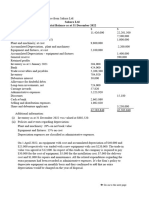

Consolidation Question and Answer

Consolidation Question and Answer

You might also like

- BHMS 4492 Financial Statement Analysis Assignment 1Document3 pagesBHMS 4492 Financial Statement Analysis Assignment 1pui shan wanNo ratings yet

- 2019 DecemberDocument14 pages2019 DecemberHsaung HaymarnNo ratings yet

- December 2019 DipIFR - Question - AnswerDocument20 pagesDecember 2019 DipIFR - Question - Answerksaqib89No ratings yet

- Financial Reporting: September/December 2017 - Sample QuestionsDocument4 pagesFinancial Reporting: September/December 2017 - Sample QuestionsNurul Nabilah SuhamiNo ratings yet

- Lecture Practice Questions - Sep.Document3 pagesLecture Practice Questions - Sep.Mariøn Lemonnier BruelNo ratings yet

- Revision QN On Ratio AnalysisDocument3 pagesRevision QN On Ratio Analysisamosoundo59No ratings yet

- Question June - 2010Document8 pagesQuestion June - 2010pawan kumar MaheshwariNo ratings yet

- f7sgp 2010 Jun QDocument9 pagesf7sgp 2010 Jun Q2010aungmyatNo ratings yet

- Class 1 HomeworkDocument10 pagesClass 1 HomeworkAngel MéndezNo ratings yet

- f7hkg 2010 Jun QDocument9 pagesf7hkg 2010 Jun QOni SegunNo ratings yet

- FINANCIAL REPORTING PAPER 2.1nov 2023Document27 pagesFINANCIAL REPORTING PAPER 2.1nov 2023xodic49847No ratings yet

- Advanced Financial Management (Singapore) : Thursday 4 June 2009Document13 pagesAdvanced Financial Management (Singapore) : Thursday 4 June 2009Lim CZNo ratings yet

- SBR Consolidation Mock QueDocument7 pagesSBR Consolidation Mock QuePratham BarotNo ratings yet

- ABC and XYZ - QuestionDocument2 pagesABC and XYZ - QuestionMohammad El HajjNo ratings yet

- Q3 Paper PDFDocument11 pagesQ3 Paper PDFAjit TiwariNo ratings yet

- PA T22WSB 3 Group Assignment 1Document4 pagesPA T22WSB 3 Group Assignment 1Pham Minh Thu NguyenNo ratings yet

- AP W1 Correction of ErrorsDocument4 pagesAP W1 Correction of ErrorsALYZA ANGELA ORNEDONo ratings yet

- 2019 12 December-2019-Cpe-Audit-Question-PaperDocument10 pages2019 12 December-2019-Cpe-Audit-Question-Paperkellz accountingNo ratings yet

- IFRS Exams 1716631858Document262 pagesIFRS Exams 1716631858christien tshikaNo ratings yet

- Your Answers Should Draw Upon Academic Literature Where AppropriateDocument4 pagesYour Answers Should Draw Upon Academic Literature Where AppropriateNemanja SubicNo ratings yet

- j16 Hybrid F7 QDocument7 pagesj16 Hybrid F7 QPatricia MinellyNo ratings yet

- 06 JUNE QuestionDocument11 pages06 JUNE QuestionkhengmaiNo ratings yet

- FAR - Final Preboard CPAR 92Document14 pagesFAR - Final Preboard CPAR 92joyhhazelNo ratings yet

- Financial Reporting (United Kingdom) : Tuesday 15 June 2010Document9 pagesFinancial Reporting (United Kingdom) : Tuesday 15 June 2010zulaa bNo ratings yet

- Test 4Document8 pagesTest 4govarthan1976No ratings yet

- B2 2022 May QNDocument11 pagesB2 2022 May QNRashid AbeidNo ratings yet

- Chapter 46 Cash Flow ComprehensiveDocument8 pagesChapter 46 Cash Flow ComprehensiveCheesca Macabanti - 12 Euclid-Digital ModularNo ratings yet

