Download as pdf or txt

You might also like

- UntitledDocument13 pagesUntitledAnne GuamosNo ratings yet

- Certificate of IncorporationDocument1 pageCertificate of IncorporationPritam685No ratings yet

- Aquabest Fin StatementsDocument27 pagesAquabest Fin StatementsJohn Kenneth BoholNo ratings yet

- Brief Case Study On ESEWADocument13 pagesBrief Case Study On ESEWADear World0% (1)

- R2.TAXML Solution CMA September 2022 Exam.Document5 pagesR2.TAXML Solution CMA September 2022 Exam.Raziur RahmanNo ratings yet

- Workings 23apr24Document4 pagesWorkings 23apr24Thomas DevaNo ratings yet

- Assumptions - Assumptions - Financing: Year - 0 Year - 1 Year - 2 Year - 3 Year - 4Document2 pagesAssumptions - Assumptions - Financing: Year - 0 Year - 1 Year - 2 Year - 3 Year - 4PranshuNo ratings yet

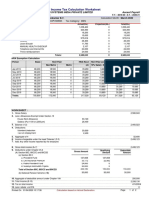

- Income Tax Calculation Worksheet: Ellucian Higher Education Systems India Private Limited Ascent PayrollDocument2 pagesIncome Tax Calculation Worksheet: Ellucian Higher Education Systems India Private Limited Ascent PayrollShiva098No ratings yet

- Only Fill Yellow Cells: WorkingsDocument2 pagesOnly Fill Yellow Cells: WorkingsvikrammoolchandaniNo ratings yet

- Principle and Practice of TaxationDocument5 pagesPrinciple and Practice of TaxationAgyeiNo ratings yet

- SESB-Budget 2013 (Departmental Budget) - Corp Comm Revised As at 17OCT2012Document38 pagesSESB-Budget 2013 (Departmental Budget) - Corp Comm Revised As at 17OCT2012roalan1No ratings yet

- Annual Computation of Taxable Salary FY 2021-22Document1 pageAnnual Computation of Taxable Salary FY 2021-22Irfan RazaNo ratings yet

- Calculo Rta 5ta 2020Document12 pagesCalculo Rta 5ta 2020CARLOS DANIEL ARELLANO SOLANONo ratings yet

- R2. TAX (M.L) Solution CMA May-2023 ExamDocument5 pagesR2. TAX (M.L) Solution CMA May-2023 ExamSharif MahmudNo ratings yet

- Cost Sheet - GenX - Team 4 .2Document7 pagesCost Sheet - GenX - Team 4 .2sanketmistry32No ratings yet

- FARM-PLAN-BUDGET-AGRINEGOSYO-2 (1) FinalDocument19 pagesFARM-PLAN-BUDGET-AGRINEGOSYO-2 (1) FinalJOURLY RANQUENo ratings yet

- StoqnamadruateDocument4 pagesStoqnamadruateDela cruz, Hainrich (Hain)No ratings yet

- Mar 2023Document1 pageMar 2023gaurav sharmaNo ratings yet

- Case 1: Market PriceDocument6 pagesCase 1: Market PriceNoor ul HudaNo ratings yet

- 3 Months PlanDocument8 pages3 Months PlanWaleed ZakariaNo ratings yet

- Se/Omc/Nalgonda - Pay Unit Code: 5112: Pay Slip For The Month of August - 2020Document1 pageSe/Omc/Nalgonda - Pay Unit Code: 5112: Pay Slip For The Month of August - 2020babu xeroxNo ratings yet

- Final Accouts Unsolved QuestionsDocument27 pagesFinal Accouts Unsolved Questionsmayank shridharNo ratings yet

- Es - Group 8Document4 pagesEs - Group 8Papa NketsiahNo ratings yet

- GYM Financial ModelingDocument12 pagesGYM Financial ModelingDivyanshu SharmaNo ratings yet

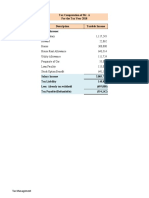

- Provisional: Provisional Income Tax CalculationDocument1 pageProvisional: Provisional Income Tax CalculationM. A Hossain & Associates Tax ConsultantsNo ratings yet

- Answer Key Discussion of Sir Paul of PreweekDocument2 pagesAnswer Key Discussion of Sir Paul of PreweekElaine Joyce GarciaNo ratings yet

- Financial StatementDocument36 pagesFinancial StatementJigoku ShojuNo ratings yet

- AACA2 AssignmentsDocument20 pagesAACA2 AssignmentsadieNo ratings yet

- Pyq (June 2018) 2.0Document1 pagePyq (June 2018) 2.0farah sofeaNo ratings yet

- STT - Mock - Test - S-24 - Suggested AnswersDocument8 pagesSTT - Mock - Test - S-24 - Suggested AnswersabdullahNo ratings yet

