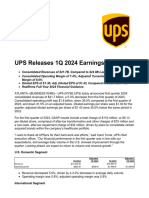

Q1-2024_Earnings-Deck

Q1-2024_Earnings-Deck

You might also like

- Sanction Letter A2301300139 1Document1 pageSanction Letter A2301300139 1Mohammed Masood50% (2)

- Total Quality Management Assignment Section: Submitted To: Sir Mohsin RashidDocument12 pagesTotal Quality Management Assignment Section: Submitted To: Sir Mohsin RashidPari Aslam WNo ratings yet

- Final Mandatory Learning LessonsDocument36 pagesFinal Mandatory Learning LessonsVallela Jagan Mohan0% (1)

- Accor Hotels - Case 2Document7 pagesAccor Hotels - Case 2Brandon CagayanNo ratings yet

- Sample Investment Term SheetDocument10 pagesSample Investment Term SheetBrrrody100% (2)

- Q4 2022 Investor Presentation FinalDocument18 pagesQ4 2022 Investor Presentation Finalmagdalena floresNo ratings yet

- Albermarle November 2022 Investor Presentation v04Document39 pagesAlbermarle November 2022 Investor Presentation v04Guillaume De SouzaNo ratings yet

- Uber Q4 23 Earnings Supplemental DataDocument28 pagesUber Q4 23 Earnings Supplemental Datadivbrown0No ratings yet

- Global Lottery Strengthening Industy Leadership With Accelerated Recurring Revenue Growth OutlookDocument21 pagesGlobal Lottery Strengthening Industy Leadership With Accelerated Recurring Revenue Growth Outlookadityakumar8960860No ratings yet

- Global Trade and Receivables Finance PresentationDocument20 pagesGlobal Trade and Receivables Finance PresentationTarun SinghNo ratings yet

- CRM Q2 FY23 Earnings PresentationDocument18 pagesCRM Q2 FY23 Earnings Presentationstan LeeNo ratings yet

- Stem InvestorPresentation 2022 Sept VFDocument27 pagesStem InvestorPresentation 2022 Sept VFDE ReddyNo ratings yet

- Second Quarter 2010 Earnings PresentationDocument24 pagesSecond Quarter 2010 Earnings PresentationNeha LoyaNo ratings yet

- Q4 2022 Earnings PresentationDocument21 pagesQ4 2022 Earnings PresentationCesar AugustoNo ratings yet

- Huntington National Bank 2021 Q3 Earnings ReviewDocument40 pagesHuntington National Bank 2021 Q3 Earnings ReviewUrderglewerNo ratings yet

- 2cjvoeqflu7sw8 Yid1o4pb 6cvddrcbdeqj Kz6clyDocument24 pages2cjvoeqflu7sw8 Yid1o4pb 6cvddrcbdeqj Kz6clySuzlonNo ratings yet

- Q1 FY22 Earnings Presentation V.finalDocument36 pagesQ1 FY22 Earnings Presentation V.finalnurshafinaawgadi06No ratings yet

- Enphase Investor Day 11 - 16 - 2021 - LowresDocument68 pagesEnphase Investor Day 11 - 16 - 2021 - LowresBruno CarvalheiroNo ratings yet

- Aviva PLC HY2021 Results PresentationDocument49 pagesAviva PLC HY2021 Results PresentationSimonSaysNo ratings yet

- GPC Investor Presentation November 2022Document31 pagesGPC Investor Presentation November 2022lucio ReisNo ratings yet

- GPC Investor Prestentation August-2022Document31 pagesGPC Investor Prestentation August-2022ЛяховецДмитрийNo ratings yet

- Capital Markets Day 2024 vFINALDocument119 pagesCapital Markets Day 2024 vFINALKaan MENEKŞEDAĞNo ratings yet

- Danaher Overview 2023Document21 pagesDanaher Overview 2023Ramesh RNo ratings yet

- StoneDocument21 pagesStoneandre.torresNo ratings yet

- Q3'21 Earnings Call PresentationDocument24 pagesQ3'21 Earnings Call Presentationsl7789No ratings yet

