Download as pdf or txt

You might also like

- Company Law-II ProjectDocument22 pagesCompany Law-II ProjectAbhinavParasharNo ratings yet

- Judgments For ReadingDocument6 pagesJudgments For ReadingjamuarsanketNo ratings yet

- EBEBE4Document6 pagesEBEBE4Porus GhurdeNo ratings yet

- Company Law ProjectDocument19 pagesCompany Law ProjectSanjiv GuptaNo ratings yet

- Mr.Ravi Sankar Deverakonda v. CoCDocument4 pagesMr.Ravi Sankar Deverakonda v. CoCNishi AgrawalNo ratings yet

- J 2023 SCC OnLine Del 437 2023 455 ITR 139 22309806773 Clcduacin 20240416 190605 1 6Document6 pagesJ 2023 SCC OnLine Del 437 2023 455 ITR 139 22309806773 Clcduacin 20240416 190605 1 622309806773No ratings yet

- CompiledDocument17 pagesCompiledMeghna SinghNo ratings yet

- Meena Anand Suryadutt Bhatt v. Union of India, 2022 SCC OnLine Bom 1505Document7 pagesMeena Anand Suryadutt Bhatt v. Union of India, 2022 SCC OnLine Bom 1505Zalak ModyNo ratings yet

- Case BriefsDocument4 pagesCase BriefsAparajita MarwahNo ratings yet

- Shah Brothers CaseDocument2 pagesShah Brothers CaseAkshara RajratnamNo ratings yet

- Insolvency Law in Review - February 2021Document23 pagesInsolvency Law in Review - February 2021Abhishek MishraNo ratings yet

- 2008 SCC Online Del 1593: (2008) 4 BC 514 in The High Court of DelhiDocument3 pages2008 SCC Online Del 1593: (2008) 4 BC 514 in The High Court of Delhirohit mewaraNo ratings yet

- Article On Debt Recovery Tribunal - FinalDocument6 pagesArticle On Debt Recovery Tribunal - Finalvasantharao venkataraoNo ratings yet

- Duties of BaileeDocument10 pagesDuties of Baileepranitaprakash138No ratings yet

- Insolvency & Bankruptcy-1 Act Business LawsDocument5 pagesInsolvency & Bankruptcy-1 Act Business LawsDango GamerNo ratings yet

- Lotus Three Dev. V Axis BankDocument3 pagesLotus Three Dev. V Axis Bankraghuvansh mishraNo ratings yet

- Versus: Efore Hakravartti AND AhiriDocument16 pagesVersus: Efore Hakravartti AND AhiriVanshika GuptaNo ratings yet

- Swiss RibbonsDocument21 pagesSwiss Ribbonsnitin kashyapNo ratings yet

- Insider Trading Regulations, 2015 - Doomed To FailureDocument8 pagesInsider Trading Regulations, 2015 - Doomed To FailureAlina SujithNo ratings yet

- Mergers Amp Acquisitions Comparative GuideDocument60 pagesMergers Amp Acquisitions Comparative Guidejagano7735No ratings yet

- J 1971 SCC OnLine Del 51 ILR 1971 1 Del 149Document14 pagesJ 1971 SCC OnLine Del 51 ILR 1971 1 Del 149Aadya AmbasthaNo ratings yet

- SSRN 4429865Document12 pagesSSRN 4429865shianasareen8No ratings yet

- J 2014 SCC OnLine Ker 1984 2014 363 ITR 81 Meghanaranip Dsnluacin 20220304 113850 1 12Document12 pagesJ 2014 SCC OnLine Ker 1984 2014 363 ITR 81 Meghanaranip Dsnluacin 20220304 113850 1 12P TejeswariNo ratings yet

- Merger and Demerger of CompaniesDocument11 pagesMerger and Demerger of CompaniesSujan Ganesh100% (1)

- Pre-Incorporation ContractsDocument18 pagesPre-Incorporation Contractsrochishnu387No ratings yet

- NV Investment Holdings LLC v. Future Retail Limited, 2021 SCC OnLine SC 557Document45 pagesNV Investment Holdings LLC v. Future Retail Limited, 2021 SCC OnLine SC 557abhisek kaushalNo ratings yet

- Jindal Global Law School Insolvency Law Working Paper SeriesDocument20 pagesJindal Global Law School Insolvency Law Working Paper SeriesyashNo ratings yet

- IBC and Companies ActDocument4 pagesIBC and Companies ActYashika patniNo ratings yet

- Ram Kohli vs. Indrama Investment PVT LTD Select 16 May, 2013Document7 pagesRam Kohli vs. Indrama Investment PVT LTD Select 16 May, 2013Harshit JoshiNo ratings yet

- PREPDocument8 pagesPREPBalapragatha MoorthyNo ratings yet

- Lalit Kumar Jain VsDocument5 pagesLalit Kumar Jain VsGautam PareekNo ratings yet

