Download as pdf or txt

You might also like

- Mathematics: Paper 2 (Calculator) Higher TierDocument20 pagesMathematics: Paper 2 (Calculator) Higher TieramnaNo ratings yet

- Biblical Values in HRMDocument26 pagesBiblical Values in HRMscona79100% (4)

- Inventory ManagementDocument26 pagesInventory ManagementIbrar ShabbirNo ratings yet

- Ma Am+saira s+Tutorial+Slides-Chap+6+-+Inventories PDFDocument17 pagesMa Am+saira s+Tutorial+Slides-Chap+6+-+Inventories PDFAli Zain ParharNo ratings yet

- Inventory Reviewer PDFDocument2 pagesInventory Reviewer PDFAina AguirreNo ratings yet

- Class No 14 & 15Document31 pagesClass No 14 & 15WILD๛SHOTッ tanvirNo ratings yet

- Inventories SPC PDFDocument8 pagesInventories SPC PDFAshish VermaNo ratings yet

- Inventory ManagementDocument9 pagesInventory ManagementLeo RajNo ratings yet

- Mgt101-15 - Accounting For InventoriesDocument69 pagesMgt101-15 - Accounting For InventoriesHaris AliNo ratings yet

- TOPIC 1 Accounting For InventoryDocument9 pagesTOPIC 1 Accounting For Inventorykirah raraNo ratings yet

- InventoryDocument16 pagesInventorySharif HassanNo ratings yet

- Chapter 4 InventoriesDocument9 pagesChapter 4 InventoriesMushar AliNo ratings yet

- Charts On AS by Rohan Sir VSMART ACADEMY PDFDocument36 pagesCharts On AS by Rohan Sir VSMART ACADEMY PDFAejaz Mohamed86% (7)

- Pertemuan 6 - Persediaan - Periodik Fifo AverageDocument13 pagesPertemuan 6 - Persediaan - Periodik Fifo Averageelhm234No ratings yet

- Study Text Cma Caf 3Document606 pagesStudy Text Cma Caf 3Muhammad KashifNo ratings yet

- ACCT1111 Chapter 6 Lecture (Revised)Document63 pagesACCT1111 Chapter 6 Lecture (Revised)Wky JimNo ratings yet

- PAS 2 InventoriesDocument16 pagesPAS 2 Inventoriesjan petosilNo ratings yet

- EOQ - Accounting For MaterialsDocument18 pagesEOQ - Accounting For MaterialsZainab ImranNo ratings yet

- A2 Sample Chapter Inventory Valuation PDFDocument19 pagesA2 Sample Chapter Inventory Valuation PDFRafa BentolilaNo ratings yet

- Module 7 13 No 11Document6 pagesModule 7 13 No 11LEIGHANNE ZYRIL SANTOSNo ratings yet

- C3 - Accounting For InventoriesDocument95 pagesC3 - Accounting For InventoriesHồ ThảoNo ratings yet

- InventoriesDocument3 pagesInventoriesNikki RañolaNo ratings yet

- 1-Working CapitalDocument13 pages1-Working CapitalAwaiZ zahidNo ratings yet

- Chapter 9 Inventory Management Teaching StudentDocument62 pagesChapter 9 Inventory Management Teaching StudentMUHAMMAD SYAFIQ ABDUL HALIMNo ratings yet

- Warehousing Fundamentals DTTDocument53 pagesWarehousing Fundamentals DTTripc95No ratings yet

- Chapter 6 - Reporting and Analyzing InventoryDocument13 pagesChapter 6 - Reporting and Analyzing InventoryCông Hoàng ĐìnhNo ratings yet

- InventoriesDocument26 pagesInventoriesAj Nicole GumsatNo ratings yet

- Pas 2 InventoriesDocument12 pagesPas 2 InventoriesLETIGIO, RHEANA ROSE M.100% (1)

- Charts On As by Rohan Sir Vsmart AcademyDocument15 pagesCharts On As by Rohan Sir Vsmart AcademyNarend SinghNo ratings yet

- Inventory Lecture NotesDocument9 pagesInventory Lecture NotesMinh ThưNo ratings yet

- Inventory Lecture Notes PDFDocument9 pagesInventory Lecture Notes PDFMinh ThưNo ratings yet

- Pas 2 InventoriesDocument13 pagesPas 2 InventoriesRoxanne GiananNo ratings yet

- Cost Accounting Chapters 1&2Document7 pagesCost Accounting Chapters 1&2ralfgerwin inesaNo ratings yet

- Inventory PDFDocument7 pagesInventory PDFJose De CuentasNo ratings yet

- Materials PDFDocument23 pagesMaterials PDFmathewsem04112006No ratings yet

- Om ReviewerDocument14 pagesOm ReviewerPippsie MalganaNo ratings yet

- Inventory Management PDFDocument49 pagesInventory Management PDFVyVyNo ratings yet

- CA Inter Accounting Revision NotesDocument106 pagesCA Inter Accounting Revision NoteskalyanikamineniNo ratings yet

