Download as pdf or txt

You might also like

- Singapore Fintech Landscape 2023Document28 pagesSingapore Fintech Landscape 2023tamlqNo ratings yet

- NETFLIX Case Study - FinalDocument21 pagesNETFLIX Case Study - FinalKatherine McLarney93% (15)

- Running Head: Netflix Brand Audit 1Document12 pagesRunning Head: Netflix Brand Audit 1Justin WattsNo ratings yet

- Study Id51495 Smart-CitiesDocument66 pagesStudy Id51495 Smart-CitiesIan TanNo ratings yet

- Netflix Vs Hulu Plus Vs Amazon Prime VideoDocument8 pagesNetflix Vs Hulu Plus Vs Amazon Prime VideoAdnanNo ratings yet

- NetflixDocument4 pagesNetflixArwa Garouachi Ep Abdelkrim100% (1)

- Third Point Letter To Disney October 2020Document5 pagesThird Point Letter To Disney October 2020FOX Business100% (2)

- EMarketer Upfront TV Digital Video Forecasts Trends 2023Document10 pagesEMarketer Upfront TV Digital Video Forecasts Trends 2023KNo ratings yet

- Nielsen+Local+Audience+Insights+Report+ January+2023Document26 pagesNielsen+Local+Audience+Insights+Report+ January+2023nobelaungNo ratings yet

- Panasonic Viera 43 In. TH-43E410X TVDocument16 pagesPanasonic Viera 43 In. TH-43E410X TVRhea NograNo ratings yet

- Consumer Durables Nov2022Document33 pagesConsumer Durables Nov2022Siddhartha RoyNo ratings yet

- EY-Ficci Media and Entertainment Report April22Document5 pagesEY-Ficci Media and Entertainment Report April22AADI SHANKARNo ratings yet

- Tsel2021 AR Webversion FINALDocument162 pagesTsel2021 AR Webversion FINALr dNo ratings yet

- Consumer Durables March 2021Document34 pagesConsumer Durables March 2021Gogol SarinNo ratings yet

- Block Chain Valley DeckDocument26 pagesBlock Chain Valley DeckBlockchain LandNo ratings yet

- Study Id82777 Internet-Advertising-WorldwideDocument56 pagesStudy Id82777 Internet-Advertising-Worldwidekshamamba2324No ratings yet

- Marketing Plan: Demand & Supply Analysis Projected Demand Year of Operation Total Projected DemandDocument5 pagesMarketing Plan: Demand & Supply Analysis Projected Demand Year of Operation Total Projected DemandMaritess MunozNo ratings yet

- Vietnam: EcommerceDocument14 pagesVietnam: EcommerceDIDINo ratings yet

- Atomico SoET First LookDocument19 pagesAtomico SoET First LookMarcus DidiusNo ratings yet

- Consumer Durables: February 2021Document33 pagesConsumer Durables: February 2021Surbhi Thakkar100% (1)

- Impact of SC Ruling To The DILG & LGUsDocument26 pagesImpact of SC Ruling To The DILG & LGUsMarijenLeaño100% (1)

- Prismark Workshop 092021Document100 pagesPrismark Workshop 092021Gibson leeNo ratings yet

- Diagram:calculations - OBUDocument6 pagesDiagram:calculations - OBUkiranNo ratings yet

- Telecom - MA - Update 2019 - vFINALDocument11 pagesTelecom - MA - Update 2019 - vFINALYandhi SuryaNo ratings yet

- US_Ad_Spending_2023Document11 pagesUS_Ad_Spending_2023Test TingNo ratings yet

- M&E Report 2024 - Advertising & Brands 2.1Document13 pagesM&E Report 2024 - Advertising & Brands 2.1Viren ThambidoraiNo ratings yet

- Publications 3182022000 ICT Indicators in Brief August 2022 31082022Document4 pagesPublications 3182022000 ICT Indicators in Brief August 2022 31082022mohegabNo ratings yet

- Pib Real Vs NominalDocument3 pagesPib Real Vs NominalCarol Valentina PARRA LATORRENo ratings yet

- Madan Bohara Marketing PRESENTATION R I1Document22 pagesMadan Bohara Marketing PRESENTATION R I1Navin AcharyaNo ratings yet

- Corporate Presentation 06032023 JP Morgan ConferenceDocument45 pagesCorporate Presentation 06032023 JP Morgan ConferenceJuan Pablo LabraNo ratings yet

