Download as pdf or txt

You might also like

- Julia Feldman - 3. INTERACTIVE - Navigate Your Online Bank AccountDocument4 pagesJulia Feldman - 3. INTERACTIVE - Navigate Your Online Bank AccountJulia Feldman69% (13)

- Australia Commonwealth Bank StatementDocument2 pagesAustralia Commonwealth Bank StatementЮлия П100% (2)

- Your Bofa Core CheckingDocument3 pagesYour Bofa Core Checkingxxalias50% (2)

- IF1 LegalDocument278 pagesIF1 Legalkhadeejah AbdulNo ratings yet

- Anz Access Advantage Statement: Welcome To Your Anz Account at A GlanceDocument5 pagesAnz Access Advantage Statement: Welcome To Your Anz Account at A GlanceNadiia Avetisian100% (1)

- Gold Account: Your Account Arranged Overdraft Limit 250.00Document6 pagesGold Account: Your Account Arranged Overdraft Limit 250.00Shaziia Ali100% (2)

- Hippo HO3 BookletDocument9 pagesHippo HO3 BookletPratyush KshirsagarNo ratings yet

- Your Adv Plus Banking: Account SummaryDocument6 pagesYour Adv Plus Banking: Account SummaryЮлия ПNo ratings yet

- Nrma Business PolicyDocument104 pagesNrma Business PolicyAnon BoletusNo ratings yet

- Singapore Bank and Branch Codes - AchcodeDocument20 pagesSingapore Bank and Branch Codes - Achcodedinesh_s_17No ratings yet

- User Manual: Intellect Core Banking System (CBS)Document50 pagesUser Manual: Intellect Core Banking System (CBS)tempo100% (5)

- Qic Home All Risks Insurance PolicyDocument32 pagesQic Home All Risks Insurance PolicyZainab GhaniNo ratings yet

- RSA Home Booklet Terms & ConditionsDocument36 pagesRSA Home Booklet Terms & ConditionsZainab GhaniNo ratings yet

- All Risks Insurance PolicyDocument33 pagesAll Risks Insurance PolicyZainab GhaniNo ratings yet

- Home Insurance Policy BookletDocument25 pagesHome Insurance Policy BookletClintonDestinyNo ratings yet

- Extra PBDocument76 pagesExtra PBAna-Maria EsanuNo ratings yet

- P1PZ 10754543 24829572Document11 pagesP1PZ 10754543 24829572Virginia perezNo ratings yet

- Protect IT ADT PDS-FSG (The School Locker)Document11 pagesProtect IT ADT PDS-FSG (The School Locker)charlieNo ratings yet

- Aussie Top Home Contents Insurance PDSDocument44 pagesAussie Top Home Contents Insurance PDSourpatchNo ratings yet

- 12 Homeinsurance-Policy-Form-June2017Document63 pages12 Homeinsurance-Policy-Form-June2017fichelNo ratings yet

- 1 Form RP Lease Agreement Flat Rate Utilities Lease 9 1 2023 To 8 31 2024Document11 pages1 Form RP Lease Agreement Flat Rate Utilities Lease 9 1 2023 To 8 31 2024Benjamin Ruiz San JuanNo ratings yet

- KEY Features.: Home Insurance ExtraDocument20 pagesKEY Features.: Home Insurance ExtraAna-Maria EsanuNo ratings yet

- 2012 Home Depot Appliance WarrantyDocument6 pages2012 Home Depot Appliance Warrantywps013No ratings yet

- Admiral Insurance CoverDocument72 pagesAdmiral Insurance CoverhenryNo ratings yet

- Home Insurance Policy Wording Insurance Home nhdhg6080 v35 012017 140617Document36 pagesHome Insurance Policy Wording Insurance Home nhdhg6080 v35 012017 140617Abdullateef ToluNo ratings yet

- Musical Insurance: Insurance Product Information DocumentDocument2 pagesMusical Insurance: Insurance Product Information DocumentEphraimNo ratings yet

- Type: Residential Bedrooms: 4 Baths: 3 Living Area: 2300 +/-Square Ft. Lot Size: 3 +/ - Acres Price: $175,000Document7 pagesType: Residential Bedrooms: 4 Baths: 3 Living Area: 2300 +/-Square Ft. Lot Size: 3 +/ - Acres Price: $175,000Olivia StovallNo ratings yet

- 1.1. FIRE & Special PerilsDocument24 pages1.1. FIRE & Special PerilsfirewNo ratings yet

