Download as docx, pdf, or txt

You might also like

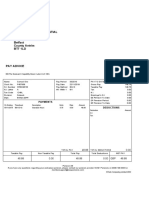

- Payslip Balp407938201933002 PDFDocument1 pagePayslip Balp407938201933002 PDFnik omek100% (1)

- Ethiopia EIU (October) : HighlightsDocument10 pagesEthiopia EIU (October) : Highlightsalokgupta87No ratings yet

- Philippines 2009-2013 Growth Projections For Project Link National Economic and Development Authority September 25, 2009Document4 pagesPhilippines 2009-2013 Growth Projections For Project Link National Economic and Development Authority September 25, 2009joeynunezNo ratings yet

- Weekly Export Risk Outlook No26 04072012Document2 pagesWeekly Export Risk Outlook No26 04072012Ali Asghar BazgirNo ratings yet

- India Economic Update: September, 2011Document17 pagesIndia Economic Update: September, 2011Rahul KaushikNo ratings yet

- Iqtisadi Eng Oct2012 RIVLIN Arab Economic WinterDocument6 pagesIqtisadi Eng Oct2012 RIVLIN Arab Economic WinterMosheDayanCenterNo ratings yet

- VN Country OutlookDocument4 pagesVN Country OutlookDang Thi Ngoc HuyenNo ratings yet

- Q#1) Productive Capacity of Various Sectors & Economic Growth in EthiopiaDocument18 pagesQ#1) Productive Capacity of Various Sectors & Economic Growth in EthiopiaManamagna OjuluNo ratings yet

- Egypt Economic ProfileDocument16 pagesEgypt Economic ProfileSameh Ahmed HassanNo ratings yet

- Country Intelligence: Report: TurkeyDocument27 pagesCountry Intelligence: Report: TurkeyFlorian SarkisNo ratings yet

- Btalk 2012 Midyear - 20120712Document45 pagesBtalk 2012 Midyear - 20120712ymahNo ratings yet

- Article - Strong Economy Despite Politics 01-1Document4 pagesArticle - Strong Economy Despite Politics 01-1Sandra MianNo ratings yet

- No. 29/2010 Inflation Report July 2010Document3 pagesNo. 29/2010 Inflation Report July 2010Amata PNo ratings yet

- Romania Long Term OutlookDocument5 pagesRomania Long Term OutlooksmaneranNo ratings yet

- Mena-2 Sunday Morning Round-Up: EgyptDocument6 pagesMena-2 Sunday Morning Round-Up: Egyptapi-66021378No ratings yet

- Add From The First Half of The Print OutsDocument4 pagesAdd From The First Half of The Print OutsAteev SinghalNo ratings yet

- World Economy 2011Document48 pagesWorld Economy 2011Arnold StalonNo ratings yet

- World Economic Situation and Prospects 2011Document48 pagesWorld Economic Situation and Prospects 2011Iris De La CalzadaNo ratings yet

- Greece Financial CrisisDocument11 pagesGreece Financial CrisisFadhili KiyaoNo ratings yet

- Financial MarketsDocument13 pagesFinancial MarketsWaqas CheemaNo ratings yet

- Karachi:: GDP Growth DefinitionDocument4 pagesKarachi:: GDP Growth DefinitionVicky AullakhNo ratings yet

- 2011 Outlook For Korean EconomyDocument2 pages2011 Outlook For Korean Economyhli9949No ratings yet

- Pakistan Economic Survey 2010 2011Document272 pagesPakistan Economic Survey 2010 2011talhaqm123No ratings yet

- What Are Emerging Markets?: Supply-DemandDocument3 pagesWhat Are Emerging Markets?: Supply-DemandMisbah UllahNo ratings yet

- Worldbank Economic Forecast PDFDocument3 pagesWorldbank Economic Forecast PDFKristian MamforteNo ratings yet

- On Shaky FoundationDocument27 pagesOn Shaky FoundationAmy HicksNo ratings yet

- Chile: 1. General TrendsDocument6 pagesChile: 1. General TrendsHenry ChavezNo ratings yet

- 2010-12-29 Yearly Review: World Economy in 2010: People in The KnowDocument5 pages2010-12-29 Yearly Review: World Economy in 2010: People in The KnowJohn Raymond Salamat PerezNo ratings yet

- 2009 Mid Year Report On Receipts and DisbursementsDocument35 pages2009 Mid Year Report On Receipts and DisbursementsNew York SenateNo ratings yet

- Greece Crisis and Impact: Dr. P.A.JohnsonDocument14 pagesGreece Crisis and Impact: Dr. P.A.JohnsonPrajwal KumarNo ratings yet

- IMF Honduras Letter of Intent 091010Document22 pagesIMF Honduras Letter of Intent 091010La GringaNo ratings yet

