Ratio Analysis of Nepal Bank

Ratio Analysis of Nepal Bank

You might also like

- Friedan Global Capitalism SummaryDocument23 pagesFriedan Global Capitalism Summaryboomroasted34100% (13)

- Profitability Analysis of Nabil Bank LTD 2022Document42 pagesProfitability Analysis of Nabil Bank LTD 2022Prajwola Gajurel83% (12)

- The History Behind The National Economic Security and ReformationAct (NESARA)Document21 pagesThe History Behind The National Economic Security and ReformationAct (NESARA)Eddie Winkler80% (5)

- 3.7: Cash Flow: Activity: AnubisDocument3 pages3.7: Cash Flow: Activity: AnubisJornarnod50% (4)

- URP Income Tax Part SolutionsDocument127 pagesURP Income Tax Part SolutionsSushant MaskeyNo ratings yet

- English-Danish DictionaryDocument94 pagesEnglish-Danish DictionaryRoyMarie100% (8)

- 15 Ways To Earn Money 2020 - The Money EquationDocument18 pages15 Ways To Earn Money 2020 - The Money EquationThe Money Equation100% (1)

- Scotiabank Case StudyDocument10 pagesScotiabank Case StudyAnkushNo ratings yet

- 2080bs Financial Performance Analysis of Standard Chartered Bank Nepal LTDDocument51 pages2080bs Financial Performance Analysis of Standard Chartered Bank Nepal LTDBikeshNo ratings yet

- Profitiability Analysis of Nabil Bank Limited: A Project Work ReportDocument39 pagesProfitiability Analysis of Nabil Bank Limited: A Project Work Reportaakash shresthaNo ratings yet

- Profitability Analysis of Standard Charted Bank Nepal LimitedDocument41 pagesProfitability Analysis of Standard Charted Bank Nepal LimitedAnjal Shrestha100% (1)

- Bikesh FinalDocument47 pagesBikesh FinalBikeshNo ratings yet

- business research report_bbs of samir tamangDocument39 pagesbusiness research report_bbs of samir tamangroshansah222901No ratings yet

- 633396592-credit-management-of-nabil-bankDocument46 pages633396592-credit-management-of-nabil-bankmagardiwakar36No ratings yet

- Credit Management of Nabil BankDocument46 pagesCredit Management of Nabil BankNijan Jyakhwo100% (1)

- final-report nic asiaDocument48 pagesfinal-report nic asiasanjiv pasmanNo ratings yet

- 747786128 Final Report Nic AsiaDocument48 pages747786128 Final Report Nic Asiamagardiwakar36No ratings yet

- Heading of Report PDFDocument10 pagesHeading of Report PDFB safe nirman and suppliers pvt. ltd.No ratings yet

- Research Report of Bodh Kumar Thapa FinalDocument47 pagesResearch Report of Bodh Kumar Thapa FinalvectopgraphicNo ratings yet

- A study of loan management of nepal bank limitedDocument42 pagesA study of loan management of nepal bank limitedBikeshNo ratings yet

- Final Year Report of BBS 4th YearDocument49 pagesFinal Year Report of BBS 4th Yearnepalfinance987100% (2)

- Analysis of Working Capital Management of Machhapuchhre Bank LTDDocument41 pagesAnalysis of Working Capital Management of Machhapuchhre Bank LTDshresthanikhil078No ratings yet

- Liquidity and Profitability Analysis of Nabil Bank LimitedDocument37 pagesLiquidity and Profitability Analysis of Nabil Bank LimitedDeep Meditation100% (4)

- Toaz.info Bbs 4th Year Final Work Pr Da9ca60c8f9195a9c5c2c2cba0971b8eDocument48 pagesToaz.info Bbs 4th Year Final Work Pr Da9ca60c8f9195a9c5c2c2cba0971b8emangar2059No ratings yet

- Loan Management of Agriculture Development BankDocument36 pagesLoan Management of Agriculture Development BankanisheshkNo ratings yet

- Nabil ProfitabilityDocument44 pagesNabil Profitabilityabhishek shah100% (2)

- BBS ReportDocument49 pagesBBS ReportRaz BinadiNo ratings yet

- Ashik Final Report LatestDocument45 pagesAshik Final Report Latestashikdai55No ratings yet

