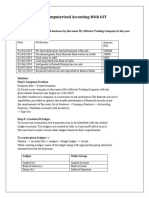

Introduction to the History of Double Entry

Introduction to the History of Double Entry

You might also like

- Group 1: Rafael Ramos Qaiser Bueno Kimverly Solis Antonio Jabson Xena Molato Kristzen LegaspiDocument7 pagesGroup 1: Rafael Ramos Qaiser Bueno Kimverly Solis Antonio Jabson Xena Molato Kristzen LegaspiReymsoNo ratings yet

- History of Accounting-WPS OfficeDocument10 pagesHistory of Accounting-WPS OfficeLea PasquinNo ratings yet

- Accounting History: Arithmetica, Geometria, Proportioni Et Proportionalita. of Course, Businesses and GovernmentsDocument11 pagesAccounting History: Arithmetica, Geometria, Proportioni Et Proportionalita. of Course, Businesses and GovernmentsPaul GeorgeNo ratings yet

- History of AccountingDocument4 pagesHistory of AccountingFaith Claire100% (2)

- Group 2 Presentation Acc 304Document22 pagesGroup 2 Presentation Acc 304iconkinging0No ratings yet

- Elective P.TDocument3 pagesElective P.TLuna LedezmaNo ratings yet

- Basic Accounting Summary Lecture-101-08!31!22Document3 pagesBasic Accounting Summary Lecture-101-08!31!22Roxane EsabinianoNo ratings yet

- 1.meaning of AccountingDocument21 pages1.meaning of AccountingNafe Singh YadavNo ratings yet

- Accounting and The Hospitality ManagerDocument27 pagesAccounting and The Hospitality ManagerPERALTA, ELISHA PREYANKANo ratings yet

- Smith Luca Pacioli Web Article REVISED 2018Document13 pagesSmith Luca Pacioli Web Article REVISED 2018JeremiahNo ratings yet

- Chapter 1-Textbook (Accounting An Introduction)Document13 pagesChapter 1-Textbook (Accounting An Introduction)Jimmy MulokoshiNo ratings yet

- Conceptual Development of Accounting: A Historical PerspectiveDocument11 pagesConceptual Development of Accounting: A Historical PerspectiveVeres IzabelaNo ratings yet

- History of Accounting.Document53 pagesHistory of Accounting.Trisha Mae Lyrica CastroNo ratings yet

- Smith Luca Pacioli Web Article REVISED 2018Document13 pagesSmith Luca Pacioli Web Article REVISED 2018Agum GumelarNo ratings yet

- CHAPTER 1 The World of AccountingDocument12 pagesCHAPTER 1 The World of AccountingChona MarcosNo ratings yet

- Chapter 1 Introduction To AccountingDocument51 pagesChapter 1 Introduction To AccountingHeisei De LunaNo ratings yet

- Cronica de Personaje ContabilidadDocument4 pagesCronica de Personaje ContabilidadKaterine JimenezNo ratings yet

- History of AccountingDocument1 pageHistory of AccountingElvira Baliag0% (1)

- 12 - Chapter TwoDocument83 pages12 - Chapter TwoMULU TEMESGENNo ratings yet

- Atp Notes HistoryDocument24 pagesAtp Notes HistoryLovemore MatondoNo ratings yet

- Course Title: Principles of Accounting Course Code: BBA 112: Agreeing To The StatementDocument8 pagesCourse Title: Principles of Accounting Course Code: BBA 112: Agreeing To The StatementSupriyo DasNo ratings yet

- Introduction-to-Acctg 1 4Document12 pagesIntroduction-to-Acctg 1 4Aenna Carmille TangubNo ratings yet

- Chapter 1-Fundamentals of Financial AccountingDocument20 pagesChapter 1-Fundamentals of Financial AccountingAudrey ReyesNo ratings yet

- Chapter 1-Fundamentals of Financial AccountingDocument11 pagesChapter 1-Fundamentals of Financial AccountingEYENNo ratings yet

- 1 Intro To AccountingDocument12 pages1 Intro To AccountingNAG-IBA MABININo ratings yet

- Group 1 PresentationDocument12 pagesGroup 1 Presentationiconkinging0No ratings yet

- The History of Accounting in The United States of AmericaDocument8 pagesThe History of Accounting in The United States of AmericaJorge Yeshayahu Gonzales-LaraNo ratings yet

