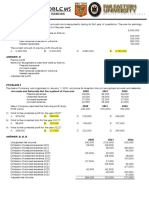

Ch 18 select problem solutions

Ch 18 select problem solutions

You might also like

- Test Bank For Taxation For Decision Makers 2020 10th Edition Shirley Dennis Escoffier Karen A Fortin DownloadDocument26 pagesTest Bank For Taxation For Decision Makers 2020 10th Edition Shirley Dennis Escoffier Karen A Fortin DownloadCrystalDavisibng100% (25)

- Acct2015 - 2021 Paper Final SolutionDocument128 pagesAcct2015 - 2021 Paper Final SolutionTan TaylorNo ratings yet

- Taxing Situations Two Cases On Income Taxes - An Accounting Case StudyDocument5 pagesTaxing Situations Two Cases On Income Taxes - An Accounting Case Studyfossaceca80% (5)

- Answer Key Chapters 1 7Document40 pagesAnswer Key Chapters 1 7Sheila Mae Guerta Lacerona74% (38)

- Ilovepdf MergedDocument100 pagesIlovepdf MergedVinny AujlaNo ratings yet

- Topic 3 Tutorial Questions PDFDocument15 pagesTopic 3 Tutorial Questions PDFKim FloresNo ratings yet

- f1 Cima Workbook Q & A PDFDocument276 pagesf1 Cima Workbook Q & A PDFYounus KhanNo ratings yet

- Chapter 6 SolutionsDocument31 pagesChapter 6 SolutionsHarsh Khandelwal67% (3)

- Model Solution: Page 1 of 6Document6 pagesModel Solution: Page 1 of 6ShuvonathNo ratings yet

- Template - Problem 18.1Document4 pagesTemplate - Problem 18.1dragonx0662No ratings yet

- Pricilla AssignmentDocument3 pagesPricilla AssignmentjasonnumahnalkelNo ratings yet

- Solutions Tax InvestigationDocument15 pagesSolutions Tax InvestigationWahida AmalinNo ratings yet

- Loan ReceivablesDocument3 pagesLoan ReceivablesAdam CuencaNo ratings yet

- Assignment 4 - SolutionsDocument2 pagesAssignment 4 - SolutionsstoryNo ratings yet

- The Institute of Chartered Accountants of Bangladesh: Sample Question Paper Certificate Level-AccountingDocument8 pagesThe Institute of Chartered Accountants of Bangladesh: Sample Question Paper Certificate Level-AccountingArif UddinNo ratings yet

- Tutorial 6 - Salaries TaxDocument5 pagesTutorial 6 - Salaries Tax周小荷No ratings yet

- Property, Plant, & Equipment Problem SetDocument3 pagesProperty, Plant, & Equipment Problem SetSarah Nicole S. LagrimasNo ratings yet

- CFASDocument4 pagesCFASAdam CuencaNo ratings yet

- Intacc2 Assignment 6.1 AnswersDocument6 pagesIntacc2 Assignment 6.1 AnswersMingNo ratings yet

- Lt234. Tvp. (Il-II) Solution Cma May-2023 Exam.Document5 pagesLt234. Tvp. (Il-II) Solution Cma May-2023 Exam.Arif HossainNo ratings yet

- Problems: Problem 12 - 2Document9 pagesProblems: Problem 12 - 2Jein PNo ratings yet

- Accounting Sample Question Along With A SolutionDocument17 pagesAccounting Sample Question Along With A SolutionNoor Mohammad Abu RaihanNo ratings yet

- REBYUDocument16 pagesREBYUChi EstrellaNo ratings yet

- Tutorial QuestionsDocument2 pagesTutorial QuestionsNishika KaranNo ratings yet

- Gov't Grant, Depreciation, Revaluation and ImpairmentDocument6 pagesGov't Grant, Depreciation, Revaluation and Impairment夜晨曦No ratings yet