- Full download Financial ACCT2 2nd Edition Godwin Solutions Manual all chapter 2024 pdfDocument44 pagesFull download Financial ACCT2 2nd Edition Godwin Solutions Manual all chapter 2024 pdfzaimechbili100% (8)

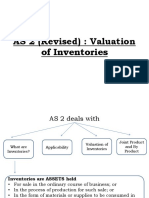

- AS 2 (Revised) : Valuation of InventoriesDocument13 pagesAS 2 (Revised) : Valuation of InventoriesAkshay PatilNo ratings yet

- CH 8 - AnswerDocument58 pagesCH 8 - Answer金沛霓No ratings yet

- Chapter 1, InventoriesDocument18 pagesChapter 1, InventoriesAmsaluNo ratings yet

- Inventory AccountingDocument27 pagesInventory AccountingAbinash Mishra100% (1)

- Inventory AccountingDocument27 pagesInventory AccountingMr. PsychoNo ratings yet

- Marathon Batch Final With Cover and Index PDFDocument106 pagesMarathon Batch Final With Cover and Index PDFChandreshNo ratings yet

- Persediaan (Inventories) : AccountingDocument66 pagesPersediaan (Inventories) : AccountingMuhammad IrsyadNo ratings yet

- OPERATIONS-MANAGEMENT PPT - UPDATED-1 NewDocument17 pagesOPERATIONS-MANAGEMENT PPT - UPDATED-1 NewSurbhi BidviNo ratings yet

- Accounting StandardsDocument56 pagesAccounting StandardsAkshay KumarNo ratings yet

- Week 02 - Valuation of Stock - SDocument4 pagesWeek 02 - Valuation of Stock - STeresa ManNo ratings yet

- TradeGecko Inventory Management Getting StartedDocument14 pagesTradeGecko Inventory Management Getting StartedranadheerarrowNo ratings yet

- Inventory Management21Document76 pagesInventory Management21Sayem SadatNo ratings yet

- Cost of Sales & InventoriesDocument17 pagesCost of Sales & InventoriesShashank100% (1)

- Chapter 2 Inventories For UseDocument18 pagesChapter 2 Inventories For UseawlachewNo ratings yet

- Inventory Valuation 1Document30 pagesInventory Valuation 1Wings MoviesNo ratings yet

- CH # 07 To 10 RevisionDocument61 pagesCH # 07 To 10 RevisionAbdul SalamNo ratings yet

- Inventory Management Unit-3Document41 pagesInventory Management Unit-3rohit singhNo ratings yet

- AUD 2 InventoryDocument25 pagesAUD 2 InventoryJayron NonguiNo ratings yet

- Kuldeep10119015pi 131028193336 Phpapp01Document23 pagesKuldeep10119015pi 131028193336 Phpapp01vini2710No ratings yet

- Stock ValuationDocument18 pagesStock Valuationdurgesh choudharyNo ratings yet

- Internal Control of Fixed Assets: A Controller and Auditor's GuideFrom EverandInternal Control of Fixed Assets: A Controller and Auditor's GuideRating: 4 out of 5 stars4/5 (1)

- CP Session 4Document1 pageCP Session 4amnaNo ratings yet

- Chap 11_Corporation_Part IDocument11 pagesChap 11_Corporation_Part IamnaNo ratings yet

- CH 14Document26 pagesCH 14amnaNo ratings yet

- Islamic CP Session 7Document1 pageIslamic CP Session 7amnaNo ratings yet

- Row ID Order ID Order Date Ship Date Ship Mode Customer IDDocument77 pagesRow ID Order ID Order Date Ship Date Ship Mode Customer IDamnaNo ratings yet

- CP Session 8Document1 pageCP Session 8amnaNo ratings yet

- CP Session 10Document1 pageCP Session 10amnaNo ratings yet

- Adorno and HorkheimerDocument5 pagesAdorno and HorkheimeramnaNo ratings yet

- Document 26Document2 pagesDocument 26amnaNo ratings yet

- TB Nurse Case Studies Training Tool 609505 7Document110 pagesTB Nurse Case Studies Training Tool 609505 7amnaNo ratings yet

- The Dagger SceneDocument2 pagesThe Dagger Sceneamna100% (1)

- Porter SceneDocument2 pagesPorter SceneamnaNo ratings yet

- Soliloquy Act 5 Scene 5Document1 pageSoliloquy Act 5 Scene 5amna100% (1)

- Act 2 Scene 3 Lines 87 To 103Document1 pageAct 2 Scene 3 Lines 87 To 103amnaNo ratings yet

- Poetry Analysis 2 La BelleDocument3 pagesPoetry Analysis 2 La BelleamnaNo ratings yet

- GCSE 1MA1 Paper 3H (Mock Set 2)Document20 pagesGCSE 1MA1 Paper 3H (Mock Set 2)amnaNo ratings yet

- GCSE 1MA1 Paper 2H (Mock Set 2) PDFDocument24 pagesGCSE 1MA1 Paper 2H (Mock Set 2) PDFamnaNo ratings yet

- Mathematics: Pearson Edexcel Functional SkillsDocument20 pagesMathematics: Pearson Edexcel Functional SkillsamnaNo ratings yet