- Luca PacioliDocument1 pageLuca PacioliChristy Allyssia VNo ratings yet

- Lesson 1 - Introduction To AccountingDocument19 pagesLesson 1 - Introduction To AccountingLeizzamar BayadogNo ratings yet

- Histroy of AccountingDocument2 pagesHistroy of AccountingFaith Reyna TanNo ratings yet

- Chapter 1-Fundamentals of Financial AccountingDocument11 pagesChapter 1-Fundamentals of Financial AccountingBlezzher Marsie ValerioNo ratings yet

- Accountancy Trabajo 1Document6 pagesAccountancy Trabajo 1Cristhian AndresNo ratings yet

- Expose 1Document4 pagesExpose 1feriel0805zNo ratings yet

- History of AccountingDocument10 pagesHistory of AccountingBlessylyn AguilarNo ratings yet

- History and Development of The Accounting ProfessionDocument7 pagesHistory and Development of The Accounting ProfessionChastine Beronilla MantillaNo ratings yet

- Chapter I Introduction To AccountinngDocument17 pagesChapter I Introduction To AccountinngVan MateoNo ratings yet

- Introduction To Accounting: Definition, Nature, Function, and History of AccountingDocument3 pagesIntroduction To Accounting: Definition, Nature, Function, and History of AccountingCaryl May Esparrago MiraNo ratings yet

- Basic AccountingDocument13 pagesBasic AccountingJoanCadenaNo ratings yet

- History of AccountingDocument5 pagesHistory of AccountingRowel Dela CruzNo ratings yet

- The RenaissanceDocument2 pagesThe RenaissanceJustine Airra OndoyNo ratings yet

- Definition and Nature of AccountingDocument16 pagesDefinition and Nature of Accountingdd8w252dfgNo ratings yet

- History of Accounting (Usman Ali Mashwani)Document2 pagesHistory of Accounting (Usman Ali Mashwani)Usman Ali MashwaniNo ratings yet

- Modern Accounting/accountancyDocument17 pagesModern Accounting/accountancysgopannairNo ratings yet

- FABM 1 - C1 - NatureOfAccountingDocument24 pagesFABM 1 - C1 - NatureOfAccountingApril Mae Villaceran100% (2)

- CH-1 The Accounting Equation2Document47 pagesCH-1 The Accounting Equation2Yasin Arafat ShuvoNo ratings yet

- FAR Topic 1Document21 pagesFAR Topic 1Princess Nicole LentijaNo ratings yet

- Accounting For ITDocument23 pagesAccounting For ITClaude CaduceusNo ratings yet

- Jake Eeeeeeeeeeeeeee EeeDocument3 pagesJake Eeeeeeeeeeeeeee EeeJake Realzon RuazolNo ratings yet

- Objective of AccountingDocument15 pagesObjective of AccountingVenus TanNo ratings yet

- Chap 01Document35 pagesChap 01ayyanaNo ratings yet

- Evolution of AccountingDocument4 pagesEvolution of AccountingRukshan WidanagamageNo ratings yet

- Fundamentals of Accountancy, Business and Management 1: Mr. Dennis C. de Dios MONDAY 10:30AM-12:30PMDocument67 pagesFundamentals of Accountancy, Business and Management 1: Mr. Dennis C. de Dios MONDAY 10:30AM-12:30PMJewell RoseNo ratings yet

- Mba 2008BDocument11 pagesMba 2008Bmenchong 123No ratings yet

- The History of AccountingDocument2 pagesThe History of Accountingbmwsergiu100% (1)

- FABM 1 Chapter 1Document17 pagesFABM 1 Chapter 1Carlo Jose SalaverNo ratings yet

- Basicaccountingconcepts - Education-Basic Accounting Concepts 2 Debits and CreditsDocument13 pagesBasicaccountingconcepts - Education-Basic Accounting Concepts 2 Debits and CreditsBommanaVamsidharreddyNo ratings yet

- Fundamentals of Accountancy, Business and Management 1Document37 pagesFundamentals of Accountancy, Business and Management 1Mylene CandidoNo ratings yet

- Nature and Regulation of Companies: Associate Professor Parmod Chand Macquarie University, Sydney, AustraliaDocument40 pagesNature and Regulation of Companies: Associate Professor Parmod Chand Macquarie University, Sydney, AustraliaSunila DeviNo ratings yet