- Tugas Penyelesaian 14 AIK - 0119101024 - Muhamad Adam Palmaleo - Kelas BDocument23 pagesTugas Penyelesaian 14 AIK - 0119101024 - Muhamad Adam Palmaleo - Kelas BAdam PalmaleoNo ratings yet

- BHMH2101 2023 Sem 2 Assignment 1 - Suggested AnswersDocument4 pagesBHMH2101 2023 Sem 2 Assignment 1 - Suggested Answerstsoi lam chanNo ratings yet

- August Q1Document3 pagesAugust Q1tengku rilNo ratings yet

- Contoh DTA DTLDocument23 pagesContoh DTA DTLZahra MawarNo ratings yet

- Valuation Final ExamDocument4 pagesValuation Final ExamJeane Mae Boo100% (1)

- UAS PA 2020-2021 Ganjil - JawabanDocument27 pagesUAS PA 2020-2021 Ganjil - JawabanNuruddin AsyifaNo ratings yet

- Auditing Problems: Ap - 01: Correction of ErrorsDocument15 pagesAuditing Problems: Ap - 01: Correction of ErrorsPrinces100% (2)

- EXAMPLE 12.1 (Current Tax Liability)Document8 pagesEXAMPLE 12.1 (Current Tax Liability)KaiWenNgNo ratings yet

- Assumptions - Assumptions - Financing: Year - 0 Year - 1 Year - 2 Year - 3 Year - 4Document2 pagesAssumptions - Assumptions - Financing: Year - 0 Year - 1 Year - 2 Year - 3 Year - 4PranshuNo ratings yet

- Cash FlowsDocument4 pagesCash FlowsAira Dane VillegasNo ratings yet

- Corrections: Suggested SolutionDocument5 pagesCorrections: Suggested SolutionZairah FranciscoNo ratings yet

- Illustrative Example Income TaxesDocument4 pagesIllustrative Example Income Taxes22700021maaeNo ratings yet

- Answers - Chapter 5 Vol 2Document5 pagesAnswers - Chapter 5 Vol 2jamfloxNo ratings yet

- Requirement 1 2023 2024 2025 2026Document17 pagesRequirement 1 2023 2024 2025 2026Soria Sophia AnnNo ratings yet

- Master Budgeting - Blades Pty LTDDocument14 pagesMaster Budgeting - Blades Pty LTDAdi KurniawanNo ratings yet

- Carry Over Next Period (Excl. Incentive)Document5 pagesCarry Over Next Period (Excl. Incentive)Divina BidarNo ratings yet

- Cashflow Solutions Q2Document7 pagesCashflow Solutions Q2calliemozartNo ratings yet

- Poa Mock Exam 2020Document13 pagesPoa Mock Exam 2020DanNo ratings yet

- Problem 7 - 6 & 7Document2 pagesProblem 7 - 6 & 7Micah April SabularseNo ratings yet

- Financial Position For The Year Ending 30/6/2009: Bank AccountDocument19 pagesFinancial Position For The Year Ending 30/6/2009: Bank Accountapi-26147386No ratings yet

- Fa July2023-Far210-StudentDocument9 pagesFa July2023-Far210-Student2022613976No ratings yet

- Quiz Accounting For Income TaxDocument5 pagesQuiz Accounting For Income TaxCmNo ratings yet

- Afar JNDocument2 pagesAfar JNjasonnumahnalkelNo ratings yet

- F1. FIOO.P December 2020Document6 pagesF1. FIOO.P December 2020Laskar REAZNo ratings yet

- Project and Risk AnalysisDocument2 pagesProject and Risk AnalysisvipukNo ratings yet

- LT234.TPF(I-II) Solution CMA January-2023 ExamDocument6 pagesLT234.TPF(I-II) Solution CMA January-2023 ExamShawn MehdiNo ratings yet

