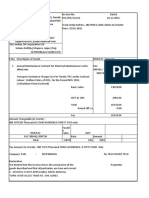

Margin Calculations 14122020

Margin Calculations 14122020

You might also like

- The Champion Legal Ads: 05-25-23Document54 pagesThe Champion Legal Ads: 05-25-23Donna S. SeayNo ratings yet

- Allocations of Risk Capital in Financial InstitutionsDocument25 pagesAllocations of Risk Capital in Financial Institutionssrikanth_balasubra_1No ratings yet

- Financial Risk Management: A Simple IntroductionFrom EverandFinancial Risk Management: A Simple IntroductionRating: 4.5 out of 5 stars4.5/5 (7)

- BIOETHICSDocument243 pagesBIOETHICSJoebeth Competente100% (5)

- Two Type of Margins Have Been SpecifiedDocument8 pagesTwo Type of Margins Have Been SpecifiedPraveen KumarNo ratings yet

- Settlement, Clearing & Risk ManagementDocument34 pagesSettlement, Clearing & Risk ManagementTapas Chandra RoyNo ratings yet

- Equity Risk Management and SLBDocument12 pagesEquity Risk Management and SLBepakhil01No ratings yet

- Chapter 5 - Multifactor Value at RiskDocument44 pagesChapter 5 - Multifactor Value at RiskVishwajit GoudNo ratings yet

- Chapter 4 Securities Operations and Risk Management PDFDocument84 pagesChapter 4 Securities Operations and Risk Management PDFMRIDUL GOELNo ratings yet

- Lecture Note 1 2Document163 pagesLecture Note 1 2Đỗ Thủy Tiên NguyễnNo ratings yet

- Tmspan Margining043001Document18 pagesTmspan Margining043001kunal bandawarNo ratings yet

- Chapter #7: Value Ate Risk (VAR)Document30 pagesChapter #7: Value Ate Risk (VAR)Smart UnlockerNo ratings yet

- Bench MarkingDocument14 pagesBench MarkingVenkatakrishnan IyerNo ratings yet

- Corporate Treasury Needs A Solid BasisDocument2 pagesCorporate Treasury Needs A Solid BasisKofikoduahNo ratings yet

- Multinational Corporations and Global Financial Environment: Facilities in More Than One CountryDocument11 pagesMultinational Corporations and Global Financial Environment: Facilities in More Than One CountryANH NGUYEN DANG QUENo ratings yet

- Mercurial Lite Paper v1Document9 pagesMercurial Lite Paper v1ivan chenNo ratings yet

- FRM Unit-2Document31 pagesFRM Unit-2prasanthi CNo ratings yet

- Revised Chapter 9Document25 pagesRevised Chapter 9Shahadat HossainNo ratings yet

- 17 Use of The Var Method For Measuring Market Risks and Calculating Capital AdequacyDocument5 pages17 Use of The Var Method For Measuring Market Risks and Calculating Capital AdequacyYounus AkhoonNo ratings yet

- Risk Management of A Cashflow Driven InvestmentDocument30 pagesRisk Management of A Cashflow Driven InvestmentRichard ChiangNo ratings yet

- Provision For Adverse DeviationsDocument7 pagesProvision For Adverse DeviationsAgnes MercyanaaNo ratings yet

- Acca Afm (P4)Document36 pagesAcca Afm (P4)SamanMurtazaNo ratings yet

- Nse Clear Backtesting PolicyDocument3 pagesNse Clear Backtesting PolicyJoshuaNo ratings yet

- Equity Risk Management PolicyDocument4 pagesEquity Risk Management PolicymkjailaniNo ratings yet

- Risk Management: Value at Risk MarginDocument3 pagesRisk Management: Value at Risk MarginrachealllNo ratings yet

- Common Stock Valuation - Part 1Document35 pagesCommon Stock Valuation - Part 1Mahmoud HassaanNo ratings yet

- 1Document5 pages1mkc2044No ratings yet

- Interest Rate Swaps (Final)Document35 pagesInterest Rate Swaps (Final)Harish SharmaNo ratings yet

- A Systematic Approach To Optimizing CollateralDocument7 pagesA Systematic Approach To Optimizing CollateralCognizantNo ratings yet

