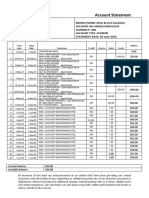

Copy of FARAP-4501 (Cash and Cash Equivalents)

Copy of FARAP-4501 (Cash and Cash Equivalents)

You might also like

- Gold Dust Draft ContractDocument12 pagesGold Dust Draft Contractflashpoint201150% (2)

- Afghan United Bank Statement SDocument2 pagesAfghan United Bank Statement SAbdulrahim khan100% (1)

- Actg6146 ReviewerDocument21 pagesActg6146 ReviewerRegine Vega100% (1)

- FARAP-4501 (Cash and Cash Equivalents)Document10 pagesFARAP-4501 (Cash and Cash Equivalents)Marya NvlzNo ratings yet

- Cash and Cash Equi Theories and ProblemsDocument29 pagesCash and Cash Equi Theories and ProblemsIris Mnemosyne100% (5)

- SsqytDocument234 pagesSsqytsaeed hiderNo ratings yet

- Jamals Black Book PDFDocument82 pagesJamals Black Book PDFShaikh awais100% (6)

- JP - Bank EBS Requiuirement Sheet ConfigDocument37 pagesJP - Bank EBS Requiuirement Sheet ConfigSahil SinhaNo ratings yet

- MT103Document6 pagesMT103wisnu ipasarNo ratings yet

- 03 - Cash & Cash Equivalents - TheoryDocument2 pages03 - Cash & Cash Equivalents - TheoryROMAR A. PIGANo ratings yet

- Cash and Cash Equivalent TheoryDocument1 pageCash and Cash Equivalent TheoryExcelsia Grace A. ParreñoNo ratings yet

- BSA REVIEW Cash TheoriesDocument4 pagesBSA REVIEW Cash TheorieschristineNo ratings yet

- Seatwork 1Document6 pagesSeatwork 1Danna VargasNo ratings yet

- Quiz 1Document9 pagesQuiz 1Czarhiena SantiagoNo ratings yet

- Assignment Mo BoboDocument5 pagesAssignment Mo BoboRommel Cabel CapalaranNo ratings yet

- Which of The Following Should Not Be Considered CashDocument5 pagesWhich of The Following Should Not Be Considered CashErica FlorentinoNo ratings yet

- Aaconapps2 03RHDocument12 pagesAaconapps2 03RHAngelica DizonNo ratings yet

- 01 - Cash and Cash Equivalents - RM - Rev2023 24Document3 pages01 - Cash and Cash Equivalents - RM - Rev2023 24pilonia.donitarosebsa1993No ratings yet

- Seatwork 1Document6 pagesSeatwork 1Danna VargasNo ratings yet

- 1 CashDocument6 pages1 CashMikaella SaduralNo ratings yet

- Theory of Accounts Cash and Cash EquivalentsDocument15 pagesTheory of Accounts Cash and Cash EquivalentsAuroraNo ratings yet

- Financial Accounting and Reporting University of Luzon Cash and Cash Equivalents College of AccountancyDocument8 pagesFinancial Accounting and Reporting University of Luzon Cash and Cash Equivalents College of AccountancyJamhel MarquezNo ratings yet

- Conceptual Framework & Accounting Standards: Northeastern CollegeDocument5 pagesConceptual Framework & Accounting Standards: Northeastern CollegeMikaella SaduralNo ratings yet

- ACC 205 TheoriesDocument9 pagesACC 205 TheoriesCASSANDRANo ratings yet

- Updates in Financial Reporting Standards: Northeastern CollegeDocument3 pagesUpdates in Financial Reporting Standards: Northeastern CollegeJobelle Grace SorianoNo ratings yet

- DocxDocument10 pagesDocxYukiNo ratings yet

- Review 105 - Day 5 Theory of AccountsDocument12 pagesReview 105 - Day 5 Theory of Accountschristine anglaNo ratings yet

- Quiz On Cash Ga TheoriesDocument5 pagesQuiz On Cash Ga TheoriesgarciarhodjeannemarthaNo ratings yet

- ALYSSA SUMMARYDocument2 pagesALYSSA SUMMARYAlyssa M. JamilNo ratings yet

- CCE BankRecon POCDocument3 pagesCCE BankRecon POCgamboamaeganNo ratings yet

- Financial Accounting 1Document35 pagesFinancial Accounting 1Bunbun 221No ratings yet