- A Brief History of Pakistani Economy 1947Document15 pagesA Brief History of Pakistani Economy 1947Muhammad FarhanNo ratings yet

- Plan: The United States Federal Government Should Deploy Space Solar PowerDocument26 pagesPlan: The United States Federal Government Should Deploy Space Solar PowerErica PenaNo ratings yet

- Angie M. Ashraf Ibrahim: APRIL 12, 2019 Mba Maiami 2019 Group DDocument8 pagesAngie M. Ashraf Ibrahim: APRIL 12, 2019 Mba Maiami 2019 Group DAmr MekkawyNo ratings yet

- Assignment 1Document3 pagesAssignment 1rhiza aperinNo ratings yet

- 2011Document494 pages2011aman.4uNo ratings yet

- Comparative Analysis OF WORLD'S ECONOMIC SITUATION AGAINST INDIA'S ECONOMIC SITUATION IN 2009-10Document17 pagesComparative Analysis OF WORLD'S ECONOMIC SITUATION AGAINST INDIA'S ECONOMIC SITUATION IN 2009-10jonty1222No ratings yet

- Motivation LetterDocument5 pagesMotivation LetterVlad ArmeanuNo ratings yet

- U2 Evidencia 2Document4 pagesU2 Evidencia 2api-299857592No ratings yet

- Prospects 2010Document5 pagesProspects 2010IPS Sri LankaNo ratings yet

- New ZealandDocument21 pagesNew ZealandKiran Kolhe100% (1)

- Levy Economics Institute of Bard College Strategic Analysis December 2011 Is The Recovery Sustainable?Document20 pagesLevy Economics Institute of Bard College Strategic Analysis December 2011 Is The Recovery Sustainable?mrwonkishNo ratings yet

- Brazil: 1. General TrendsDocument7 pagesBrazil: 1. General TrendsHenry ChavezNo ratings yet

- Balance of PaymentDocument5 pagesBalance of PaymentM.h. FokhruddinNo ratings yet

- BTI 2014 Laos Country ReportDocument28 pagesBTI 2014 Laos Country ReportPhilip BravoNo ratings yet

- Country Strategy 2011-2014 TurkeyDocument16 pagesCountry Strategy 2011-2014 TurkeyBeeHoofNo ratings yet

- Avoidingthecrisis BOLNarrativesDocument11 pagesAvoidingthecrisis BOLNarrativesRaheel AhmadNo ratings yet

- Govt Debt and DeficitDocument4 pagesGovt Debt and DeficitSiddharth TiwariNo ratings yet

- Turkey 2011 OutlookDocument5 pagesTurkey 2011 OutlookenergytrNo ratings yet

- Trade Growth To Ease in 2011 But Despite 2010 Record Surge, Crisis Hangover PersistsDocument9 pagesTrade Growth To Ease in 2011 But Despite 2010 Record Surge, Crisis Hangover PersistsreneavaldezNo ratings yet

- Case Study FRDocument2 pagesCase Study FRkushagra.karki2024No ratings yet

- Honduras Since The Coup: Economic and Social OutcomesDocument19 pagesHonduras Since The Coup: Economic and Social OutcomesCenter for Economic and Policy ResearchNo ratings yet

- EN EN: European CommissionDocument24 pagesEN EN: European Commissionapi-58353949No ratings yet

- Post 25 JanDocument8 pagesPost 25 JanMohammad Salah RagabNo ratings yet

- Political Instability Leads To Economic ChaosDocument8 pagesPolitical Instability Leads To Economic ChaosAmisha RiazNo ratings yet

- Weekly Economic Commentary 01-10-12Document6 pagesWeekly Economic Commentary 01-10-12karen_rogers9921No ratings yet

- Home Notifications: - View NotificationDocument22 pagesHome Notifications: - View NotificationshettyvishalNo ratings yet

- Securities Market in India: An OverviewDocument15 pagesSecurities Market in India: An OverviewShailender KumarNo ratings yet

- Argentina Executive SummaryDocument4 pagesArgentina Executive SummaryRodrigoTorresNo ratings yet

- 20-12 National BudgetDocument17 pages20-12 National BudgetMostern MbilimaNo ratings yet

- Middle East and North Africa Quarterly Economic Brief, July 2013: Growth Slowdown Extends into 2013From EverandMiddle East and North Africa Quarterly Economic Brief, July 2013: Growth Slowdown Extends into 2013No ratings yet

- Rise and Fall of NapoleonDocument13 pagesRise and Fall of Napoleonapi-280699460No ratings yet

- SPIL Atty DukaDocument14 pagesSPIL Atty DukashotyNo ratings yet

- Assume Jurisdiction: GR No. 32636 (1930) - Fluemer v. Hix DIGESTER: Alyssa MateoDocument1 pageAssume Jurisdiction: GR No. 32636 (1930) - Fluemer v. Hix DIGESTER: Alyssa Mateokim_santos_20No ratings yet