- B2 2021 Nov QNDocument10 pagesB2 2021 Nov QNRashid AbeidNo ratings yet

- Diploma in International Financial Reporting: Thursday 6 December 2007Document9 pagesDiploma in International Financial Reporting: Thursday 6 December 2007Ajit TiwariNo ratings yet

- Test Series: November, 2021 Mock Test Paper - 2 Intermediate (New) : Group - I Paper - 1: AccountingDocument8 pagesTest Series: November, 2021 Mock Test Paper - 2 Intermediate (New) : Group - I Paper - 1: Accountingsunil1287No ratings yet

- Financial Statement Analysis - AssignmentDocument6 pagesFinancial Statement Analysis - AssignmentJennifer JosephNo ratings yet

- Tutorial BankDocument9 pagesTutorial BankRumbidzai MapanzureNo ratings yet

- CFS 2Document2 pagesCFS 2RositaNo ratings yet

- AccrDocument2 pagesAccrlearningcantstop561No ratings yet

- Ais 212 - 2024Document3 pagesAis 212 - 2024Professor Md. Zakir Hosen FCANo ratings yet

- Sem-6 FR & FSA Model paper 1_240608_144233Document5 pagesSem-6 FR & FSA Model paper 1_240608_144233taniashaw200309No ratings yet

- Class Problem: 2Document7 pagesClass Problem: 2Riad FaisalNo ratings yet

- Financial StatementsDocument2 pagesFinancial StatementsMaria Teresa VillamayorNo ratings yet

- Fund Acct 4.1Document23 pagesFund Acct 4.1Gabi MamushetNo ratings yet

- Identify The Choice That Best Completes The Statement or Answers The QuestionDocument5 pagesIdentify The Choice That Best Completes The Statement or Answers The QuestionErine ContranoNo ratings yet

- Diploma in International Financial Reporting: Friday 8 December 2017Document8 pagesDiploma in International Financial Reporting: Friday 8 December 2017Khin Zaw HtweNo ratings yet

- 2017 DecemberDocument16 pages2017 DecemberHsaung HaymarnNo ratings yet

- Lesson 1 Partnership FormationDocument21 pagesLesson 1 Partnership FormationDan Gabrielle SalacNo ratings yet

- BAC 322 Advanced AccountingDocument9 pagesBAC 322 Advanced AccountingLawrence jnr MwapeNo ratings yet

- 301 AFA II PL III Question CMA June 2021 Exam.Document4 pages301 AFA II PL III Question CMA June 2021 Exam.rumelrashid_seuNo ratings yet

- Questions 1 A) .: Page 1 of 15Document15 pagesQuestions 1 A) .: Page 1 of 15Richie BoomaNo ratings yet

- ACC 401-2023 GA 2-EvenDocument3 pagesACC 401-2023 GA 2-EvenOhene Asare PogastyNo ratings yet

- Financila Statements 2023 FinalDocument17 pagesFinancila Statements 2023 Finallesleymohlala7No ratings yet

- Corporate Reporting (Singapore) : Tuesday 13 December 2011Document6 pagesCorporate Reporting (Singapore) : Tuesday 13 December 2011Haaris DurraniNo ratings yet

- Aafr & Aars TSB Mock QP With Solution by Sir Hasnain BadamiDocument35 pagesAafr & Aars TSB Mock QP With Solution by Sir Hasnain BadamiMuhammad Sohaib AzharNo ratings yet

- Final Ca: MAY '19 Financial ReportingDocument13 pagesFinal Ca: MAY '19 Financial ReportingJINENDRA JAINNo ratings yet

- p7sgp 2011 Dec QDocument10 pagesp7sgp 2011 Dec QamNo ratings yet

- 371 PedanticDocument2 pages371 Pedanticabdirahman farah AbdiNo ratings yet

- Instructions: Write TRUE, If The Statement Is Correct, and FALSE, If Otherwise On The Space Provided. No ErasuresDocument3 pagesInstructions: Write TRUE, If The Statement Is Correct, and FALSE, If Otherwise On The Space Provided. No ErasuresRizhelle CunananNo ratings yet