- Bond Portfolio Management StrategiesDocument36 pagesBond Portfolio Management StrategiesMuhammad HarisNo ratings yet

- VaR FRMDocument11 pagesVaR FRMshashanksrivatsa008No ratings yet

- Value To Change Because of A Change in Exchange Rates: Mearsuring and Managing Exposure To Exchange Rate FluctuationsDocument2 pagesValue To Change Because of A Change in Exchange Rates: Mearsuring and Managing Exposure To Exchange Rate FluctuationsQuỳnh GiangNo ratings yet

- Practical Ifrs 09Document10 pagesPractical Ifrs 09Farooq HaiderNo ratings yet

- Basel 1 - IntroductionDocument16 pagesBasel 1 - IntroductiondarbyglaceNo ratings yet

- AD477Document8 pagesAD477Mert BirerNo ratings yet

- 3.3. Management of Equity Price RiskDocument2 pages3.3. Management of Equity Price RiskTaher BarwaniwalaNo ratings yet

- Final FX Risk & Exposure ManagementDocument33 pagesFinal FX Risk & Exposure ManagementkarunaksNo ratings yet

- Bank and Insurance Domande V2Document6 pagesBank and Insurance Domande V2f.invernici2No ratings yet

- Chapter 7Document39 pagesChapter 7Aimes AliNo ratings yet

- FIN010 - Efficient Capital MarketsDocument3 pagesFIN010 - Efficient Capital MarketsLanz Mark RelovaNo ratings yet

- Equiy SwapsDocument6 pagesEquiy SwapsPenny Lyn CapsuyenNo ratings yet

- Estimating Long Term GrowthDocument12 pagesEstimating Long Term GrowthsamacsterNo ratings yet

- Capital Market Line and The Efficient FrontierDocument6 pagesCapital Market Line and The Efficient FrontierPushpa BaruaNo ratings yet

- Cost Volume Profit AnalysisDocument20 pagesCost Volume Profit Analysisrikesh radheNo ratings yet

- Staff Working Paper No. 597: A Comparative Analysis of Tools To Limit The Procyclicality of Initial Margin RequirementsDocument24 pagesStaff Working Paper No. 597: A Comparative Analysis of Tools To Limit The Procyclicality of Initial Margin RequirementsTBP_Think_TankNo ratings yet

- Performance AttributionDocument7 pagesPerformance AttributionMilind ParaleNo ratings yet

- Clearing and SettlementDocument19 pagesClearing and SettlementRESHMA JAYAKUMARNo ratings yet

- BRM Session 12 Credit Risk & Credit Risk ModellingDocument33 pagesBRM Session 12 Credit Risk & Credit Risk ModellingSrinita MishraNo ratings yet

- How Clearing WorksDocument4 pagesHow Clearing WorksEdward TaufikNo ratings yet

- BRM Session 6 Value at RiskDocument39 pagesBRM Session 6 Value at RiskSrinita MishraNo ratings yet

- Individual Currency Limits: Value-at-RiskDocument4 pagesIndividual Currency Limits: Value-at-RiskBinod Singh JeenaNo ratings yet

- 9 Week of Lectures: Financial Management - MGT201Document13 pages9 Week of Lectures: Financial Management - MGT201Syed Abdul Mussaver ShahNo ratings yet

- Sapm ModelsDocument20 pagesSapm ModelsAvinash TripathiNo ratings yet

- 1.2 StructuredDocument42 pages1.2 StructuredMahmoud Moh'dNo ratings yet

- Risk Premia Strategies B 102727740Document29 pagesRisk Premia Strategies B 102727740h_jacobson100% (4)

- Chapter 4Document10 pagesChapter 4Seid KassawNo ratings yet

- R Eplicating P Ortfolios and R Is K Management: Presented by Joshua Corrigan, Charles QinDocument37 pagesR Eplicating P Ortfolios and R Is K Management: Presented by Joshua Corrigan, Charles QinPratik BhagatNo ratings yet

- Case 13Document12 pagesCase 13Superb AdnanNo ratings yet

- ALM End Term MergedDocument78 pagesALM End Term MergedShruti VermaNo ratings yet

- Port Finance: Interest Rate Market On SolanaDocument11 pagesPort Finance: Interest Rate Market On SolanaMI POCOPHONENo ratings yet

