Download as pdf or txt

You might also like

- 3-s Source Document June NokyungDocument2 pages3-s Source Document June Nokyungapi-289122077No ratings yet

- Accounting 199-Accounting For Problem Solving Assignment #2 Professor Peter DemerjianDocument5 pagesAccounting 199-Accounting For Problem Solving Assignment #2 Professor Peter DemerjianEvelyn B. YareNo ratings yet

- CH 4 HW PDFDocument26 pagesCH 4 HW PDFIbra TutorNo ratings yet

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionFrom EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNo ratings yet

- 2 Foundation Ft 2 [Unsolved][18!06!2024][Final]Document6 pages2 Foundation Ft 2 [Unsolved][18!06!2024][Final]simranjitkour27No ratings yet

- Accounting Questions 27.04.2022Document5 pagesAccounting Questions 27.04.2022psree7281No ratings yet

- CA-Foundation Accounts Full Syllabus Test For Dec 2023 StudentsDocument4 pagesCA-Foundation Accounts Full Syllabus Test For Dec 2023 Studentsbabu.bhiwadiNo ratings yet

- SYJC Accounts Board Question Paper of Feb 2019Document6 pagesSYJC Accounts Board Question Paper of Feb 2019sohambhosale606No ratings yet

- Delhi Pubic School, Nacharam Accountancy - Xi Question BankDocument9 pagesDelhi Pubic School, Nacharam Accountancy - Xi Question BanklasyaNo ratings yet

- CA Foundation MTP 2020 Paper 1 AnsDocument9 pagesCA Foundation MTP 2020 Paper 1 AnsSaurabh Kumar MauryaNo ratings yet

- 21.11.23 CA-FOUNDATION MOCK TEST PAPER ACCOUNTS Dec. 23Document5 pages21.11.23 CA-FOUNDATION MOCK TEST PAPER ACCOUNTS Dec. 23RohitNo ratings yet

- Allama Iqbal Open University, Islamabad: (Department of Commerce)Document4 pagesAllama Iqbal Open University, Islamabad: (Department of Commerce)ilyas muhammadNo ratings yet

- Test Paper Ca FoundDocument5 pagesTest Paper Ca FoundSarangapani KaliyamoorthyNo ratings yet

- Model Question Papers - XIDocument86 pagesModel Question Papers - XIalbishamomin60No ratings yet

- Financial Accounting (CBCS Hons)Document7 pagesFinancial Accounting (CBCS Hons)Devil GamerNo ratings yet

- 2accounting Questions Nov Dec 2019 CL PDFDocument3 pages2accounting Questions Nov Dec 2019 CL PDFRazib Das RaazNo ratings yet

- Topic Wise Test Accounting From Incomplete RecordsDocument4 pagesTopic Wise Test Accounting From Incomplete RecordsChinmay GokhaleNo ratings yet

- MTP May20 ADocument9 pagesMTP May20 Aomkar sawantNo ratings yet

- Ca Foundation AccountsDocument7 pagesCa Foundation AccountssmartshivenduNo ratings yet

- B. Com I All PapersnDocument14 pagesB. Com I All Papersnrahim Abbas aliNo ratings yet

- Sample Paper For Class 11 Accountancy Set 1 QuestionsDocument6 pagesSample Paper For Class 11 Accountancy Set 1 Questionsrenu bhattNo ratings yet

- शिक्षा निदेिालय राष्ट्रीय राजधािी क्षेत्र ददल्ली Directorate of Education, GNCT of DelhiDocument4 pagesशिक्षा निदेिालय राष्ट्रीय राजधािी क्षेत्र ददल्ली Directorate of Education, GNCT of DelhiAshish ChNo ratings yet

- 20uafam01 BM01 20ubmam01 Principles of Financial AccountingDocument3 pages20uafam01 BM01 20ubmam01 Principles of Financial AccountingArshath KumaarNo ratings yet

- +1 Accountancy ONLINE Final Examination 2021Document5 pages+1 Accountancy ONLINE Final Examination 2021Rajwinder BansalNo ratings yet

- 11 Sample Papers Accountancy 2020 English Medium Set 1 PDFDocument13 pages11 Sample Papers Accountancy 2020 English Medium Set 1 PDFpriyaNo ratings yet

- Foundation Accounts Suggested Nov20Document25 pagesFoundation Accounts Suggested Nov20dhanushd0613No ratings yet

- FDN J22 - TS 2 - P1 Account - QueDocument5 pagesFDN J22 - TS 2 - P1 Account - QueShantanu JadhavNo ratings yet