- ACCT 204 - Chapter 3 AssignmentDocument1 pageACCT 204 - Chapter 3 Assignmentkarinedwards473No ratings yet

- 3rd BSA 3-1 Subject AsssessmentDocument224 pages3rd BSA 3-1 Subject AsssessmentChristen HerceNo ratings yet

- Afni Sumedi Purba - 003 - EA-G - Tugas AKM 2 CH 20Document13 pagesAfni Sumedi Purba - 003 - EA-G - Tugas AKM 2 CH 20Afni Sumedi PurbaNo ratings yet

- FIRST PB FAR Solutions PDFDocument6 pagesFIRST PB FAR Solutions PDFStephanie Joy NogollosNo ratings yet

- Poa Mock Exam 2020Document13 pagesPoa Mock Exam 2020DanNo ratings yet

- Receivables Morning Star Corporation: I Will Manually Check Your Answer For Rounding Off DifferencesDocument3 pagesReceivables Morning Star Corporation: I Will Manually Check Your Answer For Rounding Off DifferencesGlance BautistaNo ratings yet

- STT - Mock - Test - S-24 - Suggested AnswersDocument8 pagesSTT - Mock - Test - S-24 - Suggested AnswersabdullahNo ratings yet

- Far Situational Solution-1Document6 pagesFar Situational Solution-1Baby BearNo ratings yet

- R2. TAX ML Solution CMA January 2022 ExaminationDocument6 pagesR2. TAX ML Solution CMA January 2022 ExaminationPavel DhakaNo ratings yet

- F7 SolutionsDocument15 pagesF7 Solutionsnoor ul anum100% (1)

- 2018 Mayors Budget Release Copy 072717Document55 pages2018 Mayors Budget Release Copy 072717kristin frechetteNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionNo ratings yet

- Ch 17 select problem solutionsDocument11 pagesCh 17 select problem solutionsJannit CarasscoNo ratings yet

- ByrdChen2022_Ch05_SSPDocument7 pagesByrdChen2022_Ch05_SSPJannit CarasscoNo ratings yet

- ByrdChen2022_Ch06_SSPDocument16 pagesByrdChen2022_Ch06_SSPJannit CarasscoNo ratings yet

- CN Non-Financial and Current LiabilitiesDocument3 pagesCN Non-Financial and Current LiabilitiesJannit CarasscoNo ratings yet

- Guide To Accounting For Income Taxes NewDocument620 pagesGuide To Accounting For Income Taxes NewRahul Modi100% (1)

- Business Analysis and Valuation Quiz (10%)Document6 pagesBusiness Analysis and Valuation Quiz (10%)Evelyn AngNo ratings yet

- Beximco Pharmaceuticals Limited Statement of Financial PositionDocument55 pagesBeximco Pharmaceuticals Limited Statement of Financial Positionrimon dasNo ratings yet

- Pfizer Exam Solution ManualDocument25 pagesPfizer Exam Solution ManualDiego AguirreNo ratings yet

- Chapter 1 - Income TaxDocument30 pagesChapter 1 - Income TaxQuỳnh Anh NguyễnNo ratings yet

- Pas 12Document2 pagesPas 12JennicaBailonNo ratings yet

- Discontinuing Operations: Accounting Standard (AS) 24Document20 pagesDiscontinuing Operations: Accounting Standard (AS) 24johnsondevasia80No ratings yet

- Assignment #II - FinalDocument5 pagesAssignment #II - FinalthanNo ratings yet

- Far 8 Income TaxesDocument15 pagesFar 8 Income TaxesChesterTVNo ratings yet

- CTG - Simulated Exam FAR (2nd CE May 2017)Document8 pagesCTG - Simulated Exam FAR (2nd CE May 2017)Lowelle PacotNo ratings yet

- Fac4863 104 - 2020 - 0 - BDocument93 pagesFac4863 104 - 2020 - 0 - BNISSIBETINo ratings yet

