PGBP ALL Adjustments - CA Amit Mahajan (1)

PGBP ALL Adjustments - CA Amit Mahajan (1)

You might also like

- Bank Guarantee Swift Mt760 Sample 2Document1 pageBank Guarantee Swift Mt760 Sample 2Божидар Денев100% (1)

- 2015UniformEvaluation PaperIII PDFDocument26 pages2015UniformEvaluation PaperIII PDFAdayyat M.No ratings yet

- Sapp - KPMG Entrance Test Answer PDFDocument11 pagesSapp - KPMG Entrance Test Answer PDFTran Pham Quoc ThuyNo ratings yet

- Activity Final Tax On Passive IncomeDocument7 pagesActivity Final Tax On Passive IncomeElla Marie Lopez100% (2)

- P6MYS 2012 Dec ADocument15 pagesP6MYS 2012 Dec AFakhrul Azman NawiNo ratings yet

- Net Business IncomeDocument21 pagesNet Business IncomedonawajNo ratings yet

- LU5 WorkbookDocument16 pagesLU5 Workbookprowess222No ratings yet

- Profit and Gains of Business or Profession (PGBP) : Dr. Sonam Topgay BhutiaDocument8 pagesProfit and Gains of Business or Profession (PGBP) : Dr. Sonam Topgay BhutiaUmesh SharmaNo ratings yet

- Screenshot 2023-03-28 at 9.42.11 AMDocument38 pagesScreenshot 2023-03-28 at 9.42.11 AMKinza NawazNo ratings yet

- CFAP 5 Winter 2021Document7 pagesCFAP 5 Winter 2021Faltu BatNo ratings yet

- TAXATION: Improperly Accumulated Earnings Tax (IAET) 2020 Improperly Accumulated Earnings Tax (IAET)Document7 pagesTAXATION: Improperly Accumulated Earnings Tax (IAET) 2020 Improperly Accumulated Earnings Tax (IAET)YashNo ratings yet

- Aggregation of Income, Set Off or Carry Forward of Losses: After Studying This Chapter, You Would Be Able ToDocument31 pagesAggregation of Income, Set Off or Carry Forward of Losses: After Studying This Chapter, You Would Be Able ToSivasankariNo ratings yet

- Corporate Tax Planning & Management Mid Term Assessment-1 Maximum Marks: 20 Duration: 9:30 AM-11:00 AMDocument3 pagesCorporate Tax Planning & Management Mid Term Assessment-1 Maximum Marks: 20 Duration: 9:30 AM-11:00 AMChirag JainNo ratings yet

- Solved Past Papers Income Tax Numericals of ICMAP STAGE IV - (2003 TO 2015)Document45 pagesSolved Past Papers Income Tax Numericals of ICMAP STAGE IV - (2003 TO 2015)muneeb razaNo ratings yet

- Mr. Zulfiqar Computation of Taxable Income For Tax Year 2009 RupeesDocument5 pagesMr. Zulfiqar Computation of Taxable Income For Tax Year 2009 Rupeesmeelas123No ratings yet

- IcaiDocument12 pagesIcaibasanisujithNo ratings yet

- Txmwi 2019 Jun ADocument9 pagesTxmwi 2019 Jun AangaNo ratings yet

- Chapter 11Document42 pagesChapter 11Bashu GuragainNo ratings yet

- Add: Depreciation As Per Books: © The Institute of Chartered Accountants of IndiaDocument15 pagesAdd: Depreciation As Per Books: © The Institute of Chartered Accountants of IndiaShubham KumarNo ratings yet

- IPCC Mock Test Taxation - Only Solution - 25.09.2018Document12 pagesIPCC Mock Test Taxation - Only Solution - 25.09.2018KaustubhNo ratings yet

- Advanced Taxation: Page 1 of 8Document8 pagesAdvanced Taxation: Page 1 of 8Muhammad Usama SheikhNo ratings yet

- 1 Accounting For Taxation: Section OverviewDocument36 pages1 Accounting For Taxation: Section Overviewsimran jeswaniNo ratings yet

- Provident FundDocument9 pagesProvident Fundmohammed umairNo ratings yet

- 30 - 09 - Final AccountsDocument40 pages30 - 09 - Final Accountssachin lanjewarNo ratings yet

- Examiner Comments-Summer 2017Document12 pagesExaminer Comments-Summer 2017Mahendar BhojwaniNo ratings yet

