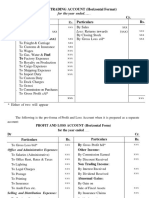

FINANCIAL STATEMENTS

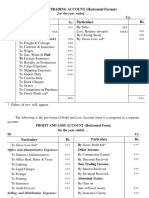

FINANCIAL STATEMENTS

You might also like

- Format Sopl and SofpDocument3 pagesFormat Sopl and SofpMuhammad Faaiz IzzeawanNo ratings yet

- CPA Review Notes 2019 - FAR (Financial Accounting and Reporting)From EverandCPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Rating: 3.5 out of 5 stars3.5/5 (17)

- Cattle Fattening FinancialsDocument5 pagesCattle Fattening Financialsprince kupaNo ratings yet

- Sime Darby BerhadDocument16 pagesSime Darby Berhadjue -No ratings yet

- Jiranna Financials 22Document20 pagesJiranna Financials 22Ellen MarkNo ratings yet

- Preparation of Financial Statement For A Sole TraderDocument8 pagesPreparation of Financial Statement For A Sole TraderDebbie Debz100% (3)

- Tutorial 7 Trade Receivables (Q)Document3 pagesTutorial 7 Trade Receivables (Q)lious liiNo ratings yet

- Chapter 2 Statement of Income and Statement of Owner's Equity PDFDocument8 pagesChapter 2 Statement of Income and Statement of Owner's Equity PDFNathaniel LacamentoNo ratings yet

- Company Final AccountsDocument13 pagesCompany Final Accountsshanthala mNo ratings yet

- Lesson 3c The Statement of Comprehensive Income - Merchandising BusinessDocument11 pagesLesson 3c The Statement of Comprehensive Income - Merchandising BusinessBenedict CladoNo ratings yet

- Format SoplDocument2 pagesFormat Soplhumairayazid12No ratings yet

- Income StatementDocument1 pageIncome StatementTanakha MaziwisaNo ratings yet

- Financial Statements of Sole Trader (Unit-04) PDFDocument3 pagesFinancial Statements of Sole Trader (Unit-04) PDFImadNo ratings yet

- Accounts Chapter 8Document10 pagesAccounts Chapter 8R.mNo ratings yet

- Chapter 7Document15 pagesChapter 7msukri_81No ratings yet

- Income Statement Format-MerchandisingDocument1 pageIncome Statement Format-MerchandisingSiam FarhanNo ratings yet

- The Income StatementDocument18 pagesThe Income Statementmudiwachokuda1234567No ratings yet

- Notes of Financial Statements or Final AccountsDocument11 pagesNotes of Financial Statements or Final Accountsrxcha.josephNo ratings yet

- Guidelines Re Selling and Admi Expenses - 2014Document2 pagesGuidelines Re Selling and Admi Expenses - 2014HaideBrocalesNo ratings yet

- Chap-7, 8 & 9 (Income Statemnet & Statement of Financial Position)Document17 pagesChap-7, 8 & 9 (Income Statemnet & Statement of Financial Position)7a4374 hisNo ratings yet

- Unit 02 Preparation of Financial Statement As Per IND AS 01Document13 pagesUnit 02 Preparation of Financial Statement As Per IND AS 01Deepak LNo ratings yet

- 10532lectuer 5 FADocument28 pages10532lectuer 5 FANajia SalmanNo ratings yet

- Xyz Company Income Statement FOR THE YEAR ENDEDDocument1 pageXyz Company Income Statement FOR THE YEAR ENDEDDaniyal AhmadNo ratings yet

- Chap-7, 8 & 9 (Income Statemnet & Statement of Financial Position)Document18 pagesChap-7, 8 & 9 (Income Statemnet & Statement of Financial Position)7a4374 hisNo ratings yet

- Merchandising OperationsDocument33 pagesMerchandising OperationsDanica MedinaNo ratings yet

- Final AccountDocument2 pagesFinal Accountmeelas123No ratings yet

- Actg101 Fs Prepa TemplateDocument16 pagesActg101 Fs Prepa TemplateJaira ClavoNo ratings yet

- Tally Trading and Profit Loss Acc Balance SheetDocument14 pagesTally Trading and Profit Loss Acc Balance Sheetsuresh kumar10No ratings yet