- q1 2020 Earnings Website PresentationDocument15 pagesq1 2020 Earnings Website PresentationTitoNo ratings yet

- Q1 2021 Earnings Call: Strategic Priorities and Financial ResultsDocument35 pagesQ1 2021 Earnings Call: Strategic Priorities and Financial ResultsMohit SinghNo ratings yet

- Q1 2024 Presentation FINALDocument6 pagesQ1 2024 Presentation FINALpeterkahwai5No ratings yet

- VF The North Face-Q219 Earnings Slides - FinalDocument39 pagesVF The North Face-Q219 Earnings Slides - FinaljojoNo ratings yet

- Informatica Investor Presentation October 2021Document52 pagesInformatica Investor Presentation October 2021Praveen LankapothuNo ratings yet

- Confluent Earnings Presentation q4 2023Document44 pagesConfluent Earnings Presentation q4 2023jbsNo ratings yet

- FY 2023 Presentation SlidesDocument58 pagesFY 2023 Presentation SlidesJonathan KinnearNo ratings yet

- FINAL Semiconductor Co-Investment Program Announcement DeckDocument11 pagesFINAL Semiconductor Co-Investment Program Announcement DeckTyler YanNo ratings yet

- NVHI Q1 2023 Earnings PresentationDocument26 pagesNVHI Q1 2023 Earnings PresentationSimona IstrateNo ratings yet

- Rategain 02022024141600 RG Ip Q3 Fy 2023 24Document27 pagesRategain 02022024141600 RG Ip Q3 Fy 2023 24Kshitij GoelNo ratings yet

- Paytm Q3 FY 2024-Earnings-Presentation INRDocument15 pagesPaytm Q3 FY 2024-Earnings-Presentation INRRishi SarafNo ratings yet

- PRMW Primo Water June 2018Document31 pagesPRMW Primo Water June 2018Ala BasterNo ratings yet

- Bird GlobalDocument30 pagesBird GlobalrzrNo ratings yet

- UPS Releases 1Q 2024 Earnings: U.S. Domestic SegmentDocument8 pagesUPS Releases 1Q 2024 Earnings: U.S. Domestic Segmentrborgesdossantos37No ratings yet

- Financial Update Q2 FY20: Nyse: CRM @salesforce - IrDocument33 pagesFinancial Update Q2 FY20: Nyse: CRM @salesforce - IrMika DeverinNo ratings yet

- Zag 1Document23 pagesZag 1jagpreet.singhNo ratings yet

- First Quarter 2022 Earnings Presentation: Thursday, May 5, 2022Document27 pagesFirst Quarter 2022 Earnings Presentation: Thursday, May 5, 2022Ion iliescy IulieNo ratings yet

- Siemens Business Fact SheetsDocument7 pagesSiemens Business Fact SheetsahadjayaNo ratings yet

- Innovative, Affordable Power & Energy Solutions: August 2018Document17 pagesInnovative, Affordable Power & Energy Solutions: August 2018Jonathan VictorNo ratings yet

- 2023-02-02 JuliusBaer FYR2022 Presentation En-2Document46 pages2023-02-02 JuliusBaer FYR2022 Presentation En-25vzz2swtzfNo ratings yet

- Trimble Q1 24 Earnings PresentationDocument22 pagesTrimble Q1 24 Earnings PresentationNitin JainNo ratings yet

- LYONDELLBASELL INDU-CL A Company Presentation 2023428 ST000000003009971585Document16 pagesLYONDELLBASELL INDU-CL A Company Presentation 2023428 ST000000003009971585Naveen TiggaNo ratings yet

- Q4'2022 Earnings Deck - Final PDFDocument18 pagesQ4'2022 Earnings Deck - Final PDFLiviuNo ratings yet

- Thanking You.: Sub: Subex Limited "The Company"-Investor Presentation On February 10, 2020Document33 pagesThanking You.: Sub: Subex Limited "The Company"-Investor Presentation On February 10, 2020Awadhesh Kumar KureelNo ratings yet

- Q4 FY21 Snowflake Investor PresentationDocument26 pagesQ4 FY21 Snowflake Investor Presentationmaathu123No ratings yet