- Port Finance: Interest Rate Market On SolanaDocument11 pagesPort Finance: Interest Rate Market On Solanaxiao dreNo ratings yet

- El Papel, LLC v. City of Seattle, No. 22-35656 (9th Cir. Oct. 26, 2023) (Memo.)Document6 pagesEl Papel, LLC v. City of Seattle, No. 22-35656 (9th Cir. Oct. 26, 2023) (Memo.)RHTNo ratings yet

- Inter Se BiddingDocument7 pagesInter Se BiddingyamikaNo ratings yet

- Topic 2.demand Supply UpdatedDocument110 pagesTopic 2.demand Supply UpdatedNguyên TúNo ratings yet

- Bike2424 PDFDocument1 pageBike2424 PDFAntonijVedernikovNo ratings yet

- Exhibit 10Document10 pagesExhibit 10Steve JosephNo ratings yet

- Salcomp Corporate Governance Statement 2009 PDFDocument10 pagesSalcomp Corporate Governance Statement 2009 PDFRajsundarNo ratings yet

- PWDCertificateDocument1 pagePWDCertificateBipin PatilNo ratings yet

- Program Officer SOPsDocument3 pagesProgram Officer SOPsshaikhsamsaeed786No ratings yet

- CMP Mobilizers AccreditationDocument4 pagesCMP Mobilizers AccreditationJayson De LemonNo ratings yet

- Sourav Bhuiyan Development of Sports LawDocument52 pagesSourav Bhuiyan Development of Sports LawLeo SouravNo ratings yet

- Patent Assignment Cover Sheet: Electronic Version v1 .1 Stylesheet Version v1 .2Document135 pagesPatent Assignment Cover Sheet: Electronic Version v1 .1 Stylesheet Version v1 .2Vivek SahNo ratings yet

- Criminal ProcedureDocument55 pagesCriminal ProcedureKhimber Claire Lala MaduyoNo ratings yet

- Chapter 5 - Ucadia Law Series: The Law Explained: Session 5 - Documents and SecuritiesDocument23 pagesChapter 5 - Ucadia Law Series: The Law Explained: Session 5 - Documents and SecuritiesMinisterNo ratings yet

- 114 Transport Iocl Jaipur Aug-2021Document2 pages114 Transport Iocl Jaipur Aug-2021vikram singh rooppuraNo ratings yet

- Wiring: Product Selection GuideDocument23 pagesWiring: Product Selection Guideharikollam1981No ratings yet

- Case No 197 - Writ of Kalikasan - Resident Marine Mammals V ReyesDocument3 pagesCase No 197 - Writ of Kalikasan - Resident Marine Mammals V ReyesKarenNo ratings yet

- Dolina Vs ValleceraDocument3 pagesDolina Vs ValleceraDario TorresNo ratings yet

- Austin Addison DocketDocument3 pagesAustin Addison DocketErin LaviolaNo ratings yet

- Volume 109, Issue 19Document20 pagesVolume 109, Issue 19The TechniqueNo ratings yet

- Numbers 0 To 9 Matching Exercise Worksheet Birthday ThemeDocument1 pageNumbers 0 To 9 Matching Exercise Worksheet Birthday Themegarbinxuli9325No ratings yet

- In Re - Cloyd GarraDocument2 pagesIn Re - Cloyd Garrafmrcsc2023No ratings yet

- Question Text: Correct Mark 1.00 Out of 1.00Document4 pagesQuestion Text: Correct Mark 1.00 Out of 1.00Christina KaukareNo ratings yet

- 152Document16 pages152Shri Kant CLCNo ratings yet

- Exam Admit CardDocument2 pagesExam Admit CardLaila MahbubaNo ratings yet

- RMC No. 15-2020 Annex ADocument3 pagesRMC No. 15-2020 Annex AKen Manacmul100% (1)

- Rice N Life Enterptise 1Document103 pagesRice N Life Enterptise 1Jasmin ZuluetaNo ratings yet

- Student Handbook AY2021-22 (26 Aug)Document28 pagesStudent Handbook AY2021-22 (26 Aug)Oscar RomainvilleNo ratings yet

- Abad-Gamo Legal Writing As A Study ToolDocument5 pagesAbad-Gamo Legal Writing As A Study ToolAlexis Louisse Gonzales100% (2)

