Download as pdf or txt

You might also like

- Ravi R Kumar August MasterclassDocument16 pagesRavi R Kumar August Masterclasssachin kundal100% (2)

- Petroleum Economics and Engineering, 3rd EdDocument466 pagesPetroleum Economics and Engineering, 3rd Edneft94% (17)

- ECO 415 CH 1 IntroDocument22 pagesECO 415 CH 1 IntroMohd ZaidNo ratings yet

- 1 - Basic Concepts and PrinciplesDocument35 pages1 - Basic Concepts and Principlessanthosh sNo ratings yet

- Introduction To Managerial EconomicsDocument23 pagesIntroduction To Managerial EconomicsVaibhav ChauhanNo ratings yet

- Economics Chap1Document68 pagesEconomics Chap1samuelNo ratings yet

- 1.1.1 The Economic Problem JHODocument37 pages1.1.1 The Economic Problem JHOJoel HollidayNo ratings yet

- Introduction To Economics by Ranjul RastogiDocument19 pagesIntroduction To Economics by Ranjul RastogiranjulNo ratings yet

- EconomicsDocument81 pagesEconomicsChrizel BreytenbachNo ratings yet

- A'Level Ecos NotesDocument342 pagesA'Level Ecos NotesBeckham T MaromoNo ratings yet

- Module 1 The Study of EconomicsDocument101 pagesModule 1 The Study of EconomicsEdrei Anthony RoblesNo ratings yet

- Document 23Document33 pagesDocument 232023856678No ratings yet

- Economics October 20, 2020 Week 2Document18 pagesEconomics October 20, 2020 Week 2Jake DayworkNo ratings yet

- ECN1101 Micro Economics: Ms. FaridaDocument24 pagesECN1101 Micro Economics: Ms. FaridaFarida ViraniNo ratings yet

- Microeconomics Notes - Saungweme - Nov2020Document54 pagesMicroeconomics Notes - Saungweme - Nov2020FARAI KABANo ratings yet

- Introduction To Economics. - MicroeconomicsDocument321 pagesIntroduction To Economics. - MicroeconomicsMelusi ShanziNo ratings yet

- Managerial Economics: Chapter One Introducing EconomicsDocument24 pagesManagerial Economics: Chapter One Introducing EconomicsRadoNo ratings yet

- Basic Concepts of EconomicsDocument30 pagesBasic Concepts of EconomicsKashif SaeedNo ratings yet

- Basic Concepts and PrinciplesDocument16 pagesBasic Concepts and PrinciplesayushiNo ratings yet

- Unit-I EconomicsDocument88 pagesUnit-I EconomicspecmbaNo ratings yet

- Learning Outcome 1 Part 1 Understand Economic Relationships Using GraphsDocument46 pagesLearning Outcome 1 Part 1 Understand Economic Relationships Using GraphsLikamva MgqamqhoNo ratings yet

- Review Session: ECON 105-D100 Spring 2024Document46 pagesReview Session: ECON 105-D100 Spring 2024Sebastian MujicaNo ratings yet

- Grade XI - Microeconomics - IntroductionDocument22 pagesGrade XI - Microeconomics - Introductionsreevaibhavi2107No ratings yet

- 101-Managerial Economics - MBADocument268 pages101-Managerial Economics - MBAKanishk P SNo ratings yet

- H2 Economics Notes (Overmugged)Document37 pagesH2 Economics Notes (Overmugged)Durai Manickam NizanthNo ratings yet

- Managerial Economics: MBAFT 6103Document36 pagesManagerial Economics: MBAFT 6103rajat9goelNo ratings yet

- FA1314 Essentials of Economic - Lesson 1 - STUDENTSDocument70 pagesFA1314 Essentials of Economic - Lesson 1 - STUDENTSCHEAH� GUO XINGNo ratings yet

- Health Economics 2Document71 pagesHealth Economics 2NICHOLAS KAUMBANo ratings yet

- Topic 1 Intro To EconomicsDocument39 pagesTopic 1 Intro To EconomicsNorainah Abdul GaniNo ratings yet

