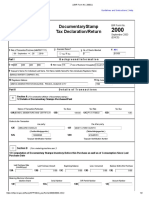

Hapi_tax_form_mar.-2024

Hapi_tax_form_mar.-2024

You might also like

- Math Lit Learner Relab Grade 11 Term 1 - 4Document62 pagesMath Lit Learner Relab Grade 11 Term 1 - 4coolkidkwaneleNo ratings yet

- MC Tax QuestionsDocument15 pagesMC Tax QuestionsTreymayne0% (2)

- Public Sector Accounting and Administrative Practices in Nigeria Volume 1From EverandPublic Sector Accounting and Administrative Practices in Nigeria Volume 1No ratings yet

- Creditable Withholding Tax ReviewerDocument6 pagesCreditable Withholding Tax ReviewerMark Rainer Yongis LozaresNo ratings yet

- Useful Information On Customs MattersDocument726 pagesUseful Information On Customs MattersAditi SharmaNo ratings yet

- Bigstock 2018 Tax Form PDFDocument1 pageBigstock 2018 Tax Form PDFBalint RoxanaNo ratings yet

- Cmty2020 2872739 1042-S 00 20210310 V01Document6 pagesCmty2020 2872739 1042-S 00 20210310 V01Muhammad RizalNo ratings yet

- Foreign Person's U.S. Source Income Subject To Withholding: Copy BDocument2 pagesForeign Person's U.S. Source Income Subject To Withholding: Copy BalexxxeosNo ratings yet

- PrintDocument5 pagesPrintErikaNo ratings yet

- Shutterstock - 2022 - Tax - Form - DANIEL CONSTANTE-3Document2 pagesShutterstock - 2022 - Tax - Form - DANIEL CONSTANTE-3Daniel ConstanteNo ratings yet

- Foreign Person's U.S. Source Income Subject To Withholding: Copy ADocument7 pagesForeign Person's U.S. Source Income Subject To Withholding: Copy Acherifelouazzani1967No ratings yet

- Formulario 1042 S Marzo 2020Document2 pagesFormulario 1042 S Marzo 2020martin_kubrickNo ratings yet

- Foreign Person's U.S. Source Income Subject To Withholding: Copy BDocument6 pagesForeign Person's U.S. Source Income Subject To Withholding: Copy BAshot KHACHATOURIAN100% (1)

- Foreign Person's U.S. Source Income Subject To Withholding: Copy BDocument2 pagesForeign Person's U.S. Source Income Subject To Withholding: Copy BshamlaNo ratings yet

- Foreign Person's U.S. Source Income Subject To Withholding: Copy BDocument2 pagesForeign Person's U.S. Source Income Subject To Withholding: Copy Balexacas51993No ratings yet

- Foreign Person's U.S. Source Income Subject To Withholding: Copy CDocument4 pagesForeign Person's U.S. Source Income Subject To Withholding: Copy Cemiliowebster6833No ratings yet

- Robinhood Crypto LLC 85 Willow Road Menlo Park, Ca 94025Document4 pagesRobinhood Crypto LLC 85 Willow Road Menlo Park, Ca 94025Jack BotNo ratings yet

- Certificate of Final Tax Withheld at Source: Kawanihan NG Rentas InternasDocument5 pagesCertificate of Final Tax Withheld at Source: Kawanihan NG Rentas InternasBrianSantiagoNo ratings yet

- Certificate of Final Tax Withheld at SourceDocument7 pagesCertificate of Final Tax Withheld at Sourcegloryfe almodalNo ratings yet

- DSTDocument2 pagesDSTRen A EleponioNo ratings yet

- Documentary Stamp Tax Declaration/Return: Fill in All Applicable Spaces. Mark All Appropriate Boxes With An "X"Document3 pagesDocumentary Stamp Tax Declaration/Return: Fill in All Applicable Spaces. Mark All Appropriate Boxes With An "X"Jansen SantosNo ratings yet

- EWT For The OCT-23 PeriodDocument12 pagesEWT For The OCT-23 Periodqhi.cgmacatiagNo ratings yet