- M36 - Quizzer 1 PDFDocument8 pagesM36 - Quizzer 1 PDFJoshua DaarolNo ratings yet

- (Ebook PDF) (Ebook PDF) Financial Accounting 15th Edition by Carl Warren All ChapterDocument43 pages(Ebook PDF) (Ebook PDF) Financial Accounting 15th Edition by Carl Warren All Chapterjinkosezan0100% (6)

- 3 Statement Model: Strictly ConfidentialDocument9 pages3 Statement Model: Strictly ConfidentialAshokNo ratings yet

- Karnataka 2nd Puc Accountancy Board Exam Question Paper Eng Version-March 2017Document8 pagesKarnataka 2nd Puc Accountancy Board Exam Question Paper Eng Version-March 2017poornimaramshettyNo ratings yet

- 04.1 - Lecture Notes - M4 - Audit Objectives, Procedures, Evidence, and Documentation (Feb 23)Document58 pages04.1 - Lecture Notes - M4 - Audit Objectives, Procedures, Evidence, and Documentation (Feb 23)Bea GarciaNo ratings yet

- John Keells Annual Report 2009 10Document152 pagesJohn Keells Annual Report 2009 10advise01No ratings yet

- Unit 3-Financial Statement AnalysisDocument55 pagesUnit 3-Financial Statement AnalysisGizaw BelayNo ratings yet

- Chapter 3 - The Adjusting ProcessDocument60 pagesChapter 3 - The Adjusting ProcessAzrielNo ratings yet

- Apollo Shoes Case AssignmentDocument68 pagesApollo Shoes Case AssignmentxusmkxfngNo ratings yet

- CourseDocument21 pagesCourseShannonNo ratings yet

- Abm 003 - ReviewerDocument12 pagesAbm 003 - ReviewerMary Beth Dela CruzNo ratings yet

- Sop 8Document4 pagesSop 8MadhuriNikamNo ratings yet

- Deepali Resume PDFDocument3 pagesDeepali Resume PDFakshayNo ratings yet

- Learn Sap-Fljco Like Never Before: SapfiDocument236 pagesLearn Sap-Fljco Like Never Before: SapfiMadhu MohanNo ratings yet

- Back To Basics: Period End Monthly/Yearly ClosingDocument128 pagesBack To Basics: Period End Monthly/Yearly ClosingAtish Muttha GNo ratings yet

- 2017 ReportDocument67 pages2017 Reportআত্মজীবনীNo ratings yet

- On January 1 2014 Palmer Company Acquired A 90 InterestDocument1 pageOn January 1 2014 Palmer Company Acquired A 90 InterestMuhammad ShahidNo ratings yet

- AKD cpt03Document91 pagesAKD cpt03Anisha RosevitaNo ratings yet

- Financial Statement Presentation Guide (Document819 pagesFinancial Statement Presentation Guide (bla csdcd100% (1)

- Fabm Reviewer 3RD QuarterDocument2 pagesFabm Reviewer 3RD QuartercxcxcxcxNo ratings yet

- Literature Review On Financial Statements Analysis - College Essay - Shankarjadhav28 1Document2 pagesLiterature Review On Financial Statements Analysis - College Essay - Shankarjadhav28 1Kobi Garbrah50% (4)

- Answer Quiz 1-Ol2Document15 pagesAnswer Quiz 1-Ol2Kristina KittyNo ratings yet

- Bac 409 Review Sessions 1-3Document3 pagesBac 409 Review Sessions 1-3Nereah DebrahNo ratings yet

- Overview of Accounting Up To PAS 1Document33 pagesOverview of Accounting Up To PAS 1jessamae gundanNo ratings yet

- Principles of Financial Accounting 1Document6 pagesPrinciples of Financial Accounting 1Amonie ReidNo ratings yet

- 2023 TIC Financial StatementsDocument6 pages2023 TIC Financial StatementsEduardoNo ratings yet

- Phil. Cpa Licensure Examination AuditingDocument9 pagesPhil. Cpa Licensure Examination AuditingbasmalabassyNo ratings yet

- Imran Ul Haq ACMA CGMA MBADocument2 pagesImran Ul Haq ACMA CGMA MBASheza FarooqNo ratings yet

- B) Sources of Evidences in Verifying The Ownership and Cost of The Following AssetsDocument4 pagesB) Sources of Evidences in Verifying The Ownership and Cost of The Following AssetsERICK MLINGWANo ratings yet

