Download as pdf or txt

You might also like

- Tantra - Shree - Meru-Tantram PDFDocument60 pagesTantra - Shree - Meru-Tantram PDFTantra Path77% (73)

- Aakaasa Bhairava TantramDocument56 pagesAakaasa Bhairava Tantramkiran_kandru86% (7)

- 1208 ManualDocument33 pages1208 Manualmg victorNo ratings yet

- Pocket Manual On The Art of History TakingDocument89 pagesPocket Manual On The Art of History TakingAkwu Akwu100% (1)

- Mesa Dew Poin ChartDocument40 pagesMesa Dew Poin ChartSdArNo ratings yet

- Rpmo October Payroll16Document22 pagesRpmo October Payroll16mennaldzNo ratings yet

- Empleyado Brochure PDFDocument3 pagesEmpleyado Brochure PDFRose ManaloNo ratings yet

- Tax Clearance BNDocument1 pageTax Clearance BNNora Goguanco PamplonaNo ratings yet

- Series of Frequency Inverter: Yantai Huifeng Electronics Co.,LtdDocument6 pagesSeries of Frequency Inverter: Yantai Huifeng Electronics Co.,LtdEzequiel Victor HugoNo ratings yet

- K'Sagar Publication GK Book Details PDFDocument5 pagesK'Sagar Publication GK Book Details PDFTilottama Deore50% (4)

- G1V2BL3 PDFDocument12 pagesG1V2BL3 PDFNeha SinghNo ratings yet

- Corrosion and Climatic Effects in Electronics: Risto HienonenDocument420 pagesCorrosion and Climatic Effects in Electronics: Risto HienonenShijumon KpNo ratings yet

- 01 - Cover - gs41Document3 pages01 - Cover - gs41Echa DudoNo ratings yet

- Khadayata Jyoti 2016-03Document104 pagesKhadayata Jyoti 2016-03reachtomrhandsomeNo ratings yet

- Khadayata Jyoti 2016-05Document100 pagesKhadayata Jyoti 2016-05manans_13No ratings yet

- ®KMSV/ Riu Âkk/S Kiul Ata Qv/.Atiuc/ QT/M T/Ek®Pv./M Ek A/L N/Eaac/ 'Ki PM/ Siuk/P OiDocument16 pages®KMSV/ Riu Âkk/S Kiul Ata Qv/.Atiuc/ QT/M T/Ek®Pv./M Ek A/L N/Eaac/ 'Ki PM/ Siuk/P Oithadar thanzawooNo ratings yet

- Anudina Bhava TharangaluDocument186 pagesAnudina Bhava TharangalusudeepraazNo ratings yet

- Preface Junior 2Document8 pagesPreface Junior 2Imam SibawaihiNo ratings yet

- Ganasakti 17 MarchDocument8 pagesGanasakti 17 Marchnirangkush nathNo ratings yet

- Jeff Cot Trot or Active ControlDocument166 pagesJeff Cot Trot or Active ControlHZ. TYMOFEINo ratings yet

- Lakshmi Kubera Poojai AshtothrasDocument28 pagesLakshmi Kubera Poojai AshtothrasNarayanan MuthuswamyNo ratings yet

- Introductory Micro Economics XIDocument116 pagesIntroductory Micro Economics XIarishreang2No ratings yet

- Logica 23Document6 pagesLogica 23teacher_miguelNo ratings yet

- Numbers The FifthDocument279 pagesNumbers The FifthМар'ян ВрюкалоNo ratings yet

- Numbers The ThirdDocument152 pagesNumbers The ThirdМар'ян ВрюкалоNo ratings yet

- Numbers The SeccondDocument76 pagesNumbers The SeccondМар'ян ВрюкалоNo ratings yet

- Numbers 1Document26 pagesNumbers 1Мар'ян ВрюкалоNo ratings yet

- 1234567890Document3 pages1234567890marcesalasNo ratings yet

- Numbers The FourthDocument178 pagesNumbers The FourthМар'ян ВрюкалоNo ratings yet

- CH 1Document27 pagesCH 1Sanjeev DubeyNo ratings yet

- YhdvcdDocument7 pagesYhdvcdFuazXNo ratings yet

- Ch-6 HindiDocument11 pagesCh-6 HindiSwapna GirishNo ratings yet

- earth inner structureDocument2 pagesearth inner structuremihabi5968No ratings yet

- Bhagavan Sri Sri Sri Venkaiahswamy Sadgurukrupa - Feb 2022-TELUGU DEVOTIONAL MONTHLY MAGAZINEDocument36 pagesBhagavan Sri Sri Sri Venkaiahswamy Sadgurukrupa - Feb 2022-TELUGU DEVOTIONAL MONTHLY MAGAZINESeshu VenkaiahswamyNo ratings yet

- Kham 116Document16 pagesKham 116Hari NirmalNo ratings yet

- Fundamental Physical Geography Class XIDocument156 pagesFundamental Physical Geography Class XIanindsNo ratings yet