- Form 1099-INT - 2022 - Template1 - Document 01Document9 pagesForm 1099-INT - 2022 - Template1 - Document 01chamuditha dilshanNo ratings yet

- Bir Form 1600 FinalDocument4 pagesBir Form 1600 Finaljhonnamaemaygue08No ratings yet

- Tax Year 2015: Important Tax Information DocumentDocument2 pagesTax Year 2015: Important Tax Information DocumentBoldie LutwigNo ratings yet

- Certificate of Final Tax Withheld at Source: Kawanihan NG Rentas InternasDocument2 pagesCertificate of Final Tax Withheld at Source: Kawanihan NG Rentas Internasben carlo ramos srNo ratings yet

- 15 Ca CBDocument6 pages15 Ca CBMithileshNo ratings yet

- Fill in All Applicable Spaces. Mark All Appropriate Boxes With An "X"Document4 pagesFill in All Applicable Spaces. Mark All Appropriate Boxes With An "X"Emelyn Ventura SantosNo ratings yet

- Untitled 26Document6 pagesUntitled 26Felipe CortezNo ratings yet

- Personal Tax Return Form IT 11GA 2023Document18 pagesPersonal Tax Return Form IT 11GA 2023Dilbar BabaNo ratings yet

- Fill in All Applicable Spaces. Mark All Appropriate Boxes With An "X"Document5 pagesFill in All Applicable Spaces. Mark All Appropriate Boxes With An "X"May Joy DepalomaNo ratings yet

- Aa Aluminum Supply Inc.Document5 pagesAa Aluminum Supply Inc.Ben Carlo RamosNo ratings yet

- Certificate of Final Tax Withheld at Source: 004 053 294 000 Barangay CentroDocument5 pagesCertificate of Final Tax Withheld at Source: 004 053 294 000 Barangay CentroHa HakdogNo ratings yet

- Certificate of Final Tax Withheld at Source: 004 053 294 000 Barangay CentroDocument5 pagesCertificate of Final Tax Withheld at Source: 004 053 294 000 Barangay CentroHa HakdogNo ratings yet

- Documentary Stamp Tax Declaration/ReturnDocument4 pagesDocumentary Stamp Tax Declaration/ReturnPajarillo Kathy AnnNo ratings yet

- 2019 08 05 12 06 16 916 - Aahca2537l - 2020Document4 pages2019 08 05 12 06 16 916 - Aahca2537l - 2020MithileshNo ratings yet

- With Holding Tax ASTDocument10 pagesWith Holding Tax ASTAnonymous ZRWdF8h3No ratings yet

- RTMF 990Document49 pagesRTMF 990Craig MaugerNo ratings yet

- Kawanihan NG Rentas Internas: Bernardo Samuel G. CadienteDocument3 pagesKawanihan NG Rentas Internas: Bernardo Samuel G. CadienteRexelleAllapitanCorderoNo ratings yet

- ftch-20f 20191231.htmDocument185 pagesftch-20f 20191231.htmMatthew NgNo ratings yet

- Form 1100Document1 pageForm 1100Hï FrequencyNo ratings yet

- Lse Eros 2018Document186 pagesLse Eros 2018Akanksha MalhotraNo ratings yet

- Ba Credit Card Funding, LLC Bank of America, National AssociationDocument30 pagesBa Credit Card Funding, LLC Bank of America, National AssociationishfaqqqNo ratings yet

- MyMichigan Medical Center Alpena 2023 990Document108 pagesMyMichigan Medical Center Alpena 2023 990JustinHinkleyNo ratings yet

- Form 2306 Witn Computation Electric BillDocument3 pagesForm 2306 Witn Computation Electric BillJanus Salinas100% (2)

- Sonali Securities WTR (Jan'22-June'22) 75ADocument8 pagesSonali Securities WTR (Jan'22-June'22) 75Alimon islamNo ratings yet

- Bir Form 2307 SampleDocument3 pagesBir Form 2307 SampleEliza Cortez Castro50% (2)

- 2306Document2 pages2306joselNo ratings yet

- SLB Annual Report 2023: Form 10-K (NYSE:SLB)Document67 pagesSLB Annual Report 2023: Form 10-K (NYSE:SLB)Suporte TecnicoNo ratings yet

