AIBL eKYC Feature v2

AIBL eKYC Feature v2

You might also like

- IATA TIDS GoLite Comparison - CanadaDocument6 pagesIATA TIDS GoLite Comparison - CanadadrsinghNo ratings yet

- Order To Cash Cycle in Oracle Apps R12 With Accounting EntriesDocument34 pagesOrder To Cash Cycle in Oracle Apps R12 With Accounting EntriesKrishna Reddy100% (5)

- Solution Manual For Auditing Assurance SDocument22 pagesSolution Manual For Auditing Assurance SJillianne Jill100% (1)

- EXIM INDIA BlockchainDocument18 pagesEXIM INDIA BlockchainKrish GopalakrishnanNo ratings yet

- Model Paper - 4Document7 pagesModel Paper - 4Shiva DubeyNo ratings yet

- Quiz 1Document3 pagesQuiz 1Yong RenNo ratings yet

- Banking - Commercial Banks - SBI Case StudyDocument38 pagesBanking - Commercial Banks - SBI Case Studymitz900857% (7)

- Capstone ProjectDocument29 pagesCapstone ProjectPrashant A UNo ratings yet

- Final Ready Reckoner For PPB Agent DeckDocument28 pagesFinal Ready Reckoner For PPB Agent Deckkumarshivam100% (1)

- Jun 2021Document10 pagesJun 2021Ravi Shankar VermaNo ratings yet

- Fdd-1q-Deposit Kyckyc Final PrintDocument11 pagesFdd-1q-Deposit Kyckyc Final PrintBablu PrasadNo ratings yet

- Bio Medical ProposalDocument5 pagesBio Medical ProposalAbdulsalam ZainabNo ratings yet

- Fihfc Kyc Aml Policy March 2020Document23 pagesFihfc Kyc Aml Policy March 2020HarpreetNo ratings yet

- Trade FinanceDocument46 pagesTrade Financeeslamnaser73No ratings yet

- NBFC Nov-23 Amended NotesDocument9 pagesNBFC Nov-23 Amended Notesrtaxhelp helpNo ratings yet

- E - Svanidhi SchemeDocument16 pagesE - Svanidhi SchemeHarshit GoelNo ratings yet

- Export FinanceDocument59 pagesExport FinancerazambaNo ratings yet

- Export FinancingDocument1 pageExport Financingdharshinisridhar97No ratings yet

- Kyc-Aml-Cft - Policy KMBT - 215 - 04431Document11 pagesKyc-Aml-Cft - Policy KMBT - 215 - 04431Santosh JayasavalNo ratings yet

- Rel 201009 e 1Document19 pagesRel 201009 e 1NyaniNo ratings yet

- CITIBANKDocument7 pagesCITIBANKSreeramNo ratings yet

- FINANCE CURRENT AFFAIRS January 2022 DAY 5Document22 pagesFINANCE CURRENT AFFAIRS January 2022 DAY 5Nehal BhaisareNo ratings yet

- JAIIB Banking Operation Module D Accounting Finance For Bankers PDFDocument40 pagesJAIIB Banking Operation Module D Accounting Finance For Bankers PDFarchana cNo ratings yet

- UntitledDocument30 pagesUntitledMANSI JOSHINo ratings yet

- First Preboard FAR ReviewDocument26 pagesFirst Preboard FAR Reviewlois martinNo ratings yet

- The Question Paper Comprises Five Case Study Questions. The Candidates Are Required To Answer Any Four Case Study Questions Out of FiveDocument15 pagesThe Question Paper Comprises Five Case Study Questions. The Candidates Are Required To Answer Any Four Case Study Questions Out of FiveGokul dnNo ratings yet

- Revised Procurement Manual: (Revised W.E.F. From June 22, 2020)Document32 pagesRevised Procurement Manual: (Revised W.E.F. From June 22, 2020)pravassNo ratings yet

- Perpetual KycDocument4 pagesPerpetual KycAnjaly Ann JosephNo ratings yet

- Credit FrameworkDocument10 pagesCredit Frameworkzubair1951No ratings yet

- The Macroeconomics of Central-Bank-based Digital CurrenciesDocument42 pagesThe Macroeconomics of Central-Bank-based Digital CurrenciesJames PoulsonNo ratings yet

- Branch Less BankingDocument48 pagesBranch Less Bankingsyedasiftanveer100% (2)

- customer-service-charter-engDocument14 pagescustomer-service-charter-engDayang Nurani AfnanNo ratings yet

