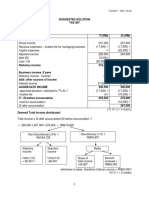

SOLUTION JUN 2018

SOLUTION JUN 2018

You might also like

- FAR210 - Feb 2023 - SSDocument11 pagesFAR210 - Feb 2023 - SSfarisha aliahNo ratings yet

- Schaum's Outline of Principles of Accounting I, Fifth EditionFrom EverandSchaum's Outline of Principles of Accounting I, Fifth EditionRating: 5 out of 5 stars5/5 (3)

- Far460 - Set 1 - Feb 2021 - Suggested SolutionsDocument8 pagesFar460 - Set 1 - Feb 2021 - Suggested SolutionsRuzaikha razaliNo ratings yet

- Chapter-21 (Solved Past Papers of CA Mod CDocument67 pagesChapter-21 (Solved Past Papers of CA Mod CJer Rama100% (4)

- Agency Agreement (Sale of Property) (Variable Commission)Document8 pagesAgency Agreement (Sale of Property) (Variable Commission)Legal Forms67% (3)

- FinAcc3 Chap4Document9 pagesFinAcc3 Chap4Iyah AmranNo ratings yet

- PHS Program of Studies 2020-2021 PDFDocument83 pagesPHS Program of Studies 2020-2021 PDFEshan Singh0% (1)

- Solution June 2019Document8 pagesSolution June 2019faiqahn602No ratings yet

- FAR Revision Answer Scheme Jul 2017Document8 pagesFAR Revision Answer Scheme Jul 2017Nurul Farahdatul Ashikin RamlanNo ratings yet

- Solution Far510 - Jun 2015Document8 pagesSolution Far510 - Jun 2015azila aliasNo ratings yet

- FAR460 - S - June 2018 - StudentsDocument6 pagesFAR460 - S - June 2018 - StudentsRuzaikha razaliNo ratings yet

- Far510 Solution July 2020Document7 pagesFar510 Solution July 2020clumsycaaaaaNo ratings yet

- Solution Far410 Jun 2019Document9 pagesSolution Far410 Jun 2019Nabilah NorddinNo ratings yet

- Solution Dec 2015Document7 pagesSolution Dec 2015anis izzatiNo ratings yet

- SOLUTION DEC 2015Document8 pagesSOLUTION DEC 2015faiqahn602No ratings yet

- Ss Far270 Fa Aug2021.PDFDocument11 pagesSs Far270 Fa Aug2021.PDFRusyda AzizNo ratings yet

- Suggested Answers TAX667 - DEC 2016Document7 pagesSuggested Answers TAX667 - DEC 2016diysNo ratings yet

- Solution Tax667 - Dec 2016Document7 pagesSolution Tax667 - Dec 2016Zahiratul QamarinaNo ratings yet

- Ans June 2018 Far410Document8 pagesAns June 2018 Far4102022478048No ratings yet

- AFS SolutionsDocument19 pagesAFS SolutionsRolivhuwaNo ratings yet

- Solution Far460 - Jun 2019Document7 pagesSolution Far460 - Jun 2019Ruzaikha razaliNo ratings yet

- FAR620 - Jun2023 - S - DR SHUKRIAH SAADDocument9 pagesFAR620 - Jun2023 - S - DR SHUKRIAH SAADNora ArifahsyaNo ratings yet

- FAR610 - TEST 1 - APRIL 2018 Suggested SolutionDocument3 pagesFAR610 - TEST 1 - APRIL 2018 Suggested SolutionAmirul AimanNo ratings yet

- Mark Scheme (Results) January 2016: Pearson Edexcel IAL in Accounting (WAC01) Paper 01Document21 pagesMark Scheme (Results) January 2016: Pearson Edexcel IAL in Accounting (WAC01) Paper 01hisakofelixNo ratings yet

- Solution Jan 2018Document8 pagesSolution Jan 2018anis izzatiNo ratings yet

- Dr-Acc. Depreciation RM 25 Mill CR - Building RM25 MillDocument7 pagesDr-Acc. Depreciation RM 25 Mill CR - Building RM25 MillsyuhadahNo ratings yet

- ASS 1 2021 Part A SolutionDocument4 pagesASS 1 2021 Part A SolutionOdzulaho DemanaNo ratings yet