- PAS 12 INCOME TAXES Cont With ProbsDocument8 pagesPAS 12 INCOME TAXES Cont With ProbsFabrienne Kate Eugenio Liberato100% (1)

- Matching Principle and Accrual Basis of AccountingDocument2 pagesMatching Principle and Accrual Basis of AccountingNazish KhalidNo ratings yet

- P22Document64 pagesP22Adnan MemonNo ratings yet

- Auditing Problem Final Exam With Answer Only, No SolutionDocument23 pagesAuditing Problem Final Exam With Answer Only, No SolutionRheu Reyes100% (1)

- Materi - INCOME TAX ACCOUNTING - 26march2021Document18 pagesMateri - INCOME TAX ACCOUNTING - 26march2021Septian Dwi AnggoroNo ratings yet

- The Accounting Records of Steven Corp A Real Estate Developer PDFDocument2 pagesThe Accounting Records of Steven Corp A Real Estate Developer PDFFreelance WorkerNo ratings yet

- Chapter 14Document40 pagesChapter 14Ivo_NichtNo ratings yet

- Hindustan Construction Co LTDDocument39 pagesHindustan Construction Co LTDLubdh PandaNo ratings yet

- Aurobindo Mar20Document10 pagesAurobindo Mar20free meNo ratings yet

- Chapter 4 - Accounting For Other LiabilitiesDocument21 pagesChapter 4 - Accounting For Other Liabilitiesjeanette lampitoc0% (1)

- Honda Cars India Limited: Detailed ReportDocument14 pagesHonda Cars India Limited: Detailed Reportb0gm3n0tNo ratings yet

- Income Taxes: ProblemsDocument12 pagesIncome Taxes: ProblemsCharles MateoNo ratings yet

- Master Budgets and Performance Planning: QuestionsDocument67 pagesMaster Budgets and Performance Planning: QuestionsFrances Nicole MuldongNo ratings yet

- FR Expected-Questions Nov-2022 B-CategoryDocument117 pagesFR Expected-Questions Nov-2022 B-CategorySrihariNo ratings yet

Download as pdf or txt

You might also like

- Test Bank For Taxation For Decision Makers 2020 10th Edition Shirley Dennis Escoffier Karen A Fortin DownloadDocument26 pagesTest Bank For Taxation For Decision Makers 2020 10th Edition Shirley Dennis Escoffier Karen A Fortin DownloadCrystalDavisibng100% (25)

- Acct2015 - 2021 Paper Final SolutionDocument128 pagesAcct2015 - 2021 Paper Final SolutionTan TaylorNo ratings yet

- Taxing Situations Two Cases On Income Taxes - An Accounting Case StudyDocument5 pagesTaxing Situations Two Cases On Income Taxes - An Accounting Case Studyfossaceca80% (5)

- Answer Key Chapters 1 7Document40 pagesAnswer Key Chapters 1 7Sheila Mae Guerta Lacerona74% (38)

- Ilovepdf MergedDocument100 pagesIlovepdf MergedVinny AujlaNo ratings yet

- Topic 3 Tutorial Questions PDFDocument15 pagesTopic 3 Tutorial Questions PDFKim FloresNo ratings yet

- f1 Cima Workbook Q & A PDFDocument276 pagesf1 Cima Workbook Q & A PDFYounus KhanNo ratings yet

- Chapter 6 SolutionsDocument31 pagesChapter 6 SolutionsHarsh Khandelwal67% (3)

- Model Solution: Page 1 of 6Document6 pagesModel Solution: Page 1 of 6ShuvonathNo ratings yet

- Template - Problem 18.1Document4 pagesTemplate - Problem 18.1dragonx0662No ratings yet

- Pricilla AssignmentDocument3 pagesPricilla AssignmentjasonnumahnalkelNo ratings yet

- Solutions Tax InvestigationDocument15 pagesSolutions Tax InvestigationWahida AmalinNo ratings yet