- Final PRJCTDocument27 pagesFinal PRJCTBilal AmjadNo ratings yet

- Best of Luck For The Finals ) : Competitive Advantage 0 )Document49 pagesBest of Luck For The Finals ) : Competitive Advantage 0 )aitzazaliNo ratings yet

- Banking Current JanuaryDocument115 pagesBanking Current JanuaryManpreet PuniaNo ratings yet

- The Gateway To Chinese ConsumersDocument21 pagesThe Gateway To Chinese Consumerszvfymzj74fNo ratings yet

- Core Banking System ModificationDocument29 pagesCore Banking System Modificationsln20ideNo ratings yet

- KYC Policy-Internet Version-Updated Upto 10.05.2021-CompressedDocument73 pagesKYC Policy-Internet Version-Updated Upto 10.05.2021-CompressedAmaanNo ratings yet

- 240066_05df4a1c-189d-42a4-9ecb-4dd2d5fa5412Document1 page240066_05df4a1c-189d-42a4-9ecb-4dd2d5fa5412dempseym135No ratings yet

- Credit Card Issuance and Conduct PolicyDocument11 pagesCredit Card Issuance and Conduct Policykabiiniya2019No ratings yet

- New Terms and ConditionDocument14 pagesNew Terms and ConditionBernie BenastoNo ratings yet

- BIL Amazon PackageDocument2 pagesBIL Amazon PackagePunit SardaNo ratings yet

- North East University Bangladesh Assignment OnDocument9 pagesNorth East University Bangladesh Assignment OnSahriar EmonNo ratings yet

- ICDS - Trading DisclosuresDocument3 pagesICDS - Trading DisclosuresSneha AgarwalNo ratings yet

- External Commercial Borrowing: Minimum Average Maturity of 3 YearsDocument24 pagesExternal Commercial Borrowing: Minimum Average Maturity of 3 YearsauavNo ratings yet

- E-Banking: Chapter ADocument35 pagesE-Banking: Chapter ApseNo ratings yet

- Catarman Executive Summary 2022Document6 pagesCatarman Executive Summary 2022kmarkcramosNo ratings yet

- Factoring: Presented By-Asheesh Pratima Priyanka Devkaran Prachi From: NIT - BHOPAL (MBA 2009-11)Document30 pagesFactoring: Presented By-Asheesh Pratima Priyanka Devkaran Prachi From: NIT - BHOPAL (MBA 2009-11)Chakraborty PankajNo ratings yet

- By Prof. Santosh KumarDocument44 pagesBy Prof. Santosh KumarSuraj KumarNo ratings yet

- Concurrent AuditDocument15 pagesConcurrent AuditAkash Agarwal100% (2)

- Export Finance: Project Guide: Prof.S.B. Kasture Project Prepared By: Sachin Parab Nmims MFM - Iii B ROLL NO.113Document56 pagesExport Finance: Project Guide: Prof.S.B. Kasture Project Prepared By: Sachin Parab Nmims MFM - Iii B ROLL NO.113rahulsatelli100% (2)

- News Magazine Jan 2022Document10 pagesNews Magazine Jan 2022kanarendranNo ratings yet

- 1.customer RequirementDocument26 pages1.customer RequirementKamila sharminNo ratings yet

- Credit Monitoring Policy - A Glimpse: Digital TrainingDocument9 pagesCredit Monitoring Policy - A Glimpse: Digital TrainingAjay Singh PhogatNo ratings yet

- B BB Bbanking Anking Anking Anking Anking: U Uu Uupdate Pdate Pdate Pdate PdateDocument20 pagesB BB Bbanking Anking Anking Anking Anking: U Uu Uupdate Pdate Pdate Pdate PdateGuruswami PrakashNo ratings yet

- Bank Concurrent AuditDocument15 pagesBank Concurrent AuditNaveen KondabathulaNo ratings yet

- Kyc V6 22072021Document4 pagesKyc V6 22072021pxp2k8mdmfNo ratings yet

- Kyc and Aml Guidelines-2020Document52 pagesKyc and Aml Guidelines-2020Nishesh KumarNo ratings yet

- Sidbi Ar 2021 22Document91 pagesSidbi Ar 2021 22kumar sivaNo ratings yet

- CFAS Reviewer - Module 4Document14 pagesCFAS Reviewer - Module 4Lizette Janiya SumantingNo ratings yet