- SolutionsDocument25 pagesSolutionsDante Jr. Dela Cruz100% (1)

- Substantiv Aud For CashDocument3 pagesSubstantiv Aud For CashJane Ruby JennieferNo ratings yet

- Review 105 - Day 5 Theory of AccountsDocument12 pagesReview 105 - Day 5 Theory of AccountsAndre PulancoNo ratings yet

- Review 105 - Day 5 Theory of AccountsDocument12 pagesReview 105 - Day 5 Theory of Accountsneo14No ratings yet

- Cash and Cash EquivalentsDocument4 pagesCash and Cash EquivalentsDessa GarongNo ratings yet

- Acctg 100C 01Document6 pagesAcctg 100C 01Jose Magallanes100% (1)

- C&CEDocument11 pagesC&CEAnne VinuyaNo ratings yet

- Cash Items ReviewerDocument49 pagesCash Items ReviewerlalalalaNo ratings yet

- Cash and Cash Equivalents TheoriesDocument5 pagesCash and Cash Equivalents Theoriesjane dillanNo ratings yet

- F 51124304Document3 pagesF 51124304hanamay_07No ratings yet

- 11 ACCT 1AB CashDocument17 pages11 ACCT 1AB CashJustLike JeloNo ratings yet

- Intermediate Accounting TheoryDocument34 pagesIntermediate Accounting TheoryRizza Christine Thereza Usbal0% (1)

- This Study Resource Was: Financial Accounting Review (Theory)Document7 pagesThis Study Resource Was: Financial Accounting Review (Theory)LianaNo ratings yet

- Petty CashDocument1 pagePetty CashRose Marie Anne ReyesNo ratings yet

- Cash and Cash Equivalents ExamDocument7 pagesCash and Cash Equivalents ExamRudydanvinz BernardoNo ratings yet

- AP.2904 - Cash and Cash Equivalents.Document7 pagesAP.2904 - Cash and Cash Equivalents.Eyes Saw0% (1)

- Cash and Cash EquivalentsDocument5 pagesCash and Cash EquivalentsSarah CaballeroNo ratings yet

- Handout - CashDocument17 pagesHandout - CashPenelope PalconNo ratings yet

- 2 - Cash and Cash EquivalentsDocument5 pages2 - Cash and Cash EquivalentsandreamrieNo ratings yet

- Quiz No. 06: Financial InstrumentsDocument2 pagesQuiz No. 06: Financial InstrumentsPHI NGUYEN HOANGNo ratings yet

- Problem Solving (With Answers)Document12 pagesProblem Solving (With Answers)sunflower100% (1)

- Theory of Accounts Cash and Cash EquivalentsDocument9 pagesTheory of Accounts Cash and Cash Equivalentsida_takahashi43% (14)

- Which Is Called As 'Part-Time Banking Outlet'?: Bank Po/ Clerks Exam SpecialDocument1 pageWhich Is Called As 'Part-Time Banking Outlet'?: Bank Po/ Clerks Exam SpecialSrikanth Harinadh BNo ratings yet

- Cash and Cash Equivalents, Bank Reconciliation, and Proof of CashDocument8 pagesCash and Cash Equivalents, Bank Reconciliation, and Proof of CashMichaelNo ratings yet

- AllreviewerDocument127 pagesAllreviewerRoyu BreakerNo ratings yet

- Inter Acctg Midterms 1Document4 pagesInter Acctg Midterms 1Jorie MeroyNo ratings yet

- AP.3404 Audit of Cash and Cash EquivalentsDocument5 pagesAP.3404 Audit of Cash and Cash EquivalentsMonica GarciaNo ratings yet

- CashDocument3 pagesCashAnne VinuyaNo ratings yet

- Q1 SMEsDocument6 pagesQ1 SMEsJennifer RasonabeNo ratings yet

- Test Bank Far 3 Cpar PDFDocument24 pagesTest Bank Far 3 Cpar PDFRommel Monfiel100% (1)

- Cash and Cash Equivalents - TheoryDocument4 pagesCash and Cash Equivalents - TheoryRandy FigueroaNo ratings yet