- Letter of OfferDocument40 pagesLetter of OfferANAPARTI NaveenNo ratings yet

- University of Petroleum & Energy Studies School of Law: B.A.LLB (HONS.)Document7 pagesUniversity of Petroleum & Energy Studies School of Law: B.A.LLB (HONS.)priyanka_kajlaNo ratings yet

- Article On IBc Boon or BaneDocument6 pagesArticle On IBc Boon or BaneJeevan LancyNo ratings yet

- CMA Final Law Super 30 - Dec 2023Document23 pagesCMA Final Law Super 30 - Dec 2023rehanrahman88896No ratings yet

- Uganda Stock Exchange Market ListingDocument10 pagesUganda Stock Exchange Market Listingdamasmart841No ratings yet

- IBC Cases SummaryDocument7 pagesIBC Cases SummaryChristina ShajuNo ratings yet

- 18BBL012 - Final SubmissionDocument10 pages18BBL012 - Final SubmissionGahna RajaniNo ratings yet

- J 2022 SCC OnLine Blog Exp 81Document8 pagesJ 2022 SCC OnLine Blog Exp 81JonNo ratings yet

- SEBI CaseDocument33 pagesSEBI CaseResearch SubhamNo ratings yet

- Fasttrack MRGRDocument13 pagesFasttrack MRGRbhavna khatwaniNo ratings yet

- Wittur CaseDocument5 pagesWittur Caseprarthana rameshNo ratings yet

- Jaipur Trade Expocentre Pvt. Ltd. NCLATDocument9 pagesJaipur Trade Expocentre Pvt. Ltd. NCLATSachika VijNo ratings yet

- Fast Track Merger Under The Companies Act 2013 IntDocument8 pagesFast Track Merger Under The Companies Act 2013 IntAayush BhardwajNo ratings yet

- Real Time Interactive Media Pvt. ... Vs Metro Mumbai Infradeveloper VTDocument6 pagesReal Time Interactive Media Pvt. ... Vs Metro Mumbai Infradeveloper VTBENE FACTORNo ratings yet

- Recovery of Debts Due To Banks and Financial InstitutionsDocument7 pagesRecovery of Debts Due To Banks and Financial InstitutionsLakhbir BrarNo ratings yet

- J_2011_SCC_OnLine_Del_1212_2011_178_DLT_569_2011_104_himanshumishralaw1_gmailcom_20240703_085615_1_11Document11 pagesJ_2011_SCC_OnLine_Del_1212_2011_178_DLT_569_2011_104_himanshumishralaw1_gmailcom_20240703_085615_1_11himanshu.mishra.law1No ratings yet

- Judgement Writing For MootDocument4 pagesJudgement Writing For MootNANCY SAJEEVANNo ratings yet

- J 2020 SCC OnLine Blog OpEd 75 Cabhishekllb18 Lawallianceeduin 20220815 190433 1 5Document5 pagesJ 2020 SCC OnLine Blog OpEd 75 Cabhishekllb18 Lawallianceeduin 20220815 190433 1 5Abhishek CharanNo ratings yet

- Vardhman Developers LTD Vs Borla Co-OperativeDocument15 pagesVardhman Developers LTD Vs Borla Co-Operativevineet jainNo ratings yet

- Salient Points of The Revised Corporation CodeDocument23 pagesSalient Points of The Revised Corporation Codencq6dmzmp4No ratings yet

- Insolvency and Bankruptcy CodeDocument3 pagesInsolvency and Bankruptcy CodeKunwarbir Singh lohatNo ratings yet

- COmpany LAw-1Document11 pagesCOmpany LAw-1Suruchi SinghNo ratings yet

- IBBI (Pre-Packaged Insolvency Resolution Process) Regulations, 2021 - Taxguru - inDocument60 pagesIBBI (Pre-Packaged Insolvency Resolution Process) Regulations, 2021 - Taxguru - inPrakalathan BatheyNo ratings yet

- Insolvency and Bankruptcy Code 2016Document4 pagesInsolvency and Bankruptcy Code 2016Tanima SoodNo ratings yet

- J 2017 SCC OnLine NCLAT 63 Shreya14 Nluassamacin 20230215 130923 1 4Document4 pagesJ 2017 SCC OnLine NCLAT 63 Shreya14 Nluassamacin 20230215 130923 1 4Shreya KumarNo ratings yet

- Best Enterprises v. S. Elanchizian, 2006 SCC OnLine Mad 338Document3 pagesBest Enterprises v. S. Elanchizian, 2006 SCC OnLine Mad 338SanjanaNo ratings yet

- Poppatlal v. State of MadrasDocument5 pagesPoppatlal v. State of Madrasriya psNo ratings yet

- Company Law II ProjectDocument21 pagesCompany Law II ProjectBhawna JoshiNo ratings yet