Download as pdf or txt

You might also like

- The Champion Legal Ads: 05-25-23Document54 pagesThe Champion Legal Ads: 05-25-23Donna S. SeayNo ratings yet

- Allocations of Risk Capital in Financial InstitutionsDocument25 pagesAllocations of Risk Capital in Financial Institutionssrikanth_balasubra_1No ratings yet

- Financial Risk Management: A Simple IntroductionFrom EverandFinancial Risk Management: A Simple IntroductionRating: 4.5 out of 5 stars4.5/5 (7)

- BIOETHICSDocument243 pagesBIOETHICSJoebeth Competente100% (5)

- Two Type of Margins Have Been SpecifiedDocument8 pagesTwo Type of Margins Have Been SpecifiedPraveen KumarNo ratings yet

- Settlement, Clearing & Risk ManagementDocument34 pagesSettlement, Clearing & Risk ManagementTapas Chandra RoyNo ratings yet

- Equity Risk Management and SLBDocument12 pagesEquity Risk Management and SLBepakhil01No ratings yet

- Chapter 5 - Multifactor Value at RiskDocument44 pagesChapter 5 - Multifactor Value at RiskVishwajit GoudNo ratings yet

- Chapter 4 Securities Operations and Risk Management PDFDocument84 pagesChapter 4 Securities Operations and Risk Management PDFMRIDUL GOELNo ratings yet

- Lecture Note 1 2Document163 pagesLecture Note 1 2Đỗ Thủy Tiên NguyễnNo ratings yet

- Tmspan Margining043001Document18 pagesTmspan Margining043001kunal bandawarNo ratings yet

- Chapter #7: Value Ate Risk (VAR)Document30 pagesChapter #7: Value Ate Risk (VAR)Smart UnlockerNo ratings yet

- Bench MarkingDocument14 pagesBench MarkingVenkatakrishnan IyerNo ratings yet

- Corporate Treasury Needs A Solid BasisDocument2 pagesCorporate Treasury Needs A Solid BasisKofikoduahNo ratings yet

- Multinational Corporations and Global Financial Environment: Facilities in More Than One CountryDocument11 pagesMultinational Corporations and Global Financial Environment: Facilities in More Than One CountryANH NGUYEN DANG QUENo ratings yet

- Mercurial Lite Paper v1Document9 pagesMercurial Lite Paper v1ivan chenNo ratings yet

- FRM Unit-2Document31 pagesFRM Unit-2prasanthi CNo ratings yet

- Revised Chapter 9Document25 pagesRevised Chapter 9Shahadat HossainNo ratings yet

- 17 Use of The Var Method For Measuring Market Risks and Calculating Capital AdequacyDocument5 pages17 Use of The Var Method For Measuring Market Risks and Calculating Capital AdequacyYounus AkhoonNo ratings yet

- Risk Management of A Cashflow Driven InvestmentDocument30 pagesRisk Management of A Cashflow Driven InvestmentRichard ChiangNo ratings yet

- Provision For Adverse DeviationsDocument7 pagesProvision For Adverse DeviationsAgnes MercyanaaNo ratings yet

- Acca Afm (P4)Document36 pagesAcca Afm (P4)SamanMurtazaNo ratings yet

- Nse Clear Backtesting PolicyDocument3 pagesNse Clear Backtesting PolicyJoshuaNo ratings yet

- Equity Risk Management PolicyDocument4 pagesEquity Risk Management PolicymkjailaniNo ratings yet

- Risk Management: Value at Risk MarginDocument3 pagesRisk Management: Value at Risk MarginrachealllNo ratings yet

- Common Stock Valuation - Part 1Document35 pagesCommon Stock Valuation - Part 1Mahmoud HassaanNo ratings yet

- 1Document5 pages1mkc2044No ratings yet

- Interest Rate Swaps (Final)Document35 pagesInterest Rate Swaps (Final)Harish SharmaNo ratings yet

- A Systematic Approach To Optimizing CollateralDocument7 pagesA Systematic Approach To Optimizing CollateralCognizantNo ratings yet

- Bond Portfolio Management StrategiesDocument36 pagesBond Portfolio Management StrategiesMuhammad HarisNo ratings yet

