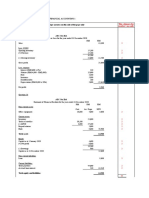

EACC1614 2023 memo main exam final

EACC1614 2023 memo main exam final

You might also like

- FAR270 JULY 2022 SolutionDocument8 pagesFAR270 JULY 2022 SolutionNur Fatin Amirah100% (3)

- Lazar Blue Book Chapter 4 Solution (1 To 14 Only)Document27 pagesLazar Blue Book Chapter 4 Solution (1 To 14 Only)Shuhada Shamsuddin75% (4)

- FAR210 - Feb 2023 - SSDocument11 pagesFAR210 - Feb 2023 - SSfarisha aliahNo ratings yet

- Far410 - SS - Feb 2022Document9 pagesFar410 - SS - Feb 2022AFIZA JASMANNo ratings yet

- SOLUTION DEC 2018 No TicksDocument8 pagesSOLUTION DEC 2018 No Ticksanis izzatiNo ratings yet

- Gr. 12 March 2022 Acc MGDocument7 pagesGr. 12 March 2022 Acc MGkhanyisilentshingila7No ratings yet

- ACCOUNTING P1 GR10 MEMO NOV2020 - EnglishDocument6 pagesACCOUNTING P1 GR10 MEMO NOV2020 - EnglishMolemo mabeleNo ratings yet

- MARCH MOCK 2024 MGDocument6 pagesMARCH MOCK 2024 MGkhanyisilentshingila7No ratings yet

- 20solution Far460 - Jun 2020 - StudentDocument10 pages20solution Far460 - Jun 2020 - StudentRuzaikha razaliNo ratings yet

- Faculty of Accountancy Bachelor of Accountancy (Hons.)Document8 pagesFaculty of Accountancy Bachelor of Accountancy (Hons.)Syafahani SafieNo ratings yet

- GP 2 Far 620Document8 pagesGP 2 Far 620Syafahani SafieNo ratings yet

- GR11 Accounting Practice Exam Memorandum June Paper 1 PDFDocument6 pagesGR11 Accounting Practice Exam Memorandum June Paper 1 PDFGood LifeNo ratings yet

- Ss Far270 Fa Aug2021.PDFDocument11 pagesSs Far270 Fa Aug2021.PDFRusyda AzizNo ratings yet

- Fa July2023-Far210-StudentDocument9 pagesFa July2023-Far210-Student2022613976No ratings yet

- Chapter 07 - Financial StatementsDocument40 pagesChapter 07 - Financial StatementsMkhonto XuluNo ratings yet

- GR10 Accounting Practice Exam Memorandum November Paper 1Document7 pagesGR10 Accounting Practice Exam Memorandum November Paper 1morukakgothatso5No ratings yet

- GP 2 Far 620Document17 pagesGP 2 Far 620Syafahani SafieNo ratings yet

- GR11 Accounting Practice Exam Memorandum November Paper 1-1 PDFDocument8 pagesGR11 Accounting Practice Exam Memorandum November Paper 1-1 PDFGood LifeNo ratings yet

- Group Project 2 Far620Document8 pagesGroup Project 2 Far620NUR ATHIRAH SUKAIMINo ratings yet

- Unit 12-Question 12-D Sol (2023)Document2 pagesUnit 12-Question 12-D Sol (2023)shirleygebenga020829No ratings yet

- Far210 - Feb2022 SS Q5Document3 pagesFar210 - Feb2022 SS Q5imn njwaaaNo ratings yet

- Accounting GR 11 June 2022 Marking GuidelineDocument5 pagesAccounting GR 11 June 2022 Marking Guidelineamilesithole1709No ratings yet

- Official GR 12 Accounting P1 Eng MemoDocument11 pagesOfficial GR 12 Accounting P1 Eng MemohlayisofilesNo ratings yet

- FAR270 - FEB 2022 SolutionDocument8 pagesFAR270 - FEB 2022 SolutionNur Fatin AmirahNo ratings yet

- Set_1_FA_SSS_FAR210_FEB2022.pdf (1)Document10 pagesSet_1_FA_SSS_FAR210_FEB2022.pdf (1)Rusyda AzizNo ratings yet

- FAC1601 Assignment 4 Solutions First Semester 2022Document17 pagesFAC1601 Assignment 4 Solutions First Semester 2022Nkhangweni Rambuda100% (1)

- Eacc1614 Test 2 Memo 2021 AdjDocument10 pagesEacc1614 Test 2 Memo 2021 AdjshabanguntandoyenkosiNo ratings yet