- Financial Management MidtermDocument4 pagesFinancial Management MidtermGrace Sinoy BastanteNo ratings yet

- Accountancy FinancialDocument9 pagesAccountancy Financialverma.vineet.officialNo ratings yet

- Gm34n84m9q81 F7FR Monitoring Test 1A Questions s16 j17Document6 pagesGm34n84m9q81 F7FR Monitoring Test 1A Questions s16 j17Chua Ru YiNo ratings yet

- December 2016 DipIFR - Question - AnswerDocument20 pagesDecember 2016 DipIFR - Question - Answerksaqib89No ratings yet

- Accounting Mock ExamDocument6 pagesAccounting Mock ExamKiran alex ChallagiriNo ratings yet

- One Year of Living with COVID-19: An Assessment of How ADB Members Fought the Pandemic in 2020From EverandOne Year of Living with COVID-19: An Assessment of How ADB Members Fought the Pandemic in 2020No ratings yet

- Assignment 0ne Due 25 October 2020 Group (1)Document7 pagesAssignment 0ne Due 25 October 2020 Group (1)Jeremiah NcubeNo ratings yet

- zviko CVDocument2 pageszviko CVJeremiah NcubeNo ratings yet

- hygDocument3 pageshygJeremiah NcubeNo ratings yet

- Group 18 PresentationDocument11 pagesGroup 18 PresentationJeremiah NcubeNo ratings yet

- SummaryDocument4 pagesSummaryJeremiah NcubeNo ratings yet

- Inclass TestDocument2 pagesInclass TestJeremiah NcubeNo ratings yet

- QN 5 Performance Management PresentationDocument8 pagesQN 5 Performance Management PresentationJeremiah NcubeNo ratings yet

- Mlambi Shingai Qn14 PresentatDocument11 pagesMlambi Shingai Qn14 PresentatJeremiah NcubeNo ratings yet

- Nigel Mutukwa Question 9 PresentationDocument10 pagesNigel Mutukwa Question 9 PresentationJeremiah NcubeNo ratings yet

- Question 8 PresentationDocument11 pagesQuestion 8 PresentationJeremiah NcubeNo ratings yet

- Chingombe Kudzai and Julius CUACM 413 PresentationDocument9 pagesChingombe Kudzai and Julius CUACM 413 PresentationJeremiah NcubeNo ratings yet

- PM PresentationDocument12 pagesPM PresentationJeremiah NcubeNo ratings yet

- Group 18 PreseNtation. (Evalaution of The Synergy Between Communication and Leadersip)Document15 pagesGroup 18 PreseNtation. (Evalaution of The Synergy Between Communication and Leadersip)Jeremiah NcubeNo ratings yet

- Performance Management PresentationDocument14 pagesPerformance Management PresentationJeremiah NcubeNo ratings yet

- Question 13 Mangwiro LTDDocument3 pagesQuestion 13 Mangwiro LTDJeremiah NcubeNo ratings yet

- Joy Ben Question 13Document13 pagesJoy Ben Question 13Jeremiah NcubeNo ratings yet

- Group 3 PresentationDocument10 pagesGroup 3 PresentationJeremiah NcubeNo ratings yet

- Group 17 Block Presentation (c20141840x)Document7 pagesGroup 17 Block Presentation (c20141840x)Jeremiah NcubeNo ratings yet

- Group PresentationDocument3 pagesGroup PresentationJeremiah NcubeNo ratings yet

- Transfer Pricing, Tax Avoidance and International TaxationDocument81 pagesTransfer Pricing, Tax Avoidance and International TaxationJeremiah NcubeNo ratings yet