Download as pdf or txt

You might also like

- Group 1: Rafael Ramos Qaiser Bueno Kimverly Solis Antonio Jabson Xena Molato Kristzen LegaspiDocument7 pagesGroup 1: Rafael Ramos Qaiser Bueno Kimverly Solis Antonio Jabson Xena Molato Kristzen LegaspiReymsoNo ratings yet

- History of Accounting-WPS OfficeDocument10 pagesHistory of Accounting-WPS OfficeLea PasquinNo ratings yet

- Accounting History: Arithmetica, Geometria, Proportioni Et Proportionalita. of Course, Businesses and GovernmentsDocument11 pagesAccounting History: Arithmetica, Geometria, Proportioni Et Proportionalita. of Course, Businesses and GovernmentsPaul GeorgeNo ratings yet

- History of AccountingDocument4 pagesHistory of AccountingFaith Claire100% (2)

- Group 2 Presentation Acc 304Document22 pagesGroup 2 Presentation Acc 304iconkinging0No ratings yet

- Elective P.TDocument3 pagesElective P.TLuna LedezmaNo ratings yet

- Basic Accounting Summary Lecture-101-08!31!22Document3 pagesBasic Accounting Summary Lecture-101-08!31!22Roxane EsabinianoNo ratings yet

- 1.meaning of AccountingDocument21 pages1.meaning of AccountingNafe Singh YadavNo ratings yet

- Accounting and The Hospitality ManagerDocument27 pagesAccounting and The Hospitality ManagerPERALTA, ELISHA PREYANKANo ratings yet

- Smith Luca Pacioli Web Article REVISED 2018Document13 pagesSmith Luca Pacioli Web Article REVISED 2018JeremiahNo ratings yet

- Chapter 1-Textbook (Accounting An Introduction)Document13 pagesChapter 1-Textbook (Accounting An Introduction)Jimmy MulokoshiNo ratings yet

- Conceptual Development of Accounting: A Historical PerspectiveDocument11 pagesConceptual Development of Accounting: A Historical PerspectiveVeres IzabelaNo ratings yet

- History of Accounting.Document53 pagesHistory of Accounting.Trisha Mae Lyrica CastroNo ratings yet

- Smith Luca Pacioli Web Article REVISED 2018Document13 pagesSmith Luca Pacioli Web Article REVISED 2018Agum GumelarNo ratings yet

- CHAPTER 1 The World of AccountingDocument12 pagesCHAPTER 1 The World of AccountingChona MarcosNo ratings yet

- Chapter 1 Introduction To AccountingDocument51 pagesChapter 1 Introduction To AccountingHeisei De LunaNo ratings yet

- Cronica de Personaje ContabilidadDocument4 pagesCronica de Personaje ContabilidadKaterine JimenezNo ratings yet

- History of AccountingDocument1 pageHistory of AccountingElvira Baliag0% (1)

- 12 - Chapter TwoDocument83 pages12 - Chapter TwoMULU TEMESGENNo ratings yet

- Atp Notes HistoryDocument24 pagesAtp Notes HistoryLovemore MatondoNo ratings yet

- Course Title: Principles of Accounting Course Code: BBA 112: Agreeing To The StatementDocument8 pagesCourse Title: Principles of Accounting Course Code: BBA 112: Agreeing To The StatementSupriyo DasNo ratings yet

- Introduction-to-Acctg 1 4Document12 pagesIntroduction-to-Acctg 1 4Aenna Carmille TangubNo ratings yet

- Chapter 1-Fundamentals of Financial AccountingDocument20 pagesChapter 1-Fundamentals of Financial AccountingAudrey ReyesNo ratings yet

- Chapter 1-Fundamentals of Financial AccountingDocument11 pagesChapter 1-Fundamentals of Financial AccountingEYENNo ratings yet

- 1 Intro To AccountingDocument12 pages1 Intro To AccountingNAG-IBA MABININo ratings yet

- Group 1 PresentationDocument12 pagesGroup 1 Presentationiconkinging0No ratings yet

- The History of Accounting in The United States of AmericaDocument8 pagesThe History of Accounting in The United States of AmericaJorge Yeshayahu Gonzales-LaraNo ratings yet