- An Overview of Compulsory Strata Management Law in NSW: Michael Pobi, Pobi LawyersFrom EverandAn Overview of Compulsory Strata Management Law in NSW: Michael Pobi, Pobi LawyersNo ratings yet

- WLDoc 15-8-01 10 - 19 (PM)Document115 pagesWLDoc 15-8-01 10 - 19 (PM)Varun PaiNo ratings yet

- Dissolution of A CompanyDocument4 pagesDissolution of A CompanyRazman RuzaimiNo ratings yet

- Velayo V Shell Co of The PhilsDocument3 pagesVelayo V Shell Co of The PhilsistefifayNo ratings yet

- Insolvency and Bankruptcy CodeDocument13 pagesInsolvency and Bankruptcy CodeMishika PanditaNo ratings yet

- NotesDocument9 pagesNotesErika GuillermoNo ratings yet

- Company Law Revision Full NoteDocument130 pagesCompany Law Revision Full NoteChip choiNo ratings yet

- NCLT Mumbai Order - CP (IB) - 1882:MB:2018Document15 pagesNCLT Mumbai Order - CP (IB) - 1882:MB:2018Pival K. PeddireddiNo ratings yet

- Business Law Module No. 2Document10 pagesBusiness Law Module No. 2Yolly DiazNo ratings yet

- Incoming and Outgoing PartnersDocument39 pagesIncoming and Outgoing PartnersYatharth KohliNo ratings yet

- Problem Solving - Lump-Sum LiquidationDocument8 pagesProblem Solving - Lump-Sum Liquidationchxrlttx100% (2)

- Module 4 PARTNERSHIP LiquidationFEB 2021Document53 pagesModule 4 PARTNERSHIP LiquidationFEB 2021Grace RoqueNo ratings yet

- A Primer On Us Bankruptcy - StroockDocument247 pagesA Primer On Us Bankruptcy - Stroock83jjmack100% (1)

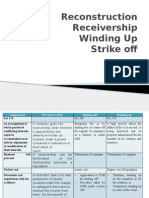

- Reconstruction Receivership Winding Up Strike OffDocument71 pagesReconstruction Receivership Winding Up Strike OffMohammad Hasrul AkmalNo ratings yet

- Documents Provided by Bryan Calvo Against Dariel Fernandez in Miami-Dade Tax Collector's Race, 2024Document1 pageDocuments Provided by Bryan Calvo Against Dariel Fernandez in Miami-Dade Tax Collector's Race, 2024Political CortaditoNo ratings yet

- Business Law Chpater 1-10Document17 pagesBusiness Law Chpater 1-10Richie GulayNo ratings yet

- Hernandez V Rural BankDocument4 pagesHernandez V Rural BankKaira CarlosNo ratings yet

- Priority As Pathology The Pari Passu MythDocument42 pagesPriority As Pathology The Pari Passu Mythabshawn23No ratings yet

- PACIFIC ACE FINANCE LTD. (PAFIN) v. EIJI YANAGISAWADocument17 pagesPACIFIC ACE FINANCE LTD. (PAFIN) v. EIJI YANAGISAWAAnne ObnamiaNo ratings yet

- CPC ProjectDocument19 pagesCPC ProjectYoYoAviNo ratings yet

- E-Commerce ActDocument18 pagesE-Commerce Actcherry blossomNo ratings yet

- Course: Advanced Accounting: Chapter 2: Partnership Liquidation and IncorporationDocument4 pagesCourse: Advanced Accounting: Chapter 2: Partnership Liquidation and Incorporationmohamed dahir AbdirahmaanNo ratings yet

- Pension Provision in Germany - The First and Second Pillars in FocusDocument6 pagesPension Provision in Germany - The First and Second Pillars in FocuspensiontalkNo ratings yet

- Banking Assignment OnDocument10 pagesBanking Assignment OnGursimran SinghNo ratings yet

- Philippine Civil Code Articles No. 1193-1208Document9 pagesPhilippine Civil Code Articles No. 1193-1208Kuma MineNo ratings yet

- ACTBFAR - Exercise Set #3Document6 pagesACTBFAR - Exercise Set #3Cha PampolinaNo ratings yet

- CH 14 Company LawDocument22 pagesCH 14 Company Lawrishita mittalNo ratings yet

- Voluntary Winding UpDocument12 pagesVoluntary Winding UpAinun Sailah Binti NordinNo ratings yet

- Parcor Prelims Reviewer QuestionsDocument6 pagesParcor Prelims Reviewer QuestionsCHARLIZE MONTONNo ratings yet

- Lia4009 - BR006 - Maklumat KursusDocument4 pagesLia4009 - BR006 - Maklumat KursusAbelNo ratings yet

- Ques Bank Sanidhiya Saraf 65d20a6f 75d2 4add 9db2 Ce3e0e036cfdDocument17 pagesQues Bank Sanidhiya Saraf 65d20a6f 75d2 4add 9db2 Ce3e0e036cfdAnil SomraNo ratings yet