- SolutionDocument57 pagesSolutionJeremiah NcubeNo ratings yet

- Corporate Government Oct 2023Document1 pageCorporate Government Oct 2023Jeremiah NcubeNo ratings yet

- FIIs in India.........Document12 pagesFIIs in India.........JogenderNo ratings yet

- Branch Accounting CMADocument41 pagesBranch Accounting CMAyash.sharmaNo ratings yet

- 3 5 46 850Document5 pages3 5 46 850suresh100% (1)

- Academic Fees Payment GuidelinesDocument2 pagesAcademic Fees Payment GuidelinesCrackPODNo ratings yet

- GboDocument5 pagesGborosechaithuNo ratings yet

- SAP - FICO Course ContentDocument10 pagesSAP - FICO Course Contentchaitanya vutukuriNo ratings yet

- CH 3 Savings & Investments, Credit and DebtDocument18 pagesCH 3 Savings & Investments, Credit and DebtSURAYA BINTI HARUN MoeNo ratings yet

- Zelizer Viviana - The Proliferation of Social Currencies (Art.) PDFDocument11 pagesZelizer Viviana - The Proliferation of Social Currencies (Art.) PDFmarioNo ratings yet

- Equity Securities - Answer Key PDFDocument5 pagesEquity Securities - Answer Key PDFVikaNo ratings yet

- PT. Ungaran WanakaryaDocument2 pagesPT. Ungaran WanakaryaPrince NeroNo ratings yet

- Forex Trading 1Document6 pagesForex Trading 1Pablo Gabrio88% (8)

- Ib Form Joint Account MandateDocument1 pageIb Form Joint Account Mandatemodjo072No ratings yet

- Pile cp13Document73 pagesPile cp13casarokar100% (1)

- Chap006 Text BankDocument14 pagesChap006 Text BankAshraful AlamNo ratings yet

- 26ASDocument4 pages26ASAnubhav AsatiNo ratings yet

- Answer Capital Investment Sw2Document38 pagesAnswer Capital Investment Sw2Xandae MempinNo ratings yet

- Quiz 1 20.06.17 Q& ADocument11 pagesQuiz 1 20.06.17 Q& ADeependra NigamNo ratings yet

- Online Banking in India: Submitted byDocument20 pagesOnline Banking in India: Submitted byAastha PrakashNo ratings yet

- Module 6 IRR and Payback PeriodDocument13 pagesModule 6 IRR and Payback PeriodRhonita Dea AndariniNo ratings yet

- Nike CaseDocument8 pagesNike Casesedobi1512No ratings yet

- Investigating The Consumers' Perception Towards Usage of Plastic Money in Bangladesh: An Application of Confirmatory Factor AnalysisDocument9 pagesInvestigating The Consumers' Perception Towards Usage of Plastic Money in Bangladesh: An Application of Confirmatory Factor AnalysisHardik ShahNo ratings yet

- Budgeting Family ResourcesDocument10 pagesBudgeting Family ResourcesKing Justin ManansalaNo ratings yet

- Mbe SyllabusDocument47 pagesMbe SyllabussanyasamNo ratings yet

- Cap Budegt ProbsDocument4 pagesCap Budegt ProbsAR Ananth Rohith BhatNo ratings yet

- Ripple Investment GuideDocument20 pagesRipple Investment GuideRippleHedgeFundNo ratings yet

- Prealgebra 4th Edition Tom Carson Solutions ManualDocument26 pagesPrealgebra 4th Edition Tom Carson Solutions ManualMichaelOlsonmterj100% (39)

- (Factsheet) MBBT-19110014Document4 pages(Factsheet) MBBT-19110014Zen LohNo ratings yet

- Oliveti-ECR710 Cash RegisterDocument31 pagesOliveti-ECR710 Cash RegisterEmmanuel Lucky OhiroNo ratings yet

- Dividend Discount Model: AssumptionsDocument27 pagesDividend Discount Model: AssumptionsSairam GovarthananNo ratings yet