- ThesisDocument35 pagesThesisAvinash De Monster DeulaNo ratings yet

- BBS Final Year ProjectDocument39 pagesBBS Final Year ProjectSamsher Kunwar100% (2)

- Effects of Credit Risk On The Financial Performance of Nepalese Commercial BanksDocument46 pagesEffects of Credit Risk On The Financial Performance of Nepalese Commercial BanksSasmina DahalNo ratings yet

- Project Work Sample - Sushila SilwalDocument48 pagesProject Work Sample - Sushila SilwalRam Prasad SilwalNo ratings yet

- Analysis of The Loan Provided by Citizen Bank Limited: A Project Work ReportDocument34 pagesAnalysis of The Loan Provided by Citizen Bank Limited: A Project Work ReportHem Raj JoshiNo ratings yet

- Report Bina FinalDocument36 pagesReport Bina FinalNxl AmikNo ratings yet

- Ajay BasnetDocument38 pagesAjay BasnetInternship ReportNo ratings yet

- Kushal Wod Final Report (Word File) (1) (1)Document33 pagesKushal Wod Final Report (Word File) (1) (1)siwashjoshi2No ratings yet

- BBS 4th Year Final WorkDocument48 pagesBBS 4th Year Final WorkNamuna Joshi88% (8)

- Sanjeeta MaharjanDocument50 pagesSanjeeta Maharjanbishnu paudelNo ratings yet

- Report 5Document31 pagesReport 5anshutaxpragatinagar2023No ratings yet

- BBS Report PDFDocument41 pagesBBS Report PDFRupak Gautam100% (1)

- 750146088-Binod-Project-Report-BBS-4th-Year-FinalDocument48 pages750146088-Binod-Project-Report-BBS-4th-Year-Finalmagardiwakar36No ratings yet

- Business Research Report For BBS Final Year of Roshan SahDocument42 pagesBusiness Research Report For BBS Final Year of Roshan Sahroshansah222901No ratings yet

- Analysis of Financial Performance of Everest Bank LimitedDocument54 pagesAnalysis of Financial Performance of Everest Bank LimitedSuresh Pangeni50% (2)

- Krit I ReportDocument55 pagesKrit I Reportprabeshchaudhary3No ratings yet

- Nic Asia Financial AnalysisDocument48 pagesNic Asia Financial Analysissanjiv pasmanNo ratings yet

- Comparative Financial Analysis of Commercial BankDocument61 pagesComparative Financial Analysis of Commercial Bankkamal KharelNo ratings yet

- business research report_for_BBS_final_year_of punaDocument51 pagesbusiness research report_for_BBS_final_year_of punaroshansah222901No ratings yet

- Report 2Document31 pagesReport 2anshutaxpragatinagar2023No ratings yet

- Lending Policy of Nepal Bank by Nabina RegmiDocument45 pagesLending Policy of Nepal Bank by Nabina RegmiKaran Pandey50% (2)

- Effect of Credit Risk On The Financial Performance of Nepalese Commercial Bank.Document40 pagesEffect of Credit Risk On The Financial Performance of Nepalese Commercial Bank.RJ RajvanshiNo ratings yet

- Project Work 5Document31 pagesProject Work 5anshutaxpragatinagar2023No ratings yet

- EDIT-sarjan-finnally-1 (1)Document43 pagesEDIT-sarjan-finnally-1 (1)hateyoui520No ratings yet

- Financial Analysis of Kumari Bank Limited 2022Document41 pagesFinancial Analysis of Kumari Bank Limited 2022Prajwola Gajurel100% (3)

- Summer Project ReportDocument55 pagesSummer Project ReportPuskar KhanalNo ratings yet

- Final ReportDocument49 pagesFinal Reportprabeshchaudhary3No ratings yet

- Bbs 4Document55 pagesBbs 4Sushant MaskeyNo ratings yet

- A Study On Marketing Strategy of Subisu Cablenet Pvt. LTDDocument9 pagesA Study On Marketing Strategy of Subisu Cablenet Pvt. LTDSaroj KhadkaNo ratings yet