- Audit of Cash PDFDocument11 pagesAudit of Cash PDFRyan Prado AndayaNo ratings yet

- 6 - Cash Flow StatementDocument42 pages6 - Cash Flow StatementBhagaban DasNo ratings yet

- Copy of MS-02 (Cost Behavior with Regression Analysis) (1)Document7 pagesCopy of MS-02 (Cost Behavior with Regression Analysis) (1)Accounting StuffNo ratings yet

- FARAP-4520Document7 pagesFARAP-4520Accounting StuffNo ratings yet

- FARAP-4517Document4 pagesFARAP-4517Accounting StuffNo ratings yet

- FARAP-4519Document4 pagesFARAP-4519Accounting StuffNo ratings yet

- FARAP-4516Document10 pagesFARAP-4516Accounting StuffNo ratings yet

- PHIL283 Diagram 2Document4 pagesPHIL283 Diagram 2Accounting StuffNo ratings yet

- The Determinates of Selecting Accounting Software: A Proposed ModelDocument26 pagesThe Determinates of Selecting Accounting Software: A Proposed ModelAccounting StuffNo ratings yet

- PHIL283 Answers 5Document2 pagesPHIL283 Answers 5Accounting StuffNo ratings yet

- Provident FundDocument9 pagesProvident FundYogesh KandariNo ratings yet

- Hachi HO2006000012712Document1 pageHachi HO2006000012712guojun sunNo ratings yet

- Practicepdf 1Document88 pagesPracticepdf 1mhoddi100% (1)

- Asistensi PE 2 - Pertemuan 6Document51 pagesAsistensi PE 2 - Pertemuan 6qonitahmutNo ratings yet

- Problem 1 1245Document3 pagesProblem 1 1245Rhanda BernardoNo ratings yet

- Calculate IRR in ExcelDocument2 pagesCalculate IRR in Excelrahulchutia100% (1)

- CH 10 SM FinalcaDocument55 pagesCH 10 SM FinalcaDania Sekar WuryandariNo ratings yet

- Audit Report Sindh Agriculture University Tandojam, SindhDocument63 pagesAudit Report Sindh Agriculture University Tandojam, Sindhsadaf_183100% (1)

- 2010 ACE Limited Annual ReportDocument233 pages2010 ACE Limited Annual ReportACELitigationWatchNo ratings yet

- Independent Auditor's ReportDocument3 pagesIndependent Auditor's ReportNyra Beldoro100% (1)

- Preface: of Public Sector and Private Sector Banks"Document47 pagesPreface: of Public Sector and Private Sector Banks"madhuri100% (1)

- 1529302103778Document6 pages1529302103778Bibhuranjan MohantaNo ratings yet

- The Singapore Property Beginner S GuideDocument39 pagesThe Singapore Property Beginner S GuideCaleb LeeNo ratings yet

- A Study of Consumer Behaviour in Relation To Insurance Products in IDBI Federal LifeDocument42 pagesA Study of Consumer Behaviour in Relation To Insurance Products in IDBI Federal LifeAshu Agarwal0% (2)

- Account Receivable PresentationDocument34 pagesAccount Receivable PresentationYakub Immanuel SaputraNo ratings yet

- Mauricio Ramirez - OTM Implementation Best PracticesDocument21 pagesMauricio Ramirez - OTM Implementation Best PracticesdbahanyNo ratings yet

- Bank Reconciliation Statement in SAPDocument8 pagesBank Reconciliation Statement in SAPcharanNo ratings yet

- Please Confirm To ContinueDocument4 pagesPlease Confirm To ContinueMahakaal Digital PointNo ratings yet

- Shipping Maritime AbbreviationsDocument22 pagesShipping Maritime Abbreviationsteo_bozo5589No ratings yet

- Body of NBL-FexDocument76 pagesBody of NBL-FexIshrat JahanNo ratings yet

- Public Auction: 15 OCT 2019, 9.30amDocument1 pagePublic Auction: 15 OCT 2019, 9.30amchek86351No ratings yet

- Fee Information Document: General Account ServicesDocument7 pagesFee Information Document: General Account Servicesdaryl30011996No ratings yet