- XII Accontancy Pre Board IIDocument9 pagesXII Accontancy Pre Board IIShivansh JaiswalNo ratings yet

Download as docx, pdf, or txt

You might also like

- BHMS 4492 Financial Statement Analysis Assignment 1Document3 pagesBHMS 4492 Financial Statement Analysis Assignment 1pui shan wanNo ratings yet

- 2019 DecemberDocument14 pages2019 DecemberHsaung HaymarnNo ratings yet

- December 2019 DipIFR - Question - AnswerDocument20 pagesDecember 2019 DipIFR - Question - Answerksaqib89No ratings yet

- Financial Reporting: September/December 2017 - Sample QuestionsDocument4 pagesFinancial Reporting: September/December 2017 - Sample QuestionsNurul Nabilah SuhamiNo ratings yet

- Lecture Practice Questions - Sep.Document3 pagesLecture Practice Questions - Sep.Mariøn Lemonnier BruelNo ratings yet

- Revision QN On Ratio AnalysisDocument3 pagesRevision QN On Ratio Analysisamosoundo59No ratings yet

- Question June - 2010Document8 pagesQuestion June - 2010pawan kumar MaheshwariNo ratings yet

- f7sgp 2010 Jun QDocument9 pagesf7sgp 2010 Jun Q2010aungmyatNo ratings yet

- Class 1 HomeworkDocument10 pagesClass 1 HomeworkAngel MéndezNo ratings yet

- f7hkg 2010 Jun QDocument9 pagesf7hkg 2010 Jun QOni SegunNo ratings yet

- FINANCIAL REPORTING PAPER 2.1nov 2023Document27 pagesFINANCIAL REPORTING PAPER 2.1nov 2023xodic49847No ratings yet

- Advanced Financial Management (Singapore) : Thursday 4 June 2009Document13 pagesAdvanced Financial Management (Singapore) : Thursday 4 June 2009Lim CZNo ratings yet

- SBR Consolidation Mock QueDocument7 pagesSBR Consolidation Mock QuePratham BarotNo ratings yet

- ABC and XYZ - QuestionDocument2 pagesABC and XYZ - QuestionMohammad El HajjNo ratings yet

- Q3 Paper PDFDocument11 pagesQ3 Paper PDFAjit TiwariNo ratings yet

- PA T22WSB 3 Group Assignment 1Document4 pagesPA T22WSB 3 Group Assignment 1Pham Minh Thu NguyenNo ratings yet

- AP W1 Correction of ErrorsDocument4 pagesAP W1 Correction of ErrorsALYZA ANGELA ORNEDONo ratings yet

- 2019 12 December-2019-Cpe-Audit-Question-PaperDocument10 pages2019 12 December-2019-Cpe-Audit-Question-Paperkellz accountingNo ratings yet

- IFRS Exams 1716631858Document262 pagesIFRS Exams 1716631858christien tshikaNo ratings yet

- Your Answers Should Draw Upon Academic Literature Where AppropriateDocument4 pagesYour Answers Should Draw Upon Academic Literature Where AppropriateNemanja SubicNo ratings yet

- j16 Hybrid F7 QDocument7 pagesj16 Hybrid F7 QPatricia MinellyNo ratings yet

- 06 JUNE QuestionDocument11 pages06 JUNE QuestionkhengmaiNo ratings yet

- FAR - Final Preboard CPAR 92Document14 pagesFAR - Final Preboard CPAR 92joyhhazelNo ratings yet

- Financial Reporting (United Kingdom) : Tuesday 15 June 2010Document9 pagesFinancial Reporting (United Kingdom) : Tuesday 15 June 2010zulaa bNo ratings yet

- Test 4Document8 pagesTest 4govarthan1976No ratings yet

- B2 2022 May QNDocument11 pagesB2 2022 May QNRashid AbeidNo ratings yet

- Chapter 46 Cash Flow ComprehensiveDocument8 pagesChapter 46 Cash Flow ComprehensiveCheesca Macabanti - 12 Euclid-Digital ModularNo ratings yet

