Financial Services

Financial Services

You might also like

- PenFed Loan Check MethodDocument23 pagesPenFed Loan Check MethodOlaseni Luqman71% (7)

- Technopreneurship WK13Document96 pagesTechnopreneurship WK13Juvill VillaroyaNo ratings yet

- Impact of Self Help Group - Bank Linkage Programme and Its Role On The Upliftmentof The Poor Special Reference To Raigad District MH State Prasada RaoDocument302 pagesImpact of Self Help Group - Bank Linkage Programme and Its Role On The Upliftmentof The Poor Special Reference To Raigad District MH State Prasada RaosheetalNo ratings yet

- Chapter No.4 Conceptual FrameworkDocument64 pagesChapter No.4 Conceptual Frameworkpooja shandilyaNo ratings yet

- Corporate Finance Assignment: ON Role of Financial Services in Economic Development of A CountryDocument8 pagesCorporate Finance Assignment: ON Role of Financial Services in Economic Development of A CountryYaman SalujaNo ratings yet

- Sources of Funds: Unit IiDocument36 pagesSources of Funds: Unit IiFara HameedNo ratings yet

- Innovative Financial ServicesDocument9 pagesInnovative Financial ServicesShubham GuptaNo ratings yet

- Financial Services - Unit 1Document72 pagesFinancial Services - Unit 1Darshini Thummar-ppmNo ratings yet

- Unit 3 Financial ServicesDocument18 pagesUnit 3 Financial ServicesCaptain Rs -pubg mobileNo ratings yet

- Fund Based Financial ServicesDocument45 pagesFund Based Financial Servicesamitsingla19No ratings yet

- Credit Card FraudsDocument63 pagesCredit Card FraudsAnaghaPuranikNo ratings yet

- BantomtatDocument5 pagesBantomtatmanhphatcube1704No ratings yet

- Roll No:1017 Subject:Fundamentals of Financial Services Presentation Topic: Classification of Financial ServicesDocument24 pagesRoll No:1017 Subject:Fundamentals of Financial Services Presentation Topic: Classification of Financial ServicesRama SardesaiNo ratings yet

- FIM- UNIT -4Document8 pagesFIM- UNIT -4manishramesh555No ratings yet

- Short Term FinancingDocument16 pagesShort Term FinancingKoko AlakNo ratings yet

- FM Chapter 2: Source of FinanceDocument11 pagesFM Chapter 2: Source of FinancePillows GonzalesNo ratings yet

- Chapter 6Document27 pagesChapter 6adNo ratings yet

- Sources of Financing To Non-GovtDocument14 pagesSources of Financing To Non-GovtCorolla SedanNo ratings yet

- CollateralDocument3 pagesCollateralVeronicaNo ratings yet

- Guia Segundo ParcialDocument12 pagesGuia Segundo ParcialBety MedinaNo ratings yet

- Services That Are Offered by Financial Companies Are Called Financial ServicesDocument8 pagesServices That Are Offered by Financial Companies Are Called Financial ServicesPari SavlaNo ratings yet

- AssignmentDocument4 pagesAssignmentMahamNo ratings yet

- I & E FinanceDocument37 pagesI & E FinanceDeepak GuptaNo ratings yet

- Unit 1Document12 pagesUnit 1Manav MundraNo ratings yet

- Chapter 2Document21 pagesChapter 2fentawmelaku1993No ratings yet

- Financial Services Management: Presented by - Saurabh ShahDocument110 pagesFinancial Services Management: Presented by - Saurabh ShahKarim MerchantNo ratings yet

- Classification of Financial Services IndustryDocument4 pagesClassification of Financial Services IndustryRiteshHPatelNo ratings yet

- POF Assignment 01Document5 pagesPOF Assignment 01Dhoni KhanNo ratings yet

- Chapter 8Document54 pagesChapter 8Bishounen 42No ratings yet

- Unit I MBF22408T Credit Risk and Recovery ManagementDocument17 pagesUnit I MBF22408T Credit Risk and Recovery ManagementSheetal DwevediNo ratings yet