- Project Work of Laxmi Bank.Document39 pagesProject Work of Laxmi Bank.Millionaire Mentality67% (3)

- Analysis of Liquidity and Profitability PDFDocument46 pagesAnalysis of Liquidity and Profitability PDFBadri mauryaNo ratings yet

- proposal reportDocument42 pagesproposal report3006sthasushanNo ratings yet

- Leading Piratic of Merged Commercial BanksDocument48 pagesLeading Piratic of Merged Commercial Bankslokendradhakal52No ratings yet

- Project Work 3Document31 pagesProject Work 3anshutaxpragatinagar2023No ratings yet

- Jivit Final Front PartDocument9 pagesJivit Final Front PartBikeshNo ratings yet

- Project Report Pratham_BBS 4th yearDocument54 pagesProject Report Pratham_BBS 4th yearbinuNo ratings yet

- Competency-Based Accounting Education, Training, and Certification: An Implementation GuideFrom EverandCompetency-Based Accounting Education, Training, and Certification: An Implementation GuideNo ratings yet

- Layout Er SuggestDocument1 pageLayout Er SuggestSushant MaskeyNo ratings yet

- Basundhara Tala ThapDocument2 pagesBasundhara Tala ThapSushant MaskeyNo ratings yet

- Bbs 4Document55 pagesBbs 4Sushant MaskeyNo ratings yet

- Exam Date: 2079-10-29 (2023-02-12) : IT Training Passed Out Student The Institute of Chartered Accountants of NepalDocument1 pageExam Date: 2079-10-29 (2023-02-12) : IT Training Passed Out Student The Institute of Chartered Accountants of NepalSushant MaskeyNo ratings yet

- 500 Question SetDocument72 pages500 Question SetSushant MaskeyNo ratings yet

- Exam Date: 2079-11-26 (2023-03-10) : IT Training Passed Out Student The Institute of Chartered Accountants of NepalDocument1 pageExam Date: 2079-11-26 (2023-03-10) : IT Training Passed Out Student The Institute of Chartered Accountants of NepalSushant MaskeyNo ratings yet

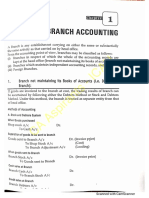

- Branch AccountingDocument51 pagesBranch AccountingSushant MaskeyNo ratings yet

- MS Word: Marks AllocationDocument1 pageMS Word: Marks AllocationSushant MaskeyNo ratings yet

- IT ResultDocument1 pageIT ResultSushant MaskeyNo ratings yet

- UntitledDocument72 pagesUntitledSushant MaskeyNo ratings yet

- Chapter 4: LeverageDocument15 pagesChapter 4: LeverageSushant MaskeyNo ratings yet

- Risk Return Basics/Portfolio Management: Learning Objective of The ChapterDocument34 pagesRisk Return Basics/Portfolio Management: Learning Objective of The ChapterSushant MaskeyNo ratings yet

- Budget AnswersDocument6 pagesBudget AnswersSushant MaskeyNo ratings yet

- Chapter 4: LeverageDocument15 pagesChapter 4: LeverageSushant MaskeyNo ratings yet

- Valn of CMN StockDocument18 pagesValn of CMN StockSushant Maskey0% (1)

- Cost of CapitalDocument37 pagesCost of CapitalSushant Maskey100% (1)

- Govt AuditingDocument12 pagesGovt AuditingSushant MaskeyNo ratings yet

- Overheads PracticalDocument37 pagesOverheads PracticalSushant Maskey100% (1)

- Capital StructureDocument31 pagesCapital StructureSushant Maskey100% (1)

- Labour/Employee Cost: Classification of Labor CostDocument9 pagesLabour/Employee Cost: Classification of Labor CostSushant MaskeyNo ratings yet

- Ican Revision Class - Bond Valuation (Cap-Ii) : Ca Rajendra Mangal Joshi 1Document16 pagesIcan Revision Class - Bond Valuation (Cap-Ii) : Ca Rajendra Mangal Joshi 1Sushant MaskeyNo ratings yet

- CAPII Suggested Dec2015Document87 pagesCAPII Suggested Dec2015Sushant MaskeyNo ratings yet