- Support FS FatimaDocument64 pagesSupport FS FatimaMarijude NogalNo ratings yet

- Nominal & Real GDP (2003-2022) in Bangladesh Over The YearsDocument2 pagesNominal & Real GDP (2003-2022) in Bangladesh Over The Yearssadia TFNo ratings yet

- Sample Demand Supply AnalysisDocument7 pagesSample Demand Supply AnalysisKathleen Rose Bambico100% (1)

- Global Leaf Manufacturing Company: Bataan Peninsula State UniversityDocument19 pagesGlobal Leaf Manufacturing Company: Bataan Peninsula State Universitymaicah sidonNo ratings yet

- PWC Gto 2023Document20 pagesPWC Gto 2023Manpreet Singh RekhiNo ratings yet

- Radex Electric Co. Forecasting and InvestmentDocument3 pagesRadex Electric Co. Forecasting and InvestmentJacquin MokayaNo ratings yet

- Q1 2022 ColliersQuarterly JakartaDocument28 pagesQ1 2022 ColliersQuarterly Jakartanur mawaddah100% (1)

- 1t Chan Activity2Document14 pages1t Chan Activity2irish chanNo ratings yet

- Managerial Economics-CIA 3Document8 pagesManagerial Economics-CIA 3ABHISHEKA SINGH 2127201No ratings yet

- Global Pay TV ForecastsDocument12 pagesGlobal Pay TV ForecastsVinh LươngNo ratings yet

- DuF2023 En-DataDocument40 pagesDuF2023 En-Datakunaldua.nietNo ratings yet

- Consumer Durables December 2023Document33 pagesConsumer Durables December 2023raghunandhan.cvNo ratings yet

- Demand and Supply Analysis 1Document5 pagesDemand and Supply Analysis 1Casiño B ACNo ratings yet

- Study - Id15889 - Streaming in The Us Statista DossierDocument38 pagesStudy - Id15889 - Streaming in The Us Statista Dossierchng!!No ratings yet

- One PagerDocument1 pageOne PagerTejas KadamNo ratings yet

- How 5G Will Transform The Business of Media & Entertainment: OCTOBER 2018Document19 pagesHow 5G Will Transform The Business of Media & Entertainment: OCTOBER 2018Dương Hồng QuânNo ratings yet

- 2C2P-IDC-InfoBrief AP241267IB Final SmallDocument17 pages2C2P-IDC-InfoBrief AP241267IB Final Smalljefcheung19No ratings yet

- Executive Summary: Click To Add Text Click To Add TextDocument11 pagesExecutive Summary: Click To Add Text Click To Add Textteam5DTCMNo ratings yet

- EY-Ficci Media and Entertainment Report April22 - 2Document3 pagesEY-Ficci Media and Entertainment Report April22 - 2Sargam SinghalNo ratings yet

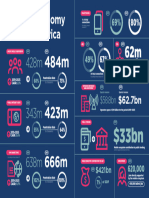

- GSMA MobileEconomy2020 LATAM Infographic EngDocument1 pageGSMA MobileEconomy2020 LATAM Infographic EngDaniel NavarroNo ratings yet

- Over-The-Top Television (OTT)Document17 pagesOver-The-Top Television (OTT)rammanohar22No ratings yet

- Calgary and Region Economic Outlook 2022 Spring ExecutiveSummaryDocument6 pagesCalgary and Region Economic Outlook 2022 Spring ExecutiveSummaryvishalprojects8899No ratings yet

- Corporate Finance MUSHRAFDocument6 pagesCorporate Finance MUSHRAFjilanisayyed16No ratings yet

- Roadmap For A Digitalized Brazil - GSMA 2Document1 pageRoadmap For A Digitalized Brazil - GSMA 2nzeribe loveNo ratings yet

- Thuong ThuongDocument6 pagesThuong ThuongTrần Lê Thanh NhànNo ratings yet

- Demand Supply Analysis TemplatesDocument7 pagesDemand Supply Analysis TemplatesAce Gene ArellanoNo ratings yet

- A Budget ComparisonDocument1 pageA Budget Comparisonnachama_soloveichikNo ratings yet

- AE PetaDocument4 pagesAE PetaAlyanna Patricia EstebanNo ratings yet

- Drones: Industries & MarketsDocument46 pagesDrones: Industries & MarketsXinwei LinNo ratings yet