- Full Notes MBF22408T Credit Risk and Recovery ManagementDocument90 pagesFull Notes MBF22408T Credit Risk and Recovery ManagementSheetal DwevediNo ratings yet

- Direct Financingdirect Vs Indirect FinancinngDocument2 pagesDirect Financingdirect Vs Indirect FinancinngMorelate KupfurwaNo ratings yet

- Business Management: FinanceDocument42 pagesBusiness Management: FinanceRamNo ratings yet

- Discus in Detail The Following Financial Institutions/government Agencies Financial Relationship With Construction CompaniesDocument5 pagesDiscus in Detail The Following Financial Institutions/government Agencies Financial Relationship With Construction CompaniesAbrsh AbrshNo ratings yet

- FINANCIAL SERVICES - Final - CHP - 1Document32 pagesFINANCIAL SERVICES - Final - CHP - 1ParthNo ratings yet

- Fmi CH 1 130730050202 Phpapp01Document36 pagesFmi CH 1 130730050202 Phpapp01Jubayet HossainNo ratings yet

- 20MEV3CA Venture FinancingDocument107 pages20MEV3CA Venture FinancingsrinivasanscribdNo ratings yet

- FMIS Assignment 2Document8 pagesFMIS Assignment 2nitin heart hakerNo ratings yet

- Week 6 and Week 7Document49 pagesWeek 6 and Week 7Muneeb AmanNo ratings yet

- Types of Other Depository InstitutionsDocument8 pagesTypes of Other Depository Institutionsnatnaelsleshi3No ratings yet

- SecuritizationDocument8 pagesSecuritizationDdev ThaparrNo ratings yet

- Definition of Business FinanceDocument4 pagesDefinition of Business FinanceClovisNo ratings yet

- 2 Financial Assets and MarketsDocument42 pages2 Financial Assets and MarketsM-Faheem AslamNo ratings yet

- Lesson - Sources of FundsDocument14 pagesLesson - Sources of FundsJohn Paul GonzalesNo ratings yet

- BPP - CH - 3 Sources of FundDocument11 pagesBPP - CH - 3 Sources of Fundsamrawithagos2002No ratings yet

- Mfs Unit 2 FinalDocument12 pagesMfs Unit 2 FinalRama SardesaiNo ratings yet

- Bank LendingDocument77 pagesBank Lendinghaarrisali7No ratings yet

- Chapter-2 (Saleh Sir)Document24 pagesChapter-2 (Saleh Sir)MD Rakib MiaNo ratings yet

- Financial MarketDocument8 pagesFinancial Marketshahid3454No ratings yet

- Import FinancingDocument11 pagesImport FinancingDheeraj rawatNo ratings yet

- Unit VDocument9 pagesUnit VJayNo ratings yet

- Ekonomi - Non BankDocument9 pagesEkonomi - Non BankDian FirdausNo ratings yet

- Financing The Working Capital 1Document3 pagesFinancing The Working Capital 1Angelie AnilloNo ratings yet

- Sources of Working CapitalDocument7 pagesSources of Working CapitalSreelekshmi Kr100% (1)

- Banking ReportDocument2 pagesBanking ReportAnasNo ratings yet

- Personal FinanceDocument1 pagePersonal FinanceMaika J. PudaderaNo ratings yet

- Chpater 5 - Banking SystemDocument10 pagesChpater 5 - Banking System21augustNo ratings yet

- Venture CapitalDocument17 pagesVenture CapitalVidhyaBalaNo ratings yet

- Economic Functions of The Financial InstitutionsDocument3 pagesEconomic Functions of The Financial InstitutionsKemotherapy LifesucksNo ratings yet

- Loans and AdvancesDocument6 pagesLoans and AdvancesAnusuya Chela100% (1)

- Tactical Objective: Strategic Maneuvers, Decoding the Art of Military PrecisionFrom EverandTactical Objective: Strategic Maneuvers, Decoding the Art of Military PrecisionNo ratings yet

- Unit 5 - Business StrategyDocument12 pagesUnit 5 - Business StrategyABRIL TANIA PATI TORREZNo ratings yet