- EDP Audit CIS Environment MeaningDocument7 pagesEDP Audit CIS Environment MeaningSushant MaskeyNo ratings yet

- RD TReeqim RSFH XACz 0 W91617196460Document10 pagesRD TReeqim RSFH XACz 0 W91617196460Sushant MaskeyNo ratings yet

- NIOjid Akjc MDI9 L 5 Ulv I1617282937Document4 pagesNIOjid Akjc MDI9 L 5 Ulv I1617282937Sushant MaskeyNo ratings yet

- Labour: (A) (B) (C) (D) (E)Document40 pagesLabour: (A) (B) (C) (D) (E)Sushant Maskey100% (1)

- Budget & Budgetary ControlDocument15 pagesBudget & Budgetary ControlSushant MaskeyNo ratings yet

- Sapm - 2 MarksDocument17 pagesSapm - 2 MarksA Senthilkumar100% (3)

- Salary Backed Loan Application Form: DdmmyyyyDocument4 pagesSalary Backed Loan Application Form: Ddmmyyyynwabudefrank9No ratings yet

- PART III Financial LiabilitiesDocument3 pagesPART III Financial LiabilitiesMatteo VidottoNo ratings yet

- Class Discussion QuestionsDocument2 pagesClass Discussion Questionshank hillNo ratings yet

- ContractDocument22 pagesContractsakshi singhNo ratings yet

- Working Paper: The Ukraine Support Tracker: Which Countries Help Ukraine and How?Document58 pagesWorking Paper: The Ukraine Support Tracker: Which Countries Help Ukraine and How?Blitz bgNo ratings yet

- Credit Guarantee Corporation Malaysia Berhad Steering SME Development in MalaysiaDocument16 pagesCredit Guarantee Corporation Malaysia Berhad Steering SME Development in MalaysiaLi Jean TanNo ratings yet

- E BankingDocument11 pagesE BankingBalaraman Gnanam.sNo ratings yet

- ACC300 Final Exam Score 90%Document9 pagesACC300 Final Exam Score 90%G JhaNo ratings yet

- Sephora CSDocument4 pagesSephora CSAbhishek ShardaNo ratings yet

- 2132531t483700 Ratio Analysis Project ReportDocument139 pages2132531t483700 Ratio Analysis Project ReportAmanNo ratings yet

- The Financial Risk Manager (FRM®) CertificationDocument2 pagesThe Financial Risk Manager (FRM®) CertificationRonaldoNo ratings yet

- Pan Y, Tse D, 2000, The Hierarchical Model of Market Entry ModesDocument21 pagesPan Y, Tse D, 2000, The Hierarchical Model of Market Entry ModesGian Carlos Tarifeño SanchezNo ratings yet

- WB Historical Chronology 1944 2005Document424 pagesWB Historical Chronology 1944 2005Muhammad Badar Ismail DheendaNo ratings yet

- Businessstandardpaper PDFDocument18 pagesBusinessstandardpaper PDFAasha InugalaNo ratings yet

- LangDocument20 pagesLangHumberto anco lopezNo ratings yet

- Proposed Chart of Accounts-8Document62 pagesProposed Chart of Accounts-8Zimbo Kigo100% (1)

- BRM Assignment 07Document17 pagesBRM Assignment 07Sahan RodrigoNo ratings yet

- Lesson Plan Banking and Financial SkillsDocument9 pagesLesson Plan Banking and Financial SkillsBaiqtrie WidyaNo ratings yet

- Bank Loan Prediction Using Machine LearnDocument7 pagesBank Loan Prediction Using Machine Learnmonkey wiseNo ratings yet

- CORTEZ, Gracie Dan-ECEA119-B11-Case-Analysis-for-Group 2Document4 pagesCORTEZ, Gracie Dan-ECEA119-B11-Case-Analysis-for-Group 2sugar mamiNo ratings yet

- International Capital Markets - AnkurDocument24 pagesInternational Capital Markets - AnkurRaj K GahlotNo ratings yet

- Pest Analysis Sri LankaDocument8 pagesPest Analysis Sri LankaSai VasudevanNo ratings yet