- SP - XI - AccountancyDocument3 pagesSP - XI - AccountancyPriyankadevi PrabuNo ratings yet

- Vidya Sagar: Foundation Major Test - 1 (Series - 3) Nov - 20 "Principles and Practice of Accounting"Document5 pagesVidya Sagar: Foundation Major Test - 1 (Series - 3) Nov - 20 "Principles and Practice of Accounting"sonubudsNo ratings yet

- Mam2e 72221Document8 pagesMam2e 72221priyanehasahaNo ratings yet

- Accounting Round 1Document6 pagesAccounting Round 1Malhar ShahNo ratings yet

- 2019-04 ICMAB FL 001 PAC Year Question April 2019Document3 pages2019-04 ICMAB FL 001 PAC Year Question April 2019Mohammad ShahidNo ratings yet

- Ugmbcc04 - Business AccountingDocument4 pagesUgmbcc04 - Business AccountingShreya MitraNo ratings yet

- LHU8Q Olopr DaisyAcountXIDocument35 pagesLHU8Q Olopr DaisyAcountXIDido MuczNo ratings yet

- Accounts Suggested Ans CAF Nov 20Document25 pagesAccounts Suggested Ans CAF Nov 20Anshu DasNo ratings yet

- Paper - 1: Principles and Practice of Accounting: Question No. 1 Is CompulsoryDocument25 pagesPaper - 1: Principles and Practice of Accounting: Question No. 1 Is CompulsorySaurabh JainNo ratings yet

- 0438Document7 pages0438murtaza5500No ratings yet

- Nava Bharath National School Annur Annual Examination - 2021 AccountancyDocument5 pagesNava Bharath National School Annur Annual Examination - 2021 AccountancypranavNo ratings yet

- 11 Com Pre-ExamDocument4 pages11 Com Pre-ExamObaid Khan50% (2)

- Gujarat Technological UniversityDocument4 pagesGujarat Technological UniversityAniket PatelNo ratings yet

- Test 5 Solutions AccountsDocument9 pagesTest 5 Solutions AccountsVijayasri KumaravelNo ratings yet

- XI Acc 3Document4 pagesXI Acc 3Bhumika ShaldarNo ratings yet

- 8104 MbaexDocument3 pages8104 Mbaexgaurav jainNo ratings yet

- UCO1501Document4 pagesUCO1501PRIYA LAKSHMANNo ratings yet

- 12 Ut 1,2Document7 pages12 Ut 1,2Soni soniyaNo ratings yet

- Model-Financial Accounting - Set1 - CZ21ADocument4 pagesModel-Financial Accounting - Set1 - CZ21AJuli SunNo ratings yet

- 5401Document6 pages5401ArumNo ratings yet

- IN IN: Government Diploma AND Certificate Co - Operative HousingDocument6 pagesIN IN: Government Diploma AND Certificate Co - Operative HousingShahnawaz ShaikhNo ratings yet

- Financial AccountingDocument4 pagesFinancial AccountingMaithili SUBRAMANIANNo ratings yet

- Corporate Accounting Imp QuestionsDocument10 pagesCorporate Accounting Imp QuestionsbalachandranharipriyaNo ratings yet

- Introduction To Accounting: Certificate in Accounting and Finance Stage ExaminationsDocument4 pagesIntroduction To Accounting: Certificate in Accounting and Finance Stage ExaminationsSkans R&DNo ratings yet

- Deso 04Document5 pagesDeso 04Nguyễn Quốc TuấnNo ratings yet

- Test 3Document8 pagesTest 3govarthan1976No ratings yet

- XI Pre-BoardDocument7 pagesXI Pre-BoardSamar Singh Rathore0% (1)

- Qus. MTP Accounts - 09.12.23Document5 pagesQus. MTP Accounts - 09.12.23karann021003No ratings yet

- Management Programme: MS-04: Accounting and Finance For ManagersDocument5 pagesManagement Programme: MS-04: Accounting and Finance For Managersanon_323108No ratings yet

- P6 June 2023 SY23Document5 pagesP6 June 2023 SY23Shivam GuptaNo ratings yet

- MTP 23 54 Questions 1717476460Document8 pagesMTP 23 54 Questions 171747646023prfb31No ratings yet

- CA Foundation Paper 1 Principles and Practice of Accounting SADocument24 pagesCA Foundation Paper 1 Principles and Practice of Accounting SAavula Venkatrao100% (1)

- 1 Af 101 FfaDocument4 pages1 Af 101 FfaHakim JanNo ratings yet

- 0438Document9 pages0438Ahmed BilalNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionNo ratings yet