- Investment Services and Investment Process of Unicon Investment SolutionsDocument15 pagesInvestment Services and Investment Process of Unicon Investment SolutionsArif KhanNo ratings yet

- Section 80d of Income TaxDocument7 pagesSection 80d of Income TaxBAJRANG LAL AgrawalNo ratings yet

- Activity 3.5 General Annuity: MembersDocument9 pagesActivity 3.5 General Annuity: MembersBrix RemanesesNo ratings yet

- Apr.12 - 871 App Nri FormDocument10 pagesApr.12 - 871 App Nri FormsnkrmNo ratings yet

- Basic Ratemaking - Chapter 4 - Lesson 2Document23 pagesBasic Ratemaking - Chapter 4 - Lesson 2djqNo ratings yet

- Sbimf Project ReportDocument66 pagesSbimf Project ReportAman Gupta100% (1)

- Equitas AR20 PDFDocument196 pagesEquitas AR20 PDFpinky gargNo ratings yet

- Description: 1. Question Details Jmodd7 5.4.001.cmi. (1639656)Document3 pagesDescription: 1. Question Details Jmodd7 5.4.001.cmi. (1639656)Suvaid KcNo ratings yet

- DMCI Homes Online Payment ManualDocument15 pagesDMCI Homes Online Payment ManualdizzybeeNo ratings yet

- Balance Sheet of HDFC STANDARD LIFE As at March 31 For Five YearsDocument7 pagesBalance Sheet of HDFC STANDARD LIFE As at March 31 For Five YearsNagendra PrasadNo ratings yet

- ABC Analysis - Adv Accounts by TRGDocument2 pagesABC Analysis - Adv Accounts by TRGshubrasiNo ratings yet

- American International Group (AIG) Fraud Case Analysis: ContentsDocument7 pagesAmerican International Group (AIG) Fraud Case Analysis: ContentsShuvo HowladerNo ratings yet

- Fundamental Analysis PDFDocument7 pagesFundamental Analysis PDFMonil BarbhayaNo ratings yet

- Set 3 - Pce Sample Questions 1. Which Act Is ... - ZurichDocument17 pagesSet 3 - Pce Sample Questions 1. Which Act Is ... - ZurichJasveen KaurNo ratings yet

- Comparable Companies 3E TemplateDocument22 pagesComparable Companies 3E TemplateLohith Kumar ReddyNo ratings yet

- COC LEVEL-3 PracticalDocument81 pagesCOC LEVEL-3 PracticalMohammed AbduramanNo ratings yet

- Chapter 1Document77 pagesChapter 1dieulinh230604No ratings yet

- Reading 47 Fundamentals of Credit AnalysisDocument18 pagesReading 47 Fundamentals of Credit AnalysisNeerajNo ratings yet

- MS Nov 14 2006 ETF QuarterlyDocument268 pagesMS Nov 14 2006 ETF Quarterlyapi-3838885100% (1)

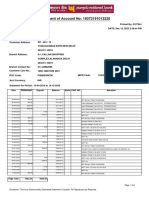

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument3 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalancePooja GolandeNo ratings yet

- MUCLecture 2022 51643431Document15 pagesMUCLecture 2022 51643431gold.2000.dzNo ratings yet

- 1.permanent Account Number (PAN)Document15 pages1.permanent Account Number (PAN)Yash GoklaniNo ratings yet

- KavitaDocument8 pagesKavitaSneha SharmaNo ratings yet

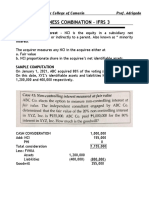

- Lesson 3. Consolidated Financial StatementsDocument6 pagesLesson 3. Consolidated Financial StatementsKsUnlockerNo ratings yet

- Chapter 2 IAS 1 Presentation of Financial StatementsDocument85 pagesChapter 2 IAS 1 Presentation of Financial StatementsLidia SamuelNo ratings yet

- Cancellation of Sip STP SWP Form CANARA ROBECODocument2 pagesCancellation of Sip STP SWP Form CANARA ROBECOSabyaNo ratings yet