- POA FormatsDocument7 pagesPOA FormatsWilliNo ratings yet

- Income StatementDocument4 pagesIncome StatementBurhan AzharNo ratings yet

- Fundamentals of Accounting and Business ManagementDocument4 pagesFundamentals of Accounting and Business ManagementSan Juan Ezthie100% (1)

- Final - Accounts Format 234 PDFDocument13 pagesFinal - Accounts Format 234 PDFajaychattaNo ratings yet

- Final - Accounts Format PDFDocument13 pagesFinal - Accounts Format PDFajaychatta100% (1)

- AAAAADocument2 pagesAAAAAIrish CastilloNo ratings yet

- Is SofpDocument2 pagesIs SofpHilwa FarhanNo ratings yet

- Income Statement FormatDocument2 pagesIncome Statement FormatShruti MohanNo ratings yet

- Manufacturing AccountDocument2 pagesManufacturing Accountmeelas123100% (2)

- Departmental TradingDocument1 pageDepartmental Tradingmeelas123No ratings yet

- Accounting FormatsDocument21 pagesAccounting FormatsAsima ZubairNo ratings yet

- Unit - Iii Final Account: I.e., All Manufacturing Expenses, Carriage, Cartage, Freight, Duty EtcDocument9 pagesUnit - Iii Final Account: I.e., All Manufacturing Expenses, Carriage, Cartage, Freight, Duty EtcWelcome 1995No ratings yet

- Chapter 6 - SOPL FormatDocument1 pageChapter 6 - SOPL Formatquraisha irdinaNo ratings yet

- Formats of Income Statement, Balance Sheet & Cash Flow StatementDocument3 pagesFormats of Income Statement, Balance Sheet & Cash Flow StatementAli RazaNo ratings yet

- A2 Accounting Revision KitDocument135 pagesA2 Accounting Revision KitWaniya AmirNo ratings yet

- Final Accounts of SoletradersDocument9 pagesFinal Accounts of SoletradersShanavaz AsokachalilNo ratings yet

- General Format For Final AccountsDocument2 pagesGeneral Format For Final AccountsGokulCj GroveNo ratings yet

- Business IncomeDocument8 pagesBusiness IncomeMoon Kim100% (1)

- Accounting 0452 Notes-Ch8Document3 pagesAccounting 0452 Notes-Ch8Huma PeeranNo ratings yet

- Lesson 3d Preparation of Statement of Comprehensive Income - Manufacturing BusinessDocument8 pagesLesson 3d Preparation of Statement of Comprehensive Income - Manufacturing BusinessBenedict CladoNo ratings yet

- Final Account - PDF FormatDocument8 pagesFinal Account - PDF Formatpranaylanjewar644No ratings yet

- Chapter 2 Format and Importance of Financial StatementsDocument36 pagesChapter 2 Format and Importance of Financial Statementsprincekelvin09No ratings yet

- Fundamentals of Accountancy, Business, and Management 2: Prepared By: Mark Vincent B. Bantog, LPTDocument15 pagesFundamentals of Accountancy, Business, and Management 2: Prepared By: Mark Vincent B. Bantog, LPTSherlock HolmesNo ratings yet

- Proforma of Final AccountsDocument3 pagesProforma of Final AccountsSarath kumar C100% (1)

- Mickey EntrepreneurshipDocument80 pagesMickey EntrepreneurshipJamaica AdayNo ratings yet

- Cash From Operations: Reconciliation of ToDocument2 pagesCash From Operations: Reconciliation of ToArshad ChaudharyNo ratings yet

- ACCOUNTINGDocument2 pagesACCOUNTINGMarie OrbetaNo ratings yet

- FSs For CompaniesDocument9 pagesFSs For CompaniesFarid UddinNo ratings yet

- CHAPTER 2 StudentDocument10 pagesCHAPTER 2 Studentfelicia tanNo ratings yet

- AC 102 Financial Statements FormatsDocument5 pagesAC 102 Financial Statements FormatsBendroza MelatosiNo ratings yet

- Final AccountsDocument9 pagesFinal AccountsRositaNo ratings yet

- Merchandising Operations: Inventory Base. These Items Are Then Resold To Customers and Recorded As Sales RevenueDocument12 pagesMerchandising Operations: Inventory Base. These Items Are Then Resold To Customers and Recorded As Sales RevenueMingxNo ratings yet