- Fire Insurance - ResidentialDocument3 pagesFire Insurance - ResidentialchenghaocchNo ratings yet

- To Report A Claim, Call:: ImportantDocument37 pagesTo Report A Claim, Call:: ImportantruralfincaNo ratings yet

- Enc Fltres Gty00469 03547315 10 FLT F0938174 00001 T405 06cjak Post 1Document22 pagesEnc Fltres Gty00469 03547315 10 FLT F0938174 00001 T405 06cjak Post 1NORZILA BINTI ABDULLAH KPM-GuruNo ratings yet

- 12 Months Contract 16Document6 pages12 Months Contract 16William JamesonNo ratings yet

- Home Contents Insurance PDS - 25 Apr 2020 1Document51 pagesHome Contents Insurance PDS - 25 Apr 2020 1thesowhatNo ratings yet

- Burglary InsuranceDocument3 pagesBurglary InsuranceAshish3143No ratings yet

- AXA Flats PolicyDocument32 pagesAXA Flats PolicymantiheadNo ratings yet

- Key Facts Home Building Policy CurrentDocument2 pagesKey Facts Home Building Policy CurrentMahil PathiranaNo ratings yet

- Master Insurance PolicyDocument4 pagesMaster Insurance PolicyLaura MayNo ratings yet

- Service & Replace Non-ADHDocument2 pagesService & Replace Non-ADHariel_droletNo ratings yet

- What To Do After A Fire in A CompanyDocument17 pagesWhat To Do After A Fire in A CompanyScribdTranslationsNo ratings yet

- Professional Indemnity Insurance For General Professionals: Summary of CoverDocument4 pagesProfessional Indemnity Insurance For General Professionals: Summary of CoverTriumph OkojieNo ratings yet

- SAVE 20%: Jewellery & Watch CareDocument2 pagesSAVE 20%: Jewellery & Watch CareJudyNo ratings yet

- ST TH TH, THDocument23 pagesST TH TH, THAshok SheodassNo ratings yet

- Household Insurance Policy Document Ergo: Underwritten byDocument50 pagesHousehold Insurance Policy Document Ergo: Underwritten byAlfredo StaraceNo ratings yet

- Fire Insurance - Product Disclosure SheetDocument2 pagesFire Insurance - Product Disclosure SheetchenghaocchNo ratings yet

- LLA 001 007 Guide To Your Landlord Insurance CoverDocument68 pagesLLA 001 007 Guide To Your Landlord Insurance CoverDhar RakulNo ratings yet

- Caravan Touring QUESTTOURINGEU Policy WordingDocument15 pagesCaravan Touring QUESTTOURINGEU Policy Wordingkonrad whiteleyNo ratings yet

- Home Emergency CoverDocument10 pagesHome Emergency Coverapi-269946717No ratings yet

- Duuo - Tenant - Policy - TLL CAD 002 EN MAR 16 2020Document56 pagesDuuo - Tenant - Policy - TLL CAD 002 EN MAR 16 2020DocNo ratings yet

- Policy WordingsDocument24 pagesPolicy WordingsAnonymous KOjlzDNo ratings yet

- Property Owners Adjustment Policy From Aviva PDFDocument13 pagesProperty Owners Adjustment Policy From Aviva PDFSamuelChanNo ratings yet

- XCoverTnC_3NQDN-8TKB6-INSDocument6 pagesXCoverTnC_3NQDN-8TKB6-INSadityaraj676768No ratings yet

- Plan Name Plan Reference Purchase Date Plan Number: 111-184238 Pure Promise 5 Year $800 & Under August 23, 2019 27778Document4 pagesPlan Name Plan Reference Purchase Date Plan Number: 111-184238 Pure Promise 5 Year $800 & Under August 23, 2019 27778jane pascalNo ratings yet

- Insurance.: Protection For Your Home and CarDocument20 pagesInsurance.: Protection For Your Home and CarOsprey SkeerNo ratings yet

- Quote Hippo 2021 05 25Document3 pagesQuote Hippo 2021 05 25usxqqvjzunlnoiiswsNo ratings yet

- Warranties Liabilities Patents Bids and InsuranceDocument39 pagesWarranties Liabilities Patents Bids and InsuranceIVAN JOHN BITONNo ratings yet

- 01 - Home Finance BookletDocument72 pages01 - Home Finance BookletWeedrowNo ratings yet