- Accounting P1 Memo May June 2023 Eng Free StateDocument11 pagesAccounting P1 Memo May June 2023 Eng Free StateSimiNo ratings yet

- EACC1614 Main Exam Memo 2022Document6 pagesEACC1614 Main Exam Memo 2022asandantlumayo77No ratings yet

- August Q1Document3 pagesAugust Q1tengku rilNo ratings yet

- Tuto 6Document6 pagesTuto 6WEI QUAN LEENo ratings yet

- ACC117 - Chapter 4-3 - Tutorial - Solution - Textbook Page 95, 98 - 99Document6 pagesACC117 - Chapter 4-3 - Tutorial - Solution - Textbook Page 95, 98 - 99taerrybombNo ratings yet

- Past Exam QuestionDocument3 pagesPast Exam QuestionYến Hoàng HảiNo ratings yet

- Far570 Group ProjectDocument4 pagesFar570 Group ProjectN FrzanahNo ratings yet

- Accounting Worksheet 2 Answer SheetDocument31 pagesAccounting Worksheet 2 Answer Sheetzeldazitha87No ratings yet

- Group Project 2 - Published Account DEC2019 FAR270 - SSDocument6 pagesGroup Project 2 - Published Account DEC2019 FAR270 - SSHaru BiruNo ratings yet

- FAR210 Aug 2023 S PDFDocument10 pagesFAR210 Aug 2023 S PDFNUR AYUNI BALQISH AHMAD MULIADINo ratings yet

- JAN 2024 (1)Document3 pagesJAN 2024 (1)Nur Alya DamiaNo ratings yet

- LC032GLP000EVDocument16 pagesLC032GLP000EVrianrocheNo ratings yet

- Sam's Introductory Accounting AnswersDocument1 pageSam's Introductory Accounting AnswersSamuelNo ratings yet

- Unit 12-Question 12-C Sol (2023)Document2 pagesUnit 12-Question 12-C Sol (2023)shirleygebenga020829No ratings yet

- Bac 3 Review QNSDocument16 pagesBac 3 Review QNSsaidkhatib368No ratings yet

- Income Statements For The November: @Chapter7AnalyslngandlnterpretlngflnanclalstatementsDocument1 pageIncome Statements For The November: @Chapter7AnalyslngandlnterpretlngflnanclalstatementsAik Luen LimNo ratings yet

- FAR270_AC1104EDocument17 pagesFAR270_AC1104ENur SaidatulNo ratings yet

- Taxation Solution 2018 SeptemberDocument9 pagesTaxation Solution 2018 SeptemberIffah NasuhaaNo ratings yet

- RBGH Financials 31 December 2020 Colour 18.03.2021 3 Full PageseddDocument3 pagesRBGH Financials 31 December 2020 Colour 18.03.2021 3 Full PageseddFuaad DodooNo ratings yet

- Assignment 1 (Part 2)Document10 pagesAssignment 1 (Part 2)Sanghya MahendranNo ratings yet

- Ans Jan 2018 Far410Document8 pagesAns Jan 2018 Far4102022478048No ratings yet

- Profit & Loss Accounts: Wing Chair GirogioDocument3 pagesProfit & Loss Accounts: Wing Chair Girogiofarsi786No ratings yet

- Annual-Report-FML-30-June-2020-23 Vol 2Document1 pageAnnual-Report-FML-30-June-2020-23 Vol 2Bluish FlameNo ratings yet

- PYQ June 2018Document4 pagesPYQ June 2018Nur Amira NadiaNo ratings yet

- 11 ACC CH 6.11 To 6.16 MemosDocument19 pages11 ACC CH 6.11 To 6.16 Memosora mashaNo ratings yet

- Accountancy & Auditing-IDocument4 pagesAccountancy & Auditing-Izaman virkNo ratings yet

- Fin Acc n6 Int. Exam 2017 s2 MGDocument7 pagesFin Acc n6 Int. Exam 2017 s2 MGprofessional accountantsNo ratings yet

- The Institute of Chartered Accountants of Bangladesh: Sample Question Paper Certificate Level-AccountingDocument8 pagesThe Institute of Chartered Accountants of Bangladesh: Sample Question Paper Certificate Level-AccountingArif UddinNo ratings yet

- FAC1602 Exam PackDocument25 pagesFAC1602 Exam PackNthabeza De Ntha MogaleNo ratings yet

