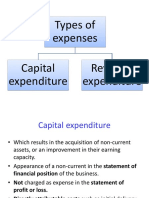

'O' Level Accounting Capital and Revenue Expenditure

'O' Level Accounting Capital and Revenue Expenditure

You might also like

- Wells Fargo Bank StatementDocument1 pageWells Fargo Bank StatementKirill DelyNo ratings yet

- Corp Financial ReportingDocument7 pagesCorp Financial ReportingJustin L De ArmondNo ratings yet

- Types of Expenses Capital Expenditure Revenue ExpenditureDocument8 pagesTypes of Expenses Capital Expenditure Revenue ExpenditureChong Kuan PeiNo ratings yet

- MEFADocument24 pagesMEFASai Teja MadhaNo ratings yet

- Chapter 2Document3 pagesChapter 2Jk DVSNo ratings yet

- Final Accounts: Manufacturing, Trading and P&L A/cDocument51 pagesFinal Accounts: Manufacturing, Trading and P&L A/cAnit Jacob Philip100% (1)

- Revenue ExpendituresDocument8 pagesRevenue ExpendituresAdvertising Alaska Holiday100% (1)

- Chapter 4 - Income Measurement & Accrual Accounting: Recognition & Measurement in Financial StatementsDocument5 pagesChapter 4 - Income Measurement & Accrual Accounting: Recognition & Measurement in Financial StatementsHareem Zoya WarsiNo ratings yet

- Cee 4Document13 pagesCee 4Abdullah RamzanNo ratings yet

- 5 6172302118171443573 PDFDocument3 pages5 6172302118171443573 PDFPavan RaiNo ratings yet

- Chapter - 7 Income Statements Learning Objectives: Dr. Trading A/C CRDocument14 pagesChapter - 7 Income Statements Learning Objectives: Dr. Trading A/C CRSaket_srv2100% (1)

- Annual ReportDocument5 pagesAnnual Reportmengjun0987654311No ratings yet

- Facilitators Guide For Accenture-IGNOU Diploma Program: Unit 4Document20 pagesFacilitators Guide For Accenture-IGNOU Diploma Program: Unit 4Vinay SinghNo ratings yet

- Reconciliation of Cost & Financial AccountsDocument13 pagesReconciliation of Cost & Financial AccountsRahulNo ratings yet

- 2211posting 061cab6e3d56f89 03363994Document12 pages2211posting 061cab6e3d56f89 03363994Saleh RaoufNo ratings yet

- Capital Vs Revenue Exp..... Point PresentationDocument16 pagesCapital Vs Revenue Exp..... Point PresentationVinay Kumar100% (1)

- Mba775 - ACF 6 - Adjustments To Earnings Before Using DCF ModelsDocument14 pagesMba775 - ACF 6 - Adjustments To Earnings Before Using DCF Modelsshubhtandon123No ratings yet

- ACCOUNTING: Inflation AccountingDocument34 pagesACCOUNTING: Inflation Accountingmehul100% (2)

- Chapter 2 WileyDocument29 pagesChapter 2 Wileyp876468No ratings yet

- Preparation of financial statements1Document40 pagesPreparation of financial statements1swarnajit paulNo ratings yet

- Fundamentals of Accounting PDFDocument52 pagesFundamentals of Accounting PDFomid sangarNo ratings yet

- Introduction To Financial Accounting (FFA/FAB) : DR Ahmad AlshehabiDocument55 pagesIntroduction To Financial Accounting (FFA/FAB) : DR Ahmad AlshehabiKye SimpsonNo ratings yet

- The Balance SheetDocument101 pagesThe Balance SheethakomoNo ratings yet

- FCA-CSzBS - II UnitDocument34 pagesFCA-CSzBS - II UnitSURIYA VARSHANNo ratings yet

- Balance Sheet: by Dr. ArchanaDocument19 pagesBalance Sheet: by Dr. ArchanaHan JeeNo ratings yet

- Introa5 7Document41 pagesIntroa5 7Ameya RanadiveNo ratings yet

- Accounting For Managers Ch02Document31 pagesAccounting For Managers Ch02Abdul Naseer KhacsarNo ratings yet

- Module D - Final Accounts of Banks & Companies - PresentationDocument102 pagesModule D - Final Accounts of Banks & Companies - PresentationASHISH GUPTANo ratings yet