- HaiDocument20 pagesHaikuku's entertainmentNo ratings yet

- CA Solar Share 529 ProgramDocument72 pagesCA Solar Share 529 Programd_fanthamNo ratings yet

Download as xlsx, pdf, or txt

You might also like

- Gold Dust Draft ContractDocument12 pagesGold Dust Draft Contractflashpoint201150% (2)

- Afghan United Bank Statement SDocument2 pagesAfghan United Bank Statement SAbdulrahim khan100% (1)

- Actg6146 ReviewerDocument21 pagesActg6146 ReviewerRegine Vega100% (1)

- FARAP-4501 (Cash and Cash Equivalents)Document10 pagesFARAP-4501 (Cash and Cash Equivalents)Marya NvlzNo ratings yet

- Cash and Cash Equi Theories and ProblemsDocument29 pagesCash and Cash Equi Theories and ProblemsIris Mnemosyne100% (5)

- SsqytDocument234 pagesSsqytsaeed hiderNo ratings yet

- Jamals Black Book PDFDocument82 pagesJamals Black Book PDFShaikh awais100% (6)

- JP - Bank EBS Requiuirement Sheet ConfigDocument37 pagesJP - Bank EBS Requiuirement Sheet ConfigSahil SinhaNo ratings yet

- MT103Document6 pagesMT103wisnu ipasarNo ratings yet

- 03 - Cash & Cash Equivalents - TheoryDocument2 pages03 - Cash & Cash Equivalents - TheoryROMAR A. PIGANo ratings yet

- Cash and Cash Equivalent TheoryDocument1 pageCash and Cash Equivalent TheoryExcelsia Grace A. ParreñoNo ratings yet

- BSA REVIEW Cash TheoriesDocument4 pagesBSA REVIEW Cash TheorieschristineNo ratings yet

- Seatwork 1Document6 pagesSeatwork 1Danna VargasNo ratings yet

- Quiz 1Document9 pagesQuiz 1Czarhiena SantiagoNo ratings yet

- Assignment Mo BoboDocument5 pagesAssignment Mo BoboRommel Cabel CapalaranNo ratings yet

- Which of The Following Should Not Be Considered CashDocument5 pagesWhich of The Following Should Not Be Considered CashErica FlorentinoNo ratings yet

- Aaconapps2 03RHDocument12 pagesAaconapps2 03RHAngelica DizonNo ratings yet

- 01 - Cash and Cash Equivalents - RM - Rev2023 24Document3 pages01 - Cash and Cash Equivalents - RM - Rev2023 24pilonia.donitarosebsa1993No ratings yet

- Seatwork 1Document6 pagesSeatwork 1Danna VargasNo ratings yet

- 1 CashDocument6 pages1 CashMikaella SaduralNo ratings yet

- Theory of Accounts Cash and Cash EquivalentsDocument15 pagesTheory of Accounts Cash and Cash EquivalentsAuroraNo ratings yet

- Financial Accounting and Reporting University of Luzon Cash and Cash Equivalents College of AccountancyDocument8 pagesFinancial Accounting and Reporting University of Luzon Cash and Cash Equivalents College of AccountancyJamhel MarquezNo ratings yet

- Conceptual Framework & Accounting Standards: Northeastern CollegeDocument5 pagesConceptual Framework & Accounting Standards: Northeastern CollegeMikaella SaduralNo ratings yet

- ACC 205 TheoriesDocument9 pagesACC 205 TheoriesCASSANDRANo ratings yet

- Updates in Financial Reporting Standards: Northeastern CollegeDocument3 pagesUpdates in Financial Reporting Standards: Northeastern CollegeJobelle Grace SorianoNo ratings yet

- DocxDocument10 pagesDocxYukiNo ratings yet

- Review 105 - Day 5 Theory of AccountsDocument12 pagesReview 105 - Day 5 Theory of Accountschristine anglaNo ratings yet

- Quiz On Cash Ga TheoriesDocument5 pagesQuiz On Cash Ga TheoriesgarciarhodjeannemarthaNo ratings yet

- ALYSSA SUMMARYDocument2 pagesALYSSA SUMMARYAlyssa M. JamilNo ratings yet

- CCE BankRecon POCDocument3 pagesCCE BankRecon POCgamboamaeganNo ratings yet

- Financial Accounting 1Document35 pagesFinancial Accounting 1Bunbun 221No ratings yet