- VaR FRMDocument11 pagesVaR FRMshashanksrivatsa008No ratings yet

- Value To Change Because of A Change in Exchange Rates: Mearsuring and Managing Exposure To Exchange Rate FluctuationsDocument2 pagesValue To Change Because of A Change in Exchange Rates: Mearsuring and Managing Exposure To Exchange Rate FluctuationsQuỳnh GiangNo ratings yet

- Practical Ifrs 09Document10 pagesPractical Ifrs 09Farooq HaiderNo ratings yet

- Basel 1 - IntroductionDocument16 pagesBasel 1 - IntroductiondarbyglaceNo ratings yet

- AD477Document8 pagesAD477Mert BirerNo ratings yet

- 3.3. Management of Equity Price RiskDocument2 pages3.3. Management of Equity Price RiskTaher BarwaniwalaNo ratings yet

- Final FX Risk & Exposure ManagementDocument33 pagesFinal FX Risk & Exposure ManagementkarunaksNo ratings yet

- Bank and Insurance Domande V2Document6 pagesBank and Insurance Domande V2f.invernici2No ratings yet

- Chapter 7Document39 pagesChapter 7Aimes AliNo ratings yet

- FIN010 - Efficient Capital MarketsDocument3 pagesFIN010 - Efficient Capital MarketsLanz Mark RelovaNo ratings yet

- Equiy SwapsDocument6 pagesEquiy SwapsPenny Lyn CapsuyenNo ratings yet

- Estimating Long Term GrowthDocument12 pagesEstimating Long Term GrowthsamacsterNo ratings yet

- Capital Market Line and The Efficient FrontierDocument6 pagesCapital Market Line and The Efficient FrontierPushpa BaruaNo ratings yet

- Cost Volume Profit AnalysisDocument20 pagesCost Volume Profit Analysisrikesh radheNo ratings yet

- Staff Working Paper No. 597: A Comparative Analysis of Tools To Limit The Procyclicality of Initial Margin RequirementsDocument24 pagesStaff Working Paper No. 597: A Comparative Analysis of Tools To Limit The Procyclicality of Initial Margin RequirementsTBP_Think_TankNo ratings yet

- Performance AttributionDocument7 pagesPerformance AttributionMilind ParaleNo ratings yet

- Clearing and SettlementDocument19 pagesClearing and SettlementRESHMA JAYAKUMARNo ratings yet

- BRM Session 12 Credit Risk & Credit Risk ModellingDocument33 pagesBRM Session 12 Credit Risk & Credit Risk ModellingSrinita MishraNo ratings yet

- How Clearing WorksDocument4 pagesHow Clearing WorksEdward TaufikNo ratings yet

- BRM Session 6 Value at RiskDocument39 pagesBRM Session 6 Value at RiskSrinita MishraNo ratings yet

- Individual Currency Limits: Value-at-RiskDocument4 pagesIndividual Currency Limits: Value-at-RiskBinod Singh JeenaNo ratings yet

- 9 Week of Lectures: Financial Management - MGT201Document13 pages9 Week of Lectures: Financial Management - MGT201Syed Abdul Mussaver ShahNo ratings yet

- Sapm ModelsDocument20 pagesSapm ModelsAvinash TripathiNo ratings yet

- 1.2 StructuredDocument42 pages1.2 StructuredMahmoud Moh'dNo ratings yet

- Risk Premia Strategies B 102727740Document29 pagesRisk Premia Strategies B 102727740h_jacobson100% (4)

- Chapter 4Document10 pagesChapter 4Seid KassawNo ratings yet

- R Eplicating P Ortfolios and R Is K Management: Presented by Joshua Corrigan, Charles QinDocument37 pagesR Eplicating P Ortfolios and R Is K Management: Presented by Joshua Corrigan, Charles QinPratik BhagatNo ratings yet

- Case 13Document12 pagesCase 13Superb AdnanNo ratings yet

- ALM End Term MergedDocument78 pagesALM End Term MergedShruti VermaNo ratings yet

- Port Finance: Interest Rate Market On SolanaDocument11 pagesPort Finance: Interest Rate Market On SolanaMI POCOPHONENo ratings yet