- Noc Q4 2015Document13 pagesNoc Q4 2015vedran1980No ratings yet

- Second Quarter 2020 Earnings: July 31, 2020Document21 pagesSecond Quarter 2020 Earnings: July 31, 2020manojkp33No ratings yet

- 1Q 2024 Analyst Slide Deck - Final 1Document28 pages1Q 2024 Analyst Slide Deck - Final 1stahp03No ratings yet

- 4Q2022 ResultsPresentation 1mar2023 FinalDocument14 pages4Q2022 ResultsPresentation 1mar2023 FinalCharlie CalitrokeNo ratings yet

- Q3-2021 Earnings-Supplemental 11.04.21 FINALDocument28 pagesQ3-2021 Earnings-Supplemental 11.04.21 FINALTay YisiongNo ratings yet

- FISCAL 2021 Q2 Earnings: NOVEMBER 5, 2020Document25 pagesFISCAL 2021 Q2 Earnings: NOVEMBER 5, 2020sl7789No ratings yet

- DXC Q1FY24 Earnings DeckDocument47 pagesDXC Q1FY24 Earnings Decky.belausavaNo ratings yet

- Ferguson Virtual Investor Day 2022 PresentationDocument56 pagesFerguson Virtual Investor Day 2022 PresentationEric BoroianNo ratings yet

- Strategy Presentation 2015 Results Vfinal 05.25.2016Document52 pagesStrategy Presentation 2015 Results Vfinal 05.25.2016masterjugasan6974No ratings yet

- 2019 North America Investor Tour PresentationsDocument84 pages2019 North America Investor Tour PresentationsNoshan OneitoNo ratings yet

- F5 Networks Inc. Volterra Inc. - M&A CallDocument30 pagesF5 Networks Inc. Volterra Inc. - M&A CallpriyanshuNo ratings yet

- 1HFY24 Results PresentationDocument32 pages1HFY24 Results PresentationRexNo ratings yet

- Amgen 2019 JP Morgan PresentationDocument32 pagesAmgen 2019 JP Morgan PresentationmedtechyNo ratings yet

- COTY Jun 2018Document10 pagesCOTY Jun 2018Ala BasterNo ratings yet

- Miscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryFrom EverandMiscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- FMP100 1284Document3 pagesFMP100 1284mihai84pNo ratings yet

- Dt e17l4 e21l4 Bedienungsanleitung.pdfDocument229 pagesDt e17l4 e21l4 Bedienungsanleitung.pdfmihai84pNo ratings yet

- CISZGH20240708-02Document2 pagesCISZGH20240708-02mihai84pNo ratings yet

- Bloc Orb - IdwDocument1 pageBloc Orb - Idwmihai84pNo ratings yet

- HARSCO CORP 10-K (Annual Reports) 2009-02-24Document205 pagesHARSCO CORP 10-K (Annual Reports) 2009-02-24http://secwatch.comNo ratings yet

- Kelway Invoice4Document3 pagesKelway Invoice4LibertyDreams'mdNo ratings yet

- Process Costing: Managerial AccountingDocument56 pagesProcess Costing: Managerial AccountingSpidey ModeNo ratings yet

- Hinrich Foundation NUS - Semiconductors at The Heart of The US China Tech War PDFDocument90 pagesHinrich Foundation NUS - Semiconductors at The Heart of The US China Tech War PDFMichaela PlatzerNo ratings yet

- Intern Report - BRAC BankDocument124 pagesIntern Report - BRAC Bankashik0526No ratings yet

- Handling Prolongation and Disruption ClaimsDocument0 pagesHandling Prolongation and Disruption ClaimsAnonymous pGodzH4xL100% (1)

- Appropriation Ordinance n0.1 2021Document7 pagesAppropriation Ordinance n0.1 2021Melody Frac ZapateroNo ratings yet

- ANG en Construction Business 23022006Document94 pagesANG en Construction Business 23022006Cris NeculaNo ratings yet

- Vinculum Oracle Gold PartnerDocument1 pageVinculum Oracle Gold PartnerSiddhartha TripathiNo ratings yet