- B2 2021 Nov QNDocument10 pagesB2 2021 Nov QNRashid AbeidNo ratings yet

- Diploma in International Financial Reporting: Thursday 6 December 2007Document9 pagesDiploma in International Financial Reporting: Thursday 6 December 2007Ajit TiwariNo ratings yet

- Test Series: November, 2021 Mock Test Paper - 2 Intermediate (New) : Group - I Paper - 1: AccountingDocument8 pagesTest Series: November, 2021 Mock Test Paper - 2 Intermediate (New) : Group - I Paper - 1: Accountingsunil1287No ratings yet

- Financial Statement Analysis - AssignmentDocument6 pagesFinancial Statement Analysis - AssignmentJennifer JosephNo ratings yet

- Tutorial BankDocument9 pagesTutorial BankRumbidzai MapanzureNo ratings yet

- CFS 2Document2 pagesCFS 2RositaNo ratings yet

- AccrDocument2 pagesAccrlearningcantstop561No ratings yet

- Ais 212 - 2024Document3 pagesAis 212 - 2024Professor Md. Zakir Hosen FCANo ratings yet

- Sem-6 FR & FSA Model paper 1_240608_144233Document5 pagesSem-6 FR & FSA Model paper 1_240608_144233taniashaw200309No ratings yet

- Class Problem: 2Document7 pagesClass Problem: 2Riad FaisalNo ratings yet

- Financial StatementsDocument2 pagesFinancial StatementsMaria Teresa VillamayorNo ratings yet

- Fund Acct 4.1Document23 pagesFund Acct 4.1Gabi MamushetNo ratings yet

- Identify The Choice That Best Completes The Statement or Answers The QuestionDocument5 pagesIdentify The Choice That Best Completes The Statement or Answers The QuestionErine ContranoNo ratings yet

- Diploma in International Financial Reporting: Friday 8 December 2017Document8 pagesDiploma in International Financial Reporting: Friday 8 December 2017Khin Zaw HtweNo ratings yet

- 2017 DecemberDocument16 pages2017 DecemberHsaung HaymarnNo ratings yet

- Lesson 1 Partnership FormationDocument21 pagesLesson 1 Partnership FormationDan Gabrielle SalacNo ratings yet

- BAC 322 Advanced AccountingDocument9 pagesBAC 322 Advanced AccountingLawrence jnr MwapeNo ratings yet

- 301 AFA II PL III Question CMA June 2021 Exam.Document4 pages301 AFA II PL III Question CMA June 2021 Exam.rumelrashid_seuNo ratings yet

- Questions 1 A) .: Page 1 of 15Document15 pagesQuestions 1 A) .: Page 1 of 15Richie BoomaNo ratings yet

- ACC 401-2023 GA 2-EvenDocument3 pagesACC 401-2023 GA 2-EvenOhene Asare PogastyNo ratings yet

- Financila Statements 2023 FinalDocument17 pagesFinancila Statements 2023 Finallesleymohlala7No ratings yet

- Corporate Reporting (Singapore) : Tuesday 13 December 2011Document6 pagesCorporate Reporting (Singapore) : Tuesday 13 December 2011Haaris DurraniNo ratings yet

- Aafr & Aars TSB Mock QP With Solution by Sir Hasnain BadamiDocument35 pagesAafr & Aars TSB Mock QP With Solution by Sir Hasnain BadamiMuhammad Sohaib AzharNo ratings yet

- Final Ca: MAY '19 Financial ReportingDocument13 pagesFinal Ca: MAY '19 Financial ReportingJINENDRA JAINNo ratings yet

- p7sgp 2011 Dec QDocument10 pagesp7sgp 2011 Dec QamNo ratings yet

- 371 PedanticDocument2 pages371 Pedanticabdirahman farah AbdiNo ratings yet

- Instructions: Write TRUE, If The Statement Is Correct, and FALSE, If Otherwise On The Space Provided. No ErasuresDocument3 pagesInstructions: Write TRUE, If The Statement Is Correct, and FALSE, If Otherwise On The Space Provided. No ErasuresRizhelle CunananNo ratings yet