- Amount To Be Included in Income (Sec. 9) : Particulars: Inclusion Reason To Include or Not IncludeDocument2 pagesAmount To Be Included in Income (Sec. 9) : Particulars: Inclusion Reason To Include or Not IncludeBashu GuragainNo ratings yet

- HW 20 June 2020 Name: Mohamad Fidri Bin Shamsudin Class: Atx-C Lecturer: Ms NabilahDocument12 pagesHW 20 June 2020 Name: Mohamad Fidri Bin Shamsudin Class: Atx-C Lecturer: Ms NabilahPutera IzwanNo ratings yet

- Paper - 4: Taxation Section A: Income TaxDocument24 pagesPaper - 4: Taxation Section A: Income TaxChhaya JajuNo ratings yet

- Session 8 - Final Accounts - Practice ProblemsDocument16 pagesSession 8 - Final Accounts - Practice ProblemsanandakumarNo ratings yet

- Solved Question Paper For November 2018 EXAM (New Syllabus)Document21 pagesSolved Question Paper For November 2018 EXAM (New Syllabus)Ravi PrakashNo ratings yet

- Chapter 2 Capsule SessionDocument40 pagesChapter 2 Capsule SessionKshitishNo ratings yet

- IT II AnswerDocument4 pagesIT II AnswerChandhini RNo ratings yet

- Tax SuggestedDocument28 pagesTax SuggestedHemaNo ratings yet

- TAX 06 - RIT Gross IncomeDocument3 pagesTAX 06 - RIT Gross IncomeEdith DalidaNo ratings yet

- CAF 06 - TaxationDocument7 pagesCAF 06 - TaxationKhurram ShahzadNo ratings yet

- Applied Taxation ACCT 370: Rabia SaleemDocument23 pagesApplied Taxation ACCT 370: Rabia Saleemsultan siddiquiNo ratings yet

- The Accounting Cycle: Reporting Financial ResultsDocument8 pagesThe Accounting Cycle: Reporting Financial ResultsOmar KhanNo ratings yet

- Indirect MethodDocument34 pagesIndirect MethodHacker SKNo ratings yet

- Paper 4 Studycafe - inDocument28 pagesPaper 4 Studycafe - inApeksha ChilwalNo ratings yet

- DT Nov 2022 PaperDocument26 pagesDT Nov 2022 PaperPoonam Sunil Lalwani LalwaniNo ratings yet

- Aggregation of IncomeDocument30 pagesAggregation of Incomeraja naiduNo ratings yet

- Ryan RemsDocument56 pagesRyan Remsmimi supasNo ratings yet

- Suggested Nov 2019Document23 pagesSuggested Nov 2019just Konkan thingsNo ratings yet

- Exam Practice ReviewDocument9 pagesExam Practice ReviewSafi NurulNo ratings yet

- Wa0039.Document14 pagesWa0039.abdulraqeeb alareqiNo ratings yet

- Fund Flow StatementDocument21 pagesFund Flow StatementPGNo ratings yet

- Session 8 - Gross Income - Inclusions and ExclusionsDocument12 pagesSession 8 - Gross Income - Inclusions and ExclusionsMitzi WamarNo ratings yet

- Notes - ACCTG 114 - 04 26 - 04 28 2022Document13 pagesNotes - ACCTG 114 - 04 26 - 04 28 2022Janna Mari FriasNo ratings yet

- (I) (B) (Ii) (D) (Iii) (D) (Iv) (C) (V) (A) (Vi) (C) (Vii) (A) (Viii) (D) (Ix) (C) (X) (C)Document8 pages(I) (B) (Ii) (D) (Iii) (D) (Iv) (C) (V) (A) (Vi) (C) (Vii) (A) (Viii) (D) (Ix) (C) (X) (C)santosh palNo ratings yet

- Equipment Shall Be ExcludedDocument2 pagesEquipment Shall Be ExcludedKatherine MagpantayNo ratings yet

- Profits Tax Computation Illustration 2023S - Suggested Answers Ver2Document2 pagesProfits Tax Computation Illustration 2023S - Suggested Answers Ver2何健珩No ratings yet

- PDF Document E64dfec87bb0 1Document75 pagesPDF Document E64dfec87bb0 120BRM051 Sukant SNo ratings yet

- 8.special Tax Rates of Companies & MATDocument22 pages8.special Tax Rates of Companies & MATMuthu nayagamNo ratings yet