- Standard Reports in SAP Business One (A)Document4 pagesStandard Reports in SAP Business One (A)sap becerraNo ratings yet

- FFM Group 3 PresentationDocument5 pagesFFM Group 3 Presentationlohithagowda122001No ratings yet

- Tech MahindraDocument4 pagesTech Mahindrayoha priyaNo ratings yet

- TDSWorkings AspxDocument2 pagesTDSWorkings Aspxchandruv29eNo ratings yet

- Causes of Rural IndebtednessDocument8 pagesCauses of Rural IndebtednessAditi DeyNo ratings yet

- Introduction To Financial Planning 2017contentsDocument8 pagesIntroduction To Financial Planning 2017contentsABC 123No ratings yet

- Rainbow Industries 1Document22 pagesRainbow Industries 1wajahat HassanNo ratings yet

- Exam Audit ProblemDocument5 pagesExam Audit ProblemNhel AlvaroNo ratings yet

- 2019 EngDocument426 pages2019 EngRizki AbdullahNo ratings yet

- Gender and LaborDocument9 pagesGender and LaborKristine San Luis PotencianoNo ratings yet

- First Crisis Then Catastrophe - Embargoed 0001 GMT 12 April 2022Document31 pagesFirst Crisis Then Catastrophe - Embargoed 0001 GMT 12 April 2022Pedro Marquez RosalesNo ratings yet

- Circular BBA Sem-1 Major MinorDocument2 pagesCircular BBA Sem-1 Major MinoranishNo ratings yet

- Earnings Update Q4FY15 (Company Update)Document45 pagesEarnings Update Q4FY15 (Company Update)Shyam SunderNo ratings yet

- Prosenjit Bhowmik Internship ReportDocument63 pagesProsenjit Bhowmik Internship ReportProsenjit BhowmikNo ratings yet

- PART1 - Entrepreneurs-The Driving Force Behind Small BusinessesDocument7 pagesPART1 - Entrepreneurs-The Driving Force Behind Small BusinessesKim John IlaganNo ratings yet

- VEERADocument28 pagesVEERAVeera Mani SNo ratings yet

Download as pdf or txt

You might also like

- Sanction Letter A2301300139 1Document1 pageSanction Letter A2301300139 1Mohammed Masood50% (2)

- Total Quality Management Assignment Section: Submitted To: Sir Mohsin RashidDocument12 pagesTotal Quality Management Assignment Section: Submitted To: Sir Mohsin RashidPari Aslam WNo ratings yet

- Final Mandatory Learning LessonsDocument36 pagesFinal Mandatory Learning LessonsVallela Jagan Mohan0% (1)

- Accor Hotels - Case 2Document7 pagesAccor Hotels - Case 2Brandon CagayanNo ratings yet

- Sample Investment Term SheetDocument10 pagesSample Investment Term SheetBrrrody100% (2)

- Q4 2022 Investor Presentation FinalDocument18 pagesQ4 2022 Investor Presentation Finalmagdalena floresNo ratings yet

- Albermarle November 2022 Investor Presentation v04Document39 pagesAlbermarle November 2022 Investor Presentation v04Guillaume De SouzaNo ratings yet

- Uber Q4 23 Earnings Supplemental DataDocument28 pagesUber Q4 23 Earnings Supplemental Datadivbrown0No ratings yet

- Global Lottery Strengthening Industy Leadership With Accelerated Recurring Revenue Growth OutlookDocument21 pagesGlobal Lottery Strengthening Industy Leadership With Accelerated Recurring Revenue Growth Outlookadityakumar8960860No ratings yet

- Global Trade and Receivables Finance PresentationDocument20 pagesGlobal Trade and Receivables Finance PresentationTarun SinghNo ratings yet

- CRM Q2 FY23 Earnings PresentationDocument18 pagesCRM Q2 FY23 Earnings Presentationstan LeeNo ratings yet

- Stem InvestorPresentation 2022 Sept VFDocument27 pagesStem InvestorPresentation 2022 Sept VFDE ReddyNo ratings yet