- PR 117 Part 2Document9 pagesPR 117 Part 2viswadevassociates.tvmNo ratings yet

- Gross Reportable Compensation Income 285,000Document3 pagesGross Reportable Compensation Income 285,000WenjunNo ratings yet

- TM PQsDocument9 pagesTM PQsAnooshayNo ratings yet

- SSF Not Listed-Monthly Salary Sheet With TDS Calculation 2076-2077Document29 pagesSSF Not Listed-Monthly Salary Sheet With TDS Calculation 2076-2077samNo ratings yet

- Dissolution PDFDocument4 pagesDissolution PDFCyangenNo ratings yet

- Model Solution: Page 1 of 6Document6 pagesModel Solution: Page 1 of 6ShuvonathNo ratings yet

- Plas Mech BS 07-08Document32 pagesPlas Mech BS 07-08plasmechNo ratings yet

- Template 2 Task 3 Calculation Worksheet - BSBFIM601Document17 pagesTemplate 2 Task 3 Calculation Worksheet - BSBFIM601Writing Experts0% (1)

- Paye Calculator-2Document11 pagesPaye Calculator-2MORRIS MURIGINo ratings yet

- Team PRTC FPB Oct 2023 - Tax (Q)Document8 pagesTeam PRTC FPB Oct 2023 - Tax (Q)Daphne PerezNo ratings yet

- LG Feasibility Study (Self Service Laundry) 2016Document1 pageLG Feasibility Study (Self Service Laundry) 2016Faty BercasioNo ratings yet

- Capital Investment Break-Up: Marketing and PromotionDocument7 pagesCapital Investment Break-Up: Marketing and PromotionDeepak RamamoorthyNo ratings yet

- Chapter 1Document18 pagesChapter 1Kenny WongNo ratings yet

- TM PQsDocument10 pagesTM PQsAnooshayNo ratings yet

- Salma Saifi May SlipDocument2 pagesSalma Saifi May Slipsalma saifiNo ratings yet

- Kirandeep September SalaryDocument1 pageKirandeep September Salaryprince.gill07No ratings yet

- 1% Stock Movement StrategyDocument1 page1% Stock Movement Strategyashish10mca9394No ratings yet

- Kirandeep August SalaryDocument1 pageKirandeep August Salaryprince.gill07No ratings yet

- Taxation Review Dec2016Document6 pagesTaxation Review Dec2016Shaiful Alam FCANo ratings yet

- Test 3 FinaccDocument8 pagesTest 3 FinaccPaul ChavundukaNo ratings yet

- Salary For Sep - 2022Document1 pageSalary For Sep - 2022narottam.ojhaNo ratings yet

- Capital Contribution: Stockholder TINDocument17 pagesCapital Contribution: Stockholder TINEddie ParazoNo ratings yet

- NON MEDICLAIM AY2024-25 SARBANI BORA-BDPPB0721G-ComputationDocument2 pagesNON MEDICLAIM AY2024-25 SARBANI BORA-BDPPB0721G-ComputationlaskarmohinNo ratings yet

- f6vnm 2007 Dec ADocument6 pagesf6vnm 2007 Dec APhạm Hùng DũngNo ratings yet

- PRTC Tax 1st PB 0522 This Is PRTC Tax Problem Quizzes Assignement Drills Answer Key - CompressDocument16 pagesPRTC Tax 1st PB 0522 This Is PRTC Tax Problem Quizzes Assignement Drills Answer Key - CompressNovemae CollamatNo ratings yet

- Income Taxation Answer ExamDocument5 pagesIncome Taxation Answer Examyezaquera100% (1)

- Case01 02Document24 pagesCase01 02Sakshi SharmaNo ratings yet

- Final CaseDocument25 pagesFinal CaseSakshi SharmaNo ratings yet

- Cashflow Net Room RevenueDocument4 pagesCashflow Net Room RevenueAshadi CahyadiNo ratings yet

- Semi FinalDocument17 pagesSemi FinalJane TuazonNo ratings yet

- Partnership OperationsDocument9 pagesPartnership OperationsJay Mark Marcial JosolNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- LT344.CGSP(AL-I) Question CMA January-2023 Exam.Document2 pagesLT344.CGSP(AL-I) Question CMA January-2023 Exam.Shawn MehdiNo ratings yet

- CM121.COA(IL-I) Question CMA January-2023 Exam.Document7 pagesCM121.COA(IL-I) Question CMA January-2023 Exam.Shawn MehdiNo ratings yet

- LT125.CBL (IL-I) Solution CMA January-2023 ExamDocument1 pageLT125.CBL (IL-I) Solution CMA January-2023 ExamShawn MehdiNo ratings yet

- Advanced MGTDocument136 pagesAdvanced MGTShawn MehdiNo ratings yet

- CM231.MAC(IL-II) Question CMA January-2023 Exam.Document8 pagesCM231.MAC(IL-II) Question CMA January-2023 Exam.Shawn MehdiNo ratings yet