- Loan ReceivablesDocument3 pagesLoan ReceivablesAdam CuencaNo ratings yet

- Assignment 4 - SolutionsDocument2 pagesAssignment 4 - SolutionsstoryNo ratings yet

- The Institute of Chartered Accountants of Bangladesh: Sample Question Paper Certificate Level-AccountingDocument8 pagesThe Institute of Chartered Accountants of Bangladesh: Sample Question Paper Certificate Level-AccountingArif UddinNo ratings yet

- Tutorial 6 - Salaries TaxDocument5 pagesTutorial 6 - Salaries Tax周小荷No ratings yet

- Property, Plant, & Equipment Problem SetDocument3 pagesProperty, Plant, & Equipment Problem SetSarah Nicole S. LagrimasNo ratings yet

- CFASDocument4 pagesCFASAdam CuencaNo ratings yet

- Intacc2 Assignment 6.1 AnswersDocument6 pagesIntacc2 Assignment 6.1 AnswersMingNo ratings yet

- Lt234. Tvp. (Il-II) Solution Cma May-2023 Exam.Document5 pagesLt234. Tvp. (Il-II) Solution Cma May-2023 Exam.Arif HossainNo ratings yet

- Problems: Problem 12 - 2Document9 pagesProblems: Problem 12 - 2Jein PNo ratings yet

- Accounting Sample Question Along With A SolutionDocument17 pagesAccounting Sample Question Along With A SolutionNoor Mohammad Abu RaihanNo ratings yet

- REBYUDocument16 pagesREBYUChi EstrellaNo ratings yet

- Tutorial QuestionsDocument2 pagesTutorial QuestionsNishika KaranNo ratings yet

- Gov't Grant, Depreciation, Revaluation and ImpairmentDocument6 pagesGov't Grant, Depreciation, Revaluation and Impairment夜晨曦No ratings yet

- Tugas Penyelesaian 14 AIK - 0119101024 - Muhamad Adam Palmaleo - Kelas BDocument23 pagesTugas Penyelesaian 14 AIK - 0119101024 - Muhamad Adam Palmaleo - Kelas BAdam PalmaleoNo ratings yet

- BHMH2101 2023 Sem 2 Assignment 1 - Suggested AnswersDocument4 pagesBHMH2101 2023 Sem 2 Assignment 1 - Suggested Answerstsoi lam chanNo ratings yet

- August Q1Document3 pagesAugust Q1tengku rilNo ratings yet

- Contoh DTA DTLDocument23 pagesContoh DTA DTLZahra MawarNo ratings yet

- Valuation Final ExamDocument4 pagesValuation Final ExamJeane Mae Boo100% (1)

- UAS PA 2020-2021 Ganjil - JawabanDocument27 pagesUAS PA 2020-2021 Ganjil - JawabanNuruddin AsyifaNo ratings yet

- Auditing Problems: Ap - 01: Correction of ErrorsDocument15 pagesAuditing Problems: Ap - 01: Correction of ErrorsPrinces100% (2)

- EXAMPLE 12.1 (Current Tax Liability)Document8 pagesEXAMPLE 12.1 (Current Tax Liability)KaiWenNgNo ratings yet

- Assumptions - Assumptions - Financing: Year - 0 Year - 1 Year - 2 Year - 3 Year - 4Document2 pagesAssumptions - Assumptions - Financing: Year - 0 Year - 1 Year - 2 Year - 3 Year - 4PranshuNo ratings yet

- Cash FlowsDocument4 pagesCash FlowsAira Dane VillegasNo ratings yet

- Corrections: Suggested SolutionDocument5 pagesCorrections: Suggested SolutionZairah FranciscoNo ratings yet

- Illustrative Example Income TaxesDocument4 pagesIllustrative Example Income Taxes22700021maaeNo ratings yet

- Answers - Chapter 5 Vol 2Document5 pagesAnswers - Chapter 5 Vol 2jamfloxNo ratings yet