- Lesson 5Document31 pagesLesson 5Glenda DestrizaNo ratings yet

- Class 15Document14 pagesClass 15Majid IqbalNo ratings yet

- Preparation of Final AccountDocument32 pagesPreparation of Final AccountCHARLES FURTADONo ratings yet

- Basic Accounting TermsDocument12 pagesBasic Accounting TermsNathan DavidNo ratings yet

- Chapter 23 Current Cost AccountingDocument24 pagesChapter 23 Current Cost AccountingElaine Fiona VillafuerteNo ratings yet

- 03 Completing The Accounting Cycle of A Merchandising BusinessDocument62 pages03 Completing The Accounting Cycle of A Merchandising BusinessApril SasamNo ratings yet

- Acc Adjustments PDFDocument15 pagesAcc Adjustments PDFHana YusriNo ratings yet

- Account TitlesDocument4 pagesAccount TitlesChristian VelascoNo ratings yet

- CE 309 FINANCIAL STATEMENT ANALYSIS Lecture Sept 2013Document98 pagesCE 309 FINANCIAL STATEMENT ANALYSIS Lecture Sept 2013kundayi shavaNo ratings yet

- Liquidity of Short-Term Assets Related Debt-Paying Ability: Mehwish KiranDocument33 pagesLiquidity of Short-Term Assets Related Debt-Paying Ability: Mehwish KiranAlina ZubairNo ratings yet

- Module Business Finance Chapter 2Document25 pagesModule Business Finance Chapter 2Atria Lenn Villamiel BugalNo ratings yet

- Chapter 2Document12 pagesChapter 2Ashekin MahadiNo ratings yet

- AFIN102 Notes Pack 3Document52 pagesAFIN102 Notes Pack 3boy.poo90No ratings yet

- Session 2a Handout PDFDocument7 pagesSession 2a Handout PDFChin Hung YauNo ratings yet

- Abm01 - Module 4.2Document25 pagesAbm01 - Module 4.2Love JcwNo ratings yet

- Basic Accounting Principles: The Financial StatementsDocument55 pagesBasic Accounting Principles: The Financial Statementsthella deva prasadNo ratings yet

- Fabm 1 ReviewerDocument4 pagesFabm 1 Reviewersolisleslie.0707No ratings yet

- Part 6.a - AccountingDocument38 pagesPart 6.a - AccountingzhengcunzhangNo ratings yet

- Acc721: Framework For Accounting & ReportingDocument14 pagesAcc721: Framework For Accounting & ReportingJason InufiNo ratings yet

- Accountingnit Jamshedpur NotesDocument47 pagesAccountingnit Jamshedpur NotesSuraj KumarNo ratings yet

- Chapter 9 - Current Liabilities: Contingencies, and The Time Value of MoneyDocument8 pagesChapter 9 - Current Liabilities: Contingencies, and The Time Value of MoneyHareem Zoya WarsiNo ratings yet

- Ch2 - Financial Statement Analysis - NTHDocument107 pagesCh2 - Financial Statement Analysis - NTHAnh NguyễnNo ratings yet

- Chapter 12Document8 pagesChapter 12Hareem Zoya WarsiNo ratings yet

- L 5 Cost of CapitalDocument16 pagesL 5 Cost of CapitalMansi SainiNo ratings yet

- Financial ManagementDocument53 pagesFinancial ManagementOmNo ratings yet

- CHAPTER 4 BACT Equation Expanded To Show Operating ActivitiesDocument50 pagesCHAPTER 4 BACT Equation Expanded To Show Operating Activities2051611No ratings yet

- Basic TerminologiesDocument20 pagesBasic TerminologiesMOHAMED USAIDNo ratings yet

- Assets Are The Items Your Company Owns That Can Provide FutureDocument11 pagesAssets Are The Items Your Company Owns That Can Provide FuturestudentNo ratings yet

- Basic Financial Literacy_CSR_UpdateDocument46 pagesBasic Financial Literacy_CSR_UpdatehtayminkineNo ratings yet

- Accounting Fundamentals: By: Prof Jayraj JavheriDocument41 pagesAccounting Fundamentals: By: Prof Jayraj JavherijayrajNo ratings yet

- Capital Budgeting SOBD-4Document30 pagesCapital Budgeting SOBD-4shrutisirsa1No ratings yet