- Suggested Jan 2021Document25 pagesSuggested Jan 2021just Konkan thingsNo ratings yet

- Aggregation of Income, Set-Off and Carry Forward of LossesDocument18 pagesAggregation of Income, Set-Off and Carry Forward of LossesJoseph SalidoNo ratings yet

- Direct IndirectTaxesinIndia October2019 B B A WithCredits RegularJune-2017PatternSecondYearB B A E31C0FB4Document3 pagesDirect IndirectTaxesinIndia October2019 B B A WithCredits RegularJune-2017PatternSecondYearB B A E31C0FB4Mubin Shaikh NooruNo ratings yet

- Learning Unit 8 - Treatments of Dividends During ConsolidationDocument41 pagesLearning Unit 8 - Treatments of Dividends During ConsolidationThulani NdlovuNo ratings yet

- Dividend Received From A Domestic CompanyDocument9 pagesDividend Received From A Domestic Companyshiraz shabbirNo ratings yet

- Financial Management MidtermDocument4 pagesFinancial Management MidtermGrace Sinoy BastanteNo ratings yet

- Tax Dec 21 SugesstedDocument27 pagesTax Dec 21 SugesstedShailjaNo ratings yet

- Accounting Chapter 2Document19 pagesAccounting Chapter 2MUHAMMAD ZULHAIRI BIN ROSLI STUDENTNo ratings yet

- Learning Unit 9 Treatment of Preference Shares During ConsolidationDocument57 pagesLearning Unit 9 Treatment of Preference Shares During ConsolidationThulani NdlovuNo ratings yet

- Additional Questions On Financial Statements and Cash BookDocument5 pagesAdditional Questions On Financial Statements and Cash BookBoi NonoNo ratings yet

- FM_Formula_Chart_One_Page @CAInterLegendsDocument5 pagesFM_Formula_Chart_One_Page @CAInterLegendsParth SarafNo ratings yet

- Dividend Day 2Document14 pagesDividend Day 2Parth SarafNo ratings yet

- The Indian Contract Act, 1872Document64 pagesThe Indian Contract Act, 1872Parth SarafNo ratings yet

- FVFDDocument20 pagesFVFDParth SarafNo ratings yet

- FederalDocument15 pagesFederalNeil NitinNo ratings yet

- Tax AnswersDocument168 pagesTax AnswersukqrnnnjhfwsxqoykuNo ratings yet

- IT QuestionDocument3 pagesIT QuestionSathish SmartNo ratings yet

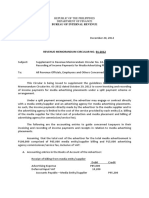

- Revenue Memorandum Circular No. 91-2012: Bureau of Internal RevenueDocument3 pagesRevenue Memorandum Circular No. 91-2012: Bureau of Internal RevenueHenson MontalvoNo ratings yet

- 12 Format of Mis For MFG ConcernDocument5 pages12 Format of Mis For MFG ConcernRaj Kothari MNo ratings yet

- xoIPV9pH45 PDFDocument1 pagexoIPV9pH45 PDFhalloarnabNo ratings yet

- Tax Invoice: Invoice Details Client DetailsDocument2 pagesTax Invoice: Invoice Details Client DetailsARUN M GOHILNo ratings yet

- WINRO154 BudgetLetterRequest - Semi MonthlyCashAssistanceBudgetCalculation - SNAPBudgetCalculationForCA&CA SSICases 585277954Document6 pagesWINRO154 BudgetLetterRequest - Semi MonthlyCashAssistanceBudgetCalculation - SNAPBudgetCalculationForCA&CA SSICases 585277954schwartzdaven7No ratings yet

- Table of Creditable Withholding Tax RatesDocument4 pagesTable of Creditable Withholding Tax RatesZandra Mari Dela PenaNo ratings yet

- Intacc All Mar 19Document4 pagesIntacc All Mar 19Mila MercadoNo ratings yet

- Chapter 3 - Seat Work - Assignment #3 - ACCOUNTING FOR GOVERNMENT AND NON - PROFIT ORGANIZATIONSDocument5 pagesChapter 3 - Seat Work - Assignment #3 - ACCOUNTING FOR GOVERNMENT AND NON - PROFIT ORGANIZATIONSDonise Ronadel SantosNo ratings yet

- The Finnerty Furniture Company A Manufacturer and Wholesaler of High QualityDocument2 pagesThe Finnerty Furniture Company A Manufacturer and Wholesaler of High QualityAmit PandeyNo ratings yet