- Set_1_FA_SSS_FAR210_FEB2022.pdf (1)Document10 pagesSet_1_FA_SSS_FAR210_FEB2022.pdf (1)Rusyda AzizNo ratings yet

- CH 4 Answers 09Document10 pagesCH 4 Answers 09ExequielCamisaCrusperoNo ratings yet

- SS Mar22 PDFDocument8 pagesSS Mar22 PDFuser mrmysteryNo ratings yet

- Fa Far Sesi 2Document28 pagesFa Far Sesi 2hdyhNo ratings yet

- Final Account - Sole Trader - Practice QuestionDocument3 pagesFinal Account - Sole Trader - Practice QuestionMUSTHARI KHANNo ratings yet

- 05 Activity 1 BALADocument3 pages05 Activity 1 BALAPola PolzNo ratings yet

- Solution Dec 2014Document8 pagesSolution Dec 2014anis izzatiNo ratings yet

- Gr11 Acc P1 (English) 2020 Exemplars Possible AnswersDocument14 pagesGr11 Acc P1 (English) 2020 Exemplars Possible AnswersNITANo ratings yet

- Master Budget Illustrationv2Document16 pagesMaster Budget Illustrationv2Rianne NavidadNo ratings yet

- PSPM AA025 - ANSWERS CHAPTER 7 Absorption Costing and Marginal CostingDocument7 pagesPSPM AA025 - ANSWERS CHAPTER 7 Absorption Costing and Marginal CostingDanish AqashahNo ratings yet

- 2017 FRK 100 Year Test 2 Suggested SolutionDocument5 pages2017 FRK 100 Year Test 2 Suggested SolutionFrederick LekalakalaNo ratings yet

- 2013 May A2 MSDocument15 pages2013 May A2 MSGithmii mNo ratings yet

- Individual AssignmentDocument22 pagesIndividual AssignmentEda LimNo ratings yet

- Answers 2014 Vol 3 CH 4 PDFDocument8 pagesAnswers 2014 Vol 3 CH 4 PDFLian Blakely CousinNo ratings yet

- Mark Scheme (Results) June 2011: GCE Accounting (6001) Paper 01Document19 pagesMark Scheme (Results) June 2011: GCE Accounting (6001) Paper 01Fahrin NehaNo ratings yet

- Taxation Solution 2018 SeptemberDocument9 pagesTaxation Solution 2018 SeptemberIffah NasuhaaNo ratings yet

- Unit 12-Question 12-B Sol (2023)Document2 pagesUnit 12-Question 12-B Sol (2023)shirleygebenga020829No ratings yet

- Unit 12-Question 12-C Sol (2023)Document2 pagesUnit 12-Question 12-C Sol (2023)shirleygebenga020829No ratings yet

- Solution - Business Income - Bonda Enterprise Feb2021Document2 pagesSolution - Business Income - Bonda Enterprise Feb2021HANIS IZYAN MAT ISANo ratings yet

- 2013 Jan A2 MSDocument15 pages2013 Jan A2 MSzaainmariyam12No ratings yet

- Tutorial Cash FlowDocument18 pagesTutorial Cash FlowmellNo ratings yet

- 2007 Jan U1 U2 PDFDocument31 pages2007 Jan U1 U2 PDFTharakaaNo ratings yet

- 2022 Grade 11 Provincial Examination Accounting P1 (English) June 2022 Possible AnswersDocument10 pages2022 Grade 11 Provincial Examination Accounting P1 (English) June 2022 Possible AnswersChantelle IsaksNo ratings yet

- JAN 2024 (1)Document3 pagesJAN 2024 (1)Nur Alya DamiaNo ratings yet

- Solutions of Revision Session by AMK Sept 2020 AttemptDocument13 pagesSolutions of Revision Session by AMK Sept 2020 AttemptShehrozSTNo ratings yet

- Fac2601-2013-6 - Answers PDFDocument9 pagesFac2601-2013-6 - Answers PDFcandiceNo ratings yet

- Financial Accounting and Reporting: IFRS - 2015 December MSDocument18 pagesFinancial Accounting and Reporting: IFRS - 2015 December MSMarchella LukitoNo ratings yet

- Financial Accounting and Reporting: IFRS - 2016 June MSDocument17 pagesFinancial Accounting and Reporting: IFRS - 2016 June MSMarchella LukitoNo ratings yet

- Mark Scheme - AccountingDocument23 pagesMark Scheme - AccountingDanielNo ratings yet