- Reference: Principles of ManagementDocument1 pageReference: Principles of ManagementShawn MehdiNo ratings yet

- AcknowledgementDocument1 pageAcknowledgementShawn MehdiNo ratings yet

- Table of Content: Topic NameDocument1 pageTable of Content: Topic NameShawn MehdiNo ratings yet

- Cover PageDocument1 pageCover PageShawn MehdiNo ratings yet

- Steps in Control Process in ManagementDocument10 pagesSteps in Control Process in ManagementShawn MehdiNo ratings yet

- Controlling Function of ManagementDocument1 pageControlling Function of ManagementShawn MehdiNo ratings yet

- ConclutionDocument1 pageConclutionShawn MehdiNo ratings yet

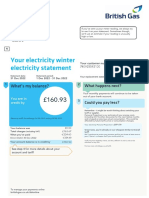

- Your Electricity Winter Electricity Statement: What's My Balance?Document1 pageYour Electricity Winter Electricity Statement: What's My Balance?Nikita TishchenkoNo ratings yet

- TAX-Chap 2-3 Question and AnswerDocument13 pagesTAX-Chap 2-3 Question and AnswerPoison Ivy100% (1)

- Direct Tax Summary NotesDocument88 pagesDirect Tax Summary NotesAlisha LukeNo ratings yet

- Chapter 8 Exclusions From Gross IncomeDocument4 pagesChapter 8 Exclusions From Gross IncomeMary Jane PabroaNo ratings yet

- Indian Income Tax Return Verification Form: Form Itr-V Assessment YearDocument1 pageIndian Income Tax Return Verification Form: Form Itr-V Assessment Yearaccount patnaNo ratings yet

- Challan 900 (08-03-2018)Document1 pageChallan 900 (08-03-2018)Shankey JAlanNo ratings yet

- Heads of Income Monthly Actual YTD Projected TotalDocument2 pagesHeads of Income Monthly Actual YTD Projected TotalDsr Santhosh KumarNo ratings yet

- ESOP Calculator IndiaDocument2 pagesESOP Calculator IndiajdonNo ratings yet

- Digital Banking: by Navdeep KaurDocument7 pagesDigital Banking: by Navdeep KaurNavdeep Kaur XII-ENo ratings yet

- Entertainment Tax in IndiaDocument3 pagesEntertainment Tax in IndiaEbne AkramNo ratings yet

- MT 940 Customer Statement Message (In SAP Format) .: Field 20: Transaction Reference NumberDocument6 pagesMT 940 Customer Statement Message (In SAP Format) .: Field 20: Transaction Reference NumberSuryanarayana TataNo ratings yet

- RPT Pay Slip NIIT1Document1 pageRPT Pay Slip NIIT1kingnilay9831No ratings yet

- RMC No 47-2019Document5 pagesRMC No 47-2019Renren QuiranteNo ratings yet

- Commonwealth Act Tax 466Document7 pagesCommonwealth Act Tax 466makulitkulit00No ratings yet

- E BusinessDocument28 pagesE BusinessSHADARE ABAYOMINo ratings yet

- Activating GST For Your CompanyDocument158 pagesActivating GST For Your CompanyTapas GhoshNo ratings yet

- TH THDocument3 pagesTH THBenidick PascuaNo ratings yet

- Accounting ProcessDocument6 pagesAccounting ProcessJen NerNo ratings yet

- Quiz 001 80%Document4 pagesQuiz 001 80%jrence0% (1)

- BillDocument7 pagesBillstanciucorinaioanaNo ratings yet

- CIR vs. Lednicky (1964)Document1 pageCIR vs. Lednicky (1964)Emil BautistaNo ratings yet

- Professional Abridgement Previous Organizational Highlights: Jindal Naturecure Institute, Bangalore, IndiaDocument3 pagesProfessional Abridgement Previous Organizational Highlights: Jindal Naturecure Institute, Bangalore, IndiaAdditya ChauhanNo ratings yet

- GGGDocument3 pagesGGGkasmir cidroNo ratings yet

- Paypal'S Seller Protection ProgramDocument6 pagesPaypal'S Seller Protection ProgramAxl Jose Cabrera VizcayaNo ratings yet

- Balance - RisexerDocument1 pageBalance - RisexerLaser002 RaackNo ratings yet

- Vintage Vision Int'L, Inc. Vintage Vision Int'L, Inc. Vintage Vision Int'L, IncDocument33 pagesVintage Vision Int'L, Inc. Vintage Vision Int'L, Inc. Vintage Vision Int'L, IncAvriLyn Palmero ELavigneNo ratings yet

- May-19-3084Document4 pagesMay-19-3084Rizvan MasroorNo ratings yet

- Manage Invoice Options - US1 Business UnitDocument2 pagesManage Invoice Options - US1 Business UnitI'm RangaNo ratings yet