- Luca PacioliDocument1 pageLuca PacioliChristy Allyssia VNo ratings yet

- Lesson 1 - Introduction To AccountingDocument19 pagesLesson 1 - Introduction To AccountingLeizzamar BayadogNo ratings yet

- Histroy of AccountingDocument2 pagesHistroy of AccountingFaith Reyna TanNo ratings yet

- Chapter 1-Fundamentals of Financial AccountingDocument11 pagesChapter 1-Fundamentals of Financial AccountingBlezzher Marsie ValerioNo ratings yet

- Accountancy Trabajo 1Document6 pagesAccountancy Trabajo 1Cristhian AndresNo ratings yet

- Expose 1Document4 pagesExpose 1feriel0805zNo ratings yet

- History of AccountingDocument10 pagesHistory of AccountingBlessylyn AguilarNo ratings yet

- History and Development of The Accounting ProfessionDocument7 pagesHistory and Development of The Accounting ProfessionChastine Beronilla MantillaNo ratings yet

- Chapter I Introduction To AccountinngDocument17 pagesChapter I Introduction To AccountinngVan MateoNo ratings yet

- Introduction To Accounting: Definition, Nature, Function, and History of AccountingDocument3 pagesIntroduction To Accounting: Definition, Nature, Function, and History of AccountingCaryl May Esparrago MiraNo ratings yet

- Basic AccountingDocument13 pagesBasic AccountingJoanCadenaNo ratings yet

- History of AccountingDocument5 pagesHistory of AccountingRowel Dela CruzNo ratings yet

- The RenaissanceDocument2 pagesThe RenaissanceJustine Airra OndoyNo ratings yet

- Definition and Nature of AccountingDocument16 pagesDefinition and Nature of Accountingdd8w252dfgNo ratings yet

- History of Accounting (Usman Ali Mashwani)Document2 pagesHistory of Accounting (Usman Ali Mashwani)Usman Ali MashwaniNo ratings yet

- Modern Accounting/accountancyDocument17 pagesModern Accounting/accountancysgopannairNo ratings yet

- FABM 1 - C1 - NatureOfAccountingDocument24 pagesFABM 1 - C1 - NatureOfAccountingApril Mae Villaceran100% (2)

- CH-1 The Accounting Equation2Document47 pagesCH-1 The Accounting Equation2Yasin Arafat ShuvoNo ratings yet

- FAR Topic 1Document21 pagesFAR Topic 1Princess Nicole LentijaNo ratings yet

- Accounting For ITDocument23 pagesAccounting For ITClaude CaduceusNo ratings yet

- Jake Eeeeeeeeeeeeeee EeeDocument3 pagesJake Eeeeeeeeeeeeeee EeeJake Realzon RuazolNo ratings yet

- Objective of AccountingDocument15 pagesObjective of AccountingVenus TanNo ratings yet

- Chap 01Document35 pagesChap 01ayyanaNo ratings yet

- Evolution of AccountingDocument4 pagesEvolution of AccountingRukshan WidanagamageNo ratings yet

- Fundamentals of Accountancy, Business and Management 1: Mr. Dennis C. de Dios MONDAY 10:30AM-12:30PMDocument67 pagesFundamentals of Accountancy, Business and Management 1: Mr. Dennis C. de Dios MONDAY 10:30AM-12:30PMJewell RoseNo ratings yet

- Mba 2008BDocument11 pagesMba 2008Bmenchong 123No ratings yet

- The History of AccountingDocument2 pagesThe History of Accountingbmwsergiu100% (1)

- FABM 1 Chapter 1Document17 pagesFABM 1 Chapter 1Carlo Jose SalaverNo ratings yet

- Basicaccountingconcepts - Education-Basic Accounting Concepts 2 Debits and CreditsDocument13 pagesBasicaccountingconcepts - Education-Basic Accounting Concepts 2 Debits and CreditsBommanaVamsidharreddyNo ratings yet

- Fundamentals of Accountancy, Business and Management 1Document37 pagesFundamentals of Accountancy, Business and Management 1Mylene CandidoNo ratings yet

- Nature and Regulation of Companies: Associate Professor Parmod Chand Macquarie University, Sydney, AustraliaDocument40 pagesNature and Regulation of Companies: Associate Professor Parmod Chand Macquarie University, Sydney, AustraliaSunila DeviNo ratings yet

- M36 - Quizzer 1 PDFDocument8 pagesM36 - Quizzer 1 PDFJoshua DaarolNo ratings yet