- Ans Cabi - 2012 - FaDocument19 pagesAns Cabi - 2012 - FaJahanzaib ButtNo ratings yet

- Yolanda Reality Work Sheet For The Month Ended April 2020Document2 pagesYolanda Reality Work Sheet For The Month Ended April 2020Hannah DimalibotNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Equity Valuation: Models from Leading Investment BanksFrom EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNo ratings yet

- Goto 1702966919Document5 pagesGoto 1702966919Anonymous XoUqrqyuNo ratings yet

- Chapter 10Document18 pagesChapter 10Yousef WardatNo ratings yet

- Annexure 1Document2 pagesAnnexure 1National HeraldNo ratings yet

- Financial Accounting Marathon PartnershipDocument37 pagesFinancial Accounting Marathon PartnershipPriyvrat MamgainNo ratings yet

- Assemblies of God Building Projects Stand 3435 Unit 3 Kudube 0400Document2 pagesAssemblies of God Building Projects Stand 3435 Unit 3 Kudube 0400Mandlakayise MabizelaNo ratings yet

- Issue and Redemption of Shares 2Document3 pagesIssue and Redemption of Shares 2Prince TshepoNo ratings yet

- CH 14 FMDocument2 pagesCH 14 FMAsep KurniaNo ratings yet

- CH 18 IFM10 CH 19 Test BankDocument12 pagesCH 18 IFM10 CH 19 Test Bankajones1219100% (1)

- Befa Question BankDocument9 pagesBefa Question Bank20bd1a6655No ratings yet

- Intermediate Accounting I - Notes (9.13.2022)Document18 pagesIntermediate Accounting I - Notes (9.13.2022)Mainit, Shiela Mae, S.No ratings yet

- Final AccountsDocument18 pagesFinal AccountsAkella kavya SharmaNo ratings yet

- Chap 14Document27 pagesChap 14Thu YếnNo ratings yet

- Untitled 7Document2 pagesUntitled 7subhash221103No ratings yet

- Intercompany DividendsDocument6 pagesIntercompany DividendsClauie BarsNo ratings yet

- CFA一级基础段衍生 Tom 标准版Document113 pagesCFA一级基础段衍生 Tom 标准版Evelyn YangNo ratings yet

- Problem 1 - The Accounts and Their Balances in The Ledger of Generic Pharma On December 31Document2 pagesProblem 1 - The Accounts and Their Balances in The Ledger of Generic Pharma On December 31Pepegon SalinasNo ratings yet

- Business License Single Page With Group 171393758498Document1 pageBusiness License Single Page With Group 171393758498Affan AhmadNo ratings yet

- Ratios of BajajDocument2 pagesRatios of BajajSunil KumarNo ratings yet

- Chapter 2: Statement of Financial Position Statement of Financial PositionDocument16 pagesChapter 2: Statement of Financial Position Statement of Financial PositionDaniella Mae ElipNo ratings yet

- Caf 5 Far1 Spring 2019xsxDocument5 pagesCaf 5 Far1 Spring 2019xsxMustafa ZaheerNo ratings yet

- Investment in AssociateDocument2 pagesInvestment in AssociateChiChi0% (1)

- Cover PageDocument6 pagesCover PageJobair TanvirNo ratings yet

- University of The Cordilleras College of Accountancy Quiz On Partnership Formation 1Document6 pagesUniversity of The Cordilleras College of Accountancy Quiz On Partnership Formation 1Ian Ranilopa100% (1)

- AQR Momentum Index MethodologyDocument8 pagesAQR Momentum Index MethodologyHo Kai LunNo ratings yet

- Capital BudgetingDocument26 pagesCapital BudgetingB112NITESH KUMAR SAHUNo ratings yet

- Job Order CostingDocument39 pagesJob Order CostingCharisse Ahnne Toslolado100% (1)

- Solutions To Problems: Smart/Gitman/Joehnk, Fundamentals of Investing, 12/e Chapter 3Document2 pagesSolutions To Problems: Smart/Gitman/Joehnk, Fundamentals of Investing, 12/e Chapter 3Rio Yow-yow Lansang CastroNo ratings yet

- Ch13 Wiley Plus Wk3Document58 pagesCh13 Wiley Plus Wk3Prakash VaidhyanathanNo ratings yet

- Sample Case StudiesDocument29 pagesSample Case StudiesAbc SNo ratings yet

- 11 EM ACC PUBLIC MLM 23-24 - PagenumberDocument11 pages11 EM ACC PUBLIC MLM 23-24 - Pagenumberkms195kds2007No ratings yet