- MCQS Trail BalanceDocument2 pagesMCQS Trail BalanceSai KrishnaNo ratings yet

- C2G Terms and ConditionsDocument13 pagesC2G Terms and ConditionsMark Titus Montoya RamosNo ratings yet

- Gr11 ACC P2 (ENG) June 2022 Answer BookDocument10 pagesGr11 ACC P2 (ENG) June 2022 Answer Bookora mashaNo ratings yet

- Billing BlockDocument58 pagesBilling BlockSourav Kumar100% (1)

- Accounting EQB Chapter 15 QsDocument41 pagesAccounting EQB Chapter 15 Qsnatalia hariniNo ratings yet

- Yusingco, Rhealene A. ABM 12 - St. Paul: Fundamentals of Accounting 2 Unit Test For Statement of Financial PositionDocument13 pagesYusingco, Rhealene A. ABM 12 - St. Paul: Fundamentals of Accounting 2 Unit Test For Statement of Financial PositionRaymond Roco100% (1)

- Sap Fico NotesDocument235 pagesSap Fico Notespunardeep88% (8)

- Part 1 - Acc - 2016Document10 pagesPart 1 - Acc - 2016Sheikh Mass JahNo ratings yet

- Model Question Set 1Document2 pagesModel Question Set 1Destiny Tuition CentreNo ratings yet

- Account Statement: Shashwat MishraDocument11 pagesAccount Statement: Shashwat MishraShashwat MishraNo ratings yet

- Jewellery Business Solution: SolutionsDocument5 pagesJewellery Business Solution: SolutionsmehtavikalpNo ratings yet

- WWW - Isr.umd - Edu Austin Ense621.d Projects04.d Project-Food-OrderingDocument46 pagesWWW - Isr.umd - Edu Austin Ense621.d Projects04.d Project-Food-OrderingjollyggNo ratings yet

- Winding Up111Document9 pagesWinding Up111Jenever Leo SerranoNo ratings yet

- Working Capital ManagementDocument18 pagesWorking Capital ManagementSumanDasNo ratings yet

- Mutasi Muhamad 11102022Document23 pagesMutasi Muhamad 11102022arlan alexandriaNo ratings yet

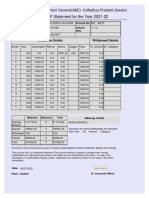

- GPF Statement For The Year 2021-22: O/o The Pr. Accountant General (A&E) - II, Madhya Pradesh, GwaliorDocument1 pageGPF Statement For The Year 2021-22: O/o The Pr. Accountant General (A&E) - II, Madhya Pradesh, GwaliorSHIVGOPAL KULHADENo ratings yet

- Trading and Profit and Loss Account Further ConsiderationsDocument5 pagesTrading and Profit and Loss Account Further ConsiderationsbillNo ratings yet

- Accounting (2) Chapter (5) : LevelDocument14 pagesAccounting (2) Chapter (5) : LevelMohamed DiabNo ratings yet

- Chapter 5 Accounting For Disbursements and Related TransactionsDocument2 pagesChapter 5 Accounting For Disbursements and Related TransactionsJaps100% (1)

- Bat4M Adjusting Entries: Learning Goal: Review: How To Record Adjusting Entries For A Service BusinessDocument5 pagesBat4M Adjusting Entries: Learning Goal: Review: How To Record Adjusting Entries For A Service BusinessJohnMurray111No ratings yet

- ReviewerDocument67 pagesReviewerKyungsoo DohNo ratings yet

- APDocument38 pagesAPCyvee Joy Hongayo OcheaNo ratings yet

- Question Bank of Sem - 1 To Sem-9 of Faculty of Law PDFDocument203 pagesQuestion Bank of Sem - 1 To Sem-9 of Faculty of Law PDFHasnain Qaiyumi0% (1)

- CIR V Petron CorpDocument15 pagesCIR V Petron CorpChristiane Marie BajadaNo ratings yet

- Receipt and Payment AccountDocument3 pagesReceipt and Payment Accountsarvesh.bhartiNo ratings yet

- m2 Performance Assessment AlejandrosorianoDocument11 pagesm2 Performance Assessment AlejandrosorianoALEJANDRO SORIANONo ratings yet

- Cap College NewDocument10 pagesCap College NewAbby Joy FlavianoNo ratings yet

![2 Foundation Ft 2 [Unsolved][18!06!2024][Final]](https://imgv2-1-f.scribdassets.com/img/document/748304142/149x198/d7b0feefcd/1720248967?v=1)