Download as docx, pdf, or txt

You might also like

- Sample Nigerian Employment ContractDocument9 pagesSample Nigerian Employment ContractOna Offiaeli73% (11)

- Hammer Group SeptDec 2023Document5 pagesHammer Group SeptDec 2023Adilah AzamNo ratings yet

- Alice Bianco vs. Lamington Farm ClubDocument74 pagesAlice Bianco vs. Lamington Farm ClubAlexis TarraziNo ratings yet

- QSP-06 Risk AssessmentDocument3 pagesQSP-06 Risk AssessmentHarits As Siddiq100% (1)

- Schedules in Indian ConstitutionDocument4 pagesSchedules in Indian ConstitutionSurya Pratap SinghNo ratings yet

- Mamatha Traders Adjuducation Order Us 73 - CompressedDocument31 pagesMamatha Traders Adjuducation Order Us 73 - Compressedurmilachoudhary1999No ratings yet

- DRC 01 ReplyDocument5 pagesDRC 01 Replyrameshbara.rksNo ratings yet

- Digitally Proceedings of P Hanumantharao & Sons 2018-19 S-73Document31 pagesDigitally Proceedings of P Hanumantharao & Sons 2018-19 S-73CTOAUDIT1 BLYNo ratings yet

- Ram NameDocument2 pagesRam NameStock PsychologistNo ratings yet

- Aino Communique 111th Edition Jan 2023 PDFDocument14 pagesAino Communique 111th Edition Jan 2023 PDFSwathi JainNo ratings yet

- Latest Updation in GSTN PortalDocument47 pagesLatest Updation in GSTN PortalVenkat BalaNo ratings yet

- REPLYDocument4 pagesREPLYVishal DwivediNo ratings yet

- Action For Difference in ITC Between 3B and 2ADocument46 pagesAction For Difference in ITC Between 3B and 2Aphani raja kumarNo ratings yet

- Eturns: This Chapter Will Equip You ToDocument52 pagesEturns: This Chapter Will Equip You ToShowkat MalikNo ratings yet

- GST Audit Amendment Notes by Pankaj GargDocument12 pagesGST Audit Amendment Notes by Pankaj GargGopal Airan100% (2)

- Form GST ASMT - 11 - NNNNNDocument2 pagesForm GST ASMT - 11 - NNNNNGovindNo ratings yet

- Sec 183Document1 pageSec 183goelshubham92No ratings yet

- Eturns: After Studying This Chapter, You Will Be Able ToDocument70 pagesEturns: After Studying This Chapter, You Will Be Able ToChandan ganapathi HcNo ratings yet

- GSTR ReturnDocument136 pagesGSTR Returnyoyorikee0% (1)

- Advisory 2710 2Document20 pagesAdvisory 2710 2Pushpraj SinghNo ratings yet

- GSTV70P4 November 27 December 3 (PG 144) SamplechapterDocument2 pagesGSTV70P4 November 27 December 3 (PG 144) SamplechapterSatyakanth SunkaraNo ratings yet

- Hc-Allows-Errros in ITC Availment in Tax Head - Rectification-Of-Gstr-3b-After-Expiry-Of-Statutory-Time-LimitDocument3 pagesHc-Allows-Errros in ITC Availment in Tax Head - Rectification-Of-Gstr-3b-After-Expiry-Of-Statutory-Time-LimitychichghareNo ratings yet

- Returns in Goods and Services Tax: Section 37-47 of CGST Act, 2017Document73 pagesReturns in Goods and Services Tax: Section 37-47 of CGST Act, 2017Nikhil PahariaNo ratings yet

- Asmt 10 1920Document69 pagesAsmt 10 1920Prashant ZawareNo ratings yet

- GSTR 9 GSTR 9C 1700889649Document33 pagesGSTR 9 GSTR 9C 1700889649Jayant JoshiNo ratings yet

- TaxesDocument2 pagesTaxesRameshNadarNo ratings yet

- Returns: FAQ'sDocument25 pagesReturns: FAQ'smun1barejaNo ratings yet

- Faqs On New GST Retu Rns FormsDocument14 pagesFaqs On New GST Retu Rns FormsFizo KjNo ratings yet

- 74824bos60500 cp15Document90 pages74824bos60500 cp15soni12c2004No ratings yet

- Aino Communique Mar 23 113th EditionDocument13 pagesAino Communique Mar 23 113th EditionSwathi JainNo ratings yet