- Requirement: Determine The Financial Liabilities To Be Disclosed in The NotesDocument4 pagesRequirement: Determine The Financial Liabilities To Be Disclosed in The NotesInvisible CionNo ratings yet

Download as docx, pdf, or txt

You might also like

- PenFed Loan Check MethodDocument23 pagesPenFed Loan Check MethodOlaseni Luqman71% (7)

- Technopreneurship WK13Document96 pagesTechnopreneurship WK13Juvill VillaroyaNo ratings yet

- Impact of Self Help Group - Bank Linkage Programme and Its Role On The Upliftmentof The Poor Special Reference To Raigad District MH State Prasada RaoDocument302 pagesImpact of Self Help Group - Bank Linkage Programme and Its Role On The Upliftmentof The Poor Special Reference To Raigad District MH State Prasada RaosheetalNo ratings yet

- Chapter No.4 Conceptual FrameworkDocument64 pagesChapter No.4 Conceptual Frameworkpooja shandilyaNo ratings yet

- Corporate Finance Assignment: ON Role of Financial Services in Economic Development of A CountryDocument8 pagesCorporate Finance Assignment: ON Role of Financial Services in Economic Development of A CountryYaman SalujaNo ratings yet

- Sources of Funds: Unit IiDocument36 pagesSources of Funds: Unit IiFara HameedNo ratings yet

- Innovative Financial ServicesDocument9 pagesInnovative Financial ServicesShubham GuptaNo ratings yet

- Financial Services - Unit 1Document72 pagesFinancial Services - Unit 1Darshini Thummar-ppmNo ratings yet

- Unit 3 Financial ServicesDocument18 pagesUnit 3 Financial ServicesCaptain Rs -pubg mobileNo ratings yet

- Fund Based Financial ServicesDocument45 pagesFund Based Financial Servicesamitsingla19No ratings yet

- Credit Card FraudsDocument63 pagesCredit Card FraudsAnaghaPuranikNo ratings yet

- BantomtatDocument5 pagesBantomtatmanhphatcube1704No ratings yet

- Roll No:1017 Subject:Fundamentals of Financial Services Presentation Topic: Classification of Financial ServicesDocument24 pagesRoll No:1017 Subject:Fundamentals of Financial Services Presentation Topic: Classification of Financial ServicesRama SardesaiNo ratings yet

- FIM- UNIT -4Document8 pagesFIM- UNIT -4manishramesh555No ratings yet

- Short Term FinancingDocument16 pagesShort Term FinancingKoko AlakNo ratings yet

- FM Chapter 2: Source of FinanceDocument11 pagesFM Chapter 2: Source of FinancePillows GonzalesNo ratings yet

- Chapter 6Document27 pagesChapter 6adNo ratings yet

- Sources of Financing To Non-GovtDocument14 pagesSources of Financing To Non-GovtCorolla SedanNo ratings yet

- CollateralDocument3 pagesCollateralVeronicaNo ratings yet

- Guia Segundo ParcialDocument12 pagesGuia Segundo ParcialBety MedinaNo ratings yet

- Services That Are Offered by Financial Companies Are Called Financial ServicesDocument8 pagesServices That Are Offered by Financial Companies Are Called Financial ServicesPari SavlaNo ratings yet

- AssignmentDocument4 pagesAssignmentMahamNo ratings yet

- I & E FinanceDocument37 pagesI & E FinanceDeepak GuptaNo ratings yet

- Unit 1Document12 pagesUnit 1Manav MundraNo ratings yet

- Chapter 2Document21 pagesChapter 2fentawmelaku1993No ratings yet

- Financial Services Management: Presented by - Saurabh ShahDocument110 pagesFinancial Services Management: Presented by - Saurabh ShahKarim MerchantNo ratings yet

- Classification of Financial Services IndustryDocument4 pagesClassification of Financial Services IndustryRiteshHPatelNo ratings yet

- POF Assignment 01Document5 pagesPOF Assignment 01Dhoni KhanNo ratings yet

- Chapter 8Document54 pagesChapter 8Bishounen 42No ratings yet

- Unit I MBF22408T Credit Risk and Recovery ManagementDocument17 pagesUnit I MBF22408T Credit Risk and Recovery ManagementSheetal DwevediNo ratings yet