Download as xlsx, pdf, or txt

You might also like

- FAR270 JULY 2022 SolutionDocument8 pagesFAR270 JULY 2022 SolutionNur Fatin Amirah100% (3)

- Lazar Blue Book Chapter 4 Solution (1 To 14 Only)Document27 pagesLazar Blue Book Chapter 4 Solution (1 To 14 Only)Shuhada Shamsuddin75% (4)

- FAR210 - Feb 2023 - SSDocument11 pagesFAR210 - Feb 2023 - SSfarisha aliahNo ratings yet

- Far410 - SS - Feb 2022Document9 pagesFar410 - SS - Feb 2022AFIZA JASMANNo ratings yet

- SOLUTION DEC 2018 No TicksDocument8 pagesSOLUTION DEC 2018 No Ticksanis izzatiNo ratings yet

- Gr. 12 March 2022 Acc MGDocument7 pagesGr. 12 March 2022 Acc MGkhanyisilentshingila7No ratings yet

- ACCOUNTING P1 GR10 MEMO NOV2020 - EnglishDocument6 pagesACCOUNTING P1 GR10 MEMO NOV2020 - EnglishMolemo mabeleNo ratings yet

- MARCH MOCK 2024 MGDocument6 pagesMARCH MOCK 2024 MGkhanyisilentshingila7No ratings yet

- 20solution Far460 - Jun 2020 - StudentDocument10 pages20solution Far460 - Jun 2020 - StudentRuzaikha razaliNo ratings yet

- Faculty of Accountancy Bachelor of Accountancy (Hons.)Document8 pagesFaculty of Accountancy Bachelor of Accountancy (Hons.)Syafahani SafieNo ratings yet

- GP 2 Far 620Document8 pagesGP 2 Far 620Syafahani SafieNo ratings yet

- GR11 Accounting Practice Exam Memorandum June Paper 1 PDFDocument6 pagesGR11 Accounting Practice Exam Memorandum June Paper 1 PDFGood LifeNo ratings yet

- Ss Far270 Fa Aug2021.PDFDocument11 pagesSs Far270 Fa Aug2021.PDFRusyda AzizNo ratings yet

- Fa July2023-Far210-StudentDocument9 pagesFa July2023-Far210-Student2022613976No ratings yet

- Chapter 07 - Financial StatementsDocument40 pagesChapter 07 - Financial StatementsMkhonto XuluNo ratings yet

- GR10 Accounting Practice Exam Memorandum November Paper 1Document7 pagesGR10 Accounting Practice Exam Memorandum November Paper 1morukakgothatso5No ratings yet

- GP 2 Far 620Document17 pagesGP 2 Far 620Syafahani SafieNo ratings yet

- GR11 Accounting Practice Exam Memorandum November Paper 1-1 PDFDocument8 pagesGR11 Accounting Practice Exam Memorandum November Paper 1-1 PDFGood LifeNo ratings yet

- Group Project 2 Far620Document8 pagesGroup Project 2 Far620NUR ATHIRAH SUKAIMINo ratings yet

- Unit 12-Question 12-D Sol (2023)Document2 pagesUnit 12-Question 12-D Sol (2023)shirleygebenga020829No ratings yet

- Far210 - Feb2022 SS Q5Document3 pagesFar210 - Feb2022 SS Q5imn njwaaaNo ratings yet

- Accounting GR 11 June 2022 Marking GuidelineDocument5 pagesAccounting GR 11 June 2022 Marking Guidelineamilesithole1709No ratings yet

- Official GR 12 Accounting P1 Eng MemoDocument11 pagesOfficial GR 12 Accounting P1 Eng MemohlayisofilesNo ratings yet

- FAR270 - FEB 2022 SolutionDocument8 pagesFAR270 - FEB 2022 SolutionNur Fatin AmirahNo ratings yet

- Set_1_FA_SSS_FAR210_FEB2022.pdf (1)Document10 pagesSet_1_FA_SSS_FAR210_FEB2022.pdf (1)Rusyda AzizNo ratings yet

- FAC1601 Assignment 4 Solutions First Semester 2022Document17 pagesFAC1601 Assignment 4 Solutions First Semester 2022Nkhangweni Rambuda100% (1)

- Eacc1614 Test 2 Memo 2021 AdjDocument10 pagesEacc1614 Test 2 Memo 2021 AdjshabanguntandoyenkosiNo ratings yet