- LetterDocument2 pagesLetterP.KANNANNo ratings yet

- GST LatestAmendments Issues 01072023Document85 pagesGST LatestAmendments Issues 01072023Selvakumar MuthurajNo ratings yet

- Draft - GST Audit Report - DS ASSAMDocument35 pagesDraft - GST Audit Report - DS ASSAMSUNIL YADAVNo ratings yet

- Attachment 1Document2 pagesAttachment 1khabrilaalNo ratings yet

- Patanjali Arogya Kendra 2018-19Document5 pagesPatanjali Arogya Kendra 2018-19tuensangnagaland2018No ratings yet

- DRAFT REPLY GST ITC IN GSTR-3B VS 2ADocument5 pagesDRAFT REPLY GST ITC IN GSTR-3B VS 2ARajeev RanjanNo ratings yet

- Form GST ASMT 11 - Clyde BergemannDocument5 pagesForm GST ASMT 11 - Clyde BergemannektaNo ratings yet

- GSTR 9 9A CA Mohit SinghalDocument61 pagesGSTR 9 9A CA Mohit SinghalRishav AnandNo ratings yet

- GSTR 9 9C FY 22 23 DUE 31st December 2023 1694345252Document7 pagesGSTR 9 9C FY 22 23 DUE 31st December 2023 1694345252RajatNo ratings yet

- Nation: MarketDocument9 pagesNation: MarketDebashis MitraNo ratings yet

- Annual Return - Salem BranchDocument23 pagesAnnual Return - Salem BranchSureshkumarNo ratings yet

- Circular Refund 142 11 2020Document3 pagesCircular Refund 142 11 2020Gulrana AlamNo ratings yet

- Record Notebook Faculty of Arts & Commerce Department of Cost & Management Accounting (Cma)Document16 pagesRecord Notebook Faculty of Arts & Commerce Department of Cost & Management Accounting (Cma)Sha dowNo ratings yet

- All About Electronic Credit Reversal N Re-Claimed Statement - CA Swapnil MunotDocument4 pagesAll About Electronic Credit Reversal N Re-Claimed Statement - CA Swapnil MunotkevadiyashreyaNo ratings yet

- GST Automated NoticesDocument6 pagesGST Automated NoticesMaunik ParikhNo ratings yet

- 168_36ABUPT4818Q3ZE_VEERASWAMY_THEGULLA_FY_18_19Document7 pages168_36ABUPT4818Q3ZE_VEERASWAMY_THEGULLA_FY_18_19funny todaysNo ratings yet

- Sri Chowdeshwari Rice TradersDocument2 pagesSri Chowdeshwari Rice Tradershemanth1234No ratings yet

- Study Material of TaxationDocument4 pagesStudy Material of TaxationAishuNo ratings yet

- GSTDocument40 pagesGSTsangkhawmaNo ratings yet

- Circular No. 57/31/2018 GST Dated 04.09.2018Document17 pagesCircular No. 57/31/2018 GST Dated 04.09.2018RAJARAJESHWARI M GNo ratings yet

- Template For PresentationDocument9 pagesTemplate For PresentationTheodorus RiadyNo ratings yet

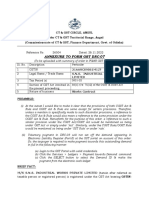

- Annexure To Form GST Drc-07: 21AAVCS9861M1ZF S.N.S. Industrial Works Private LimitedDocument5 pagesAnnexure To Form GST Drc-07: 21AAVCS9861M1ZF S.N.S. Industrial Works Private LimitedBiswajit MishraNo ratings yet

- Tax Law - Penal ProvisionsDocument23 pagesTax Law - Penal ProvisionsArsalan Ahmad100% (1)

- Taxguru - in-gSTR 9C Reconciliation Statement - A Detailed AnalysisDocument4 pagesTaxguru - in-gSTR 9C Reconciliation Statement - A Detailed Analysisavinayak675No ratings yet

- Amendment Booklet NOV 21 - by CA Yachaa Mutha BhuratDocument46 pagesAmendment Booklet NOV 21 - by CA Yachaa Mutha BhuratSuraj BijlaniNo ratings yet

- Returns GSTDocument25 pagesReturns GSTRahul RockzzNo ratings yet

- Audit Under Fiscal Laws GST AuditDocument4 pagesAudit Under Fiscal Laws GST AuditRanjit BhogesaraNo ratings yet

- GST Healthcheck Sample Report v1Document148 pagesGST Healthcheck Sample Report v1Gauravkumar KateNo ratings yet