- Broadway Bridge Design Workshop PowerpointDocument47 pagesBroadway Bridge Design Workshop PowerpointMark ReinhardtNo ratings yet

- Summary of Bank Niaga'S Case Study A. A Glance of Bank NiagaDocument4 pagesSummary of Bank Niaga'S Case Study A. A Glance of Bank Niagaaldiansyar mugiaNo ratings yet

- Pre-Advanced 1 - Final Written Test - Tipo BDocument5 pagesPre-Advanced 1 - Final Written Test - Tipo BJulia SantosNo ratings yet

- Mcafee Data Loss Prevention Endpoint For Windows 11.0 Update 6 Release NotesDocument5 pagesMcafee Data Loss Prevention Endpoint For Windows 11.0 Update 6 Release NoteselibunNo ratings yet

- Home Economics 2008 PDFDocument37 pagesHome Economics 2008 PDFAndrew ArahaNo ratings yet

- 27.0 - Confined Spaces v3.0 EnglishDocument14 pages27.0 - Confined Spaces v3.0 Englishwaheed0% (1)

- III Sem Eafm Indian Banking System NewDocument1 pageIII Sem Eafm Indian Banking System NewSuryaNo ratings yet

- Annual Report Library Management System 2020-2021Document144 pagesAnnual Report Library Management System 2020-2021ARUNAVA SAMANTANo ratings yet

- The Canterville Ghost and Other Stories: Book KeyDocument4 pagesThe Canterville Ghost and Other Stories: Book KeyDesweet12No ratings yet

- Dekada '70 Reaction PaperDocument1 pageDekada '70 Reaction PaperSaxourie XiaoNo ratings yet

- Principles of Accounting Past Paper 1Document6 pagesPrinciples of Accounting Past Paper 1Muhannad AliNo ratings yet

- Final Advt VS PA-IDocument14 pagesFinal Advt VS PA-IDivyesh HarwaniNo ratings yet

- When Your Spouse Wants A Divorce and You Don't: Kim BowenDocument16 pagesWhen Your Spouse Wants A Divorce and You Don't: Kim Boweninneed1100% (1)

- LESLIE, C. Scientific Racism Reflections On Peer Review, Science and IdeologyDocument22 pagesLESLIE, C. Scientific Racism Reflections On Peer Review, Science and IdeologyÉden RodriguesNo ratings yet

- NTCP AnalysisDocument12 pagesNTCP AnalysisParas KhuranaNo ratings yet

- Lecture 2 - Cost AssignmentDocument10 pagesLecture 2 - Cost AssignmentJaquin0% (1)

- Borrowing Cost & Gov Grants-QUIZDocument3 pagesBorrowing Cost & Gov Grants-QUIZDanah EstilloreNo ratings yet

- Nil EndorsementDocument1 pageNil EndorsementDhawal SharmaNo ratings yet

- CLE 7 Week 3 - Prophets Speak To Us About HolinessDocument5 pagesCLE 7 Week 3 - Prophets Speak To Us About HolinessSrRose Ann ReballosNo ratings yet

- Vendor Selection CriteriaDocument2 pagesVendor Selection CriteriaMohammad Faraz AkhterNo ratings yet

- Produse ROSHEN Cota TVADocument6 pagesProduse ROSHEN Cota TVABadea BogdanNo ratings yet

- How To Design and Conduct A Country Programme Evaluation at UnfpaDocument228 pagesHow To Design and Conduct A Country Programme Evaluation at UnfpaskurgniydNo ratings yet

- ISSO (Class-7) WorksheetDocument17 pagesISSO (Class-7) WorksheetCHITRAKSHI GEHLOTNo ratings yet

- Personality, Attitudes, and Work BehaviorsDocument3 pagesPersonality, Attitudes, and Work BehaviorsNoella ColesioNo ratings yet

- I AM - Week 9 - Jehovah TsidkenuDocument42 pagesI AM - Week 9 - Jehovah TsidkenuHarvest Time Church100% (1)

- Composers in The MoviesDocument382 pagesComposers in The Moviessandranoriega135150% (2)

- 78903567-Garga by GargacharyaDocument55 pages78903567-Garga by GargacharyaGirish BegoorNo ratings yet

- P A V E: Ilot Ircraft EN Ironment Xternal PressuresDocument1 pageP A V E: Ilot Ircraft EN Ironment Xternal PressuresSohailArdeshiriNo ratings yet