- The Ratio (Interview Special) 10 Feb 2023Document21 pagesThe Ratio (Interview Special) 10 Feb 2023Niraj PatelNo ratings yet

Download as docx, pdf, or txt

You might also like

- Friedan Global Capitalism SummaryDocument23 pagesFriedan Global Capitalism Summaryboomroasted34100% (13)

- Profitability Analysis of Nabil Bank LTD 2022Document42 pagesProfitability Analysis of Nabil Bank LTD 2022Prajwola Gajurel83% (12)

- The History Behind The National Economic Security and ReformationAct (NESARA)Document21 pagesThe History Behind The National Economic Security and ReformationAct (NESARA)Eddie Winkler80% (5)

- 3.7: Cash Flow: Activity: AnubisDocument3 pages3.7: Cash Flow: Activity: AnubisJornarnod50% (4)

- URP Income Tax Part SolutionsDocument127 pagesURP Income Tax Part SolutionsSushant MaskeyNo ratings yet

- English-Danish DictionaryDocument94 pagesEnglish-Danish DictionaryRoyMarie100% (8)

- 15 Ways To Earn Money 2020 - The Money EquationDocument18 pages15 Ways To Earn Money 2020 - The Money EquationThe Money Equation100% (1)

- Scotiabank Case StudyDocument10 pagesScotiabank Case StudyAnkushNo ratings yet

- 2080bs Financial Performance Analysis of Standard Chartered Bank Nepal LTDDocument51 pages2080bs Financial Performance Analysis of Standard Chartered Bank Nepal LTDBikeshNo ratings yet

- Profitiability Analysis of Nabil Bank Limited: A Project Work ReportDocument39 pagesProfitiability Analysis of Nabil Bank Limited: A Project Work Reportaakash shresthaNo ratings yet

- Profitability Analysis of Standard Charted Bank Nepal LimitedDocument41 pagesProfitability Analysis of Standard Charted Bank Nepal LimitedAnjal Shrestha100% (1)

- Bikesh FinalDocument47 pagesBikesh FinalBikeshNo ratings yet

- business research report_bbs of samir tamangDocument39 pagesbusiness research report_bbs of samir tamangroshansah222901No ratings yet

- 633396592-credit-management-of-nabil-bankDocument46 pages633396592-credit-management-of-nabil-bankmagardiwakar36No ratings yet

- Credit Management of Nabil BankDocument46 pagesCredit Management of Nabil BankNijan Jyakhwo100% (1)

- final-report nic asiaDocument48 pagesfinal-report nic asiasanjiv pasmanNo ratings yet

- 747786128 Final Report Nic AsiaDocument48 pages747786128 Final Report Nic Asiamagardiwakar36No ratings yet

- Heading of Report PDFDocument10 pagesHeading of Report PDFB safe nirman and suppliers pvt. ltd.No ratings yet

- Research Report of Bodh Kumar Thapa FinalDocument47 pagesResearch Report of Bodh Kumar Thapa FinalvectopgraphicNo ratings yet

- A study of loan management of nepal bank limitedDocument42 pagesA study of loan management of nepal bank limitedBikeshNo ratings yet

- Final Year Report of BBS 4th YearDocument49 pagesFinal Year Report of BBS 4th Yearnepalfinance987100% (2)

- Analysis of Working Capital Management of Machhapuchhre Bank LTDDocument41 pagesAnalysis of Working Capital Management of Machhapuchhre Bank LTDshresthanikhil078No ratings yet

- Liquidity and Profitability Analysis of Nabil Bank LimitedDocument37 pagesLiquidity and Profitability Analysis of Nabil Bank LimitedDeep Meditation100% (4)

- Toaz.info Bbs 4th Year Final Work Pr Da9ca60c8f9195a9c5c2c2cba0971b8eDocument48 pagesToaz.info Bbs 4th Year Final Work Pr Da9ca60c8f9195a9c5c2c2cba0971b8emangar2059No ratings yet

- Loan Management of Agriculture Development BankDocument36 pagesLoan Management of Agriculture Development BankanisheshkNo ratings yet

- Nabil ProfitabilityDocument44 pagesNabil Profitabilityabhishek shah100% (2)