- Second Quarter 2010 Earnings PresentationDocument24 pagesSecond Quarter 2010 Earnings PresentationNeha LoyaNo ratings yet

- Q4 2022 Earnings PresentationDocument21 pagesQ4 2022 Earnings PresentationCesar AugustoNo ratings yet

- Huntington National Bank 2021 Q3 Earnings ReviewDocument40 pagesHuntington National Bank 2021 Q3 Earnings ReviewUrderglewerNo ratings yet

- 2cjvoeqflu7sw8 Yid1o4pb 6cvddrcbdeqj Kz6clyDocument24 pages2cjvoeqflu7sw8 Yid1o4pb 6cvddrcbdeqj Kz6clySuzlonNo ratings yet

- Q1 FY22 Earnings Presentation V.finalDocument36 pagesQ1 FY22 Earnings Presentation V.finalnurshafinaawgadi06No ratings yet

- Enphase Investor Day 11 - 16 - 2021 - LowresDocument68 pagesEnphase Investor Day 11 - 16 - 2021 - LowresBruno CarvalheiroNo ratings yet

- Aviva PLC HY2021 Results PresentationDocument49 pagesAviva PLC HY2021 Results PresentationSimonSaysNo ratings yet

- GPC Investor Presentation November 2022Document31 pagesGPC Investor Presentation November 2022lucio ReisNo ratings yet

- GPC Investor Prestentation August-2022Document31 pagesGPC Investor Prestentation August-2022ЛяховецДмитрийNo ratings yet

- Capital Markets Day 2024 vFINALDocument119 pagesCapital Markets Day 2024 vFINALKaan MENEKŞEDAĞNo ratings yet

- Danaher Overview 2023Document21 pagesDanaher Overview 2023Ramesh RNo ratings yet

- StoneDocument21 pagesStoneandre.torresNo ratings yet

- Q3'21 Earnings Call PresentationDocument24 pagesQ3'21 Earnings Call Presentationsl7789No ratings yet

- q1 2020 Earnings Website PresentationDocument15 pagesq1 2020 Earnings Website PresentationTitoNo ratings yet

- Q1 2021 Earnings Call: Strategic Priorities and Financial ResultsDocument35 pagesQ1 2021 Earnings Call: Strategic Priorities and Financial ResultsMohit SinghNo ratings yet

- Q1 2024 Presentation FINALDocument6 pagesQ1 2024 Presentation FINALpeterkahwai5No ratings yet

- VF The North Face-Q219 Earnings Slides - FinalDocument39 pagesVF The North Face-Q219 Earnings Slides - FinaljojoNo ratings yet

- Informatica Investor Presentation October 2021Document52 pagesInformatica Investor Presentation October 2021Praveen LankapothuNo ratings yet

- Confluent Earnings Presentation q4 2023Document44 pagesConfluent Earnings Presentation q4 2023jbsNo ratings yet

- FY 2023 Presentation SlidesDocument58 pagesFY 2023 Presentation SlidesJonathan KinnearNo ratings yet

- FINAL Semiconductor Co-Investment Program Announcement DeckDocument11 pagesFINAL Semiconductor Co-Investment Program Announcement DeckTyler YanNo ratings yet

- NVHI Q1 2023 Earnings PresentationDocument26 pagesNVHI Q1 2023 Earnings PresentationSimona IstrateNo ratings yet

- Rategain 02022024141600 RG Ip Q3 Fy 2023 24Document27 pagesRategain 02022024141600 RG Ip Q3 Fy 2023 24Kshitij GoelNo ratings yet

- Paytm Q3 FY 2024-Earnings-Presentation INRDocument15 pagesPaytm Q3 FY 2024-Earnings-Presentation INRRishi SarafNo ratings yet

- PRMW Primo Water June 2018Document31 pagesPRMW Primo Water June 2018Ala BasterNo ratings yet

- Bird GlobalDocument30 pagesBird GlobalrzrNo ratings yet

- UPS Releases 1Q 2024 Earnings: U.S. Domestic SegmentDocument8 pagesUPS Releases 1Q 2024 Earnings: U.S. Domestic Segmentrborgesdossantos37No ratings yet