- Avaaz Foundation - 2022 Form 990Document49 pagesAvaaz Foundation - 2022 Form 990falconson.bNo ratings yet

- 20212Document2 pages20212carriemccabe0% (1)

- Irs Form 1099 BDocument9 pagesIrs Form 1099 BMikhael Yah-Shah Dean: VeilourNo ratings yet

- FBR FerozabadDocument1 pageFBR Ferozabadferozabad schoolNo ratings yet

- Certificate of Final Tax Withheld at Source: Kawanihan NG Rentas InternasDocument3 pagesCertificate of Final Tax Withheld at Source: Kawanihan NG Rentas InternasAnaliza ValdehuezaNo ratings yet

- Abayao-Worwor Furniture ShopDocument4 pagesAbayao-Worwor Furniture ShopBen Carlo RamosNo ratings yet

- U.S. Income Tax Return For An S Corporation: For Calendar Year 2023 or Tax Year Beginning, 2023, Ending, 20Document5 pagesU.S. Income Tax Return For An S Corporation: For Calendar Year 2023 or Tax Year Beginning, 2023, Ending, 20h0oud4No ratings yet

- Bir 2306 PLDTDocument9 pagesBir 2306 PLDTKevinjhen ManaloNo ratings yet

- Hong Thien PhuocBui2018Document6 pagesHong Thien PhuocBui2018Thien BaoNo ratings yet

- Bir 1600Document13 pagesBir 1600Adelaida TuazonNo ratings yet

- Drafted BIR Form No. 2000Document2 pagesDrafted BIR Form No. 2000Kevin Besa100% (1)

- 1099 Misc 1Document1 page1099 Misc 1Anonymous FR8yGDSVgNo ratings yet

- Wealth Management Planning: The UK Tax PrinciplesFrom EverandWealth Management Planning: The UK Tax PrinciplesRating: 4.5 out of 5 stars4.5/5 (2)

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- J.K. Lasser's Your Income Tax 2024: For Preparing Your 2023 Tax ReturnFrom EverandJ.K. Lasser's Your Income Tax 2024: For Preparing Your 2023 Tax ReturnNo ratings yet

- UGC NET Economics QuestionsDocument17 pagesUGC NET Economics QuestionsMohammed Rafeeq AhmedNo ratings yet

- What Is An RRSP?: Prepared For CHOU Financial June 14, 2012Document3 pagesWhat Is An RRSP?: Prepared For CHOU Financial June 14, 2012api-97071804No ratings yet

- 19) ? All of These 20) Had Increased and Interest Rates Had DecreasedDocument369 pages19) ? All of These 20) Had Increased and Interest Rates Had DecreasedVibhasNo ratings yet

- Alternative Minimum TaxDocument2 pagesAlternative Minimum TaxJeremy A. MillerNo ratings yet

- Itctp 2022Document4 pagesItctp 2022Muskaan ShawNo ratings yet

- Brief Exercise 10.1: Cash Payment For Interest Expense in Y1Document5 pagesBrief Exercise 10.1: Cash Payment For Interest Expense in Y1KAINAT MUSHTAQNo ratings yet

- CENTRAL AZUCARERA DE DON PEDRO v. CITY OF MANILADocument14 pagesCENTRAL AZUCARERA DE DON PEDRO v. CITY OF MANILAKC FOV GrievanceNo ratings yet

- TenderDocument31 pagesTenderdurgesh pandharpureNo ratings yet

- Councilwoman Gym Press ReleaseDocument3 pagesCouncilwoman Gym Press ReleaseIan GaviganNo ratings yet

- Taxation Academy Handout-CDocument5 pagesTaxation Academy Handout-CMarcellin MarcaNo ratings yet

- Joint Venture Return of Investment Remittance: Irc@ccccltd - CNDocument14 pagesJoint Venture Return of Investment Remittance: Irc@ccccltd - CNBenjaminNo ratings yet

- Signature Authorization: Departrnent The Treasury Rer¡enlle SeruiceDocument2 pagesSignature Authorization: Departrnent The Treasury Rer¡enlle SeruiceMartha SanchezNo ratings yet