- Financial Management MidtermDocument4 pagesFinancial Management MidtermGrace Sinoy BastanteNo ratings yet

- Accountancy FinancialDocument9 pagesAccountancy Financialverma.vineet.officialNo ratings yet

- Gm34n84m9q81 F7FR Monitoring Test 1A Questions s16 j17Document6 pagesGm34n84m9q81 F7FR Monitoring Test 1A Questions s16 j17Chua Ru YiNo ratings yet

- December 2016 DipIFR - Question - AnswerDocument20 pagesDecember 2016 DipIFR - Question - Answerksaqib89No ratings yet

- Accounting Mock ExamDocument6 pagesAccounting Mock ExamKiran alex ChallagiriNo ratings yet

- One Year of Living with COVID-19: An Assessment of How ADB Members Fought the Pandemic in 2020From EverandOne Year of Living with COVID-19: An Assessment of How ADB Members Fought the Pandemic in 2020No ratings yet

- Assignment 0ne Due 25 October 2020 Group (1)Document7 pagesAssignment 0ne Due 25 October 2020 Group (1)Jeremiah NcubeNo ratings yet

- zviko CVDocument2 pageszviko CVJeremiah NcubeNo ratings yet

- hygDocument3 pageshygJeremiah NcubeNo ratings yet

- Group 18 PresentationDocument11 pagesGroup 18 PresentationJeremiah NcubeNo ratings yet

- SummaryDocument4 pagesSummaryJeremiah NcubeNo ratings yet

- Inclass TestDocument2 pagesInclass TestJeremiah NcubeNo ratings yet

- QN 5 Performance Management PresentationDocument8 pagesQN 5 Performance Management PresentationJeremiah NcubeNo ratings yet

- Mlambi Shingai Qn14 PresentatDocument11 pagesMlambi Shingai Qn14 PresentatJeremiah NcubeNo ratings yet

- Nigel Mutukwa Question 9 PresentationDocument10 pagesNigel Mutukwa Question 9 PresentationJeremiah NcubeNo ratings yet

- Question 8 PresentationDocument11 pagesQuestion 8 PresentationJeremiah NcubeNo ratings yet

- Chingombe Kudzai and Julius CUACM 413 PresentationDocument9 pagesChingombe Kudzai and Julius CUACM 413 PresentationJeremiah NcubeNo ratings yet

- PM PresentationDocument12 pagesPM PresentationJeremiah NcubeNo ratings yet

- Group 18 PreseNtation. (Evalaution of The Synergy Between Communication and Leadersip)Document15 pagesGroup 18 PreseNtation. (Evalaution of The Synergy Between Communication and Leadersip)Jeremiah NcubeNo ratings yet

- Performance Management PresentationDocument14 pagesPerformance Management PresentationJeremiah NcubeNo ratings yet

- Question 13 Mangwiro LTDDocument3 pagesQuestion 13 Mangwiro LTDJeremiah NcubeNo ratings yet

- Joy Ben Question 13Document13 pagesJoy Ben Question 13Jeremiah NcubeNo ratings yet

- Group 3 PresentationDocument10 pagesGroup 3 PresentationJeremiah NcubeNo ratings yet

- Group 17 Block Presentation (c20141840x)Document7 pagesGroup 17 Block Presentation (c20141840x)Jeremiah NcubeNo ratings yet

- Group PresentationDocument3 pagesGroup PresentationJeremiah NcubeNo ratings yet

- Transfer Pricing, Tax Avoidance and International TaxationDocument81 pagesTransfer Pricing, Tax Avoidance and International TaxationJeremiah NcubeNo ratings yet

- SolutionDocument57 pagesSolutionJeremiah NcubeNo ratings yet

- Corporate Government Oct 2023Document1 pageCorporate Government Oct 2023Jeremiah NcubeNo ratings yet