- (Ebook PDF) (Ebook PDF) Financial Accounting 15th Edition by Carl Warren All ChapterDocument43 pages(Ebook PDF) (Ebook PDF) Financial Accounting 15th Edition by Carl Warren All Chapterjinkosezan0100% (6)

- 3 Statement Model: Strictly ConfidentialDocument9 pages3 Statement Model: Strictly ConfidentialAshokNo ratings yet

- Karnataka 2nd Puc Accountancy Board Exam Question Paper Eng Version-March 2017Document8 pagesKarnataka 2nd Puc Accountancy Board Exam Question Paper Eng Version-March 2017poornimaramshettyNo ratings yet

- 04.1 - Lecture Notes - M4 - Audit Objectives, Procedures, Evidence, and Documentation (Feb 23)Document58 pages04.1 - Lecture Notes - M4 - Audit Objectives, Procedures, Evidence, and Documentation (Feb 23)Bea GarciaNo ratings yet

- John Keells Annual Report 2009 10Document152 pagesJohn Keells Annual Report 2009 10advise01No ratings yet

- Unit 3-Financial Statement AnalysisDocument55 pagesUnit 3-Financial Statement AnalysisGizaw BelayNo ratings yet

- Chapter 3 - The Adjusting ProcessDocument60 pagesChapter 3 - The Adjusting ProcessAzrielNo ratings yet

- Apollo Shoes Case AssignmentDocument68 pagesApollo Shoes Case AssignmentxusmkxfngNo ratings yet

- CourseDocument21 pagesCourseShannonNo ratings yet

- Abm 003 - ReviewerDocument12 pagesAbm 003 - ReviewerMary Beth Dela CruzNo ratings yet

- Sop 8Document4 pagesSop 8MadhuriNikamNo ratings yet

- Deepali Resume PDFDocument3 pagesDeepali Resume PDFakshayNo ratings yet

- Learn Sap-Fljco Like Never Before: SapfiDocument236 pagesLearn Sap-Fljco Like Never Before: SapfiMadhu MohanNo ratings yet

- Back To Basics: Period End Monthly/Yearly ClosingDocument128 pagesBack To Basics: Period End Monthly/Yearly ClosingAtish Muttha GNo ratings yet

- 2017 ReportDocument67 pages2017 Reportআত্মজীবনীNo ratings yet

- On January 1 2014 Palmer Company Acquired A 90 InterestDocument1 pageOn January 1 2014 Palmer Company Acquired A 90 InterestMuhammad ShahidNo ratings yet

- AKD cpt03Document91 pagesAKD cpt03Anisha RosevitaNo ratings yet

- Financial Statement Presentation Guide (Document819 pagesFinancial Statement Presentation Guide (bla csdcd100% (1)

- Fabm Reviewer 3RD QuarterDocument2 pagesFabm Reviewer 3RD QuartercxcxcxcxNo ratings yet

- Literature Review On Financial Statements Analysis - College Essay - Shankarjadhav28 1Document2 pagesLiterature Review On Financial Statements Analysis - College Essay - Shankarjadhav28 1Kobi Garbrah50% (4)

- Answer Quiz 1-Ol2Document15 pagesAnswer Quiz 1-Ol2Kristina KittyNo ratings yet

- Bac 409 Review Sessions 1-3Document3 pagesBac 409 Review Sessions 1-3Nereah DebrahNo ratings yet

- Overview of Accounting Up To PAS 1Document33 pagesOverview of Accounting Up To PAS 1jessamae gundanNo ratings yet

- Principles of Financial Accounting 1Document6 pagesPrinciples of Financial Accounting 1Amonie ReidNo ratings yet

- 2023 TIC Financial StatementsDocument6 pages2023 TIC Financial StatementsEduardoNo ratings yet

- Phil. Cpa Licensure Examination AuditingDocument9 pagesPhil. Cpa Licensure Examination AuditingbasmalabassyNo ratings yet

- Imran Ul Haq ACMA CGMA MBADocument2 pagesImran Ul Haq ACMA CGMA MBASheza FarooqNo ratings yet

- B) Sources of Evidences in Verifying The Ownership and Cost of The Following AssetsDocument4 pagesB) Sources of Evidences in Verifying The Ownership and Cost of The Following AssetsERICK MLINGWANo ratings yet