- NPO - Income &expenditureDocument47 pagesNPO - Income &expenditureAhmad NawazNo ratings yet

- EC 1 - Acctg Cycle Part 2 ConceptsDocument3 pagesEC 1 - Acctg Cycle Part 2 ConceptsChelay EscarezNo ratings yet

- S.Y.J.C. (Commerce) Book-Kkeping & Accoutancy Partnership Final Accounts Compiled By: Prof. Bosco FernandesDocument11 pagesS.Y.J.C. (Commerce) Book-Kkeping & Accoutancy Partnership Final Accounts Compiled By: Prof. Bosco FernandesDheer BhanushaliNo ratings yet

- Accounting Staff Written AnswerDocument2 pagesAccounting Staff Written Answercla manpowerservices100% (1)

- Project Report Papad ManufacturingDocument7 pagesProject Report Papad ManufacturingPriyotosh DasNo ratings yet

- Chapter 04 Completing The Accounting CycleDocument45 pagesChapter 04 Completing The Accounting CycleMohammad RekabderNo ratings yet

- PARCORDocument5 pagesPARCORjelai anselmoNo ratings yet

- Accrual Accounting ProcessDocument33 pagesAccrual Accounting ProcessLu CasNo ratings yet

- Identify The Choice That Best Completes The Statement or Answers The QuestionDocument8 pagesIdentify The Choice That Best Completes The Statement or Answers The QuestionMary Grace Errabo FloridoNo ratings yet

- Fundamentals of Accounting Fall 2022Document5 pagesFundamentals of Accounting Fall 2022umer iqbalNo ratings yet

- ULOb Activity 1Document4 pagesULOb Activity 1emem resuentoNo ratings yet

- 2012 Paper F9 Mnemonics and Charts Sample Download v1Document55 pages2012 Paper F9 Mnemonics and Charts Sample Download v1Yashvin AlwarNo ratings yet

- AE 19 Exercise Problem Financial Planning and Forecasting 2Document2 pagesAE 19 Exercise Problem Financial Planning and Forecasting 2John Anjelo MoraldeNo ratings yet

- Connect2India Advanced Company ReportDocument20 pagesConnect2India Advanced Company ReportBabar Khan100% (1)

- Cash Flow Statement 2016-2020Document8 pagesCash Flow Statement 2016-2020yip manNo ratings yet

- Balance Sheet s8 Shared 2021Document18 pagesBalance Sheet s8 Shared 2021nikhil gangwarNo ratings yet

- Harvard 2Document12 pagesHarvard 2Author MuriithiNo ratings yet

- Pt. Sumber Alam Sekurau: Material ReceiveDocument5 pagesPt. Sumber Alam Sekurau: Material ReceiveAlbert NathanNo ratings yet

- Chapter 4 4 4 4 4Document7 pagesChapter 4 4 4 4 4Rabie HarounNo ratings yet

- Oilcorp FinancialStatement ShareStats Properties NoticeAGM (490KB)Document65 pagesOilcorp FinancialStatement ShareStats Properties NoticeAGM (490KB)James WarrenNo ratings yet

- P17Document8 pagesP17Maria Adventia JovancaNo ratings yet

- National Accounting Standard For Commercial Organisations 1 "Presentation of Financial Statements"Document15 pagesNational Accounting Standard For Commercial Organisations 1 "Presentation of Financial Statements"azimovazNo ratings yet

- Cannon Ball Review With Exercises Part 2 PDFDocument30 pagesCannon Ball Review With Exercises Part 2 PDFLayNo ratings yet

- Chapter (2) : Financial Feasibility StudyDocument52 pagesChapter (2) : Financial Feasibility StudyDing RarugalNo ratings yet

- tbch12Document35 pagestbch12Daisy Jane V. CamalingNo ratings yet

- Home Office and BranchDocument6 pagesHome Office and BranchYudna YuNo ratings yet

- Afar 2 Quizzes AcgsbdjxjcudhdhDocument27 pagesAfar 2 Quizzes Acgsbdjxjcudhdhrandomlungs121223No ratings yet

- Case StudyDocument22 pagesCase StudyM Zain Ul AbedeenNo ratings yet

- Payables: When We Receive The Goods in The Staging Area The Accounting Entry Would Be (MAS) / (GRN)Document15 pagesPayables: When We Receive The Goods in The Staging Area The Accounting Entry Would Be (MAS) / (GRN)VK SHARMANo ratings yet