- Financial Update Q2 FY20: Nyse: CRM @salesforce - IrDocument33 pagesFinancial Update Q2 FY20: Nyse: CRM @salesforce - IrMika DeverinNo ratings yet

- Zag 1Document23 pagesZag 1jagpreet.singhNo ratings yet

- First Quarter 2022 Earnings Presentation: Thursday, May 5, 2022Document27 pagesFirst Quarter 2022 Earnings Presentation: Thursday, May 5, 2022Ion iliescy IulieNo ratings yet

- Siemens Business Fact SheetsDocument7 pagesSiemens Business Fact SheetsahadjayaNo ratings yet

- Innovative, Affordable Power & Energy Solutions: August 2018Document17 pagesInnovative, Affordable Power & Energy Solutions: August 2018Jonathan VictorNo ratings yet

- 2023-02-02 JuliusBaer FYR2022 Presentation En-2Document46 pages2023-02-02 JuliusBaer FYR2022 Presentation En-25vzz2swtzfNo ratings yet

- Trimble Q1 24 Earnings PresentationDocument22 pagesTrimble Q1 24 Earnings PresentationNitin JainNo ratings yet

- LYONDELLBASELL INDU-CL A Company Presentation 2023428 ST000000003009971585Document16 pagesLYONDELLBASELL INDU-CL A Company Presentation 2023428 ST000000003009971585Naveen TiggaNo ratings yet

- Q4'2022 Earnings Deck - Final PDFDocument18 pagesQ4'2022 Earnings Deck - Final PDFLiviuNo ratings yet

- Thanking You.: Sub: Subex Limited "The Company"-Investor Presentation On February 10, 2020Document33 pagesThanking You.: Sub: Subex Limited "The Company"-Investor Presentation On February 10, 2020Awadhesh Kumar KureelNo ratings yet

- Q4 FY21 Snowflake Investor PresentationDocument26 pagesQ4 FY21 Snowflake Investor Presentationmaathu123No ratings yet

- Noc Q4 2015Document13 pagesNoc Q4 2015vedran1980No ratings yet

- Second Quarter 2020 Earnings: July 31, 2020Document21 pagesSecond Quarter 2020 Earnings: July 31, 2020manojkp33No ratings yet

- 1Q 2024 Analyst Slide Deck - Final 1Document28 pages1Q 2024 Analyst Slide Deck - Final 1stahp03No ratings yet

- 4Q2022 ResultsPresentation 1mar2023 FinalDocument14 pages4Q2022 ResultsPresentation 1mar2023 FinalCharlie CalitrokeNo ratings yet

- Q3-2021 Earnings-Supplemental 11.04.21 FINALDocument28 pagesQ3-2021 Earnings-Supplemental 11.04.21 FINALTay YisiongNo ratings yet

- FISCAL 2021 Q2 Earnings: NOVEMBER 5, 2020Document25 pagesFISCAL 2021 Q2 Earnings: NOVEMBER 5, 2020sl7789No ratings yet

- DXC Q1FY24 Earnings DeckDocument47 pagesDXC Q1FY24 Earnings Decky.belausavaNo ratings yet

- Ferguson Virtual Investor Day 2022 PresentationDocument56 pagesFerguson Virtual Investor Day 2022 PresentationEric BoroianNo ratings yet

- Strategy Presentation 2015 Results Vfinal 05.25.2016Document52 pagesStrategy Presentation 2015 Results Vfinal 05.25.2016masterjugasan6974No ratings yet

- 2019 North America Investor Tour PresentationsDocument84 pages2019 North America Investor Tour PresentationsNoshan OneitoNo ratings yet

- F5 Networks Inc. Volterra Inc. - M&A CallDocument30 pagesF5 Networks Inc. Volterra Inc. - M&A CallpriyanshuNo ratings yet

- 1HFY24 Results PresentationDocument32 pages1HFY24 Results PresentationRexNo ratings yet

- Amgen 2019 JP Morgan PresentationDocument32 pagesAmgen 2019 JP Morgan PresentationmedtechyNo ratings yet