- BBS ReportDocument49 pagesBBS ReportRaz BinadiNo ratings yet

- Ashik Final Report LatestDocument45 pagesAshik Final Report Latestashikdai55No ratings yet

- ThesisDocument35 pagesThesisAvinash De Monster DeulaNo ratings yet

- BBS Final Year ProjectDocument39 pagesBBS Final Year ProjectSamsher Kunwar100% (2)

- Effects of Credit Risk On The Financial Performance of Nepalese Commercial BanksDocument46 pagesEffects of Credit Risk On The Financial Performance of Nepalese Commercial BanksSasmina DahalNo ratings yet

- Project Work Sample - Sushila SilwalDocument48 pagesProject Work Sample - Sushila SilwalRam Prasad SilwalNo ratings yet

- Analysis of The Loan Provided by Citizen Bank Limited: A Project Work ReportDocument34 pagesAnalysis of The Loan Provided by Citizen Bank Limited: A Project Work ReportHem Raj JoshiNo ratings yet

- Report Bina FinalDocument36 pagesReport Bina FinalNxl AmikNo ratings yet

- Ajay BasnetDocument38 pagesAjay BasnetInternship ReportNo ratings yet

- Kushal Wod Final Report (Word File) (1) (1)Document33 pagesKushal Wod Final Report (Word File) (1) (1)siwashjoshi2No ratings yet

- BBS 4th Year Final WorkDocument48 pagesBBS 4th Year Final WorkNamuna Joshi88% (8)

- Sanjeeta MaharjanDocument50 pagesSanjeeta Maharjanbishnu paudelNo ratings yet

- Report 5Document31 pagesReport 5anshutaxpragatinagar2023No ratings yet

- BBS Report PDFDocument41 pagesBBS Report PDFRupak Gautam100% (1)

- 750146088-Binod-Project-Report-BBS-4th-Year-FinalDocument48 pages750146088-Binod-Project-Report-BBS-4th-Year-Finalmagardiwakar36No ratings yet

- Business Research Report For BBS Final Year of Roshan SahDocument42 pagesBusiness Research Report For BBS Final Year of Roshan Sahroshansah222901No ratings yet

- Analysis of Financial Performance of Everest Bank LimitedDocument54 pagesAnalysis of Financial Performance of Everest Bank LimitedSuresh Pangeni50% (2)

- Krit I ReportDocument55 pagesKrit I Reportprabeshchaudhary3No ratings yet

- Nic Asia Financial AnalysisDocument48 pagesNic Asia Financial Analysissanjiv pasmanNo ratings yet

- Comparative Financial Analysis of Commercial BankDocument61 pagesComparative Financial Analysis of Commercial Bankkamal KharelNo ratings yet

- business research report_for_BBS_final_year_of punaDocument51 pagesbusiness research report_for_BBS_final_year_of punaroshansah222901No ratings yet

- Report 2Document31 pagesReport 2anshutaxpragatinagar2023No ratings yet

- Lending Policy of Nepal Bank by Nabina RegmiDocument45 pagesLending Policy of Nepal Bank by Nabina RegmiKaran Pandey50% (2)

- Effect of Credit Risk On The Financial Performance of Nepalese Commercial Bank.Document40 pagesEffect of Credit Risk On The Financial Performance of Nepalese Commercial Bank.RJ RajvanshiNo ratings yet

- Project Work 5Document31 pagesProject Work 5anshutaxpragatinagar2023No ratings yet

- EDIT-sarjan-finnally-1 (1)Document43 pagesEDIT-sarjan-finnally-1 (1)hateyoui520No ratings yet

- Financial Analysis of Kumari Bank Limited 2022Document41 pagesFinancial Analysis of Kumari Bank Limited 2022Prajwola Gajurel100% (3)

- Summer Project ReportDocument55 pagesSummer Project ReportPuskar KhanalNo ratings yet

- Final ReportDocument49 pagesFinal Reportprabeshchaudhary3No ratings yet

- Bbs 4Document55 pagesBbs 4Sushant MaskeyNo ratings yet

- A Study On Marketing Strategy of Subisu Cablenet Pvt. LTDDocument9 pagesA Study On Marketing Strategy of Subisu Cablenet Pvt. LTDSaroj KhadkaNo ratings yet