- Session 5 - Financial Statement AnalysisDocument42 pagesSession 5 - Financial Statement AnalysisVaibhav JainNo ratings yet

- Financial Accounting and Reporting Study Guide NotesFrom EverandFinancial Accounting and Reporting Study Guide NotesRating: 1 out of 5 stars1/5 (1)

- Unit 1 FMDocument14 pagesUnit 1 FMRICKY KALITANo ratings yet

- Calculations - Mr. Prem Ranjan & SudhaDocument72 pagesCalculations - Mr. Prem Ranjan & SudhaVinay Kumar100% (1)

- SME Rating (Methodology)Document6 pagesSME Rating (Methodology)radhika1991No ratings yet

- Afterpay Research PDFDocument33 pagesAfterpay Research PDFNikhil JoyNo ratings yet

- Dalio Ebook FINAL PDFDocument48 pagesDalio Ebook FINAL PDFvuhieptran100% (1)

- Kosamattam Finance Limited Prospectus AprilDocument287 pagesKosamattam Finance Limited Prospectus Aprilmehtarahul999No ratings yet

- Jpmorgan Trust IIDocument180 pagesJpmorgan Trust IIgunjanbihaniNo ratings yet

- MAhmed 3269 18189 2 Lecture Capital Budgeting and EstimatingDocument12 pagesMAhmed 3269 18189 2 Lecture Capital Budgeting and EstimatingSadia AbidNo ratings yet

- I7oB nKtGDi6RyT0Document6 pagesI7oB nKtGDi6RyT0Gretta BrownNo ratings yet

- Statement of Account: Date Tran Id Remarks UTR Number Instr. ID Withdrawals Deposits BalanceDocument1 pageStatement of Account: Date Tran Id Remarks UTR Number Instr. ID Withdrawals Deposits BalanceRohan TiwariNo ratings yet

- FM 1Document3 pagesFM 1anon-940489No ratings yet

- GP FundDocument45 pagesGP FundHaroon KhanNo ratings yet

- Commission StructureDocument3 pagesCommission StructureRandom ManiacNo ratings yet

- Concept of Capital and Revenue TransactionsDocument5 pagesConcept of Capital and Revenue TransactionsYakkstar 21No ratings yet

- FDP On Tax Planning, Financial Planning & Filing of ItrDocument4 pagesFDP On Tax Planning, Financial Planning & Filing of ItrAman KumarNo ratings yet

- Dividend Policy Gorden, Walter & MM Model Practice QuestionsDocument1 pageDividend Policy Gorden, Walter & MM Model Practice QuestionsAmjad AliNo ratings yet

- Chapter-1 Indian Banking System PDFDocument53 pagesChapter-1 Indian Banking System PDFbhuvaneswarimpNo ratings yet

- Test Bank For Government and Not For Profit Accounting 8th by GranofDocument20 pagesTest Bank For Government and Not For Profit Accounting 8th by GranofHorace Renfroe100% (47)

- Solutions 2021 MockExamDocument15 pagesSolutions 2021 MockExamdayeyoutai779No ratings yet

- A Study On Impact of Phone Pe Payment With Special Reference To YouthDocument110 pagesA Study On Impact of Phone Pe Payment With Special Reference To YouthAJAY RATHORENo ratings yet

- FM II 2022 Assignment IDocument7 pagesFM II 2022 Assignment IAmanuel AbebawNo ratings yet

- Bank StatementDocument24 pagesBank StatementJames PeterNo ratings yet

- Centronics Corporation v. Genicom CorporationDocument1 pageCentronics Corporation v. Genicom CorporationcrlstinaaaNo ratings yet

- LM Busmath q2 Module 2 Wk2 CasillaDocument30 pagesLM Busmath q2 Module 2 Wk2 CasillaDonna CasillaNo ratings yet

- Lecture Notes - Business Finance 2Document3 pagesLecture Notes - Business Finance 2Aslan AlpNo ratings yet

- New Developments in Islamic Economics: Article InformationDocument19 pagesNew Developments in Islamic Economics: Article Informationsajid bhattiNo ratings yet

- Name: Nikhil P. PalanDocument7 pagesName: Nikhil P. PalanVinit BhindeNo ratings yet

- Wellington Global Innovation Fund Factsheet July 2022Document2 pagesWellington Global Innovation Fund Factsheet July 2022snehalNo ratings yet