- Full Notes MBF22408T Credit Risk and Recovery ManagementDocument90 pagesFull Notes MBF22408T Credit Risk and Recovery ManagementSheetal DwevediNo ratings yet

- Direct Financingdirect Vs Indirect FinancinngDocument2 pagesDirect Financingdirect Vs Indirect FinancinngMorelate KupfurwaNo ratings yet

- Business Management: FinanceDocument42 pagesBusiness Management: FinanceRamNo ratings yet

- Discus in Detail The Following Financial Institutions/government Agencies Financial Relationship With Construction CompaniesDocument5 pagesDiscus in Detail The Following Financial Institutions/government Agencies Financial Relationship With Construction CompaniesAbrsh AbrshNo ratings yet

- FINANCIAL SERVICES - Final - CHP - 1Document32 pagesFINANCIAL SERVICES - Final - CHP - 1ParthNo ratings yet

- Fmi CH 1 130730050202 Phpapp01Document36 pagesFmi CH 1 130730050202 Phpapp01Jubayet HossainNo ratings yet

- 20MEV3CA Venture FinancingDocument107 pages20MEV3CA Venture FinancingsrinivasanscribdNo ratings yet

- FMIS Assignment 2Document8 pagesFMIS Assignment 2nitin heart hakerNo ratings yet

- Week 6 and Week 7Document49 pagesWeek 6 and Week 7Muneeb AmanNo ratings yet

- Types of Other Depository InstitutionsDocument8 pagesTypes of Other Depository Institutionsnatnaelsleshi3No ratings yet

- SecuritizationDocument8 pagesSecuritizationDdev ThaparrNo ratings yet

- Definition of Business FinanceDocument4 pagesDefinition of Business FinanceClovisNo ratings yet

- 2 Financial Assets and MarketsDocument42 pages2 Financial Assets and MarketsM-Faheem AslamNo ratings yet

- Lesson - Sources of FundsDocument14 pagesLesson - Sources of FundsJohn Paul GonzalesNo ratings yet

- BPP - CH - 3 Sources of FundDocument11 pagesBPP - CH - 3 Sources of Fundsamrawithagos2002No ratings yet

- Mfs Unit 2 FinalDocument12 pagesMfs Unit 2 FinalRama SardesaiNo ratings yet

- Bank LendingDocument77 pagesBank Lendinghaarrisali7No ratings yet

- Chapter-2 (Saleh Sir)Document24 pagesChapter-2 (Saleh Sir)MD Rakib MiaNo ratings yet

- Financial MarketDocument8 pagesFinancial Marketshahid3454No ratings yet

- Import FinancingDocument11 pagesImport FinancingDheeraj rawatNo ratings yet

- Unit VDocument9 pagesUnit VJayNo ratings yet

- Ekonomi - Non BankDocument9 pagesEkonomi - Non BankDian FirdausNo ratings yet

- Financing The Working Capital 1Document3 pagesFinancing The Working Capital 1Angelie AnilloNo ratings yet

- Sources of Working CapitalDocument7 pagesSources of Working CapitalSreelekshmi Kr100% (1)

- Banking ReportDocument2 pagesBanking ReportAnasNo ratings yet

- Personal FinanceDocument1 pagePersonal FinanceMaika J. PudaderaNo ratings yet

- Chpater 5 - Banking SystemDocument10 pagesChpater 5 - Banking System21augustNo ratings yet

- Venture CapitalDocument17 pagesVenture CapitalVidhyaBalaNo ratings yet

- Economic Functions of The Financial InstitutionsDocument3 pagesEconomic Functions of The Financial InstitutionsKemotherapy LifesucksNo ratings yet

- Loans and AdvancesDocument6 pagesLoans and AdvancesAnusuya Chela100% (1)

- Tactical Objective: Strategic Maneuvers, Decoding the Art of Military PrecisionFrom EverandTactical Objective: Strategic Maneuvers, Decoding the Art of Military PrecisionNo ratings yet