- SolutionsDocument25 pagesSolutionsDante Jr. Dela Cruz100% (1)

- Substantiv Aud For CashDocument3 pagesSubstantiv Aud For CashJane Ruby JennieferNo ratings yet

- Review 105 - Day 5 Theory of AccountsDocument12 pagesReview 105 - Day 5 Theory of AccountsAndre PulancoNo ratings yet

- Review 105 - Day 5 Theory of AccountsDocument12 pagesReview 105 - Day 5 Theory of Accountsneo14No ratings yet

- Cash and Cash EquivalentsDocument4 pagesCash and Cash EquivalentsDessa GarongNo ratings yet

- Acctg 100C 01Document6 pagesAcctg 100C 01Jose Magallanes100% (1)

- C&CEDocument11 pagesC&CEAnne VinuyaNo ratings yet

- Cash Items ReviewerDocument49 pagesCash Items ReviewerlalalalaNo ratings yet

- Cash and Cash Equivalents TheoriesDocument5 pagesCash and Cash Equivalents Theoriesjane dillanNo ratings yet

- F 51124304Document3 pagesF 51124304hanamay_07No ratings yet

- 11 ACCT 1AB CashDocument17 pages11 ACCT 1AB CashJustLike JeloNo ratings yet

- Intermediate Accounting TheoryDocument34 pagesIntermediate Accounting TheoryRizza Christine Thereza Usbal0% (1)

- This Study Resource Was: Financial Accounting Review (Theory)Document7 pagesThis Study Resource Was: Financial Accounting Review (Theory)LianaNo ratings yet

- Petty CashDocument1 pagePetty CashRose Marie Anne ReyesNo ratings yet

- Cash and Cash Equivalents ExamDocument7 pagesCash and Cash Equivalents ExamRudydanvinz BernardoNo ratings yet

- AP.2904 - Cash and Cash Equivalents.Document7 pagesAP.2904 - Cash and Cash Equivalents.Eyes Saw0% (1)

- Cash and Cash EquivalentsDocument5 pagesCash and Cash EquivalentsSarah CaballeroNo ratings yet

- Handout - CashDocument17 pagesHandout - CashPenelope PalconNo ratings yet

- 2 - Cash and Cash EquivalentsDocument5 pages2 - Cash and Cash EquivalentsandreamrieNo ratings yet

- Quiz No. 06: Financial InstrumentsDocument2 pagesQuiz No. 06: Financial InstrumentsPHI NGUYEN HOANGNo ratings yet

- Problem Solving (With Answers)Document12 pagesProblem Solving (With Answers)sunflower100% (1)

- Theory of Accounts Cash and Cash EquivalentsDocument9 pagesTheory of Accounts Cash and Cash Equivalentsida_takahashi43% (14)

- Which Is Called As 'Part-Time Banking Outlet'?: Bank Po/ Clerks Exam SpecialDocument1 pageWhich Is Called As 'Part-Time Banking Outlet'?: Bank Po/ Clerks Exam SpecialSrikanth Harinadh BNo ratings yet

- Cash and Cash Equivalents, Bank Reconciliation, and Proof of CashDocument8 pagesCash and Cash Equivalents, Bank Reconciliation, and Proof of CashMichaelNo ratings yet

- AllreviewerDocument127 pagesAllreviewerRoyu BreakerNo ratings yet

- Inter Acctg Midterms 1Document4 pagesInter Acctg Midterms 1Jorie MeroyNo ratings yet

- AP.3404 Audit of Cash and Cash EquivalentsDocument5 pagesAP.3404 Audit of Cash and Cash EquivalentsMonica GarciaNo ratings yet

- CashDocument3 pagesCashAnne VinuyaNo ratings yet

- Q1 SMEsDocument6 pagesQ1 SMEsJennifer RasonabeNo ratings yet

- Test Bank Far 3 Cpar PDFDocument24 pagesTest Bank Far 3 Cpar PDFRommel Monfiel100% (1)

- Cash and Cash Equivalents - TheoryDocument4 pagesCash and Cash Equivalents - TheoryRandy FigueroaNo ratings yet

- Audit of Cash PDFDocument11 pagesAudit of Cash PDFRyan Prado AndayaNo ratings yet