- Special Topics in Financial ManagementDocument36 pagesSpecial Topics in Financial ManagementChristel Mae Boseo100% (1)

Download as pdf or txt

You might also like

- Wells Fargo Bank StatementDocument1 pageWells Fargo Bank StatementKirill DelyNo ratings yet

- Corp Financial ReportingDocument7 pagesCorp Financial ReportingJustin L De ArmondNo ratings yet

- Types of Expenses Capital Expenditure Revenue ExpenditureDocument8 pagesTypes of Expenses Capital Expenditure Revenue ExpenditureChong Kuan PeiNo ratings yet

- MEFADocument24 pagesMEFASai Teja MadhaNo ratings yet

- Chapter 2Document3 pagesChapter 2Jk DVSNo ratings yet

- Final Accounts: Manufacturing, Trading and P&L A/cDocument51 pagesFinal Accounts: Manufacturing, Trading and P&L A/cAnit Jacob Philip100% (1)

- Revenue ExpendituresDocument8 pagesRevenue ExpendituresAdvertising Alaska Holiday100% (1)

- Chapter 4 - Income Measurement & Accrual Accounting: Recognition & Measurement in Financial StatementsDocument5 pagesChapter 4 - Income Measurement & Accrual Accounting: Recognition & Measurement in Financial StatementsHareem Zoya WarsiNo ratings yet

- Cee 4Document13 pagesCee 4Abdullah RamzanNo ratings yet

- 5 6172302118171443573 PDFDocument3 pages5 6172302118171443573 PDFPavan RaiNo ratings yet

- Chapter - 7 Income Statements Learning Objectives: Dr. Trading A/C CRDocument14 pagesChapter - 7 Income Statements Learning Objectives: Dr. Trading A/C CRSaket_srv2100% (1)

- Annual ReportDocument5 pagesAnnual Reportmengjun0987654311No ratings yet

- Facilitators Guide For Accenture-IGNOU Diploma Program: Unit 4Document20 pagesFacilitators Guide For Accenture-IGNOU Diploma Program: Unit 4Vinay SinghNo ratings yet

- Reconciliation of Cost & Financial AccountsDocument13 pagesReconciliation of Cost & Financial AccountsRahulNo ratings yet

- 2211posting 061cab6e3d56f89 03363994Document12 pages2211posting 061cab6e3d56f89 03363994Saleh RaoufNo ratings yet

- Capital Vs Revenue Exp..... Point PresentationDocument16 pagesCapital Vs Revenue Exp..... Point PresentationVinay Kumar100% (1)

- Mba775 - ACF 6 - Adjustments To Earnings Before Using DCF ModelsDocument14 pagesMba775 - ACF 6 - Adjustments To Earnings Before Using DCF Modelsshubhtandon123No ratings yet

- ACCOUNTING: Inflation AccountingDocument34 pagesACCOUNTING: Inflation Accountingmehul100% (2)

- Chapter 2 WileyDocument29 pagesChapter 2 Wileyp876468No ratings yet

- Preparation of financial statements1Document40 pagesPreparation of financial statements1swarnajit paulNo ratings yet

- Fundamentals of Accounting PDFDocument52 pagesFundamentals of Accounting PDFomid sangarNo ratings yet

- Introduction To Financial Accounting (FFA/FAB) : DR Ahmad AlshehabiDocument55 pagesIntroduction To Financial Accounting (FFA/FAB) : DR Ahmad AlshehabiKye SimpsonNo ratings yet

- The Balance SheetDocument101 pagesThe Balance SheethakomoNo ratings yet

- FCA-CSzBS - II UnitDocument34 pagesFCA-CSzBS - II UnitSURIYA VARSHANNo ratings yet

- Balance Sheet: by Dr. ArchanaDocument19 pagesBalance Sheet: by Dr. ArchanaHan JeeNo ratings yet

- Introa5 7Document41 pagesIntroa5 7Ameya RanadiveNo ratings yet

- Accounting For Managers Ch02Document31 pagesAccounting For Managers Ch02Abdul Naseer KhacsarNo ratings yet

- Module D - Final Accounts of Banks & Companies - PresentationDocument102 pagesModule D - Final Accounts of Banks & Companies - PresentationASHISH GUPTANo ratings yet