- Port Finance: Interest Rate Market On SolanaDocument11 pagesPort Finance: Interest Rate Market On Solanaxiao dreNo ratings yet

- El Papel, LLC v. City of Seattle, No. 22-35656 (9th Cir. Oct. 26, 2023) (Memo.)Document6 pagesEl Papel, LLC v. City of Seattle, No. 22-35656 (9th Cir. Oct. 26, 2023) (Memo.)RHTNo ratings yet

- Inter Se BiddingDocument7 pagesInter Se BiddingyamikaNo ratings yet

- Topic 2.demand Supply UpdatedDocument110 pagesTopic 2.demand Supply UpdatedNguyên TúNo ratings yet

- Bike2424 PDFDocument1 pageBike2424 PDFAntonijVedernikovNo ratings yet

- Exhibit 10Document10 pagesExhibit 10Steve JosephNo ratings yet

- Salcomp Corporate Governance Statement 2009 PDFDocument10 pagesSalcomp Corporate Governance Statement 2009 PDFRajsundarNo ratings yet

- PWDCertificateDocument1 pagePWDCertificateBipin PatilNo ratings yet

- Program Officer SOPsDocument3 pagesProgram Officer SOPsshaikhsamsaeed786No ratings yet

- CMP Mobilizers AccreditationDocument4 pagesCMP Mobilizers AccreditationJayson De LemonNo ratings yet

- Sourav Bhuiyan Development of Sports LawDocument52 pagesSourav Bhuiyan Development of Sports LawLeo SouravNo ratings yet

- Patent Assignment Cover Sheet: Electronic Version v1 .1 Stylesheet Version v1 .2Document135 pagesPatent Assignment Cover Sheet: Electronic Version v1 .1 Stylesheet Version v1 .2Vivek SahNo ratings yet

- Criminal ProcedureDocument55 pagesCriminal ProcedureKhimber Claire Lala MaduyoNo ratings yet

- Chapter 5 - Ucadia Law Series: The Law Explained: Session 5 - Documents and SecuritiesDocument23 pagesChapter 5 - Ucadia Law Series: The Law Explained: Session 5 - Documents and SecuritiesMinisterNo ratings yet

- 114 Transport Iocl Jaipur Aug-2021Document2 pages114 Transport Iocl Jaipur Aug-2021vikram singh rooppuraNo ratings yet

- Wiring: Product Selection GuideDocument23 pagesWiring: Product Selection Guideharikollam1981No ratings yet

- Case No 197 - Writ of Kalikasan - Resident Marine Mammals V ReyesDocument3 pagesCase No 197 - Writ of Kalikasan - Resident Marine Mammals V ReyesKarenNo ratings yet

- Dolina Vs ValleceraDocument3 pagesDolina Vs ValleceraDario TorresNo ratings yet

- Austin Addison DocketDocument3 pagesAustin Addison DocketErin LaviolaNo ratings yet

- Volume 109, Issue 19Document20 pagesVolume 109, Issue 19The TechniqueNo ratings yet

- Numbers 0 To 9 Matching Exercise Worksheet Birthday ThemeDocument1 pageNumbers 0 To 9 Matching Exercise Worksheet Birthday Themegarbinxuli9325No ratings yet

- In Re - Cloyd GarraDocument2 pagesIn Re - Cloyd Garrafmrcsc2023No ratings yet

- Question Text: Correct Mark 1.00 Out of 1.00Document4 pagesQuestion Text: Correct Mark 1.00 Out of 1.00Christina KaukareNo ratings yet

- 152Document16 pages152Shri Kant CLCNo ratings yet

- Exam Admit CardDocument2 pagesExam Admit CardLaila MahbubaNo ratings yet

- RMC No. 15-2020 Annex ADocument3 pagesRMC No. 15-2020 Annex AKen Manacmul100% (1)

- Rice N Life Enterptise 1Document103 pagesRice N Life Enterptise 1Jasmin ZuluetaNo ratings yet

- Student Handbook AY2021-22 (26 Aug)Document28 pagesStudent Handbook AY2021-22 (26 Aug)Oscar RomainvilleNo ratings yet

- Abad-Gamo Legal Writing As A Study ToolDocument5 pagesAbad-Gamo Legal Writing As A Study ToolAlexis Louisse Gonzales100% (2)