Download as docx, pdf, or txt

You might also like

- Format Sopl and SofpDocument3 pagesFormat Sopl and SofpMuhammad Faaiz IzzeawanNo ratings yet

- CPA Review Notes 2019 - FAR (Financial Accounting and Reporting)From EverandCPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Rating: 3.5 out of 5 stars3.5/5 (17)

- Cattle Fattening FinancialsDocument5 pagesCattle Fattening Financialsprince kupaNo ratings yet

- Sime Darby BerhadDocument16 pagesSime Darby Berhadjue -No ratings yet

- Jiranna Financials 22Document20 pagesJiranna Financials 22Ellen MarkNo ratings yet

- Preparation of Financial Statement For A Sole TraderDocument8 pagesPreparation of Financial Statement For A Sole TraderDebbie Debz100% (3)

- Tutorial 7 Trade Receivables (Q)Document3 pagesTutorial 7 Trade Receivables (Q)lious liiNo ratings yet

- Chapter 2 Statement of Income and Statement of Owner's Equity PDFDocument8 pagesChapter 2 Statement of Income and Statement of Owner's Equity PDFNathaniel LacamentoNo ratings yet

- Company Final AccountsDocument13 pagesCompany Final Accountsshanthala mNo ratings yet

- Lesson 3c The Statement of Comprehensive Income - Merchandising BusinessDocument11 pagesLesson 3c The Statement of Comprehensive Income - Merchandising BusinessBenedict CladoNo ratings yet

- Format SoplDocument2 pagesFormat Soplhumairayazid12No ratings yet

- Income StatementDocument1 pageIncome StatementTanakha MaziwisaNo ratings yet

- Financial Statements of Sole Trader (Unit-04) PDFDocument3 pagesFinancial Statements of Sole Trader (Unit-04) PDFImadNo ratings yet

- Accounts Chapter 8Document10 pagesAccounts Chapter 8R.mNo ratings yet

- Chapter 7Document15 pagesChapter 7msukri_81No ratings yet

- Income Statement Format-MerchandisingDocument1 pageIncome Statement Format-MerchandisingSiam FarhanNo ratings yet

- The Income StatementDocument18 pagesThe Income Statementmudiwachokuda1234567No ratings yet

- Notes of Financial Statements or Final AccountsDocument11 pagesNotes of Financial Statements or Final Accountsrxcha.josephNo ratings yet

- Guidelines Re Selling and Admi Expenses - 2014Document2 pagesGuidelines Re Selling and Admi Expenses - 2014HaideBrocalesNo ratings yet

- Chap-7, 8 & 9 (Income Statemnet & Statement of Financial Position)Document17 pagesChap-7, 8 & 9 (Income Statemnet & Statement of Financial Position)7a4374 hisNo ratings yet

- Unit 02 Preparation of Financial Statement As Per IND AS 01Document13 pagesUnit 02 Preparation of Financial Statement As Per IND AS 01Deepak LNo ratings yet

- 10532lectuer 5 FADocument28 pages10532lectuer 5 FANajia SalmanNo ratings yet

- Xyz Company Income Statement FOR THE YEAR ENDEDDocument1 pageXyz Company Income Statement FOR THE YEAR ENDEDDaniyal AhmadNo ratings yet

- Chap-7, 8 & 9 (Income Statemnet & Statement of Financial Position)Document18 pagesChap-7, 8 & 9 (Income Statemnet & Statement of Financial Position)7a4374 hisNo ratings yet

- Merchandising OperationsDocument33 pagesMerchandising OperationsDanica MedinaNo ratings yet

- Final AccountDocument2 pagesFinal Accountmeelas123No ratings yet

- Actg101 Fs Prepa TemplateDocument16 pagesActg101 Fs Prepa TemplateJaira ClavoNo ratings yet

- Tally Trading and Profit Loss Acc Balance SheetDocument14 pagesTally Trading and Profit Loss Acc Balance Sheetsuresh kumar10No ratings yet

- POA FormatsDocument7 pagesPOA FormatsWilliNo ratings yet

- Income StatementDocument4 pagesIncome StatementBurhan AzharNo ratings yet

- Fundamentals of Accounting and Business ManagementDocument4 pagesFundamentals of Accounting and Business ManagementSan Juan Ezthie100% (1)