- Requirement 1 2023 2024 2025 2026Document17 pagesRequirement 1 2023 2024 2025 2026Soria Sophia AnnNo ratings yet

- Master Budgeting - Blades Pty LTDDocument14 pagesMaster Budgeting - Blades Pty LTDAdi KurniawanNo ratings yet

- Carry Over Next Period (Excl. Incentive)Document5 pagesCarry Over Next Period (Excl. Incentive)Divina BidarNo ratings yet

- Cashflow Solutions Q2Document7 pagesCashflow Solutions Q2calliemozartNo ratings yet

- Poa Mock Exam 2020Document13 pagesPoa Mock Exam 2020DanNo ratings yet

- Problem 7 - 6 & 7Document2 pagesProblem 7 - 6 & 7Micah April SabularseNo ratings yet

- Financial Position For The Year Ending 30/6/2009: Bank AccountDocument19 pagesFinancial Position For The Year Ending 30/6/2009: Bank Accountapi-26147386No ratings yet

- Fa July2023-Far210-StudentDocument9 pagesFa July2023-Far210-Student2022613976No ratings yet

- Quiz Accounting For Income TaxDocument5 pagesQuiz Accounting For Income TaxCmNo ratings yet

- Afar JNDocument2 pagesAfar JNjasonnumahnalkelNo ratings yet

- F1. FIOO.P December 2020Document6 pagesF1. FIOO.P December 2020Laskar REAZNo ratings yet

- Project and Risk AnalysisDocument2 pagesProject and Risk AnalysisvipukNo ratings yet

- LT234.TPF(I-II) Solution CMA January-2023 ExamDocument6 pagesLT234.TPF(I-II) Solution CMA January-2023 ExamShawn MehdiNo ratings yet

- ACCT 204 - Chapter 3 AssignmentDocument1 pageACCT 204 - Chapter 3 Assignmentkarinedwards473No ratings yet

- 3rd BSA 3-1 Subject AsssessmentDocument224 pages3rd BSA 3-1 Subject AsssessmentChristen HerceNo ratings yet

- Afni Sumedi Purba - 003 - EA-G - Tugas AKM 2 CH 20Document13 pagesAfni Sumedi Purba - 003 - EA-G - Tugas AKM 2 CH 20Afni Sumedi PurbaNo ratings yet

- FIRST PB FAR Solutions PDFDocument6 pagesFIRST PB FAR Solutions PDFStephanie Joy NogollosNo ratings yet

- Poa Mock Exam 2020Document13 pagesPoa Mock Exam 2020DanNo ratings yet

- Receivables Morning Star Corporation: I Will Manually Check Your Answer For Rounding Off DifferencesDocument3 pagesReceivables Morning Star Corporation: I Will Manually Check Your Answer For Rounding Off DifferencesGlance BautistaNo ratings yet

- STT - Mock - Test - S-24 - Suggested AnswersDocument8 pagesSTT - Mock - Test - S-24 - Suggested AnswersabdullahNo ratings yet

- Far Situational Solution-1Document6 pagesFar Situational Solution-1Baby BearNo ratings yet

- R2. TAX ML Solution CMA January 2022 ExaminationDocument6 pagesR2. TAX ML Solution CMA January 2022 ExaminationPavel DhakaNo ratings yet

- F7 SolutionsDocument15 pagesF7 Solutionsnoor ul anum100% (1)

- 2018 Mayors Budget Release Copy 072717Document55 pages2018 Mayors Budget Release Copy 072717kristin frechetteNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionNo ratings yet

- Ch 17 select problem solutionsDocument11 pagesCh 17 select problem solutionsJannit CarasscoNo ratings yet

- ByrdChen2022_Ch05_SSPDocument7 pagesByrdChen2022_Ch05_SSPJannit CarasscoNo ratings yet