Download as pdf or txt

You might also like

- FAR210 - Feb 2023 - SSDocument11 pagesFAR210 - Feb 2023 - SSfarisha aliahNo ratings yet

- Schaum's Outline of Principles of Accounting I, Fifth EditionFrom EverandSchaum's Outline of Principles of Accounting I, Fifth EditionRating: 5 out of 5 stars5/5 (3)

- Far460 - Set 1 - Feb 2021 - Suggested SolutionsDocument8 pagesFar460 - Set 1 - Feb 2021 - Suggested SolutionsRuzaikha razaliNo ratings yet

- Chapter-21 (Solved Past Papers of CA Mod CDocument67 pagesChapter-21 (Solved Past Papers of CA Mod CJer Rama100% (4)

- Agency Agreement (Sale of Property) (Variable Commission)Document8 pagesAgency Agreement (Sale of Property) (Variable Commission)Legal Forms67% (3)

- FinAcc3 Chap4Document9 pagesFinAcc3 Chap4Iyah AmranNo ratings yet

- PHS Program of Studies 2020-2021 PDFDocument83 pagesPHS Program of Studies 2020-2021 PDFEshan Singh0% (1)

- Solution June 2019Document8 pagesSolution June 2019faiqahn602No ratings yet

- FAR Revision Answer Scheme Jul 2017Document8 pagesFAR Revision Answer Scheme Jul 2017Nurul Farahdatul Ashikin RamlanNo ratings yet

- Solution Far510 - Jun 2015Document8 pagesSolution Far510 - Jun 2015azila aliasNo ratings yet

- FAR460 - S - June 2018 - StudentsDocument6 pagesFAR460 - S - June 2018 - StudentsRuzaikha razaliNo ratings yet

- Far510 Solution July 2020Document7 pagesFar510 Solution July 2020clumsycaaaaaNo ratings yet

- Solution Far410 Jun 2019Document9 pagesSolution Far410 Jun 2019Nabilah NorddinNo ratings yet

- Solution Dec 2015Document7 pagesSolution Dec 2015anis izzatiNo ratings yet

- SOLUTION DEC 2015Document8 pagesSOLUTION DEC 2015faiqahn602No ratings yet

- Ss Far270 Fa Aug2021.PDFDocument11 pagesSs Far270 Fa Aug2021.PDFRusyda AzizNo ratings yet

- Suggested Answers TAX667 - DEC 2016Document7 pagesSuggested Answers TAX667 - DEC 2016diysNo ratings yet

- Solution Tax667 - Dec 2016Document7 pagesSolution Tax667 - Dec 2016Zahiratul QamarinaNo ratings yet

- Ans June 2018 Far410Document8 pagesAns June 2018 Far4102022478048No ratings yet

- AFS SolutionsDocument19 pagesAFS SolutionsRolivhuwaNo ratings yet

- Solution Far460 - Jun 2019Document7 pagesSolution Far460 - Jun 2019Ruzaikha razaliNo ratings yet

- FAR620 - Jun2023 - S - DR SHUKRIAH SAADDocument9 pagesFAR620 - Jun2023 - S - DR SHUKRIAH SAADNora ArifahsyaNo ratings yet

- FAR610 - TEST 1 - APRIL 2018 Suggested SolutionDocument3 pagesFAR610 - TEST 1 - APRIL 2018 Suggested SolutionAmirul AimanNo ratings yet

- Mark Scheme (Results) January 2016: Pearson Edexcel IAL in Accounting (WAC01) Paper 01Document21 pagesMark Scheme (Results) January 2016: Pearson Edexcel IAL in Accounting (WAC01) Paper 01hisakofelixNo ratings yet

- Solution Jan 2018Document8 pagesSolution Jan 2018anis izzatiNo ratings yet

- Dr-Acc. Depreciation RM 25 Mill CR - Building RM25 MillDocument7 pagesDr-Acc. Depreciation RM 25 Mill CR - Building RM25 MillsyuhadahNo ratings yet

- ASS 1 2021 Part A SolutionDocument4 pagesASS 1 2021 Part A SolutionOdzulaho DemanaNo ratings yet

- Set_1_FA_SSS_FAR210_FEB2022.pdf (1)Document10 pagesSet_1_FA_SSS_FAR210_FEB2022.pdf (1)Rusyda AzizNo ratings yet