- Accounting P1 Memo May June 2023 Eng Free StateDocument11 pagesAccounting P1 Memo May June 2023 Eng Free StateSimiNo ratings yet

- EACC1614 Main Exam Memo 2022Document6 pagesEACC1614 Main Exam Memo 2022asandantlumayo77No ratings yet

- August Q1Document3 pagesAugust Q1tengku rilNo ratings yet

- Tuto 6Document6 pagesTuto 6WEI QUAN LEENo ratings yet

- ACC117 - Chapter 4-3 - Tutorial - Solution - Textbook Page 95, 98 - 99Document6 pagesACC117 - Chapter 4-3 - Tutorial - Solution - Textbook Page 95, 98 - 99taerrybombNo ratings yet

- Past Exam QuestionDocument3 pagesPast Exam QuestionYến Hoàng HảiNo ratings yet

- Far570 Group ProjectDocument4 pagesFar570 Group ProjectN FrzanahNo ratings yet

- Accounting Worksheet 2 Answer SheetDocument31 pagesAccounting Worksheet 2 Answer Sheetzeldazitha87No ratings yet

- Group Project 2 - Published Account DEC2019 FAR270 - SSDocument6 pagesGroup Project 2 - Published Account DEC2019 FAR270 - SSHaru BiruNo ratings yet

- FAR210 Aug 2023 S PDFDocument10 pagesFAR210 Aug 2023 S PDFNUR AYUNI BALQISH AHMAD MULIADINo ratings yet

- JAN 2024 (1)Document3 pagesJAN 2024 (1)Nur Alya DamiaNo ratings yet

- LC032GLP000EVDocument16 pagesLC032GLP000EVrianrocheNo ratings yet

- Sam's Introductory Accounting AnswersDocument1 pageSam's Introductory Accounting AnswersSamuelNo ratings yet

- Unit 12-Question 12-C Sol (2023)Document2 pagesUnit 12-Question 12-C Sol (2023)shirleygebenga020829No ratings yet

- Bac 3 Review QNSDocument16 pagesBac 3 Review QNSsaidkhatib368No ratings yet

- Income Statements For The November: @Chapter7AnalyslngandlnterpretlngflnanclalstatementsDocument1 pageIncome Statements For The November: @Chapter7AnalyslngandlnterpretlngflnanclalstatementsAik Luen LimNo ratings yet

- FAR270_AC1104EDocument17 pagesFAR270_AC1104ENur SaidatulNo ratings yet

- Taxation Solution 2018 SeptemberDocument9 pagesTaxation Solution 2018 SeptemberIffah NasuhaaNo ratings yet

- RBGH Financials 31 December 2020 Colour 18.03.2021 3 Full PageseddDocument3 pagesRBGH Financials 31 December 2020 Colour 18.03.2021 3 Full PageseddFuaad DodooNo ratings yet

- Assignment 1 (Part 2)Document10 pagesAssignment 1 (Part 2)Sanghya MahendranNo ratings yet

- Ans Jan 2018 Far410Document8 pagesAns Jan 2018 Far4102022478048No ratings yet

- Profit & Loss Accounts: Wing Chair GirogioDocument3 pagesProfit & Loss Accounts: Wing Chair Girogiofarsi786No ratings yet

- Annual-Report-FML-30-June-2020-23 Vol 2Document1 pageAnnual-Report-FML-30-June-2020-23 Vol 2Bluish FlameNo ratings yet

- PYQ June 2018Document4 pagesPYQ June 2018Nur Amira NadiaNo ratings yet

- 11 ACC CH 6.11 To 6.16 MemosDocument19 pages11 ACC CH 6.11 To 6.16 Memosora mashaNo ratings yet

- Accountancy & Auditing-IDocument4 pagesAccountancy & Auditing-Izaman virkNo ratings yet

- Fin Acc n6 Int. Exam 2017 s2 MGDocument7 pagesFin Acc n6 Int. Exam 2017 s2 MGprofessional accountantsNo ratings yet

- The Institute of Chartered Accountants of Bangladesh: Sample Question Paper Certificate Level-AccountingDocument8 pagesThe Institute of Chartered Accountants of Bangladesh: Sample Question Paper Certificate Level-AccountingArif UddinNo ratings yet

- FAC1602 Exam PackDocument25 pagesFAC1602 Exam PackNthabeza De Ntha MogaleNo ratings yet

- Ans Cabi - 2012 - FaDocument19 pagesAns Cabi - 2012 - FaJahanzaib ButtNo ratings yet