- 6 - Cash Flow StatementDocument42 pages6 - Cash Flow StatementBhagaban DasNo ratings yet

- Copy of MS-02 (Cost Behavior with Regression Analysis) (1)Document7 pagesCopy of MS-02 (Cost Behavior with Regression Analysis) (1)Accounting StuffNo ratings yet

- FARAP-4520Document7 pagesFARAP-4520Accounting StuffNo ratings yet

- FARAP-4517Document4 pagesFARAP-4517Accounting StuffNo ratings yet

- FARAP-4519Document4 pagesFARAP-4519Accounting StuffNo ratings yet

- FARAP-4516Document10 pagesFARAP-4516Accounting StuffNo ratings yet

- PHIL283 Diagram 2Document4 pagesPHIL283 Diagram 2Accounting StuffNo ratings yet

- The Determinates of Selecting Accounting Software: A Proposed ModelDocument26 pagesThe Determinates of Selecting Accounting Software: A Proposed ModelAccounting StuffNo ratings yet

- PHIL283 Answers 5Document2 pagesPHIL283 Answers 5Accounting StuffNo ratings yet

- Provident FundDocument9 pagesProvident FundYogesh KandariNo ratings yet

- Hachi HO2006000012712Document1 pageHachi HO2006000012712guojun sunNo ratings yet

- Practicepdf 1Document88 pagesPracticepdf 1mhoddi100% (1)

- Asistensi PE 2 - Pertemuan 6Document51 pagesAsistensi PE 2 - Pertemuan 6qonitahmutNo ratings yet

- Problem 1 1245Document3 pagesProblem 1 1245Rhanda BernardoNo ratings yet

- Calculate IRR in ExcelDocument2 pagesCalculate IRR in Excelrahulchutia100% (1)

- CH 10 SM FinalcaDocument55 pagesCH 10 SM FinalcaDania Sekar WuryandariNo ratings yet

- Audit Report Sindh Agriculture University Tandojam, SindhDocument63 pagesAudit Report Sindh Agriculture University Tandojam, Sindhsadaf_183100% (1)

- 2010 ACE Limited Annual ReportDocument233 pages2010 ACE Limited Annual ReportACELitigationWatchNo ratings yet

- Independent Auditor's ReportDocument3 pagesIndependent Auditor's ReportNyra Beldoro100% (1)

- Preface: of Public Sector and Private Sector Banks"Document47 pagesPreface: of Public Sector and Private Sector Banks"madhuri100% (1)

- 1529302103778Document6 pages1529302103778Bibhuranjan MohantaNo ratings yet

- The Singapore Property Beginner S GuideDocument39 pagesThe Singapore Property Beginner S GuideCaleb LeeNo ratings yet

- A Study of Consumer Behaviour in Relation To Insurance Products in IDBI Federal LifeDocument42 pagesA Study of Consumer Behaviour in Relation To Insurance Products in IDBI Federal LifeAshu Agarwal0% (2)

- Account Receivable PresentationDocument34 pagesAccount Receivable PresentationYakub Immanuel SaputraNo ratings yet

- Mauricio Ramirez - OTM Implementation Best PracticesDocument21 pagesMauricio Ramirez - OTM Implementation Best PracticesdbahanyNo ratings yet

- Bank Reconciliation Statement in SAPDocument8 pagesBank Reconciliation Statement in SAPcharanNo ratings yet

- Please Confirm To ContinueDocument4 pagesPlease Confirm To ContinueMahakaal Digital PointNo ratings yet

- Shipping Maritime AbbreviationsDocument22 pagesShipping Maritime Abbreviationsteo_bozo5589No ratings yet

- Body of NBL-FexDocument76 pagesBody of NBL-FexIshrat JahanNo ratings yet

- Public Auction: 15 OCT 2019, 9.30amDocument1 pagePublic Auction: 15 OCT 2019, 9.30amchek86351No ratings yet

- Fee Information Document: General Account ServicesDocument7 pagesFee Information Document: General Account Servicesdaryl30011996No ratings yet

- HaiDocument20 pagesHaikuku's entertainmentNo ratings yet

- CA Solar Share 529 ProgramDocument72 pagesCA Solar Share 529 Programd_fanthamNo ratings yet