- The Economic Problem Opportunity Cost Production Possibility FrontiersDocument10 pagesThe Economic Problem Opportunity Cost Production Possibility FrontiersMonkey2111No ratings yet

- Week 1 Introduction To MicroeconomicsDocument39 pagesWeek 1 Introduction To Microeconomicstissot63No ratings yet

- Introduction To MicroeconomicsDocument43 pagesIntroduction To MicroeconomicshassamNo ratings yet

- Introduction To Economics: Choices, Choices, Choices, - .Document68 pagesIntroduction To Economics: Choices, Choices, Choices, - .shahumang11No ratings yet

- AP Macro Unit 1 SummaryDocument110 pagesAP Macro Unit 1 SummaryJonathan CarrollNo ratings yet

- Chapter 02Document6 pagesChapter 02Hope Trinity EnriquezNo ratings yet

- Econs Slides - Lecture One-1Document37 pagesEcons Slides - Lecture One-1seidujude10No ratings yet

- Business Economics BBA-107 Unit-1Document252 pagesBusiness Economics BBA-107 Unit-1Vivek BaloniNo ratings yet

- Eco IntroDocument20 pagesEco IntroREHANRAJNo ratings yet

- Microeconomics Course: BY Emery Emerimana MBA-Project Management and Finance Email: Tel: 71 578 069/75 658 470Document103 pagesMicroeconomics Course: BY Emery Emerimana MBA-Project Management and Finance Email: Tel: 71 578 069/75 658 470dan dylan terimbereNo ratings yet

- Principles of Economics 1Document36 pagesPrinciples of Economics 1reda gadNo ratings yet

- Economics?!?!!!: Economic Perspectives, Ideas and PrinciplesDocument37 pagesEconomics?!?!!!: Economic Perspectives, Ideas and PrinciplesitsurassNo ratings yet

- Engineering Economics and Management: Dr. Md. Aynal HaqueDocument64 pagesEngineering Economics and Management: Dr. Md. Aynal Haquesojib yeasinNo ratings yet

- Pengantar Ekonomi Pert 1Document75 pagesPengantar Ekonomi Pert 1Perfect DarksideNo ratings yet

- Unit 1 Summary (For Posting Online)Document63 pagesUnit 1 Summary (For Posting Online)Legogie Moses AnoghenaNo ratings yet

- Managerial Economics - Chapter 1 - Introducing EconomicsDocument35 pagesManagerial Economics - Chapter 1 - Introducing EconomicsAhmed SaeidNo ratings yet

- Introduction To EconomicsDocument15 pagesIntroduction To EconomicsNainika ReddyNo ratings yet

- Type Your TextDocument32 pagesType Your TextDevyansh GuptaNo ratings yet

- #1 Introduction To Economics - 2020Document30 pages#1 Introduction To Economics - 2020Rachmad AriefNo ratings yet

- Thinking Like An Economist:: Studying Scarcity, or Quantifying Both What You Don't and What You Can't HaveDocument314 pagesThinking Like An Economist:: Studying Scarcity, or Quantifying Both What You Don't and What You Can't HaveSébastien UrienNo ratings yet

- Opportunity Cost and PPC Presentation 2Document26 pagesOpportunity Cost and PPC Presentation 2adriana suasnavar.No ratings yet

- Introductory LectureDocument30 pagesIntroductory LectureayushiNo ratings yet

- Chapter 1 - Intro Eco162Document5 pagesChapter 1 - Intro Eco162daliaikhram98100% (1)

- Basics of Economics For Sport StudentsDocument69 pagesBasics of Economics For Sport StudentsAttila KajosNo ratings yet

- Principles of Economic Lecture NotesDocument21 pagesPrinciples of Economic Lecture NotesadelaideglxNo ratings yet

- Applied Economics Lesson 1 PDFDocument41 pagesApplied Economics Lesson 1 PDFStephanie Mae BulaongNo ratings yet

- Macroeconomics CH 1Document30 pagesMacroeconomics CH 1karim kobeissiNo ratings yet

- Micro - 02 - Choice in A World of ScarcityDocument26 pagesMicro - 02 - Choice in A World of ScarcityYah Yah CarioNo ratings yet