- Lesson 5Document31 pagesLesson 5Glenda DestrizaNo ratings yet

- Class 15Document14 pagesClass 15Majid IqbalNo ratings yet

- Preparation of Final AccountDocument32 pagesPreparation of Final AccountCHARLES FURTADONo ratings yet

- Basic Accounting TermsDocument12 pagesBasic Accounting TermsNathan DavidNo ratings yet

- Chapter 23 Current Cost AccountingDocument24 pagesChapter 23 Current Cost AccountingElaine Fiona VillafuerteNo ratings yet

- 03 Completing The Accounting Cycle of A Merchandising BusinessDocument62 pages03 Completing The Accounting Cycle of A Merchandising BusinessApril SasamNo ratings yet

- Acc Adjustments PDFDocument15 pagesAcc Adjustments PDFHana YusriNo ratings yet

- Account TitlesDocument4 pagesAccount TitlesChristian VelascoNo ratings yet

- CE 309 FINANCIAL STATEMENT ANALYSIS Lecture Sept 2013Document98 pagesCE 309 FINANCIAL STATEMENT ANALYSIS Lecture Sept 2013kundayi shavaNo ratings yet

- Liquidity of Short-Term Assets Related Debt-Paying Ability: Mehwish KiranDocument33 pagesLiquidity of Short-Term Assets Related Debt-Paying Ability: Mehwish KiranAlina ZubairNo ratings yet

- Module Business Finance Chapter 2Document25 pagesModule Business Finance Chapter 2Atria Lenn Villamiel BugalNo ratings yet

- Chapter 2Document12 pagesChapter 2Ashekin MahadiNo ratings yet

- AFIN102 Notes Pack 3Document52 pagesAFIN102 Notes Pack 3boy.poo90No ratings yet

- Session 2a Handout PDFDocument7 pagesSession 2a Handout PDFChin Hung YauNo ratings yet

- Abm01 - Module 4.2Document25 pagesAbm01 - Module 4.2Love JcwNo ratings yet

- Basic Accounting Principles: The Financial StatementsDocument55 pagesBasic Accounting Principles: The Financial Statementsthella deva prasadNo ratings yet

- Fabm 1 ReviewerDocument4 pagesFabm 1 Reviewersolisleslie.0707No ratings yet

- Part 6.a - AccountingDocument38 pagesPart 6.a - AccountingzhengcunzhangNo ratings yet

- Acc721: Framework For Accounting & ReportingDocument14 pagesAcc721: Framework For Accounting & ReportingJason InufiNo ratings yet

- Accountingnit Jamshedpur NotesDocument47 pagesAccountingnit Jamshedpur NotesSuraj KumarNo ratings yet

- Chapter 9 - Current Liabilities: Contingencies, and The Time Value of MoneyDocument8 pagesChapter 9 - Current Liabilities: Contingencies, and The Time Value of MoneyHareem Zoya WarsiNo ratings yet

- Ch2 - Financial Statement Analysis - NTHDocument107 pagesCh2 - Financial Statement Analysis - NTHAnh NguyễnNo ratings yet

- Chapter 12Document8 pagesChapter 12Hareem Zoya WarsiNo ratings yet

- L 5 Cost of CapitalDocument16 pagesL 5 Cost of CapitalMansi SainiNo ratings yet

- Financial ManagementDocument53 pagesFinancial ManagementOmNo ratings yet

- CHAPTER 4 BACT Equation Expanded To Show Operating ActivitiesDocument50 pagesCHAPTER 4 BACT Equation Expanded To Show Operating Activities2051611No ratings yet

- Basic TerminologiesDocument20 pagesBasic TerminologiesMOHAMED USAIDNo ratings yet

- Assets Are The Items Your Company Owns That Can Provide FutureDocument11 pagesAssets Are The Items Your Company Owns That Can Provide FuturestudentNo ratings yet

- Basic Financial Literacy_CSR_UpdateDocument46 pagesBasic Financial Literacy_CSR_UpdatehtayminkineNo ratings yet

- Accounting Fundamentals: By: Prof Jayraj JavheriDocument41 pagesAccounting Fundamentals: By: Prof Jayraj JavherijayrajNo ratings yet

- Capital Budgeting SOBD-4Document30 pagesCapital Budgeting SOBD-4shrutisirsa1No ratings yet

- Session 5 - Financial Statement AnalysisDocument42 pagesSession 5 - Financial Statement AnalysisVaibhav JainNo ratings yet