- ByrdChen2022_Ch06_SSPDocument16 pagesByrdChen2022_Ch06_SSPJannit CarasscoNo ratings yet

- CN Non-Financial and Current LiabilitiesDocument3 pagesCN Non-Financial and Current LiabilitiesJannit CarasscoNo ratings yet

- Guide To Accounting For Income Taxes NewDocument620 pagesGuide To Accounting For Income Taxes NewRahul Modi100% (1)

- Business Analysis and Valuation Quiz (10%)Document6 pagesBusiness Analysis and Valuation Quiz (10%)Evelyn AngNo ratings yet

- Beximco Pharmaceuticals Limited Statement of Financial PositionDocument55 pagesBeximco Pharmaceuticals Limited Statement of Financial Positionrimon dasNo ratings yet

- Pfizer Exam Solution ManualDocument25 pagesPfizer Exam Solution ManualDiego AguirreNo ratings yet

- Chapter 1 - Income TaxDocument30 pagesChapter 1 - Income TaxQuỳnh Anh NguyễnNo ratings yet

- Pas 12Document2 pagesPas 12JennicaBailonNo ratings yet

- Discontinuing Operations: Accounting Standard (AS) 24Document20 pagesDiscontinuing Operations: Accounting Standard (AS) 24johnsondevasia80No ratings yet

- Assignment #II - FinalDocument5 pagesAssignment #II - FinalthanNo ratings yet

- Far 8 Income TaxesDocument15 pagesFar 8 Income TaxesChesterTVNo ratings yet

- CTG - Simulated Exam FAR (2nd CE May 2017)Document8 pagesCTG - Simulated Exam FAR (2nd CE May 2017)Lowelle PacotNo ratings yet

- Fac4863 104 - 2020 - 0 - BDocument93 pagesFac4863 104 - 2020 - 0 - BNISSIBETINo ratings yet

- PAS 12 INCOME TAXES Cont With ProbsDocument8 pagesPAS 12 INCOME TAXES Cont With ProbsFabrienne Kate Eugenio Liberato100% (1)

- Matching Principle and Accrual Basis of AccountingDocument2 pagesMatching Principle and Accrual Basis of AccountingNazish KhalidNo ratings yet

- P22Document64 pagesP22Adnan MemonNo ratings yet

- Auditing Problem Final Exam With Answer Only, No SolutionDocument23 pagesAuditing Problem Final Exam With Answer Only, No SolutionRheu Reyes100% (1)

- Materi - INCOME TAX ACCOUNTING - 26march2021Document18 pagesMateri - INCOME TAX ACCOUNTING - 26march2021Septian Dwi AnggoroNo ratings yet

- The Accounting Records of Steven Corp A Real Estate Developer PDFDocument2 pagesThe Accounting Records of Steven Corp A Real Estate Developer PDFFreelance WorkerNo ratings yet

- Chapter 14Document40 pagesChapter 14Ivo_NichtNo ratings yet

- Hindustan Construction Co LTDDocument39 pagesHindustan Construction Co LTDLubdh PandaNo ratings yet

- Aurobindo Mar20Document10 pagesAurobindo Mar20free meNo ratings yet

- Chapter 4 - Accounting For Other LiabilitiesDocument21 pagesChapter 4 - Accounting For Other Liabilitiesjeanette lampitoc0% (1)

- Honda Cars India Limited: Detailed ReportDocument14 pagesHonda Cars India Limited: Detailed Reportb0gm3n0tNo ratings yet

- Income Taxes: ProblemsDocument12 pagesIncome Taxes: ProblemsCharles MateoNo ratings yet

- Master Budgets and Performance Planning: QuestionsDocument67 pagesMaster Budgets and Performance Planning: QuestionsFrances Nicole MuldongNo ratings yet

- FR Expected-Questions Nov-2022 B-CategoryDocument117 pagesFR Expected-Questions Nov-2022 B-CategorySrihariNo ratings yet