- Chapter 1Document35 pagesChapter 1Nidhi HiranwarNo ratings yet

- Introduction To Economics: Choices, Choices, Choices, - .Document69 pagesIntroduction To Economics: Choices, Choices, Choices, - .Prasad GharatNo ratings yet

- Microeconomics NotesDocument49 pagesMicroeconomics NotesNever DoviNo ratings yet

- Slides NotesDocument20 pagesSlides Notesnabihah zaidiNo ratings yet

- 1 - Demand and Supply Analysis-1Document31 pages1 - Demand and Supply Analysis-1jrntrmprNo ratings yet

- Unit 2_HRMDocument45 pagesUnit 2_HRMjrntrmprNo ratings yet

- Iep Balance of PaymentDocument7 pagesIep Balance of PaymentjrntrmprNo ratings yet

- BPV-2 EmbroideryDocument15 pagesBPV-2 EmbroideryjrntrmprNo ratings yet

- Book.133 - CA Inter - IT - Problems - Solutions - PT 2 - 5 Chs - 155 Pgs - 46th Ses Reg. Btchs - ImageDocument155 pagesBook.133 - CA Inter - IT - Problems - Solutions - PT 2 - 5 Chs - 155 Pgs - 46th Ses Reg. Btchs - ImagejrntrmprNo ratings yet

- Milky Meadows DairyDocument23 pagesMilky Meadows DairyjrntrmprNo ratings yet

- Book 24 - CA Inter - 46th Session Reg Bts - F.M - 46E - PT 2 - 67 Pgs - ImageDocument67 pagesBook 24 - CA Inter - 46th Session Reg Bts - F.M - 46E - PT 2 - 67 Pgs - ImagejrntrmprNo ratings yet

- Book 25 - CA Inter - 46th Session Regular Batches - Costing - Part 3 - 1 Chapter - 52 Pages - ImageDocument52 pagesBook 25 - CA Inter - 46th Session Regular Batches - Costing - Part 3 - 1 Chapter - 52 Pages - ImagejrntrmprNo ratings yet

- Book 95 - CA Inter - 46th Ses Reg Batches - Acc Standards - Gr.2 - PT 6 - 1 CH - 21 Pgs - ImageDocument21 pagesBook 95 - CA Inter - 46th Ses Reg Batches - Acc Standards - Gr.2 - PT 6 - 1 CH - 21 Pgs - ImagejrntrmprNo ratings yet

- Book 27 - CA Inter - 46th Session Reg Bts - Income Tax - MCQs - PT 1 - 129 Pgs. - ImageDocument129 pagesBook 27 - CA Inter - 46th Session Reg Bts - Income Tax - MCQs - PT 1 - 129 Pgs. - ImagejrntrmprNo ratings yet

- Book 94 - CA Inter - 46th Session Reg Batches - C Law - PT 10 - 1 CH - 25 Pgs - ImageDocument25 pagesBook 94 - CA Inter - 46th Session Reg Batches - C Law - PT 10 - 1 CH - 25 Pgs - ImagejrntrmprNo ratings yet

- Book 26 - CA Inter - 46th Session Reg Bts - Costing (Theory) - All Chs - 77 Pgs - ImageDocument77 pagesBook 26 - CA Inter - 46th Session Reg Bts - Costing (Theory) - All Chs - 77 Pgs - ImagejrntrmprNo ratings yet

- Book 30 - CA Inter - 46th Reg. Bts - LAW - PT 4 - 1 CH - 80 Pgs - ImageDocument82 pagesBook 30 - CA Inter - 46th Reg. Bts - LAW - PT 4 - 1 CH - 80 Pgs - ImagejrntrmprNo ratings yet

- Book 29 - Valuation Rules For CA InterDocument6 pagesBook 29 - Valuation Rules For CA InterjrntrmprNo ratings yet

- SAP MM PurchaseDocument56 pagesSAP MM PurchasesagarthegameNo ratings yet

- The Global Economy and Market Integration: Lexie Vera P MagawayDocument29 pagesThe Global Economy and Market Integration: Lexie Vera P MagawayJames Dagohoy AmbayNo ratings yet