- GCS Instant Issue - Key Facts For Flat - Maisonette Indemnity (MI)Document1 pageGCS Instant Issue - Key Facts For Flat - Maisonette Indemnity (MI)krisukNo ratings yet

- Pds BuildingDocument60 pagesPds BuildingJohnNo ratings yet

- Property Insurance HandbookDocument12 pagesProperty Insurance HandbookPriyanka TiwariNo ratings yet

- Iq Student Accommodation Endsleigh Insurance 2014-15Document3 pagesIq Student Accommodation Endsleigh Insurance 2014-15iQuniaccommodationNo ratings yet

- Policy Summary - OCTOBER 2021Document6 pagesPolicy Summary - OCTOBER 2021RichardNo ratings yet

- Fire InsuranceDocument21 pagesFire InsuranceJaime DaliuagNo ratings yet

- Aviation Fuelling Liability PdsDocument3 pagesAviation Fuelling Liability PdsNoraini Mohd Shariff100% (1)

- 1003 Info Setting Up Managing Your RentalDocument10 pages1003 Info Setting Up Managing Your RentalTnem NatNo ratings yet

- Alpha Terms of Business 01-04-18Document2 pagesAlpha Terms of Business 01-04-18Liam BakerNo ratings yet

- Policy Booklet Jun23Document44 pagesPolicy Booklet Jun23racheleandchapmanNo ratings yet

- Menards Extended Protection Plan BrochureDocument4 pagesMenards Extended Protection Plan BrochureGreg JohnsonNo ratings yet

- Insurance Property Insurance Personal PropertyDocument19 pagesInsurance Property Insurance Personal Propertybonat07No ratings yet

- Vancouver Law CourtsDocument2 pagesVancouver Law CourtsLcarowanNo ratings yet

- Accounting 2 - 4rd ModuleDocument4 pagesAccounting 2 - 4rd ModuleJessalyn Sarmiento TancioNo ratings yet

- Miss Juliet September Statement... 2022Document6 pagesMiss Juliet September Statement... 2022adilNo ratings yet

- Result (Phase-I) To Be Displayed On WebsiteDocument14 pagesResult (Phase-I) To Be Displayed On Websiteneekuj malikNo ratings yet

- Uco Bank PDFDocument3 pagesUco Bank PDFAshish kumarNo ratings yet

- Statement of Account: Transaction Date Description Debit Credit Available BalanceDocument5 pagesStatement of Account: Transaction Date Description Debit Credit Available Balancekenshin uraharaNo ratings yet

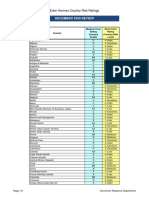

- December 2020 Review: Euler Hermes Country Risk RatingsDocument5 pagesDecember 2020 Review: Euler Hermes Country Risk RatingsLFNo ratings yet

- Nathaniel Enoch Cox - 71840000001639132Document3 pagesNathaniel Enoch Cox - 71840000001639132Steven Lee0% (1)

- Statement 17-MAY-23 AC 83684369 19041511Document6 pagesStatement 17-MAY-23 AC 83684369 19041511Larisa BalintNo ratings yet

- Your Barclays Bank Account StatementDocument1 pageYour Barclays Bank Account StatementНазарій ТершівськийNo ratings yet

- Intermediate Accounting - Quiz No. 2Document3 pagesIntermediate Accounting - Quiz No. 2Rejie AndoNo ratings yet

- Barclays BankDocument4 pagesBarclays BanktsundereadamsNo ratings yet

- Brown Label & White Label ATMsDocument2 pagesBrown Label & White Label ATMsSwastik Nandy100% (1)

- NBS Bank Statement Sep 2023Document2 pagesNBS Bank Statement Sep 2023Eric CartmanNo ratings yet

- OpTransactionHistory11 10 2021Document2 pagesOpTransactionHistory11 10 2021X HureNo ratings yet

- How To Pay AbroadDocument17 pagesHow To Pay AbroadApril Tamondong0% (1)

- Banks and Merchants List PDFDocument1 pageBanks and Merchants List PDFJoseph NovillaNo ratings yet

- Coduri IBANDocument1 pageCoduri IBANIlieșDoraNo ratings yet

- Causelist22024 01 11Document28 pagesCauselist22024 01 11Kamal NaraniyaNo ratings yet

- 4ME Brochure Update V2657Document12 pages4ME Brochure Update V2657ElijahNo ratings yet

- 2branch Cashier Training Manual 1.6Document21 pages2branch Cashier Training Manual 1.6Ashenafi GirmaNo ratings yet