- CH 4 Answers 09Document10 pagesCH 4 Answers 09ExequielCamisaCrusperoNo ratings yet

- SS Mar22 PDFDocument8 pagesSS Mar22 PDFuser mrmysteryNo ratings yet

- Fa Far Sesi 2Document28 pagesFa Far Sesi 2hdyhNo ratings yet

- Final Account - Sole Trader - Practice QuestionDocument3 pagesFinal Account - Sole Trader - Practice QuestionMUSTHARI KHANNo ratings yet

- 05 Activity 1 BALADocument3 pages05 Activity 1 BALAPola PolzNo ratings yet

- Solution Dec 2014Document8 pagesSolution Dec 2014anis izzatiNo ratings yet

- Gr11 Acc P1 (English) 2020 Exemplars Possible AnswersDocument14 pagesGr11 Acc P1 (English) 2020 Exemplars Possible AnswersNITANo ratings yet

- Master Budget Illustrationv2Document16 pagesMaster Budget Illustrationv2Rianne NavidadNo ratings yet

- PSPM AA025 - ANSWERS CHAPTER 7 Absorption Costing and Marginal CostingDocument7 pagesPSPM AA025 - ANSWERS CHAPTER 7 Absorption Costing and Marginal CostingDanish AqashahNo ratings yet

- 2017 FRK 100 Year Test 2 Suggested SolutionDocument5 pages2017 FRK 100 Year Test 2 Suggested SolutionFrederick LekalakalaNo ratings yet

- 2013 May A2 MSDocument15 pages2013 May A2 MSGithmii mNo ratings yet

- Individual AssignmentDocument22 pagesIndividual AssignmentEda LimNo ratings yet

- Answers 2014 Vol 3 CH 4 PDFDocument8 pagesAnswers 2014 Vol 3 CH 4 PDFLian Blakely CousinNo ratings yet

- Mark Scheme (Results) June 2011: GCE Accounting (6001) Paper 01Document19 pagesMark Scheme (Results) June 2011: GCE Accounting (6001) Paper 01Fahrin NehaNo ratings yet

- Taxation Solution 2018 SeptemberDocument9 pagesTaxation Solution 2018 SeptemberIffah NasuhaaNo ratings yet

- Unit 12-Question 12-B Sol (2023)Document2 pagesUnit 12-Question 12-B Sol (2023)shirleygebenga020829No ratings yet

- Unit 12-Question 12-C Sol (2023)Document2 pagesUnit 12-Question 12-C Sol (2023)shirleygebenga020829No ratings yet

- Solution - Business Income - Bonda Enterprise Feb2021Document2 pagesSolution - Business Income - Bonda Enterprise Feb2021HANIS IZYAN MAT ISANo ratings yet

- 2013 Jan A2 MSDocument15 pages2013 Jan A2 MSzaainmariyam12No ratings yet

- Tutorial Cash FlowDocument18 pagesTutorial Cash FlowmellNo ratings yet

- 2007 Jan U1 U2 PDFDocument31 pages2007 Jan U1 U2 PDFTharakaaNo ratings yet

- 2022 Grade 11 Provincial Examination Accounting P1 (English) June 2022 Possible AnswersDocument10 pages2022 Grade 11 Provincial Examination Accounting P1 (English) June 2022 Possible AnswersChantelle IsaksNo ratings yet

- JAN 2024 (1)Document3 pagesJAN 2024 (1)Nur Alya DamiaNo ratings yet

- Solutions of Revision Session by AMK Sept 2020 AttemptDocument13 pagesSolutions of Revision Session by AMK Sept 2020 AttemptShehrozSTNo ratings yet

- Fac2601-2013-6 - Answers PDFDocument9 pagesFac2601-2013-6 - Answers PDFcandiceNo ratings yet

- Financial Accounting and Reporting: IFRS - 2015 December MSDocument18 pagesFinancial Accounting and Reporting: IFRS - 2015 December MSMarchella LukitoNo ratings yet

- Financial Accounting and Reporting: IFRS - 2016 June MSDocument17 pagesFinancial Accounting and Reporting: IFRS - 2016 June MSMarchella LukitoNo ratings yet

- Mark Scheme - AccountingDocument23 pagesMark Scheme - AccountingDanielNo ratings yet