- The Basel Ii "Use Test" - a Retail Credit Approach: Developing and Implementing Effective Retail Credit Risk Strategies Using Basel IiFrom EverandThe Basel Ii "Use Test" - a Retail Credit Approach: Developing and Implementing Effective Retail Credit Risk Strategies Using Basel IiNo ratings yet

- Credit Derivatives and Structured Credit: A Guide for InvestorsFrom EverandCredit Derivatives and Structured Credit: A Guide for InvestorsNo ratings yet

- Consumer Lending Revenues World Summary: Market Values & Financials by CountryFrom EverandConsumer Lending Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Bank ReconciliationDocument6 pagesBank Reconciliationclarisse jaramillaNo ratings yet

- The Role of Blockchain in BankingDocument32 pagesThe Role of Blockchain in BankingHARIHARANNo ratings yet

- Income StatementDocument32 pagesIncome StatementAllen Ray TraqueñaNo ratings yet

- Digital SystemDocument71 pagesDigital SystemKing KelishNo ratings yet

- MBBsavings - 158118 107625 - 2016 12 31Document7 pagesMBBsavings - 158118 107625 - 2016 12 31Zahar ZekNo ratings yet

- AdvanceReceipt2021 04 22 13 17 51Document8 pagesAdvanceReceipt2021 04 22 13 17 51Ashraf AliNo ratings yet

- Kieronivanmendozagutierrez: Page1of3 Roxasdrst 4 2 1 9 - 9 9 5 6 - 4 5 Brgystonino Calapan Mindoroorientalcalapan 5 2 0 0Document4 pagesKieronivanmendozagutierrez: Page1of3 Roxasdrst 4 2 1 9 - 9 9 5 6 - 4 5 Brgystonino Calapan Mindoroorientalcalapan 5 2 0 0Kieron Ivan Mendoza GutierrezNo ratings yet

- Checks Module DocumentationDocument15 pagesChecks Module DocumentationMohamed AbdelattyNo ratings yet

- Haji AliDocument9 pagesHaji AliVaibhav PakhaleNo ratings yet

- J WF 1 J Lflujq Iaj AnDocument13 pagesJ WF 1 J Lflujq Iaj AnOmprakash JhaNo ratings yet

- Functional Analysis of Digital PaymentDocument57 pagesFunctional Analysis of Digital PaymentSejal MehrotraNo ratings yet

- Sachin Case VIVA 11septDocument2 pagesSachin Case VIVA 11septAYESHA RACHH 2127567No ratings yet

- Real SimpleDocument62 pagesReal Simplebandgar_007No ratings yet

- Accounting ConceptsDocument12 pagesAccounting ConceptsshafnafNo ratings yet

- Dimayuga TV Repair ShopDocument6 pagesDimayuga TV Repair ShoptakycabrejasNo ratings yet

- Akl Ii TM 10Document5 pagesAkl Ii TM 10Amalia FillahNo ratings yet

- AR Absolute Return + Alpha Billion Dollar Club 2010Document3 pagesAR Absolute Return + Alpha Billion Dollar Club 2010Absolute Return100% (1)

- Mas First Preboard Examination Batch 95Document11 pagesMas First Preboard Examination Batch 95Lhairyz Francine RamirezNo ratings yet

- GR12 Business Finance Module 3-4Document8 pagesGR12 Business Finance Module 3-4Jean Diane JoveloNo ratings yet

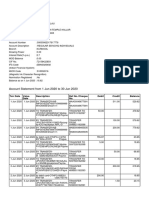

- Account Statement From 1 Jun 2020 To 30 Jun 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument4 pagesAccount Statement From 1 Jun 2020 To 30 Jun 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalancebalajiNo ratings yet

- Quiz No. 1 Accounting PrinciplesDocument4 pagesQuiz No. 1 Accounting PrinciplesElla Feliciano100% (1)

- 37.human Resource Information System Cholamandal InsuranceDocument28 pages37.human Resource Information System Cholamandal InsurancerajNo ratings yet

- Amount Rs. This Forms Part of The PERSONAL LOAN Agreement Executed Between - Insert The NameDocument13 pagesAmount Rs. This Forms Part of The PERSONAL LOAN Agreement Executed Between - Insert The NameKapil KaroliyaNo ratings yet

- International Corporate Finance: Mcgraw-Hill/IrwinDocument38 pagesInternational Corporate Finance: Mcgraw-Hill/IrwinSurya AjiNo ratings yet

- PM 2Document16 pagesPM 2priyanshu.goel1710No ratings yet

- Genuime Company Required 1 Debit CreditDocument15 pagesGenuime Company Required 1 Debit CreditAnonnNo ratings yet