- Act 1 Scene 7 Macbeth SoliquyDocument2 pagesAct 1 Scene 7 Macbeth SoliquyamnaNo ratings yet

- GCSE 1MA1 Paper 2H (Mock Set 2) PDFDocument24 pagesGCSE 1MA1 Paper 2H (Mock Set 2) PDFamnaNo ratings yet

- Big Data Analytics - National Occupational Accident and Disease Statistics 2021Document9 pagesBig Data Analytics - National Occupational Accident and Disease Statistics 2021MuhamadSadiqNo ratings yet

- PGP: Marketing Management: Prof. Siddharth Shekhar SinghDocument46 pagesPGP: Marketing Management: Prof. Siddharth Shekhar SinghAnyone SomeoneNo ratings yet

- TDS On Real Estate Transactions: Flow of DiscussionDocument32 pagesTDS On Real Estate Transactions: Flow of DiscussionANILNo ratings yet

- Banana WarDocument94 pagesBanana Warcendy.rosal17No ratings yet

- Understanding Lump SumDocument2 pagesUnderstanding Lump SumYhamNo ratings yet

- Sample Flow ChartDocument26 pagesSample Flow Chartalejandra_giraldo_3100% (4)

- COSO ERM Creating and Protecting Value PDFDocument36 pagesCOSO ERM Creating and Protecting Value PDFKevinNo ratings yet

- Risk Control Self Assessment (RCSA) : 4th Annual Operational Risk Management ForumDocument9 pagesRisk Control Self Assessment (RCSA) : 4th Annual Operational Risk Management ForumTejendrasinh GohilNo ratings yet

- Unit 8: Accounting For Spoilage, Reworked Units and Scrap ContentDocument26 pagesUnit 8: Accounting For Spoilage, Reworked Units and Scrap Contentዝምታ ተሻለ0% (1)

- CH1Uber Case QuestionsDocument3 pagesCH1Uber Case QuestionsMiguel AguirreNo ratings yet

- To All Pharmacy Institutions Approved U/s 12 of The Pharmacy ActDocument9 pagesTo All Pharmacy Institutions Approved U/s 12 of The Pharmacy ActYorest CapsulesNo ratings yet

- Shreyas DM ProfileDocument1 pageShreyas DM ProfilepranavNo ratings yet

- Statement of Account: Brittany Executive Village Ii B5 L16 San Isidro (Pob.) City of Antipolo RizalDocument1 pageStatement of Account: Brittany Executive Village Ii B5 L16 San Isidro (Pob.) City of Antipolo RizalJames Bryan Garcia SolimanNo ratings yet

- Business Model Innovation in The Digital AgeDocument12 pagesBusiness Model Innovation in The Digital AgeRubi ZimmermanNo ratings yet

- Tugas Bahasa Inggris MemoDocument5 pagesTugas Bahasa Inggris MemoNur AyuNo ratings yet

- Leah Shitabule Attachment ReportDocument17 pagesLeah Shitabule Attachment ReportOdawa JohnNo ratings yet

- FM 1610 DI Pipe and Fittings, Flexible Fittings and Couplings 2016Document23 pagesFM 1610 DI Pipe and Fittings, Flexible Fittings and Couplings 2016andyNo ratings yet

- Jmfl-Policybazaar Ic 161121Document31 pagesJmfl-Policybazaar Ic 161121Santosh RoutNo ratings yet

- Duolingo - Q2 2022 Shareholder LetterDocument25 pagesDuolingo - Q2 2022 Shareholder LetterGiancarlo ChioratoNo ratings yet

- Aramco: 1 Running Heading: AramacoDocument6 pagesAramco: 1 Running Heading: AramacoAhmed IsmailNo ratings yet

- The Industrial Disputes ActDocument5 pagesThe Industrial Disputes ActvaibhavNo ratings yet

- Chase Bank Statement Template (1) 2 - PDF - Cheque - Deposit AccountDocument1 pageChase Bank Statement Template (1) 2 - PDF - Cheque - Deposit AccountworldwidelpcleNo ratings yet

- Pengaruh Kualitas Pelayanan, Harga Dan Lokasi Terhadap Kepuasan Pelanggan Cafe MilkmooDocument20 pagesPengaruh Kualitas Pelayanan, Harga Dan Lokasi Terhadap Kepuasan Pelanggan Cafe MilkmooRobert SeranNo ratings yet

- Line-X: Paint BoothDocument15 pagesLine-X: Paint BoothYasir ButtNo ratings yet

- IHRM Notes 1Document57 pagesIHRM Notes 1Anitha ONo ratings yet

- What Is HR ConsultingDocument2 pagesWhat Is HR ConsultingRustashNo ratings yet

- ch18 Derivatives and Risk ManagementDocument32 pagesch18 Derivatives and Risk ManagementGonzalo Jr. RualesNo ratings yet

- JIS School FeesDocument4 pagesJIS School FeesAgnesNo ratings yet

- Elites Holdings Company's ProfileDocument41 pagesElites Holdings Company's Profilespacegeek145No ratings yet