- EnergyBalance CPDocument3 pagesEnergyBalance CPLiora Vanessa DopacioNo ratings yet

- VII. Market ShareDocument15 pagesVII. Market ShareGiulia TabaraNo ratings yet

- Revise Financial ProposedDocument37 pagesRevise Financial Proposedxavy villegasNo ratings yet

- DE LEON - Activity 1Document6 pagesDE LEON - Activity 1AARON POCHOLO DE LEONNo ratings yet

- Book 1Document3 pagesBook 1riyadh al kamalNo ratings yet

- Unlocking the Potential of Digital Services Trade in Asia and the PacificFrom EverandUnlocking the Potential of Digital Services Trade in Asia and the PacificNo ratings yet

- The Netflix Effect - Impacts of The Streaming Model On Television PDFDocument217 pagesThe Netflix Effect - Impacts of The Streaming Model On Television PDFAjay NigamNo ratings yet

- GlowDocument43 pagesGlowapi-454354651No ratings yet

- Streaming ServicesDocument38 pagesStreaming ServicesUnderMakerNo ratings yet

- Tyson Fury Vs Derek Chisora Live Fox08Document3 pagesTyson Fury Vs Derek Chisora Live Fox08Alex ArifNo ratings yet

- Netflix: A Strategic Analysis of The Red MenaceDocument63 pagesNetflix: A Strategic Analysis of The Red MenaceSam FarhatNo ratings yet

- Sociology IA 2023 Alana AndrewsDocument29 pagesSociology IA 2023 Alana Andrewsalovequeen12No ratings yet

- Watch - Barbie (2023) Fullmovie Free Online On 123moviesDocument6 pagesWatch - Barbie (2023) Fullmovie Free Online On 123moviesshinemargielyn gementizaNo ratings yet

- Millers Girl Stream Online 6Document6 pagesMillers Girl Stream Online 6ffrakeshNo ratings yet

- Merry Christmas Full Onl 31Document5 pagesMerry Christmas Full Onl 31refernubileNo ratings yet

- Disney 1000+ Hits by @exclasev - FileDocument25 pagesDisney 1000+ Hits by @exclasev - FileFelipe MtzNo ratings yet

- Ewc661 - Report - Research On The Impact of Netflix To The Population of Malaysia - G5Document37 pagesEwc661 - Report - Research On The Impact of Netflix To The Population of Malaysia - G5amirahNo ratings yet

- Equity Research Report NetflixDocument34 pagesEquity Research Report Netflixsumit bahugunaNo ratings yet

- Case NetFlixDocument12 pagesCase NetFlixgeniusMAHI67% (3)

- Final Marketing ReportDocument69 pagesFinal Marketing Reportapi-477137876No ratings yet

- HuluDocument9 pagesHuluSAMEER AHMEDNo ratings yet

- Pure Nintendo Magazine #1 - Oct 11Document8 pagesPure Nintendo Magazine #1 - Oct 11Pure NintendoNo ratings yet

- Hanuman Full Onl 30Document5 pagesHanuman Full Onl 30ajitkumary926No ratings yet

- Pom Acquisition AssignmentDocument8 pagesPom Acquisition AssignmentChaitanya ThakkarNo ratings yet

- Imagine Replay Whitepaper LatestDocument37 pagesImagine Replay Whitepaper LatestmbohizzatNo ratings yet

- BCG-Entertainment Goes Online PDFDocument60 pagesBCG-Entertainment Goes Online PDFAayush SinhaNo ratings yet

- TV Competition Nowhere:: How The Cable Industry Is Colluding To Kill Online TVDocument40 pagesTV Competition Nowhere:: How The Cable Industry Is Colluding To Kill Online TVsyudenfrNo ratings yet

- Channel Aggregates Content: How Much of Your Ad Revenue Comes From The Roku Channel?Document4 pagesChannel Aggregates Content: How Much of Your Ad Revenue Comes From The Roku Channel?Tara ShaghafiNo ratings yet

- Hulu 2Document3 pagesHulu 2rubyNo ratings yet

- Efe IfeDocument11 pagesEfe IfeELF JRNo ratings yet

- Situation AnalysisDocument12 pagesSituation AnalysisAnonymous nz9G2R100% (1)