Download as pdf or txt

You might also like

- IATA TIDS GoLite Comparison - CanadaDocument6 pagesIATA TIDS GoLite Comparison - CanadadrsinghNo ratings yet

- Order To Cash Cycle in Oracle Apps R12 With Accounting EntriesDocument34 pagesOrder To Cash Cycle in Oracle Apps R12 With Accounting EntriesKrishna Reddy100% (5)

- Solution Manual For Auditing Assurance SDocument22 pagesSolution Manual For Auditing Assurance SJillianne Jill100% (1)

- EXIM INDIA BlockchainDocument18 pagesEXIM INDIA BlockchainKrish GopalakrishnanNo ratings yet

- Model Paper - 4Document7 pagesModel Paper - 4Shiva DubeyNo ratings yet

- Quiz 1Document3 pagesQuiz 1Yong RenNo ratings yet

- Banking - Commercial Banks - SBI Case StudyDocument38 pagesBanking - Commercial Banks - SBI Case Studymitz900857% (7)

- Capstone ProjectDocument29 pagesCapstone ProjectPrashant A UNo ratings yet

- Final Ready Reckoner For PPB Agent DeckDocument28 pagesFinal Ready Reckoner For PPB Agent Deckkumarshivam100% (1)

- Jun 2021Document10 pagesJun 2021Ravi Shankar VermaNo ratings yet

- Fdd-1q-Deposit Kyckyc Final PrintDocument11 pagesFdd-1q-Deposit Kyckyc Final PrintBablu PrasadNo ratings yet

- Bio Medical ProposalDocument5 pagesBio Medical ProposalAbdulsalam ZainabNo ratings yet

- Fihfc Kyc Aml Policy March 2020Document23 pagesFihfc Kyc Aml Policy March 2020HarpreetNo ratings yet

- Trade FinanceDocument46 pagesTrade Financeeslamnaser73No ratings yet

- NBFC Nov-23 Amended NotesDocument9 pagesNBFC Nov-23 Amended Notesrtaxhelp helpNo ratings yet

- E - Svanidhi SchemeDocument16 pagesE - Svanidhi SchemeHarshit GoelNo ratings yet

- Export FinanceDocument59 pagesExport FinancerazambaNo ratings yet

- Export FinancingDocument1 pageExport Financingdharshinisridhar97No ratings yet

- Kyc-Aml-Cft - Policy KMBT - 215 - 04431Document11 pagesKyc-Aml-Cft - Policy KMBT - 215 - 04431Santosh JayasavalNo ratings yet

- Rel 201009 e 1Document19 pagesRel 201009 e 1NyaniNo ratings yet

- CITIBANKDocument7 pagesCITIBANKSreeramNo ratings yet

- FINANCE CURRENT AFFAIRS January 2022 DAY 5Document22 pagesFINANCE CURRENT AFFAIRS January 2022 DAY 5Nehal BhaisareNo ratings yet

- JAIIB Banking Operation Module D Accounting Finance For Bankers PDFDocument40 pagesJAIIB Banking Operation Module D Accounting Finance For Bankers PDFarchana cNo ratings yet

- UntitledDocument30 pagesUntitledMANSI JOSHINo ratings yet

- First Preboard FAR ReviewDocument26 pagesFirst Preboard FAR Reviewlois martinNo ratings yet

- The Question Paper Comprises Five Case Study Questions. The Candidates Are Required To Answer Any Four Case Study Questions Out of FiveDocument15 pagesThe Question Paper Comprises Five Case Study Questions. The Candidates Are Required To Answer Any Four Case Study Questions Out of FiveGokul dnNo ratings yet

- Revised Procurement Manual: (Revised W.E.F. From June 22, 2020)Document32 pagesRevised Procurement Manual: (Revised W.E.F. From June 22, 2020)pravassNo ratings yet

- Perpetual KycDocument4 pagesPerpetual KycAnjaly Ann JosephNo ratings yet

- Credit FrameworkDocument10 pagesCredit Frameworkzubair1951No ratings yet

- The Macroeconomics of Central-Bank-based Digital CurrenciesDocument42 pagesThe Macroeconomics of Central-Bank-based Digital CurrenciesJames PoulsonNo ratings yet

- Branch Less BankingDocument48 pagesBranch Less Bankingsyedasiftanveer100% (2)

- customer-service-charter-engDocument14 pagescustomer-service-charter-engDayang Nurani AfnanNo ratings yet

