 pagesFinancial Reporting Class Notemagnetbox8No ratings yet

- Consolidation Ownership Issues: Mcgraw-Hill/IrwinDocument41 pagesConsolidation Ownership Issues: Mcgraw-Hill/Irwinmagnetbox8No ratings yet

- The Examiner's Answers For Financial Strategy: Section ADocument18 pagesThe Examiner's Answers For Financial Strategy: Section Amagnetbox8No ratings yet

- Corporate Reporting (International) : Tuesday 15 June 2010Document7 pagesCorporate Reporting (International) : Tuesday 15 June 2010magnetbox8No ratings yet

- May 2006 Examinations: Strategy LevelDocument32 pagesMay 2006 Examinations: Strategy Levelmagnetbox8No ratings yet

- 8143 Companies Income Tax (Amendment) Act, 2007Document10 pages8143 Companies Income Tax (Amendment) Act, 2007magnetbox8No ratings yet

- Partnerships: Liquidation: Mcgraw-Hill/IrwinDocument25 pagesPartnerships: Liquidation: Mcgraw-Hill/Irwinmagnetbox8No ratings yet

- LixingcunDocument11 pagesLixingcunmagnetbox8No ratings yet

- 15 Af 503 sfm61Document4 pages15 Af 503 sfm61magnetbox8No ratings yet

- Corporate Reporting (International) : Tuesday 14 June 2011Document8 pagesCorporate Reporting (International) : Tuesday 14 June 2011magnetbox8No ratings yet

- Pakistan: Monday, The 17th February 2014Document4 pagesPakistan: Monday, The 17th February 2014magnetbox8No ratings yet

- T4 May 2014 - For PublicationDocument28 pagesT4 May 2014 - For Publicationmagnetbox8No ratings yet

- T4 - Part B Case Study Examination: Tuesday 25 February 2014Document28 pagesT4 - Part B Case Study Examination: Tuesday 25 February 2014magnetbox8No ratings yet

- T4 - Part B Case Study Examination: Wednesday 28 August 2013Document32 pagesT4 - Part B Case Study Examination: Wednesday 28 August 2013magnetbox8No ratings yet

- Western Mindanao Adventist Academy 7028 Dumingag, Zamboanga Del Sur, PhilippinesDocument9 pagesWestern Mindanao Adventist Academy 7028 Dumingag, Zamboanga Del Sur, PhilippinesJoyce Torres100% (1)

- Agreement 10256805 PDFDocument2 pagesAgreement 10256805 PDF1030sqrpioNo ratings yet

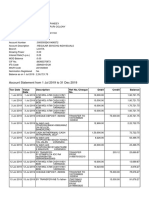

- Account Statement From 1 Jul 2019 To 31 Dec 2019: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument2 pagesAccount Statement From 1 Jul 2019 To 31 Dec 2019: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balancepratibha guptaNo ratings yet

- Eastern Mindoro College Bongabong, Oriental Mindoro Telefax (043) 2835479 E-MailDocument2 pagesEastern Mindoro College Bongabong, Oriental Mindoro Telefax (043) 2835479 E-MailPrecilla Zoleta SosaNo ratings yet

- Principles of Business For CSEC®: 2nd EditionDocument3 pagesPrinciples of Business For CSEC®: 2nd Editionyuvita prasadNo ratings yet

- Account Ledger Report: Sahajanand World TravelsDocument10 pagesAccount Ledger Report: Sahajanand World Travelsjayesh mehtaNo ratings yet

- Bill of Exchange 2Document14 pagesBill of Exchange 2uthaman gopalanNo ratings yet

- Midterm Exam 2021 With Suggested Answers ReviewerDocument8 pagesMidterm Exam 2021 With Suggested Answers ReviewerNanya BisnestNo ratings yet

- U.S. GAAP vs. IFRS: Fair Value Measurements: Prepared byDocument4 pagesU.S. GAAP vs. IFRS: Fair Value Measurements: Prepared byTempleton FerrariNo ratings yet

- 3 Statement Model Alphabet GoogleDocument8 pages3 Statement Model Alphabet GoogleSimran GargNo ratings yet

- CAPM Problems Advanced, CAPM and DDMDocument2 pagesCAPM Problems Advanced, CAPM and DDMshivushiv8431No ratings yet

- Modul AKLII-2 - Investor Acc MethodDocument31 pagesModul AKLII-2 - Investor Acc MethodLisa SilviNo ratings yet

- Geva 2008 - Payment Finality and Discharge in Funds TransfersDocument45 pagesGeva 2008 - Payment Finality and Discharge in Funds Transferssebastian agudeloNo ratings yet

- Backup Whatzap 26/09/19Document2 pagesBackup Whatzap 26/09/19RIO DE JANEIRONo ratings yet

- Capital FirstDocument34 pagesCapital FirstgreyistariNo ratings yet

- HDFC Mid-Cap Opportunities Fund - Presentation (Apr 2023)Document28 pagesHDFC Mid-Cap Opportunities Fund - Presentation (Apr 2023)RajNo ratings yet

- Unaudited Consolidated Financial Statements: For The Nine Months Ended 30 September 2021Document10 pagesUnaudited Consolidated Financial Statements: For The Nine Months Ended 30 September 2021Fuaad DodooNo ratings yet

- Auto Loan IndustryDocument38 pagesAuto Loan IndustryVinay SinghNo ratings yet

- FAR Review MaterialDocument22 pagesFAR Review MaterialAntonette Eve CelomineNo ratings yet

- Insurance LawDocument12 pagesInsurance Lawvishal agarwalNo ratings yet

- (Ust-Jpia) Acc5115 Ifr Sce and SCF ReviewerDocument5 pages(Ust-Jpia) Acc5115 Ifr Sce and SCF Revieweraly kayleNo ratings yet

- Eclips Blackscreen Date 2023mayDocument2 pagesEclips Blackscreen Date 2023mayamodukanele83% (6)

- Liabilities To Equity Ratio: SolvancyDocument2 pagesLiabilities To Equity Ratio: SolvancyNarendra PatilNo ratings yet

- B7AF100 - 2021 - OMD1 - First Sitting Exam PaperDocument12 pagesB7AF100 - 2021 - OMD1 - First Sitting Exam PaperAZLEA BINTI SYED HUSSIN (BG)No ratings yet

- PPT-SEBI (ICDR) Regulations 2023Document6 pagesPPT-SEBI (ICDR) Regulations 2023ritu.kaushik.mba25No ratings yet

- Merchant Opportunities Fund OverviewDocument1 pageMerchant Opportunities Fund OverviewhoopburnNo ratings yet

- Finance Modeling Handbook (00000002)Document1 pageFinance Modeling Handbook (00000002)baronfgfNo ratings yet