- Project Work of Laxmi Bank.Document39 pagesProject Work of Laxmi Bank.Millionaire Mentality67% (3)

- Analysis of Liquidity and Profitability PDFDocument46 pagesAnalysis of Liquidity and Profitability PDFBadri mauryaNo ratings yet

- proposal reportDocument42 pagesproposal report3006sthasushanNo ratings yet

- Leading Piratic of Merged Commercial BanksDocument48 pagesLeading Piratic of Merged Commercial Bankslokendradhakal52No ratings yet

- Project Work 3Document31 pagesProject Work 3anshutaxpragatinagar2023No ratings yet

- Jivit Final Front PartDocument9 pagesJivit Final Front PartBikeshNo ratings yet

- Project Report Pratham_BBS 4th yearDocument54 pagesProject Report Pratham_BBS 4th yearbinuNo ratings yet

- Competency-Based Accounting Education, Training, and Certification: An Implementation GuideFrom EverandCompetency-Based Accounting Education, Training, and Certification: An Implementation GuideNo ratings yet

- Layout Er SuggestDocument1 pageLayout Er SuggestSushant MaskeyNo ratings yet

- Basundhara Tala ThapDocument2 pagesBasundhara Tala ThapSushant MaskeyNo ratings yet

- Bbs 4Document55 pagesBbs 4Sushant MaskeyNo ratings yet

- Exam Date: 2079-10-29 (2023-02-12) : IT Training Passed Out Student The Institute of Chartered Accountants of NepalDocument1 pageExam Date: 2079-10-29 (2023-02-12) : IT Training Passed Out Student The Institute of Chartered Accountants of NepalSushant MaskeyNo ratings yet

- 500 Question SetDocument72 pages500 Question SetSushant MaskeyNo ratings yet

- Exam Date: 2079-11-26 (2023-03-10) : IT Training Passed Out Student The Institute of Chartered Accountants of NepalDocument1 pageExam Date: 2079-11-26 (2023-03-10) : IT Training Passed Out Student The Institute of Chartered Accountants of NepalSushant MaskeyNo ratings yet

- Branch AccountingDocument51 pagesBranch AccountingSushant MaskeyNo ratings yet

- MS Word: Marks AllocationDocument1 pageMS Word: Marks AllocationSushant MaskeyNo ratings yet

- IT ResultDocument1 pageIT ResultSushant MaskeyNo ratings yet

- UntitledDocument72 pagesUntitledSushant MaskeyNo ratings yet

- Chapter 4: LeverageDocument15 pagesChapter 4: LeverageSushant MaskeyNo ratings yet

- Risk Return Basics/Portfolio Management: Learning Objective of The ChapterDocument34 pagesRisk Return Basics/Portfolio Management: Learning Objective of The ChapterSushant MaskeyNo ratings yet

- Budget AnswersDocument6 pagesBudget AnswersSushant MaskeyNo ratings yet

- Chapter 4: LeverageDocument15 pagesChapter 4: LeverageSushant MaskeyNo ratings yet

- Valn of CMN StockDocument18 pagesValn of CMN StockSushant Maskey0% (1)

- Cost of CapitalDocument37 pagesCost of CapitalSushant Maskey100% (1)

- Govt AuditingDocument12 pagesGovt AuditingSushant MaskeyNo ratings yet

- Overheads PracticalDocument37 pagesOverheads PracticalSushant Maskey100% (1)

- Capital StructureDocument31 pagesCapital StructureSushant Maskey100% (1)

- Labour/Employee Cost: Classification of Labor CostDocument9 pagesLabour/Employee Cost: Classification of Labor CostSushant MaskeyNo ratings yet

- Ican Revision Class - Bond Valuation (Cap-Ii) : Ca Rajendra Mangal Joshi 1Document16 pagesIcan Revision Class - Bond Valuation (Cap-Ii) : Ca Rajendra Mangal Joshi 1Sushant MaskeyNo ratings yet

- CAPII Suggested Dec2015Document87 pagesCAPII Suggested Dec2015Sushant MaskeyNo ratings yet

- EDP Audit CIS Environment MeaningDocument7 pagesEDP Audit CIS Environment MeaningSushant MaskeyNo ratings yet