- Final PRJCTDocument27 pagesFinal PRJCTBilal AmjadNo ratings yet

- Best of Luck For The Finals ) : Competitive Advantage 0 )Document49 pagesBest of Luck For The Finals ) : Competitive Advantage 0 )aitzazaliNo ratings yet

- Banking Current JanuaryDocument115 pagesBanking Current JanuaryManpreet PuniaNo ratings yet

- The Gateway To Chinese ConsumersDocument21 pagesThe Gateway To Chinese Consumerszvfymzj74fNo ratings yet

- Core Banking System ModificationDocument29 pagesCore Banking System Modificationsln20ideNo ratings yet

- KYC Policy-Internet Version-Updated Upto 10.05.2021-CompressedDocument73 pagesKYC Policy-Internet Version-Updated Upto 10.05.2021-CompressedAmaanNo ratings yet

- 240066_05df4a1c-189d-42a4-9ecb-4dd2d5fa5412Document1 page240066_05df4a1c-189d-42a4-9ecb-4dd2d5fa5412dempseym135No ratings yet

- Credit Card Issuance and Conduct PolicyDocument11 pagesCredit Card Issuance and Conduct Policykabiiniya2019No ratings yet

- New Terms and ConditionDocument14 pagesNew Terms and ConditionBernie BenastoNo ratings yet

- BIL Amazon PackageDocument2 pagesBIL Amazon PackagePunit SardaNo ratings yet

- North East University Bangladesh Assignment OnDocument9 pagesNorth East University Bangladesh Assignment OnSahriar EmonNo ratings yet

- ICDS - Trading DisclosuresDocument3 pagesICDS - Trading DisclosuresSneha AgarwalNo ratings yet

- External Commercial Borrowing: Minimum Average Maturity of 3 YearsDocument24 pagesExternal Commercial Borrowing: Minimum Average Maturity of 3 YearsauavNo ratings yet

- E-Banking: Chapter ADocument35 pagesE-Banking: Chapter ApseNo ratings yet

- Catarman Executive Summary 2022Document6 pagesCatarman Executive Summary 2022kmarkcramosNo ratings yet

- Factoring: Presented By-Asheesh Pratima Priyanka Devkaran Prachi From: NIT - BHOPAL (MBA 2009-11)Document30 pagesFactoring: Presented By-Asheesh Pratima Priyanka Devkaran Prachi From: NIT - BHOPAL (MBA 2009-11)Chakraborty PankajNo ratings yet

- By Prof. Santosh KumarDocument44 pagesBy Prof. Santosh KumarSuraj KumarNo ratings yet

- Concurrent AuditDocument15 pagesConcurrent AuditAkash Agarwal100% (2)

- Export Finance: Project Guide: Prof.S.B. Kasture Project Prepared By: Sachin Parab Nmims MFM - Iii B ROLL NO.113Document56 pagesExport Finance: Project Guide: Prof.S.B. Kasture Project Prepared By: Sachin Parab Nmims MFM - Iii B ROLL NO.113rahulsatelli100% (2)

- News Magazine Jan 2022Document10 pagesNews Magazine Jan 2022kanarendranNo ratings yet

- 1.customer RequirementDocument26 pages1.customer RequirementKamila sharminNo ratings yet

- Credit Monitoring Policy - A Glimpse: Digital TrainingDocument9 pagesCredit Monitoring Policy - A Glimpse: Digital TrainingAjay Singh PhogatNo ratings yet

- B BB Bbanking Anking Anking Anking Anking: U Uu Uupdate Pdate Pdate Pdate PdateDocument20 pagesB BB Bbanking Anking Anking Anking Anking: U Uu Uupdate Pdate Pdate Pdate PdateGuruswami PrakashNo ratings yet

- Bank Concurrent AuditDocument15 pagesBank Concurrent AuditNaveen KondabathulaNo ratings yet

- Kyc V6 22072021Document4 pagesKyc V6 22072021pxp2k8mdmfNo ratings yet

- Kyc and Aml Guidelines-2020Document52 pagesKyc and Aml Guidelines-2020Nishesh KumarNo ratings yet

- Sidbi Ar 2021 22Document91 pagesSidbi Ar 2021 22kumar sivaNo ratings yet

- CFAS Reviewer - Module 4Document14 pagesCFAS Reviewer - Module 4Lizette Janiya SumantingNo ratings yet