- Catalogue Golden Dragon MelamineDocument51 pagesCatalogue Golden Dragon MelamineYetty SyamsiyatiNo ratings yet

- Balanced Drilling With Coiled TubingDocument9 pagesBalanced Drilling With Coiled TubingMin Thant MaungNo ratings yet

- Tabix 1-50 ENDocument1 pageTabix 1-50 ENuğur alparslanNo ratings yet

- HX 75Document1 pageHX 75cs gunungparaNo ratings yet

- Draft Allotment: 4174 - ST. Vincent Pallotti College of Engineering & Technology, NagpurDocument7 pagesDraft Allotment: 4174 - ST. Vincent Pallotti College of Engineering & Technology, NagpurChinmay MokhareNo ratings yet

- Akuntansi Keuangan 2 - Semester 4Document13 pagesAkuntansi Keuangan 2 - Semester 4Andrew AlamsyahNo ratings yet

- Chapter 5 - Relevant Information and Decision Making - StudentsDocument27 pagesChapter 5 - Relevant Information and Decision Making - StudentsDAN NGUYEN THENo ratings yet

- Conselation BillDocument4 pagesConselation BillSheeza NoorNo ratings yet

- Cable Lugs Bonding WireDocument3 pagesCable Lugs Bonding WireJwalaNo ratings yet

- Proposed SolutionDocument2 pagesProposed SolutionRyan MartinezNo ratings yet

- Exit Guide From ProperziDocument2 pagesExit Guide From Properzimuhammad kasyfuNo ratings yet

- 2.5 MM 1250....Document1 page2.5 MM 1250....Balaji Defence100% (1)

- Finma1 Module 2 Lesson 2Document15 pagesFinma1 Module 2 Lesson 2Jeranz ColansiNo ratings yet

- Development of Prototype and Simulation Testing For Automatic Bottle Unscramble MachineDocument15 pagesDevelopment of Prototype and Simulation Testing For Automatic Bottle Unscramble MachineSkano ChellahNo ratings yet

- Flat Sale in EnglishDocument7 pagesFlat Sale in EnglishDeep HiraniNo ratings yet

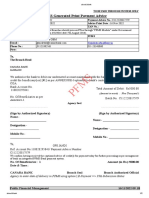

- PFMS Generated Print Payment Advice: To, The Branch HeadDocument2 pagesPFMS Generated Print Payment Advice: To, The Branch HeadPunjabi JindNo ratings yet

- Nonlinear Relationships: Y X X X X EYXDocument23 pagesNonlinear Relationships: Y X X X X EYXEmmanuella EmefeNo ratings yet

- Terex RT780Document20 pagesTerex RT780Pelican PelcomNo ratings yet

- Mecco Furniture Purchase Order PDFDocument9 pagesMecco Furniture Purchase Order PDFerrol SksoanaNo ratings yet

- Florencia Huibonhoa vs. Court of Appeals G.R. No. 95897, December 14, 1999 320 SCRA 625Document2 pagesFlorencia Huibonhoa vs. Court of Appeals G.R. No. 95897, December 14, 1999 320 SCRA 625Sofia DavidNo ratings yet

- Free Decision Tree Diagram TemplateDocument8 pagesFree Decision Tree Diagram TemplateBadrun TamanNo ratings yet

- Most Expensive Currency - Google SearchDocument1 pageMost Expensive Currency - Google SearchAbdulla JamalNo ratings yet

- Bed Discounts Top Students Sy 2021 2022Document12 pagesBed Discounts Top Students Sy 2021 2022Renen Millo BantilloNo ratings yet

- Pag IbigDocument1 pagePag IbigVenus AgustinNo ratings yet

- Quantity Surveying Field and Industry inDocument11 pagesQuantity Surveying Field and Industry inmally IzzatiNo ratings yet

- APL Apollo Tubes: Piping Gains Rating: BuyDocument28 pagesAPL Apollo Tubes: Piping Gains Rating: BuygnanaNo ratings yet