- TCT Title Transfer and Annotation Steps: 1. Prepare The Documents: by This Time in Your Buying-A-PropertyDocument5 pagesTCT Title Transfer and Annotation Steps: 1. Prepare The Documents: by This Time in Your Buying-A-PropertysejinmaNo ratings yet

- The SolopreneurDocument6 pagesThe Solopreneurjun junNo ratings yet

- 2008 Form 990 Carpenter Charity FundDocument30 pages2008 Form 990 Carpenter Charity FundLatisha WalkerNo ratings yet

- Topic 7 Capital Structure & Dividend ImputationDocument53 pagesTopic 7 Capital Structure & Dividend Imputationsir bookkeeperNo ratings yet

- Outward Supply Replated - GST Audit 9C by CA Venugopal Gella - Ver1.0Document34 pagesOutward Supply Replated - GST Audit 9C by CA Venugopal Gella - Ver1.0Kishan M Mehta CoNo ratings yet

- Opening A Company in BangladeshDocument4 pagesOpening A Company in BangladeshSuhel Md RezaNo ratings yet

- Acca f6 2020 Lecture NotesDocument209 pagesAcca f6 2020 Lecture NotesMili sarkar0% (1)

- E Receipt - Cons 0614373464Document1 pageE Receipt - Cons 0614373464yaswanthkapoorNo ratings yet

- Amendments To IFRS 2 'Share-Based Payment'Document1 pageAmendments To IFRS 2 'Share-Based Payment'Rizshelle D. AlarconNo ratings yet

- Return: Return What Is GST ReturnDocument3 pagesReturn: Return What Is GST ReturnNagarjuna ReddyNo ratings yet

- FORM 210: For Tax Payment Through Treasury / BankDocument3 pagesFORM 210: For Tax Payment Through Treasury / BankVaibhavJoreNo ratings yet

- BSBMGT605B - Assessment Task 2Document7 pagesBSBMGT605B - Assessment Task 2Ghie MoralesNo ratings yet

- 5 Ibtx: Business TaxationDocument13 pages5 Ibtx: Business Taxationmonalisha mishraNo ratings yet

- I PSF 202122Document16 pagesI PSF 202122Preethi PachipulusuNo ratings yet

Download as pdf or txt

You might also like

- Bank Guarantee Swift Mt760 Sample 2Document1 pageBank Guarantee Swift Mt760 Sample 2Божидар Денев100% (1)

- 2015UniformEvaluation PaperIII PDFDocument26 pages2015UniformEvaluation PaperIII PDFAdayyat M.No ratings yet

- Sapp - KPMG Entrance Test Answer PDFDocument11 pagesSapp - KPMG Entrance Test Answer PDFTran Pham Quoc ThuyNo ratings yet

- Activity Final Tax On Passive IncomeDocument7 pagesActivity Final Tax On Passive IncomeElla Marie Lopez100% (2)

- P6MYS 2012 Dec ADocument15 pagesP6MYS 2012 Dec AFakhrul Azman NawiNo ratings yet

- Net Business IncomeDocument21 pagesNet Business IncomedonawajNo ratings yet

- LU5 WorkbookDocument16 pagesLU5 Workbookprowess222No ratings yet

- Profit and Gains of Business or Profession (PGBP) : Dr. Sonam Topgay BhutiaDocument8 pagesProfit and Gains of Business or Profession (PGBP) : Dr. Sonam Topgay BhutiaUmesh SharmaNo ratings yet

- Screenshot 2023-03-28 at 9.42.11 AMDocument38 pagesScreenshot 2023-03-28 at 9.42.11 AMKinza NawazNo ratings yet

- CFAP 5 Winter 2021Document7 pagesCFAP 5 Winter 2021Faltu BatNo ratings yet

- TAXATION: Improperly Accumulated Earnings Tax (IAET) 2020 Improperly Accumulated Earnings Tax (IAET)Document7 pagesTAXATION: Improperly Accumulated Earnings Tax (IAET) 2020 Improperly Accumulated Earnings Tax (IAET)YashNo ratings yet

- Aggregation of Income, Set Off or Carry Forward of Losses: After Studying This Chapter, You Would Be Able ToDocument31 pagesAggregation of Income, Set Off or Carry Forward of Losses: After Studying This Chapter, You Would Be Able ToSivasankariNo ratings yet