- Broadway Bridge Design Workshop PowerpointDocument47 pagesBroadway Bridge Design Workshop PowerpointMark ReinhardtNo ratings yet

- Summary of Bank Niaga'S Case Study A. A Glance of Bank NiagaDocument4 pagesSummary of Bank Niaga'S Case Study A. A Glance of Bank Niagaaldiansyar mugiaNo ratings yet

- Pre-Advanced 1 - Final Written Test - Tipo BDocument5 pagesPre-Advanced 1 - Final Written Test - Tipo BJulia SantosNo ratings yet

- Mcafee Data Loss Prevention Endpoint For Windows 11.0 Update 6 Release NotesDocument5 pagesMcafee Data Loss Prevention Endpoint For Windows 11.0 Update 6 Release NoteselibunNo ratings yet

- Home Economics 2008 PDFDocument37 pagesHome Economics 2008 PDFAndrew ArahaNo ratings yet

- 27.0 - Confined Spaces v3.0 EnglishDocument14 pages27.0 - Confined Spaces v3.0 Englishwaheed0% (1)

- III Sem Eafm Indian Banking System NewDocument1 pageIII Sem Eafm Indian Banking System NewSuryaNo ratings yet

- Annual Report Library Management System 2020-2021Document144 pagesAnnual Report Library Management System 2020-2021ARUNAVA SAMANTANo ratings yet

- The Canterville Ghost and Other Stories: Book KeyDocument4 pagesThe Canterville Ghost and Other Stories: Book KeyDesweet12No ratings yet

- Dekada '70 Reaction PaperDocument1 pageDekada '70 Reaction PaperSaxourie XiaoNo ratings yet

- Principles of Accounting Past Paper 1Document6 pagesPrinciples of Accounting Past Paper 1Muhannad AliNo ratings yet

- Final Advt VS PA-IDocument14 pagesFinal Advt VS PA-IDivyesh HarwaniNo ratings yet

- When Your Spouse Wants A Divorce and You Don't: Kim BowenDocument16 pagesWhen Your Spouse Wants A Divorce and You Don't: Kim Boweninneed1100% (1)

- LESLIE, C. Scientific Racism Reflections On Peer Review, Science and IdeologyDocument22 pagesLESLIE, C. Scientific Racism Reflections On Peer Review, Science and IdeologyÉden RodriguesNo ratings yet

- NTCP AnalysisDocument12 pagesNTCP AnalysisParas KhuranaNo ratings yet

- Lecture 2 - Cost AssignmentDocument10 pagesLecture 2 - Cost AssignmentJaquin0% (1)

- Borrowing Cost & Gov Grants-QUIZDocument3 pagesBorrowing Cost & Gov Grants-QUIZDanah EstilloreNo ratings yet

- Nil EndorsementDocument1 pageNil EndorsementDhawal SharmaNo ratings yet

- CLE 7 Week 3 - Prophets Speak To Us About HolinessDocument5 pagesCLE 7 Week 3 - Prophets Speak To Us About HolinessSrRose Ann ReballosNo ratings yet

- Vendor Selection CriteriaDocument2 pagesVendor Selection CriteriaMohammad Faraz AkhterNo ratings yet

- Produse ROSHEN Cota TVADocument6 pagesProduse ROSHEN Cota TVABadea BogdanNo ratings yet

- How To Design and Conduct A Country Programme Evaluation at UnfpaDocument228 pagesHow To Design and Conduct A Country Programme Evaluation at UnfpaskurgniydNo ratings yet

- ISSO (Class-7) WorksheetDocument17 pagesISSO (Class-7) WorksheetCHITRAKSHI GEHLOTNo ratings yet

- Personality, Attitudes, and Work BehaviorsDocument3 pagesPersonality, Attitudes, and Work BehaviorsNoella ColesioNo ratings yet

- I AM - Week 9 - Jehovah TsidkenuDocument42 pagesI AM - Week 9 - Jehovah TsidkenuHarvest Time Church100% (1)

- Composers in The MoviesDocument382 pagesComposers in The Moviessandranoriega135150% (2)

- 78903567-Garga by GargacharyaDocument55 pages78903567-Garga by GargacharyaGirish BegoorNo ratings yet

- P A V E: Ilot Ircraft EN Ironment Xternal PressuresDocument1 pageP A V E: Ilot Ircraft EN Ironment Xternal PressuresSohailArdeshiriNo ratings yet