- Yolanda Reality Work Sheet For The Month Ended April 2020Document2 pagesYolanda Reality Work Sheet For The Month Ended April 2020Hannah DimalibotNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Equity Valuation: Models from Leading Investment BanksFrom EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNo ratings yet

- Goto 1702966919Document5 pagesGoto 1702966919Anonymous XoUqrqyuNo ratings yet

- Chapter 10Document18 pagesChapter 10Yousef WardatNo ratings yet

- Annexure 1Document2 pagesAnnexure 1National HeraldNo ratings yet

- Financial Accounting Marathon PartnershipDocument37 pagesFinancial Accounting Marathon PartnershipPriyvrat MamgainNo ratings yet

- Assemblies of God Building Projects Stand 3435 Unit 3 Kudube 0400Document2 pagesAssemblies of God Building Projects Stand 3435 Unit 3 Kudube 0400Mandlakayise MabizelaNo ratings yet

- Issue and Redemption of Shares 2Document3 pagesIssue and Redemption of Shares 2Prince TshepoNo ratings yet

- CH 14 FMDocument2 pagesCH 14 FMAsep KurniaNo ratings yet

- CH 18 IFM10 CH 19 Test BankDocument12 pagesCH 18 IFM10 CH 19 Test Bankajones1219100% (1)

- Befa Question BankDocument9 pagesBefa Question Bank20bd1a6655No ratings yet

- Intermediate Accounting I - Notes (9.13.2022)Document18 pagesIntermediate Accounting I - Notes (9.13.2022)Mainit, Shiela Mae, S.No ratings yet

- Final AccountsDocument18 pagesFinal AccountsAkella kavya SharmaNo ratings yet

- Chap 14Document27 pagesChap 14Thu YếnNo ratings yet

- Untitled 7Document2 pagesUntitled 7subhash221103No ratings yet

- Intercompany DividendsDocument6 pagesIntercompany DividendsClauie BarsNo ratings yet

- CFA一级基础段衍生 Tom 标准版Document113 pagesCFA一级基础段衍生 Tom 标准版Evelyn YangNo ratings yet

- Problem 1 - The Accounts and Their Balances in The Ledger of Generic Pharma On December 31Document2 pagesProblem 1 - The Accounts and Their Balances in The Ledger of Generic Pharma On December 31Pepegon SalinasNo ratings yet

- Business License Single Page With Group 171393758498Document1 pageBusiness License Single Page With Group 171393758498Affan AhmadNo ratings yet

- Ratios of BajajDocument2 pagesRatios of BajajSunil KumarNo ratings yet

- Chapter 2: Statement of Financial Position Statement of Financial PositionDocument16 pagesChapter 2: Statement of Financial Position Statement of Financial PositionDaniella Mae ElipNo ratings yet

- Caf 5 Far1 Spring 2019xsxDocument5 pagesCaf 5 Far1 Spring 2019xsxMustafa ZaheerNo ratings yet

- Investment in AssociateDocument2 pagesInvestment in AssociateChiChi0% (1)

- Cover PageDocument6 pagesCover PageJobair TanvirNo ratings yet

- University of The Cordilleras College of Accountancy Quiz On Partnership Formation 1Document6 pagesUniversity of The Cordilleras College of Accountancy Quiz On Partnership Formation 1Ian Ranilopa100% (1)

- AQR Momentum Index MethodologyDocument8 pagesAQR Momentum Index MethodologyHo Kai LunNo ratings yet

- Capital BudgetingDocument26 pagesCapital BudgetingB112NITESH KUMAR SAHUNo ratings yet

- Job Order CostingDocument39 pagesJob Order CostingCharisse Ahnne Toslolado100% (1)

- Solutions To Problems: Smart/Gitman/Joehnk, Fundamentals of Investing, 12/e Chapter 3Document2 pagesSolutions To Problems: Smart/Gitman/Joehnk, Fundamentals of Investing, 12/e Chapter 3Rio Yow-yow Lansang CastroNo ratings yet

- Ch13 Wiley Plus Wk3Document58 pagesCh13 Wiley Plus Wk3Prakash VaidhyanathanNo ratings yet

- Sample Case StudiesDocument29 pagesSample Case StudiesAbc SNo ratings yet

- 11 EM ACC PUBLIC MLM 23-24 - PagenumberDocument11 pages11 EM ACC PUBLIC MLM 23-24 - Pagenumberkms195kds2007No ratings yet