- Corporate Tax Planning & Management Mid Term Assessment-1 Maximum Marks: 20 Duration: 9:30 AM-11:00 AMDocument3 pagesCorporate Tax Planning & Management Mid Term Assessment-1 Maximum Marks: 20 Duration: 9:30 AM-11:00 AMChirag JainNo ratings yet

- Solved Past Papers Income Tax Numericals of ICMAP STAGE IV - (2003 TO 2015)Document45 pagesSolved Past Papers Income Tax Numericals of ICMAP STAGE IV - (2003 TO 2015)muneeb razaNo ratings yet

- Mr. Zulfiqar Computation of Taxable Income For Tax Year 2009 RupeesDocument5 pagesMr. Zulfiqar Computation of Taxable Income For Tax Year 2009 Rupeesmeelas123No ratings yet

- IcaiDocument12 pagesIcaibasanisujithNo ratings yet

- Txmwi 2019 Jun ADocument9 pagesTxmwi 2019 Jun AangaNo ratings yet

- Chapter 11Document42 pagesChapter 11Bashu GuragainNo ratings yet

- Add: Depreciation As Per Books: © The Institute of Chartered Accountants of IndiaDocument15 pagesAdd: Depreciation As Per Books: © The Institute of Chartered Accountants of IndiaShubham KumarNo ratings yet

- IPCC Mock Test Taxation - Only Solution - 25.09.2018Document12 pagesIPCC Mock Test Taxation - Only Solution - 25.09.2018KaustubhNo ratings yet

- Advanced Taxation: Page 1 of 8Document8 pagesAdvanced Taxation: Page 1 of 8Muhammad Usama SheikhNo ratings yet

- 1 Accounting For Taxation: Section OverviewDocument36 pages1 Accounting For Taxation: Section Overviewsimran jeswaniNo ratings yet

- Provident FundDocument9 pagesProvident Fundmohammed umairNo ratings yet

- 30 - 09 - Final AccountsDocument40 pages30 - 09 - Final Accountssachin lanjewarNo ratings yet

- Examiner Comments-Summer 2017Document12 pagesExaminer Comments-Summer 2017Mahendar BhojwaniNo ratings yet

- Amount To Be Included in Income (Sec. 9) : Particulars: Inclusion Reason To Include or Not IncludeDocument2 pagesAmount To Be Included in Income (Sec. 9) : Particulars: Inclusion Reason To Include or Not IncludeBashu GuragainNo ratings yet

- HW 20 June 2020 Name: Mohamad Fidri Bin Shamsudin Class: Atx-C Lecturer: Ms NabilahDocument12 pagesHW 20 June 2020 Name: Mohamad Fidri Bin Shamsudin Class: Atx-C Lecturer: Ms NabilahPutera IzwanNo ratings yet

- Paper - 4: Taxation Section A: Income TaxDocument24 pagesPaper - 4: Taxation Section A: Income TaxChhaya JajuNo ratings yet

- Session 8 - Final Accounts - Practice ProblemsDocument16 pagesSession 8 - Final Accounts - Practice ProblemsanandakumarNo ratings yet

- Solved Question Paper For November 2018 EXAM (New Syllabus)Document21 pagesSolved Question Paper For November 2018 EXAM (New Syllabus)Ravi PrakashNo ratings yet

- Chapter 2 Capsule SessionDocument40 pagesChapter 2 Capsule SessionKshitishNo ratings yet

- IT II AnswerDocument4 pagesIT II AnswerChandhini RNo ratings yet

- Tax SuggestedDocument28 pagesTax SuggestedHemaNo ratings yet

- TAX 06 - RIT Gross IncomeDocument3 pagesTAX 06 - RIT Gross IncomeEdith DalidaNo ratings yet

- CAF 06 - TaxationDocument7 pagesCAF 06 - TaxationKhurram ShahzadNo ratings yet

- Applied Taxation ACCT 370: Rabia SaleemDocument23 pagesApplied Taxation ACCT 370: Rabia Saleemsultan siddiquiNo ratings yet

- The Accounting Cycle: Reporting Financial ResultsDocument8 pagesThe Accounting Cycle: Reporting Financial ResultsOmar KhanNo ratings yet

- Indirect MethodDocument34 pagesIndirect MethodHacker SKNo ratings yet

- Paper 4 Studycafe - inDocument28 pagesPaper 4 Studycafe - inApeksha ChilwalNo ratings yet