- Draft Terms and Conditions ("Terms Sheet") : Supply of Recycled Water by GVSCCL To RINL's Visakhapatnam Steel PlantDocument7 pagesDraft Terms and Conditions ("Terms Sheet") : Supply of Recycled Water by GVSCCL To RINL's Visakhapatnam Steel PlantR VIJAYACHANDRANo ratings yet

- Principles of Marketing Term Project Module 2Document16 pagesPrinciples of Marketing Term Project Module 2Palize QaziNo ratings yet

- The Battle Over Gambling: Illeg AlDocument4 pagesThe Battle Over Gambling: Illeg AlCatherine SnowNo ratings yet

- Affidavit Diploma SSCDocument2 pagesAffidavit Diploma SSCdaniel jejillosNo ratings yet

- Annual Report 2017 Sree Rayalseema Hi PDFDocument115 pagesAnnual Report 2017 Sree Rayalseema Hi PDFSukhsagar AggarwalNo ratings yet

- ECO121 Group Assignment Report Group 1Document10 pagesECO121 Group Assignment Report Group 1Nhat HuyyNo ratings yet

- Business Plan WS-97 FormatDocument7 pagesBusiness Plan WS-97 FormatSanjay Vyas0% (1)

- Holland Aptitude TestDocument15 pagesHolland Aptitude Testpari talukdarNo ratings yet

- Financial Management: Friday 6 December 2013Document5 pagesFinancial Management: Friday 6 December 2013Nirmal ShresthaNo ratings yet

- PHIL 215 - Final Exam NotesDocument99 pagesPHIL 215 - Final Exam NotesDavidKnightNo ratings yet

- Get Out of The System Letter Pre-Tax CourtDocument14 pagesGet Out of The System Letter Pre-Tax CourtPublic Knowledge100% (9)

- Jesus Sacred Heart College vs. CirDocument2 pagesJesus Sacred Heart College vs. CirMC Quesada100% (2)

- AssignmentDocument5 pagesAssignmentMd. Alif HossainNo ratings yet

- Comparative Analysis 8424 and 10963Document31 pagesComparative Analysis 8424 and 10963Rizza Angela Mangalleno100% (2)

Download as pdf or txt

You might also like

- Math Lit Learner Relab Grade 11 Term 1 - 4Document62 pagesMath Lit Learner Relab Grade 11 Term 1 - 4coolkidkwaneleNo ratings yet

- MC Tax QuestionsDocument15 pagesMC Tax QuestionsTreymayne0% (2)

- Public Sector Accounting and Administrative Practices in Nigeria Volume 1From EverandPublic Sector Accounting and Administrative Practices in Nigeria Volume 1No ratings yet

- Creditable Withholding Tax ReviewerDocument6 pagesCreditable Withholding Tax ReviewerMark Rainer Yongis LozaresNo ratings yet

- Useful Information On Customs MattersDocument726 pagesUseful Information On Customs MattersAditi SharmaNo ratings yet

- Bigstock 2018 Tax Form PDFDocument1 pageBigstock 2018 Tax Form PDFBalint RoxanaNo ratings yet

- Cmty2020 2872739 1042-S 00 20210310 V01Document6 pagesCmty2020 2872739 1042-S 00 20210310 V01Muhammad RizalNo ratings yet

- Foreign Person's U.S. Source Income Subject To Withholding: Copy BDocument2 pagesForeign Person's U.S. Source Income Subject To Withholding: Copy BalexxxeosNo ratings yet

- PrintDocument5 pagesPrintErikaNo ratings yet

- Shutterstock - 2022 - Tax - Form - DANIEL CONSTANTE-3Document2 pagesShutterstock - 2022 - Tax - Form - DANIEL CONSTANTE-3Daniel ConstanteNo ratings yet

- Foreign Person's U.S. Source Income Subject To Withholding: Copy ADocument7 pagesForeign Person's U.S. Source Income Subject To Withholding: Copy Acherifelouazzani1967No ratings yet

- Formulario 1042 S Marzo 2020Document2 pagesFormulario 1042 S Marzo 2020martin_kubrickNo ratings yet