- FIIs in India.........Document12 pagesFIIs in India.........JogenderNo ratings yet

- Branch Accounting CMADocument41 pagesBranch Accounting CMAyash.sharmaNo ratings yet

- 3 5 46 850Document5 pages3 5 46 850suresh100% (1)

- Academic Fees Payment GuidelinesDocument2 pagesAcademic Fees Payment GuidelinesCrackPODNo ratings yet

- GboDocument5 pagesGborosechaithuNo ratings yet

- SAP - FICO Course ContentDocument10 pagesSAP - FICO Course Contentchaitanya vutukuriNo ratings yet

- CH 3 Savings & Investments, Credit and DebtDocument18 pagesCH 3 Savings & Investments, Credit and DebtSURAYA BINTI HARUN MoeNo ratings yet

- Zelizer Viviana - The Proliferation of Social Currencies (Art.) PDFDocument11 pagesZelizer Viviana - The Proliferation of Social Currencies (Art.) PDFmarioNo ratings yet

- Equity Securities - Answer Key PDFDocument5 pagesEquity Securities - Answer Key PDFVikaNo ratings yet

- PT. Ungaran WanakaryaDocument2 pagesPT. Ungaran WanakaryaPrince NeroNo ratings yet

- Forex Trading 1Document6 pagesForex Trading 1Pablo Gabrio88% (8)

- Ib Form Joint Account MandateDocument1 pageIb Form Joint Account Mandatemodjo072No ratings yet

- Pile cp13Document73 pagesPile cp13casarokar100% (1)

- Chap006 Text BankDocument14 pagesChap006 Text BankAshraful AlamNo ratings yet

- 26ASDocument4 pages26ASAnubhav AsatiNo ratings yet

- Answer Capital Investment Sw2Document38 pagesAnswer Capital Investment Sw2Xandae MempinNo ratings yet

- Quiz 1 20.06.17 Q& ADocument11 pagesQuiz 1 20.06.17 Q& ADeependra NigamNo ratings yet

- Online Banking in India: Submitted byDocument20 pagesOnline Banking in India: Submitted byAastha PrakashNo ratings yet

- Module 6 IRR and Payback PeriodDocument13 pagesModule 6 IRR and Payback PeriodRhonita Dea AndariniNo ratings yet

- Nike CaseDocument8 pagesNike Casesedobi1512No ratings yet

- Investigating The Consumers' Perception Towards Usage of Plastic Money in Bangladesh: An Application of Confirmatory Factor AnalysisDocument9 pagesInvestigating The Consumers' Perception Towards Usage of Plastic Money in Bangladesh: An Application of Confirmatory Factor AnalysisHardik ShahNo ratings yet

- Budgeting Family ResourcesDocument10 pagesBudgeting Family ResourcesKing Justin ManansalaNo ratings yet

- Mbe SyllabusDocument47 pagesMbe SyllabussanyasamNo ratings yet

- Cap Budegt ProbsDocument4 pagesCap Budegt ProbsAR Ananth Rohith BhatNo ratings yet

- Ripple Investment GuideDocument20 pagesRipple Investment GuideRippleHedgeFundNo ratings yet

- Prealgebra 4th Edition Tom Carson Solutions ManualDocument26 pagesPrealgebra 4th Edition Tom Carson Solutions ManualMichaelOlsonmterj100% (39)

- (Factsheet) MBBT-19110014Document4 pages(Factsheet) MBBT-19110014Zen LohNo ratings yet

- Oliveti-ECR710 Cash RegisterDocument31 pagesOliveti-ECR710 Cash RegisterEmmanuel Lucky OhiroNo ratings yet

- Dividend Discount Model: AssumptionsDocument27 pagesDividend Discount Model: AssumptionsSairam GovarthananNo ratings yet

- XII Accontancy Pre Board IIDocument9 pagesXII Accontancy Pre Board IIShivansh JaiswalNo ratings yet