- Final - Accounts Format 234 PDFDocument13 pagesFinal - Accounts Format 234 PDFajaychattaNo ratings yet

- Final - Accounts Format PDFDocument13 pagesFinal - Accounts Format PDFajaychatta100% (1)

- AAAAADocument2 pagesAAAAAIrish CastilloNo ratings yet

- Is SofpDocument2 pagesIs SofpHilwa FarhanNo ratings yet

- Income Statement FormatDocument2 pagesIncome Statement FormatShruti MohanNo ratings yet

- Manufacturing AccountDocument2 pagesManufacturing Accountmeelas123100% (2)

- Departmental TradingDocument1 pageDepartmental Tradingmeelas123No ratings yet

- Accounting FormatsDocument21 pagesAccounting FormatsAsima ZubairNo ratings yet

- Unit - Iii Final Account: I.e., All Manufacturing Expenses, Carriage, Cartage, Freight, Duty EtcDocument9 pagesUnit - Iii Final Account: I.e., All Manufacturing Expenses, Carriage, Cartage, Freight, Duty EtcWelcome 1995No ratings yet

- Chapter 6 - SOPL FormatDocument1 pageChapter 6 - SOPL Formatquraisha irdinaNo ratings yet

- Formats of Income Statement, Balance Sheet & Cash Flow StatementDocument3 pagesFormats of Income Statement, Balance Sheet & Cash Flow StatementAli RazaNo ratings yet

- A2 Accounting Revision KitDocument135 pagesA2 Accounting Revision KitWaniya AmirNo ratings yet

- Final Accounts of SoletradersDocument9 pagesFinal Accounts of SoletradersShanavaz AsokachalilNo ratings yet

- General Format For Final AccountsDocument2 pagesGeneral Format For Final AccountsGokulCj GroveNo ratings yet

- Business IncomeDocument8 pagesBusiness IncomeMoon Kim100% (1)

- Accounting 0452 Notes-Ch8Document3 pagesAccounting 0452 Notes-Ch8Huma PeeranNo ratings yet

- Lesson 3d Preparation of Statement of Comprehensive Income - Manufacturing BusinessDocument8 pagesLesson 3d Preparation of Statement of Comprehensive Income - Manufacturing BusinessBenedict CladoNo ratings yet

- Final Account - PDF FormatDocument8 pagesFinal Account - PDF Formatpranaylanjewar644No ratings yet

- Chapter 2 Format and Importance of Financial StatementsDocument36 pagesChapter 2 Format and Importance of Financial Statementsprincekelvin09No ratings yet

- Fundamentals of Accountancy, Business, and Management 2: Prepared By: Mark Vincent B. Bantog, LPTDocument15 pagesFundamentals of Accountancy, Business, and Management 2: Prepared By: Mark Vincent B. Bantog, LPTSherlock HolmesNo ratings yet

- Proforma of Final AccountsDocument3 pagesProforma of Final AccountsSarath kumar C100% (1)

- Mickey EntrepreneurshipDocument80 pagesMickey EntrepreneurshipJamaica AdayNo ratings yet

- Cash From Operations: Reconciliation of ToDocument2 pagesCash From Operations: Reconciliation of ToArshad ChaudharyNo ratings yet

- ACCOUNTINGDocument2 pagesACCOUNTINGMarie OrbetaNo ratings yet

- FSs For CompaniesDocument9 pagesFSs For CompaniesFarid UddinNo ratings yet

- CHAPTER 2 StudentDocument10 pagesCHAPTER 2 Studentfelicia tanNo ratings yet

- AC 102 Financial Statements FormatsDocument5 pagesAC 102 Financial Statements FormatsBendroza MelatosiNo ratings yet

- Final AccountsDocument9 pagesFinal AccountsRositaNo ratings yet

- Merchandising Operations: Inventory Base. These Items Are Then Resold To Customers and Recorded As Sales RevenueDocument12 pagesMerchandising Operations: Inventory Base. These Items Are Then Resold To Customers and Recorded As Sales RevenueMingxNo ratings yet

- NPO - Income &expenditureDocument47 pagesNPO - Income &expenditureAhmad NawazNo ratings yet