- DT Nov 2022 PaperDocument26 pagesDT Nov 2022 PaperPoonam Sunil Lalwani LalwaniNo ratings yet

- Aggregation of IncomeDocument30 pagesAggregation of Incomeraja naiduNo ratings yet

- Ryan RemsDocument56 pagesRyan Remsmimi supasNo ratings yet

- Suggested Nov 2019Document23 pagesSuggested Nov 2019just Konkan thingsNo ratings yet

- Exam Practice ReviewDocument9 pagesExam Practice ReviewSafi NurulNo ratings yet

- Wa0039.Document14 pagesWa0039.abdulraqeeb alareqiNo ratings yet

- Fund Flow StatementDocument21 pagesFund Flow StatementPGNo ratings yet

- Session 8 - Gross Income - Inclusions and ExclusionsDocument12 pagesSession 8 - Gross Income - Inclusions and ExclusionsMitzi WamarNo ratings yet

- Notes - ACCTG 114 - 04 26 - 04 28 2022Document13 pagesNotes - ACCTG 114 - 04 26 - 04 28 2022Janna Mari FriasNo ratings yet

- (I) (B) (Ii) (D) (Iii) (D) (Iv) (C) (V) (A) (Vi) (C) (Vii) (A) (Viii) (D) (Ix) (C) (X) (C)Document8 pages(I) (B) (Ii) (D) (Iii) (D) (Iv) (C) (V) (A) (Vi) (C) (Vii) (A) (Viii) (D) (Ix) (C) (X) (C)santosh palNo ratings yet

- Equipment Shall Be ExcludedDocument2 pagesEquipment Shall Be ExcludedKatherine MagpantayNo ratings yet

- Profits Tax Computation Illustration 2023S - Suggested Answers Ver2Document2 pagesProfits Tax Computation Illustration 2023S - Suggested Answers Ver2何健珩No ratings yet

- PDF Document E64dfec87bb0 1Document75 pagesPDF Document E64dfec87bb0 120BRM051 Sukant SNo ratings yet

- 8.special Tax Rates of Companies & MATDocument22 pages8.special Tax Rates of Companies & MATMuthu nayagamNo ratings yet

- Suggested Jan 2021Document25 pagesSuggested Jan 2021just Konkan thingsNo ratings yet

- Aggregation of Income, Set-Off and Carry Forward of LossesDocument18 pagesAggregation of Income, Set-Off and Carry Forward of LossesJoseph SalidoNo ratings yet

- Direct IndirectTaxesinIndia October2019 B B A WithCredits RegularJune-2017PatternSecondYearB B A E31C0FB4Document3 pagesDirect IndirectTaxesinIndia October2019 B B A WithCredits RegularJune-2017PatternSecondYearB B A E31C0FB4Mubin Shaikh NooruNo ratings yet

- Learning Unit 8 - Treatments of Dividends During ConsolidationDocument41 pagesLearning Unit 8 - Treatments of Dividends During ConsolidationThulani NdlovuNo ratings yet

- Dividend Received From A Domestic CompanyDocument9 pagesDividend Received From A Domestic Companyshiraz shabbirNo ratings yet

- Financial Management MidtermDocument4 pagesFinancial Management MidtermGrace Sinoy BastanteNo ratings yet

- Tax Dec 21 SugesstedDocument27 pagesTax Dec 21 SugesstedShailjaNo ratings yet

- Accounting Chapter 2Document19 pagesAccounting Chapter 2MUHAMMAD ZULHAIRI BIN ROSLI STUDENTNo ratings yet

- Learning Unit 9 Treatment of Preference Shares During ConsolidationDocument57 pagesLearning Unit 9 Treatment of Preference Shares During ConsolidationThulani NdlovuNo ratings yet

- Additional Questions On Financial Statements and Cash BookDocument5 pagesAdditional Questions On Financial Statements and Cash BookBoi NonoNo ratings yet

- FM_Formula_Chart_One_Page @CAInterLegendsDocument5 pagesFM_Formula_Chart_One_Page @CAInterLegendsParth SarafNo ratings yet

- Dividend Day 2Document14 pagesDividend Day 2Parth SarafNo ratings yet

- The Indian Contract Act, 1872Document64 pagesThe Indian Contract Act, 1872Parth SarafNo ratings yet