- Foreign Person's U.S. Source Income Subject To Withholding: Copy BDocument6 pagesForeign Person's U.S. Source Income Subject To Withholding: Copy BAshot KHACHATOURIAN100% (1)

- Foreign Person's U.S. Source Income Subject To Withholding: Copy BDocument2 pagesForeign Person's U.S. Source Income Subject To Withholding: Copy BshamlaNo ratings yet

- Foreign Person's U.S. Source Income Subject To Withholding: Copy BDocument2 pagesForeign Person's U.S. Source Income Subject To Withholding: Copy Balexacas51993No ratings yet

- Foreign Person's U.S. Source Income Subject To Withholding: Copy CDocument4 pagesForeign Person's U.S. Source Income Subject To Withholding: Copy Cemiliowebster6833No ratings yet

- Robinhood Crypto LLC 85 Willow Road Menlo Park, Ca 94025Document4 pagesRobinhood Crypto LLC 85 Willow Road Menlo Park, Ca 94025Jack BotNo ratings yet

- Certificate of Final Tax Withheld at Source: Kawanihan NG Rentas InternasDocument5 pagesCertificate of Final Tax Withheld at Source: Kawanihan NG Rentas InternasBrianSantiagoNo ratings yet

- Certificate of Final Tax Withheld at SourceDocument7 pagesCertificate of Final Tax Withheld at Sourcegloryfe almodalNo ratings yet

- DSTDocument2 pagesDSTRen A EleponioNo ratings yet

- Documentary Stamp Tax Declaration/Return: Fill in All Applicable Spaces. Mark All Appropriate Boxes With An "X"Document3 pagesDocumentary Stamp Tax Declaration/Return: Fill in All Applicable Spaces. Mark All Appropriate Boxes With An "X"Jansen SantosNo ratings yet

- EWT For The OCT-23 PeriodDocument12 pagesEWT For The OCT-23 Periodqhi.cgmacatiagNo ratings yet

- Form 1099-INT - 2022 - Template1 - Document 01Document9 pagesForm 1099-INT - 2022 - Template1 - Document 01chamuditha dilshanNo ratings yet

- Bir Form 1600 FinalDocument4 pagesBir Form 1600 Finaljhonnamaemaygue08No ratings yet

- Tax Year 2015: Important Tax Information DocumentDocument2 pagesTax Year 2015: Important Tax Information DocumentBoldie LutwigNo ratings yet

- Certificate of Final Tax Withheld at Source: Kawanihan NG Rentas InternasDocument2 pagesCertificate of Final Tax Withheld at Source: Kawanihan NG Rentas Internasben carlo ramos srNo ratings yet

- 15 Ca CBDocument6 pages15 Ca CBMithileshNo ratings yet

- Fill in All Applicable Spaces. Mark All Appropriate Boxes With An "X"Document4 pagesFill in All Applicable Spaces. Mark All Appropriate Boxes With An "X"Emelyn Ventura SantosNo ratings yet

- Untitled 26Document6 pagesUntitled 26Felipe CortezNo ratings yet

- Personal Tax Return Form IT 11GA 2023Document18 pagesPersonal Tax Return Form IT 11GA 2023Dilbar BabaNo ratings yet

- Fill in All Applicable Spaces. Mark All Appropriate Boxes With An "X"Document5 pagesFill in All Applicable Spaces. Mark All Appropriate Boxes With An "X"May Joy DepalomaNo ratings yet

- Aa Aluminum Supply Inc.Document5 pagesAa Aluminum Supply Inc.Ben Carlo RamosNo ratings yet

- Certificate of Final Tax Withheld at Source: 004 053 294 000 Barangay CentroDocument5 pagesCertificate of Final Tax Withheld at Source: 004 053 294 000 Barangay CentroHa HakdogNo ratings yet

- Certificate of Final Tax Withheld at Source: 004 053 294 000 Barangay CentroDocument5 pagesCertificate of Final Tax Withheld at Source: 004 053 294 000 Barangay CentroHa HakdogNo ratings yet

- Documentary Stamp Tax Declaration/ReturnDocument4 pagesDocumentary Stamp Tax Declaration/ReturnPajarillo Kathy AnnNo ratings yet