- Financial Accounting and Reporting Study Guide NotesFrom EverandFinancial Accounting and Reporting Study Guide NotesRating: 1 out of 5 stars1/5 (1)

- Unit 1 FMDocument14 pagesUnit 1 FMRICKY KALITANo ratings yet

- Calculations - Mr. Prem Ranjan & SudhaDocument72 pagesCalculations - Mr. Prem Ranjan & SudhaVinay Kumar100% (1)

- SME Rating (Methodology)Document6 pagesSME Rating (Methodology)radhika1991No ratings yet

- Afterpay Research PDFDocument33 pagesAfterpay Research PDFNikhil JoyNo ratings yet

- Dalio Ebook FINAL PDFDocument48 pagesDalio Ebook FINAL PDFvuhieptran100% (1)

- Kosamattam Finance Limited Prospectus AprilDocument287 pagesKosamattam Finance Limited Prospectus Aprilmehtarahul999No ratings yet

- Jpmorgan Trust IIDocument180 pagesJpmorgan Trust IIgunjanbihaniNo ratings yet

- MAhmed 3269 18189 2 Lecture Capital Budgeting and EstimatingDocument12 pagesMAhmed 3269 18189 2 Lecture Capital Budgeting and EstimatingSadia AbidNo ratings yet

- I7oB nKtGDi6RyT0Document6 pagesI7oB nKtGDi6RyT0Gretta BrownNo ratings yet

- Statement of Account: Date Tran Id Remarks UTR Number Instr. ID Withdrawals Deposits BalanceDocument1 pageStatement of Account: Date Tran Id Remarks UTR Number Instr. ID Withdrawals Deposits BalanceRohan TiwariNo ratings yet

- FM 1Document3 pagesFM 1anon-940489No ratings yet

- GP FundDocument45 pagesGP FundHaroon KhanNo ratings yet

- Commission StructureDocument3 pagesCommission StructureRandom ManiacNo ratings yet

- Concept of Capital and Revenue TransactionsDocument5 pagesConcept of Capital and Revenue TransactionsYakkstar 21No ratings yet

- FDP On Tax Planning, Financial Planning & Filing of ItrDocument4 pagesFDP On Tax Planning, Financial Planning & Filing of ItrAman KumarNo ratings yet

- Dividend Policy Gorden, Walter & MM Model Practice QuestionsDocument1 pageDividend Policy Gorden, Walter & MM Model Practice QuestionsAmjad AliNo ratings yet

- Chapter-1 Indian Banking System PDFDocument53 pagesChapter-1 Indian Banking System PDFbhuvaneswarimpNo ratings yet

- Test Bank For Government and Not For Profit Accounting 8th by GranofDocument20 pagesTest Bank For Government and Not For Profit Accounting 8th by GranofHorace Renfroe100% (47)

- Solutions 2021 MockExamDocument15 pagesSolutions 2021 MockExamdayeyoutai779No ratings yet

- A Study On Impact of Phone Pe Payment With Special Reference To YouthDocument110 pagesA Study On Impact of Phone Pe Payment With Special Reference To YouthAJAY RATHORENo ratings yet

- FM II 2022 Assignment IDocument7 pagesFM II 2022 Assignment IAmanuel AbebawNo ratings yet

- Bank StatementDocument24 pagesBank StatementJames PeterNo ratings yet

- Centronics Corporation v. Genicom CorporationDocument1 pageCentronics Corporation v. Genicom CorporationcrlstinaaaNo ratings yet

- LM Busmath q2 Module 2 Wk2 CasillaDocument30 pagesLM Busmath q2 Module 2 Wk2 CasillaDonna CasillaNo ratings yet

- Lecture Notes - Business Finance 2Document3 pagesLecture Notes - Business Finance 2Aslan AlpNo ratings yet

- New Developments in Islamic Economics: Article InformationDocument19 pagesNew Developments in Islamic Economics: Article Informationsajid bhattiNo ratings yet

- Name: Nikhil P. PalanDocument7 pagesName: Nikhil P. PalanVinit BhindeNo ratings yet

- Wellington Global Innovation Fund Factsheet July 2022Document2 pagesWellington Global Innovation Fund Factsheet July 2022snehalNo ratings yet

- Special Topics in Financial ManagementDocument36 pagesSpecial Topics in Financial ManagementChristel Mae Boseo100% (1)