- RD TReeqim RSFH XACz 0 W91617196460Document10 pagesRD TReeqim RSFH XACz 0 W91617196460Sushant MaskeyNo ratings yet

- NIOjid Akjc MDI9 L 5 Ulv I1617282937Document4 pagesNIOjid Akjc MDI9 L 5 Ulv I1617282937Sushant MaskeyNo ratings yet

- Labour: (A) (B) (C) (D) (E)Document40 pagesLabour: (A) (B) (C) (D) (E)Sushant Maskey100% (1)

- Budget & Budgetary ControlDocument15 pagesBudget & Budgetary ControlSushant MaskeyNo ratings yet

- Sapm - 2 MarksDocument17 pagesSapm - 2 MarksA Senthilkumar100% (3)

- Salary Backed Loan Application Form: DdmmyyyyDocument4 pagesSalary Backed Loan Application Form: Ddmmyyyynwabudefrank9No ratings yet

- PART III Financial LiabilitiesDocument3 pagesPART III Financial LiabilitiesMatteo VidottoNo ratings yet

- Class Discussion QuestionsDocument2 pagesClass Discussion Questionshank hillNo ratings yet

- ContractDocument22 pagesContractsakshi singhNo ratings yet

- Working Paper: The Ukraine Support Tracker: Which Countries Help Ukraine and How?Document58 pagesWorking Paper: The Ukraine Support Tracker: Which Countries Help Ukraine and How?Blitz bgNo ratings yet

- Credit Guarantee Corporation Malaysia Berhad Steering SME Development in MalaysiaDocument16 pagesCredit Guarantee Corporation Malaysia Berhad Steering SME Development in MalaysiaLi Jean TanNo ratings yet

- E BankingDocument11 pagesE BankingBalaraman Gnanam.sNo ratings yet

- ACC300 Final Exam Score 90%Document9 pagesACC300 Final Exam Score 90%G JhaNo ratings yet

- Sephora CSDocument4 pagesSephora CSAbhishek ShardaNo ratings yet

- 2132531t483700 Ratio Analysis Project ReportDocument139 pages2132531t483700 Ratio Analysis Project ReportAmanNo ratings yet

- The Financial Risk Manager (FRM®) CertificationDocument2 pagesThe Financial Risk Manager (FRM®) CertificationRonaldoNo ratings yet

- Pan Y, Tse D, 2000, The Hierarchical Model of Market Entry ModesDocument21 pagesPan Y, Tse D, 2000, The Hierarchical Model of Market Entry ModesGian Carlos Tarifeño SanchezNo ratings yet

- WB Historical Chronology 1944 2005Document424 pagesWB Historical Chronology 1944 2005Muhammad Badar Ismail DheendaNo ratings yet

- Businessstandardpaper PDFDocument18 pagesBusinessstandardpaper PDFAasha InugalaNo ratings yet

- LangDocument20 pagesLangHumberto anco lopezNo ratings yet

- Proposed Chart of Accounts-8Document62 pagesProposed Chart of Accounts-8Zimbo Kigo100% (1)

- BRM Assignment 07Document17 pagesBRM Assignment 07Sahan RodrigoNo ratings yet

- Lesson Plan Banking and Financial SkillsDocument9 pagesLesson Plan Banking and Financial SkillsBaiqtrie WidyaNo ratings yet

- Bank Loan Prediction Using Machine LearnDocument7 pagesBank Loan Prediction Using Machine Learnmonkey wiseNo ratings yet

- CORTEZ, Gracie Dan-ECEA119-B11-Case-Analysis-for-Group 2Document4 pagesCORTEZ, Gracie Dan-ECEA119-B11-Case-Analysis-for-Group 2sugar mamiNo ratings yet

- International Capital Markets - AnkurDocument24 pagesInternational Capital Markets - AnkurRaj K GahlotNo ratings yet

- Pest Analysis Sri LankaDocument8 pagesPest Analysis Sri LankaSai VasudevanNo ratings yet

- The Ratio (Interview Special) 10 Feb 2023Document21 pagesThe Ratio (Interview Special) 10 Feb 2023Niraj PatelNo ratings yet