- The Basel Ii "Use Test" - a Retail Credit Approach: Developing and Implementing Effective Retail Credit Risk Strategies Using Basel IiFrom EverandThe Basel Ii "Use Test" - a Retail Credit Approach: Developing and Implementing Effective Retail Credit Risk Strategies Using Basel IiNo ratings yet

- Credit Derivatives and Structured Credit: A Guide for InvestorsFrom EverandCredit Derivatives and Structured Credit: A Guide for InvestorsNo ratings yet

- Consumer Lending Revenues World Summary: Market Values & Financials by CountryFrom EverandConsumer Lending Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Bank ReconciliationDocument6 pagesBank Reconciliationclarisse jaramillaNo ratings yet

- The Role of Blockchain in BankingDocument32 pagesThe Role of Blockchain in BankingHARIHARANNo ratings yet

- Income StatementDocument32 pagesIncome StatementAllen Ray TraqueñaNo ratings yet

- Digital SystemDocument71 pagesDigital SystemKing KelishNo ratings yet

- MBBsavings - 158118 107625 - 2016 12 31Document7 pagesMBBsavings - 158118 107625 - 2016 12 31Zahar ZekNo ratings yet

- AdvanceReceipt2021 04 22 13 17 51Document8 pagesAdvanceReceipt2021 04 22 13 17 51Ashraf AliNo ratings yet

- Kieronivanmendozagutierrez: Page1of3 Roxasdrst 4 2 1 9 - 9 9 5 6 - 4 5 Brgystonino Calapan Mindoroorientalcalapan 5 2 0 0Document4 pagesKieronivanmendozagutierrez: Page1of3 Roxasdrst 4 2 1 9 - 9 9 5 6 - 4 5 Brgystonino Calapan Mindoroorientalcalapan 5 2 0 0Kieron Ivan Mendoza GutierrezNo ratings yet

- Checks Module DocumentationDocument15 pagesChecks Module DocumentationMohamed AbdelattyNo ratings yet

- Haji AliDocument9 pagesHaji AliVaibhav PakhaleNo ratings yet

- J WF 1 J Lflujq Iaj AnDocument13 pagesJ WF 1 J Lflujq Iaj AnOmprakash JhaNo ratings yet

- Functional Analysis of Digital PaymentDocument57 pagesFunctional Analysis of Digital PaymentSejal MehrotraNo ratings yet

- Sachin Case VIVA 11septDocument2 pagesSachin Case VIVA 11septAYESHA RACHH 2127567No ratings yet

- Real SimpleDocument62 pagesReal Simplebandgar_007No ratings yet

- Accounting ConceptsDocument12 pagesAccounting ConceptsshafnafNo ratings yet

- Dimayuga TV Repair ShopDocument6 pagesDimayuga TV Repair ShoptakycabrejasNo ratings yet

- Akl Ii TM 10Document5 pagesAkl Ii TM 10Amalia FillahNo ratings yet

- AR Absolute Return + Alpha Billion Dollar Club 2010Document3 pagesAR Absolute Return + Alpha Billion Dollar Club 2010Absolute Return100% (1)

- Mas First Preboard Examination Batch 95Document11 pagesMas First Preboard Examination Batch 95Lhairyz Francine RamirezNo ratings yet

- GR12 Business Finance Module 3-4Document8 pagesGR12 Business Finance Module 3-4Jean Diane JoveloNo ratings yet

- Account Statement From 1 Jun 2020 To 30 Jun 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument4 pagesAccount Statement From 1 Jun 2020 To 30 Jun 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalancebalajiNo ratings yet

- Quiz No. 1 Accounting PrinciplesDocument4 pagesQuiz No. 1 Accounting PrinciplesElla Feliciano100% (1)

- 37.human Resource Information System Cholamandal InsuranceDocument28 pages37.human Resource Information System Cholamandal InsurancerajNo ratings yet

- Amount Rs. This Forms Part of The PERSONAL LOAN Agreement Executed Between - Insert The NameDocument13 pagesAmount Rs. This Forms Part of The PERSONAL LOAN Agreement Executed Between - Insert The NameKapil KaroliyaNo ratings yet

- International Corporate Finance: Mcgraw-Hill/IrwinDocument38 pagesInternational Corporate Finance: Mcgraw-Hill/IrwinSurya AjiNo ratings yet

- PM 2Document16 pagesPM 2priyanshu.goel1710No ratings yet

- Genuime Company Required 1 Debit CreditDocument15 pagesGenuime Company Required 1 Debit CreditAnonnNo ratings yet