- Affirmative Action in IndiaDocument10 pagesAffirmative Action in IndiaSanjeev ShuklaNo ratings yet

- GSIS V Board of Commissioners - DigestDocument2 pagesGSIS V Board of Commissioners - DigestIsh GuidoteNo ratings yet

- Senator Russell Dissents: Richard Russell, John Sherman Cooper, and The Warren Commission Harold WeisbergDocument10 pagesSenator Russell Dissents: Richard Russell, John Sherman Cooper, and The Warren Commission Harold Weisbergdconway5No ratings yet

- Colias DubeDocument10 pagesColias DubeColias DubeNo ratings yet

- Delhi High Court Judgment of One Bar One VoteDocument50 pagesDelhi High Court Judgment of One Bar One VoteLatest Laws TeamNo ratings yet

- Gutierrez V DBM G.R. No. 153266 March 18, 2010Document7 pagesGutierrez V DBM G.R. No. 153266 March 18, 2010MWinbee VisitacionNo ratings yet

- Caste Judgement 19 Jan 2018Document5 pagesCaste Judgement 19 Jan 2018Anonymous SeNMZf28LQ100% (2)

- Treason - Offending Religious FeelingsDocument177 pagesTreason - Offending Religious FeelingsDairen CanlasNo ratings yet

- 14.4 Romulo V YniguezDocument2 pages14.4 Romulo V YniguezTrickster100% (1)

- Collective Bar GNGDocument24 pagesCollective Bar GNGgarimaNo ratings yet

- Whitmill v. Warner BrothersDocument22 pagesWhitmill v. Warner BrothersAyrLaw100% (2)

- Prophet, Ali and A Philosopher Named Ahmad Discuss The Allies Affect On The IranianDocument2 pagesProphet, Ali and A Philosopher Named Ahmad Discuss The Allies Affect On The Iranianashley_martin531No ratings yet

- The Faisal-Weizmann Agreement Jan. 3 1919Document2 pagesThe Faisal-Weizmann Agreement Jan. 3 1919InAntalyaNo ratings yet

- Human Rights and Religion Islamic Opposition To Hudood Ordinance in Pakistan The Case of Islahi and GhamidiDocument13 pagesHuman Rights and Religion Islamic Opposition To Hudood Ordinance in Pakistan The Case of Islahi and GhamidiJohn WickNo ratings yet

- The Court's Ruling: 73. City Assessor of Cebu City vs. Association de Benevola de Cebu - GR No. 152904, June 8, 2007Document15 pagesThe Court's Ruling: 73. City Assessor of Cebu City vs. Association de Benevola de Cebu - GR No. 152904, June 8, 2007April Dawn DaepNo ratings yet

- Ndejje ConstitutionDocument56 pagesNdejje ConstitutionIvan OketchoNo ratings yet

- City of Fort St. John - COVID-19 Safe Restart GrantDocument3 pagesCity of Fort St. John - COVID-19 Safe Restart GrantAlaskaHighwayNewsNo ratings yet

- Christian Empowerment Council - CEC Recommendations For ENP: Israel ProgrammeDocument13 pagesChristian Empowerment Council - CEC Recommendations For ENP: Israel Programmeapi-290059067No ratings yet

- Subic Bay Metropolitan Authority vs. Commission On Elections, 262 SCRA 492, G.R. No. 125416 September 26, 1996 PDFDocument24 pagesSubic Bay Metropolitan Authority vs. Commission On Elections, 262 SCRA 492, G.R. No. 125416 September 26, 1996 PDFMarl Dela ROsaNo ratings yet

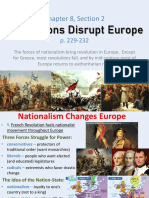

- WH - 8.2 - Revolutions Disrupt EuropeDocument6 pagesWH - 8.2 - Revolutions Disrupt EuropeS’Naii LapierreNo ratings yet

- Jurisdiction of Courts in Petitions For CertiorariDocument34 pagesJurisdiction of Courts in Petitions For Certiorarialbemart100% (1)

- Labour Laws Notes-2Document12 pagesLabour Laws Notes-2cklynn100% (2)

- 1993-G.O.Ms - No.23 dt.10.02.1993Document8 pages1993-G.O.Ms - No.23 dt.10.02.1993kamalgk100% (1)

- Case #79, 91, 103Document6 pagesCase #79, 91, 103RogelineNo ratings yet

- Economic History of IndiaDocument5 pagesEconomic History of Indiaramesh sNo ratings yet

- Contemporary World Module 1to GlobalismDocument65 pagesContemporary World Module 1to GlobalismDevouring SunNo ratings yet