- COTY Jun 2018Document10 pagesCOTY Jun 2018Ala BasterNo ratings yet

- Miscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryFrom EverandMiscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- FMP100 1284Document3 pagesFMP100 1284mihai84pNo ratings yet

- Dt e17l4 e21l4 Bedienungsanleitung.pdfDocument229 pagesDt e17l4 e21l4 Bedienungsanleitung.pdfmihai84pNo ratings yet

- CISZGH20240708-02Document2 pagesCISZGH20240708-02mihai84pNo ratings yet

- Bloc Orb - IdwDocument1 pageBloc Orb - Idwmihai84pNo ratings yet

- HARSCO CORP 10-K (Annual Reports) 2009-02-24Document205 pagesHARSCO CORP 10-K (Annual Reports) 2009-02-24http://secwatch.comNo ratings yet

- Kelway Invoice4Document3 pagesKelway Invoice4LibertyDreams'mdNo ratings yet

- Process Costing: Managerial AccountingDocument56 pagesProcess Costing: Managerial AccountingSpidey ModeNo ratings yet

- Hinrich Foundation NUS - Semiconductors at The Heart of The US China Tech War PDFDocument90 pagesHinrich Foundation NUS - Semiconductors at The Heart of The US China Tech War PDFMichaela PlatzerNo ratings yet

- Intern Report - BRAC BankDocument124 pagesIntern Report - BRAC Bankashik0526No ratings yet

- Handling Prolongation and Disruption ClaimsDocument0 pagesHandling Prolongation and Disruption ClaimsAnonymous pGodzH4xL100% (1)

- Appropriation Ordinance n0.1 2021Document7 pagesAppropriation Ordinance n0.1 2021Melody Frac ZapateroNo ratings yet

- ANG en Construction Business 23022006Document94 pagesANG en Construction Business 23022006Cris NeculaNo ratings yet

- Vinculum Oracle Gold PartnerDocument1 pageVinculum Oracle Gold PartnerSiddhartha TripathiNo ratings yet

- Standard Reports in SAP Business One (A)Document4 pagesStandard Reports in SAP Business One (A)sap becerraNo ratings yet

- FFM Group 3 PresentationDocument5 pagesFFM Group 3 Presentationlohithagowda122001No ratings yet

- Tech MahindraDocument4 pagesTech Mahindrayoha priyaNo ratings yet

- TDSWorkings AspxDocument2 pagesTDSWorkings Aspxchandruv29eNo ratings yet

- Causes of Rural IndebtednessDocument8 pagesCauses of Rural IndebtednessAditi DeyNo ratings yet

- Introduction To Financial Planning 2017contentsDocument8 pagesIntroduction To Financial Planning 2017contentsABC 123No ratings yet

- Rainbow Industries 1Document22 pagesRainbow Industries 1wajahat HassanNo ratings yet

- Exam Audit ProblemDocument5 pagesExam Audit ProblemNhel AlvaroNo ratings yet

- 2019 EngDocument426 pages2019 EngRizki AbdullahNo ratings yet

- Gender and LaborDocument9 pagesGender and LaborKristine San Luis PotencianoNo ratings yet

- First Crisis Then Catastrophe - Embargoed 0001 GMT 12 April 2022Document31 pagesFirst Crisis Then Catastrophe - Embargoed 0001 GMT 12 April 2022Pedro Marquez RosalesNo ratings yet

- Circular BBA Sem-1 Major MinorDocument2 pagesCircular BBA Sem-1 Major MinoranishNo ratings yet

- Earnings Update Q4FY15 (Company Update)Document45 pagesEarnings Update Q4FY15 (Company Update)Shyam SunderNo ratings yet

- Prosenjit Bhowmik Internship ReportDocument63 pagesProsenjit Bhowmik Internship ReportProsenjit BhowmikNo ratings yet

- PART1 - Entrepreneurs-The Driving Force Behind Small BusinessesDocument7 pagesPART1 - Entrepreneurs-The Driving Force Behind Small BusinessesKim John IlaganNo ratings yet

- VEERADocument28 pagesVEERAVeera Mani SNo ratings yet