- 2019 08 05 12 06 16 916 - Aahca2537l - 2020Document4 pages2019 08 05 12 06 16 916 - Aahca2537l - 2020MithileshNo ratings yet

- With Holding Tax ASTDocument10 pagesWith Holding Tax ASTAnonymous ZRWdF8h3No ratings yet

- RTMF 990Document49 pagesRTMF 990Craig MaugerNo ratings yet

- Kawanihan NG Rentas Internas: Bernardo Samuel G. CadienteDocument3 pagesKawanihan NG Rentas Internas: Bernardo Samuel G. CadienteRexelleAllapitanCorderoNo ratings yet

- ftch-20f 20191231.htmDocument185 pagesftch-20f 20191231.htmMatthew NgNo ratings yet

- Form 1100Document1 pageForm 1100Hï FrequencyNo ratings yet

- Lse Eros 2018Document186 pagesLse Eros 2018Akanksha MalhotraNo ratings yet

- Ba Credit Card Funding, LLC Bank of America, National AssociationDocument30 pagesBa Credit Card Funding, LLC Bank of America, National AssociationishfaqqqNo ratings yet

- MyMichigan Medical Center Alpena 2023 990Document108 pagesMyMichigan Medical Center Alpena 2023 990JustinHinkleyNo ratings yet

- Form 2306 Witn Computation Electric BillDocument3 pagesForm 2306 Witn Computation Electric BillJanus Salinas100% (2)

- Sonali Securities WTR (Jan'22-June'22) 75ADocument8 pagesSonali Securities WTR (Jan'22-June'22) 75Alimon islamNo ratings yet

- Bir Form 2307 SampleDocument3 pagesBir Form 2307 SampleEliza Cortez Castro50% (2)

- 2306Document2 pages2306joselNo ratings yet

- SLB Annual Report 2023: Form 10-K (NYSE:SLB)Document67 pagesSLB Annual Report 2023: Form 10-K (NYSE:SLB)Suporte TecnicoNo ratings yet

- Avaaz Foundation - 2022 Form 990Document49 pagesAvaaz Foundation - 2022 Form 990falconson.bNo ratings yet

- 20212Document2 pages20212carriemccabe0% (1)

- Irs Form 1099 BDocument9 pagesIrs Form 1099 BMikhael Yah-Shah Dean: VeilourNo ratings yet

- FBR FerozabadDocument1 pageFBR Ferozabadferozabad schoolNo ratings yet

- Certificate of Final Tax Withheld at Source: Kawanihan NG Rentas InternasDocument3 pagesCertificate of Final Tax Withheld at Source: Kawanihan NG Rentas InternasAnaliza ValdehuezaNo ratings yet

- Abayao-Worwor Furniture ShopDocument4 pagesAbayao-Worwor Furniture ShopBen Carlo RamosNo ratings yet

- U.S. Income Tax Return For An S Corporation: For Calendar Year 2023 or Tax Year Beginning, 2023, Ending, 20Document5 pagesU.S. Income Tax Return For An S Corporation: For Calendar Year 2023 or Tax Year Beginning, 2023, Ending, 20h0oud4No ratings yet

- Bir 2306 PLDTDocument9 pagesBir 2306 PLDTKevinjhen ManaloNo ratings yet

- Hong Thien PhuocBui2018Document6 pagesHong Thien PhuocBui2018Thien BaoNo ratings yet

- Bir 1600Document13 pagesBir 1600Adelaida TuazonNo ratings yet

- Drafted BIR Form No. 2000Document2 pagesDrafted BIR Form No. 2000Kevin Besa100% (1)

- 1099 Misc 1Document1 page1099 Misc 1Anonymous FR8yGDSVgNo ratings yet

- Wealth Management Planning: The UK Tax PrinciplesFrom EverandWealth Management Planning: The UK Tax PrinciplesRating: 4.5 out of 5 stars4.5/5 (2)

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- J.K. Lasser's Your Income Tax 2024: For Preparing Your 2023 Tax ReturnFrom EverandJ.K. Lasser's Your Income Tax 2024: For Preparing Your 2023 Tax ReturnNo ratings yet