- FORM GSTR-2B - Advisory (Available Under "Advisory" Tab of GSTR-2B) Terms UsedDocument4 pagesFORM GSTR-2B - Advisory (Available Under "Advisory" Tab of GSTR-2B) Terms UsedSachin KNNo ratings yet

- DR - MGR E & RI - Chennai - 28.05.2021-1Document21 pagesDR - MGR E & RI - Chennai - 28.05.2021-1Sha dowNo ratings yet

- Circular CGST 193Document4 pagesCircular CGST 193Jaipur-B Gr-2No ratings yet

- GSTR 9Document24 pagesGSTR 9Pushpraj SinghNo ratings yet

- GST Audit and Annual ReturnDocument15 pagesGST Audit and Annual Returnyogeshaggarwal09No ratings yet

- ReturnsDocument12 pagesReturnsPriya DasNo ratings yet

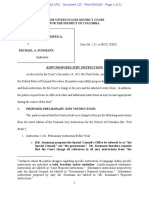

- Durham Watch: US V Sussmann Doc 125Document21 pagesDurham Watch: US V Sussmann Doc 125FightWithKashNo ratings yet

- 61-36 Epic's Proposed Order of PI Against AppleDocument3 pages61-36 Epic's Proposed Order of PI Against AppleFlorian MuellerNo ratings yet

- DLR Vol. XXXV (2019-20)Document240 pagesDLR Vol. XXXV (2019-20)MahimeshNo ratings yet

- UAE Visa Information - Visa and Passport - Before You Fly - Emirates PakistanDocument14 pagesUAE Visa Information - Visa and Passport - Before You Fly - Emirates Pakistannaina khanNo ratings yet

- CA Foundation Business Law Suggested Answers Dec 2020Document11 pagesCA Foundation Business Law Suggested Answers Dec 2020M.K Tech100% (3)

- Application FormDocument5 pagesApplication FormSaurav BansalNo ratings yet

- Authorized Capital StockDocument3 pagesAuthorized Capital Stockkero keropiNo ratings yet

- Pacaro AffidavitDocument3 pagesPacaro AffidavitSan Miguel MpsNo ratings yet

- The Visakhapatnam Cooperative Central Stores Limited.: To Whom Soever It May ConcernDocument1 pageThe Visakhapatnam Cooperative Central Stores Limited.: To Whom Soever It May ConcernGanti Santosh KumarNo ratings yet

- SME Bank, Inc. vs. de Guzman, G.R. No. 186641Document3 pagesSME Bank, Inc. vs. de Guzman, G.R. No. 186641Jerickson A. ReyesNo ratings yet

- 4 Kinds of Defective ContractsDocument2 pages4 Kinds of Defective ContractsAndrea Ellis69% (13)

- DINGRAS Manuscript11111Document23 pagesDINGRAS Manuscript11111Ncip Ilocos NorteNo ratings yet

- Equity - Trusts-1Document79 pagesEquity - Trusts-1denyohsylvesterNo ratings yet

- Discharge VoucherDocument1 pageDischarge VoucherAnonymous S0H8cqgnfiNo ratings yet

- Vic Mignogna Monica Rial, Jamie Marchi, Ron Toye, Funimation Memorandum OpinionDocument70 pagesVic Mignogna Monica Rial, Jamie Marchi, Ron Toye, Funimation Memorandum OpinionBICRNo ratings yet

- Articles of IncorporationDocument15 pagesArticles of IncorporationDGDelfinNo ratings yet

- Minutes Dec 02 2022 UpdatedDocument4 pagesMinutes Dec 02 2022 UpdatedRaquel dg.Bulaong100% (1)

- Policy New Cheque Dishonour LATESTDocument18 pagesPolicy New Cheque Dishonour LATESTAdam MarakNo ratings yet

- PostScanMail - IntlCustomerVerificationDocument2 pagesPostScanMail - IntlCustomerVerificationychocmNo ratings yet

- Letter of Placing An OrderDocument10 pagesLetter of Placing An OrderArnav SinghalNo ratings yet

- Datius Didace Law of TortsDocument39 pagesDatius Didace Law of TortsKamran RasoolNo ratings yet

- In Re Basa PDFDocument2 pagesIn Re Basa PDFEmma Ruby Aguilar-ApradoNo ratings yet

- Important Notice For Online VerificationDocument3 pagesImportant Notice For Online VerificationMithun GoudaNo ratings yet

- State Grants 21Document78 pagesState Grants 21Wmar WebNo ratings yet

- Civics Model Exam AbuneDocument19 pagesCivics Model Exam AbuneAdenach BelkawNo ratings yet