- EC 1 - Acctg Cycle Part 2 ConceptsDocument3 pagesEC 1 - Acctg Cycle Part 2 ConceptsChelay EscarezNo ratings yet

- S.Y.J.C. (Commerce) Book-Kkeping & Accoutancy Partnership Final Accounts Compiled By: Prof. Bosco FernandesDocument11 pagesS.Y.J.C. (Commerce) Book-Kkeping & Accoutancy Partnership Final Accounts Compiled By: Prof. Bosco FernandesDheer BhanushaliNo ratings yet

- Accounting Staff Written AnswerDocument2 pagesAccounting Staff Written Answercla manpowerservices100% (1)

- Project Report Papad ManufacturingDocument7 pagesProject Report Papad ManufacturingPriyotosh DasNo ratings yet

- Chapter 04 Completing The Accounting CycleDocument45 pagesChapter 04 Completing The Accounting CycleMohammad RekabderNo ratings yet

- PARCORDocument5 pagesPARCORjelai anselmoNo ratings yet

- Accrual Accounting ProcessDocument33 pagesAccrual Accounting ProcessLu CasNo ratings yet

- Identify The Choice That Best Completes The Statement or Answers The QuestionDocument8 pagesIdentify The Choice That Best Completes The Statement or Answers The QuestionMary Grace Errabo FloridoNo ratings yet

- Fundamentals of Accounting Fall 2022Document5 pagesFundamentals of Accounting Fall 2022umer iqbalNo ratings yet

- ULOb Activity 1Document4 pagesULOb Activity 1emem resuentoNo ratings yet

- 2012 Paper F9 Mnemonics and Charts Sample Download v1Document55 pages2012 Paper F9 Mnemonics and Charts Sample Download v1Yashvin AlwarNo ratings yet

- AE 19 Exercise Problem Financial Planning and Forecasting 2Document2 pagesAE 19 Exercise Problem Financial Planning and Forecasting 2John Anjelo MoraldeNo ratings yet

- Connect2India Advanced Company ReportDocument20 pagesConnect2India Advanced Company ReportBabar Khan100% (1)

- Cash Flow Statement 2016-2020Document8 pagesCash Flow Statement 2016-2020yip manNo ratings yet

- Balance Sheet s8 Shared 2021Document18 pagesBalance Sheet s8 Shared 2021nikhil gangwarNo ratings yet

- Harvard 2Document12 pagesHarvard 2Author MuriithiNo ratings yet

- Pt. Sumber Alam Sekurau: Material ReceiveDocument5 pagesPt. Sumber Alam Sekurau: Material ReceiveAlbert NathanNo ratings yet

- Chapter 4 4 4 4 4Document7 pagesChapter 4 4 4 4 4Rabie HarounNo ratings yet

- Oilcorp FinancialStatement ShareStats Properties NoticeAGM (490KB)Document65 pagesOilcorp FinancialStatement ShareStats Properties NoticeAGM (490KB)James WarrenNo ratings yet

- P17Document8 pagesP17Maria Adventia JovancaNo ratings yet

- National Accounting Standard For Commercial Organisations 1 "Presentation of Financial Statements"Document15 pagesNational Accounting Standard For Commercial Organisations 1 "Presentation of Financial Statements"azimovazNo ratings yet

- Cannon Ball Review With Exercises Part 2 PDFDocument30 pagesCannon Ball Review With Exercises Part 2 PDFLayNo ratings yet

- Chapter (2) : Financial Feasibility StudyDocument52 pagesChapter (2) : Financial Feasibility StudyDing RarugalNo ratings yet

- tbch12Document35 pagestbch12Daisy Jane V. CamalingNo ratings yet

- Home Office and BranchDocument6 pagesHome Office and BranchYudna YuNo ratings yet

- Afar 2 Quizzes AcgsbdjxjcudhdhDocument27 pagesAfar 2 Quizzes Acgsbdjxjcudhdhrandomlungs121223No ratings yet

- Case StudyDocument22 pagesCase StudyM Zain Ul AbedeenNo ratings yet

- Payables: When We Receive The Goods in The Staging Area The Accounting Entry Would Be (MAS) / (GRN)Document15 pagesPayables: When We Receive The Goods in The Staging Area The Accounting Entry Would Be (MAS) / (GRN)VK SHARMANo ratings yet