- UGC NET Economics QuestionsDocument17 pagesUGC NET Economics QuestionsMohammed Rafeeq AhmedNo ratings yet

- What Is An RRSP?: Prepared For CHOU Financial June 14, 2012Document3 pagesWhat Is An RRSP?: Prepared For CHOU Financial June 14, 2012api-97071804No ratings yet

- 19) ? All of These 20) Had Increased and Interest Rates Had DecreasedDocument369 pages19) ? All of These 20) Had Increased and Interest Rates Had DecreasedVibhasNo ratings yet

- Alternative Minimum TaxDocument2 pagesAlternative Minimum TaxJeremy A. MillerNo ratings yet

- Itctp 2022Document4 pagesItctp 2022Muskaan ShawNo ratings yet

- Brief Exercise 10.1: Cash Payment For Interest Expense in Y1Document5 pagesBrief Exercise 10.1: Cash Payment For Interest Expense in Y1KAINAT MUSHTAQNo ratings yet

- CENTRAL AZUCARERA DE DON PEDRO v. CITY OF MANILADocument14 pagesCENTRAL AZUCARERA DE DON PEDRO v. CITY OF MANILAKC FOV GrievanceNo ratings yet

- TenderDocument31 pagesTenderdurgesh pandharpureNo ratings yet

- Councilwoman Gym Press ReleaseDocument3 pagesCouncilwoman Gym Press ReleaseIan GaviganNo ratings yet

- Taxation Academy Handout-CDocument5 pagesTaxation Academy Handout-CMarcellin MarcaNo ratings yet

- Joint Venture Return of Investment Remittance: Irc@ccccltd - CNDocument14 pagesJoint Venture Return of Investment Remittance: Irc@ccccltd - CNBenjaminNo ratings yet

- Signature Authorization: Departrnent The Treasury Rer¡enlle SeruiceDocument2 pagesSignature Authorization: Departrnent The Treasury Rer¡enlle SeruiceMartha SanchezNo ratings yet

- Draft Terms and Conditions ("Terms Sheet") : Supply of Recycled Water by GVSCCL To RINL's Visakhapatnam Steel PlantDocument7 pagesDraft Terms and Conditions ("Terms Sheet") : Supply of Recycled Water by GVSCCL To RINL's Visakhapatnam Steel PlantR VIJAYACHANDRANo ratings yet

- Principles of Marketing Term Project Module 2Document16 pagesPrinciples of Marketing Term Project Module 2Palize QaziNo ratings yet

- The Battle Over Gambling: Illeg AlDocument4 pagesThe Battle Over Gambling: Illeg AlCatherine SnowNo ratings yet

- Affidavit Diploma SSCDocument2 pagesAffidavit Diploma SSCdaniel jejillosNo ratings yet

- Annual Report 2017 Sree Rayalseema Hi PDFDocument115 pagesAnnual Report 2017 Sree Rayalseema Hi PDFSukhsagar AggarwalNo ratings yet

- ECO121 Group Assignment Report Group 1Document10 pagesECO121 Group Assignment Report Group 1Nhat HuyyNo ratings yet

- Business Plan WS-97 FormatDocument7 pagesBusiness Plan WS-97 FormatSanjay Vyas0% (1)

- Holland Aptitude TestDocument15 pagesHolland Aptitude Testpari talukdarNo ratings yet

- Financial Management: Friday 6 December 2013Document5 pagesFinancial Management: Friday 6 December 2013Nirmal ShresthaNo ratings yet

- PHIL 215 - Final Exam NotesDocument99 pagesPHIL 215 - Final Exam NotesDavidKnightNo ratings yet

- Get Out of The System Letter Pre-Tax CourtDocument14 pagesGet Out of The System Letter Pre-Tax CourtPublic Knowledge100% (9)

- Jesus Sacred Heart College vs. CirDocument2 pagesJesus Sacred Heart College vs. CirMC Quesada100% (2)

- AssignmentDocument5 pagesAssignmentMd. Alif HossainNo ratings yet

- Comparative Analysis 8424 and 10963Document31 pagesComparative Analysis 8424 and 10963Rizza Angela Mangalleno100% (2)