- Unit 5 - Business StrategyDocument12 pagesUnit 5 - Business StrategyABRIL TANIA PATI TORREZNo ratings yet

- Investment Services and Investment Process of Unicon Investment SolutionsDocument15 pagesInvestment Services and Investment Process of Unicon Investment SolutionsArif KhanNo ratings yet

- Section 80d of Income TaxDocument7 pagesSection 80d of Income TaxBAJRANG LAL AgrawalNo ratings yet

- Activity 3.5 General Annuity: MembersDocument9 pagesActivity 3.5 General Annuity: MembersBrix RemanesesNo ratings yet

- Apr.12 - 871 App Nri FormDocument10 pagesApr.12 - 871 App Nri FormsnkrmNo ratings yet

- Basic Ratemaking - Chapter 4 - Lesson 2Document23 pagesBasic Ratemaking - Chapter 4 - Lesson 2djqNo ratings yet

- Sbimf Project ReportDocument66 pagesSbimf Project ReportAman Gupta100% (1)

- Equitas AR20 PDFDocument196 pagesEquitas AR20 PDFpinky gargNo ratings yet

- Description: 1. Question Details Jmodd7 5.4.001.cmi. (1639656)Document3 pagesDescription: 1. Question Details Jmodd7 5.4.001.cmi. (1639656)Suvaid KcNo ratings yet

- DMCI Homes Online Payment ManualDocument15 pagesDMCI Homes Online Payment ManualdizzybeeNo ratings yet

- Balance Sheet of HDFC STANDARD LIFE As at March 31 For Five YearsDocument7 pagesBalance Sheet of HDFC STANDARD LIFE As at March 31 For Five YearsNagendra PrasadNo ratings yet

- ABC Analysis - Adv Accounts by TRGDocument2 pagesABC Analysis - Adv Accounts by TRGshubrasiNo ratings yet

- American International Group (AIG) Fraud Case Analysis: ContentsDocument7 pagesAmerican International Group (AIG) Fraud Case Analysis: ContentsShuvo HowladerNo ratings yet

- Fundamental Analysis PDFDocument7 pagesFundamental Analysis PDFMonil BarbhayaNo ratings yet

- Set 3 - Pce Sample Questions 1. Which Act Is ... - ZurichDocument17 pagesSet 3 - Pce Sample Questions 1. Which Act Is ... - ZurichJasveen KaurNo ratings yet

- Comparable Companies 3E TemplateDocument22 pagesComparable Companies 3E TemplateLohith Kumar ReddyNo ratings yet

- COC LEVEL-3 PracticalDocument81 pagesCOC LEVEL-3 PracticalMohammed AbduramanNo ratings yet

- Chapter 1Document77 pagesChapter 1dieulinh230604No ratings yet

- Reading 47 Fundamentals of Credit AnalysisDocument18 pagesReading 47 Fundamentals of Credit AnalysisNeerajNo ratings yet

- MS Nov 14 2006 ETF QuarterlyDocument268 pagesMS Nov 14 2006 ETF Quarterlyapi-3838885100% (1)

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument3 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalancePooja GolandeNo ratings yet

- MUCLecture 2022 51643431Document15 pagesMUCLecture 2022 51643431gold.2000.dzNo ratings yet

- 1.permanent Account Number (PAN)Document15 pages1.permanent Account Number (PAN)Yash GoklaniNo ratings yet

- KavitaDocument8 pagesKavitaSneha SharmaNo ratings yet

- Lesson 3. Consolidated Financial StatementsDocument6 pagesLesson 3. Consolidated Financial StatementsKsUnlockerNo ratings yet

- Chapter 2 IAS 1 Presentation of Financial StatementsDocument85 pagesChapter 2 IAS 1 Presentation of Financial StatementsLidia SamuelNo ratings yet

- Cancellation of Sip STP SWP Form CANARA ROBECODocument2 pagesCancellation of Sip STP SWP Form CANARA ROBECOSabyaNo ratings yet

- Requirement: Determine The Financial Liabilities To Be Disclosed in The NotesDocument4 pagesRequirement: Determine The Financial Liabilities To Be Disclosed in The NotesInvisible CionNo ratings yet