- FVFDDocument20 pagesFVFDParth SarafNo ratings yet

- FederalDocument15 pagesFederalNeil NitinNo ratings yet

- Tax AnswersDocument168 pagesTax AnswersukqrnnnjhfwsxqoykuNo ratings yet

- IT QuestionDocument3 pagesIT QuestionSathish SmartNo ratings yet

- Revenue Memorandum Circular No. 91-2012: Bureau of Internal RevenueDocument3 pagesRevenue Memorandum Circular No. 91-2012: Bureau of Internal RevenueHenson MontalvoNo ratings yet

- 12 Format of Mis For MFG ConcernDocument5 pages12 Format of Mis For MFG ConcernRaj Kothari MNo ratings yet

- xoIPV9pH45 PDFDocument1 pagexoIPV9pH45 PDFhalloarnabNo ratings yet

- Tax Invoice: Invoice Details Client DetailsDocument2 pagesTax Invoice: Invoice Details Client DetailsARUN M GOHILNo ratings yet

- WINRO154 BudgetLetterRequest - Semi MonthlyCashAssistanceBudgetCalculation - SNAPBudgetCalculationForCA&CA SSICases 585277954Document6 pagesWINRO154 BudgetLetterRequest - Semi MonthlyCashAssistanceBudgetCalculation - SNAPBudgetCalculationForCA&CA SSICases 585277954schwartzdaven7No ratings yet

- Table of Creditable Withholding Tax RatesDocument4 pagesTable of Creditable Withholding Tax RatesZandra Mari Dela PenaNo ratings yet

- Intacc All Mar 19Document4 pagesIntacc All Mar 19Mila MercadoNo ratings yet

- Chapter 3 - Seat Work - Assignment #3 - ACCOUNTING FOR GOVERNMENT AND NON - PROFIT ORGANIZATIONSDocument5 pagesChapter 3 - Seat Work - Assignment #3 - ACCOUNTING FOR GOVERNMENT AND NON - PROFIT ORGANIZATIONSDonise Ronadel SantosNo ratings yet

- The Finnerty Furniture Company A Manufacturer and Wholesaler of High QualityDocument2 pagesThe Finnerty Furniture Company A Manufacturer and Wholesaler of High QualityAmit PandeyNo ratings yet

- TCT Title Transfer and Annotation Steps: 1. Prepare The Documents: by This Time in Your Buying-A-PropertyDocument5 pagesTCT Title Transfer and Annotation Steps: 1. Prepare The Documents: by This Time in Your Buying-A-PropertysejinmaNo ratings yet

- The SolopreneurDocument6 pagesThe Solopreneurjun junNo ratings yet

- 2008 Form 990 Carpenter Charity FundDocument30 pages2008 Form 990 Carpenter Charity FundLatisha WalkerNo ratings yet

- Topic 7 Capital Structure & Dividend ImputationDocument53 pagesTopic 7 Capital Structure & Dividend Imputationsir bookkeeperNo ratings yet

- Outward Supply Replated - GST Audit 9C by CA Venugopal Gella - Ver1.0Document34 pagesOutward Supply Replated - GST Audit 9C by CA Venugopal Gella - Ver1.0Kishan M Mehta CoNo ratings yet

- Opening A Company in BangladeshDocument4 pagesOpening A Company in BangladeshSuhel Md RezaNo ratings yet

- Acca f6 2020 Lecture NotesDocument209 pagesAcca f6 2020 Lecture NotesMili sarkar0% (1)

- E Receipt - Cons 0614373464Document1 pageE Receipt - Cons 0614373464yaswanthkapoorNo ratings yet

- Amendments To IFRS 2 'Share-Based Payment'Document1 pageAmendments To IFRS 2 'Share-Based Payment'Rizshelle D. AlarconNo ratings yet

- Return: Return What Is GST ReturnDocument3 pagesReturn: Return What Is GST ReturnNagarjuna ReddyNo ratings yet

- FORM 210: For Tax Payment Through Treasury / BankDocument3 pagesFORM 210: For Tax Payment Through Treasury / BankVaibhavJoreNo ratings yet

- BSBMGT605B - Assessment Task 2Document7 pagesBSBMGT605B - Assessment Task 2Ghie MoralesNo ratings yet

- 5 Ibtx: Business TaxationDocument13 pages5 Ibtx: Business Taxationmonalisha mishraNo ratings yet

- I PSF 202122Document16 pagesI PSF 202122Preethi PachipulusuNo ratings yet