- BehDocument2 pagesBehphilip.h.eadesNo ratings yet

- 2ND - Grand Olympiad - Question PaperDocument16 pages2ND - Grand Olympiad - Question Paperneetu.pravarshaNo ratings yet

- TORNEIODocument7 pagesTORNEIOClaudioLimaMatosNo ratings yet

- Description: Tags: 0203EFCFormulaGdWkshtDocument29 pagesDescription: Tags: 0203EFCFormulaGdWkshtanon-422641No ratings yet

- 1207A & 1207 ManualDocument70 pages1207A & 1207 ManualNILTON MOR100% (1)

- ODocument1 pageOgimapes258No ratings yet

- The 1 Quick 1 Brown 1 Fox 1 Jumps 1 Over 1 The 1 Lazy 1 DogDocument249 pagesThe 1 Quick 1 Brown 1 Fox 1 Jumps 1 Over 1 The 1 Lazy 1 Doganon_604916838No ratings yet

- VariosDocument3 pagesVariosAdrianNo ratings yet

- Peterson S Ultimate GRE Tool KitDocument351 pagesPeterson S Ultimate GRE Tool Kitlyasa77100% (3)

- SDFGHDocument3 pagesSDFGHpxstelpxwderNo ratings yet

- Abhivyakti Aur Madhyam Class XII HindiDocument16 pagesAbhivyakti Aur Madhyam Class XII HindiPiyush Pastor100% (3)

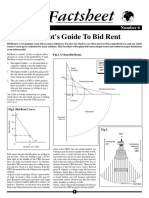

- Geo Factsheet: An Idiot's Guide To Bid RentDocument2 pagesGeo Factsheet: An Idiot's Guide To Bid RentaurennosNo ratings yet

- Dove 37 2Document4 pagesDove 37 2lovelamp88No ratings yet

- 10Document245 pages10dennis aguilar fuentesNo ratings yet

- 1204x 05 PDFDocument56 pages1204x 05 PDFAlberto MattiesNo ratings yet

- Sri Ramachandra Spinning Mills v. Province of MadrasDocument8 pagesSri Ramachandra Spinning Mills v. Province of MadrasjayabhargaviNo ratings yet

- Mario Raposo Vs HM Bhandarkar and Ors 14121993 BO0118m930463COM887859Document3 pagesMario Raposo Vs HM Bhandarkar and Ors 14121993 BO0118m930463COM887859jayabhargaviNo ratings yet

- PIL Case AnalysisDocument56 pagesPIL Case AnalysisjayabhargaviNo ratings yet

- Routledge Handbook of International EnviDocument19 pagesRoutledge Handbook of International EnvijayabhargaviNo ratings yet

- Income Tax Part IIDocument7 pagesIncome Tax Part IImary jhoyNo ratings yet

- 2021-09-30T21-06 Transaction #4321966431251448-8519037Document1 page2021-09-30T21-06 Transaction #4321966431251448-8519037fetacademymediaNo ratings yet

- Tax 3 ASSIGNMENTDocument23 pagesTax 3 ASSIGNMENTPui YanNo ratings yet

- RMC No 24-18 - Annexes B1-B5 - Required AttachmentsDocument3 pagesRMC No 24-18 - Annexes B1-B5 - Required AttachmentsGil PinoNo ratings yet

- Bai Tap - IAS 12 - Tu LuanDocument14 pagesBai Tap - IAS 12 - Tu LuanTrần Nguyễn Tuệ MinhNo ratings yet

- TAX1-LagguiRichelle 2Document4 pagesTAX1-LagguiRichelle 2Richelle GraceNo ratings yet

- Direct Taxes - I - Unit 1, Unit 2, Unit 3, Unit 5Document23 pagesDirect Taxes - I - Unit 1, Unit 2, Unit 3, Unit 5JayNo ratings yet

- IT Compensation NotesDocument33 pagesIT Compensation NotesWinnie GiveraNo ratings yet

- Best in Sytems Tech. 2021payrollsignedDocument20 pagesBest in Sytems Tech. 2021payrollsignedSombre Sumayo Jackie MarieNo ratings yet

- GP Mobil Bill-Dec-19Document69 pagesGP Mobil Bill-Dec-19biddut782No ratings yet

- Chapter 1 Problems HDocument14 pagesChapter 1 Problems Hbalaji RNo ratings yet

- GST Book Bank AnswersDocument10 pagesGST Book Bank AnswersAditya DasNo ratings yet

- Annex A - Format of Notice of Discrepancy - RMC 102-2020 1Document2 pagesAnnex A - Format of Notice of Discrepancy - RMC 102-2020 1Joanna AbañoNo ratings yet

- Summary of Cash PaymentsDocument4 pagesSummary of Cash PaymentsmellicentdhaNo ratings yet

- 42.gaston vs. Republic Planter's Bank 158 Scra 626Document1 page42.gaston vs. Republic Planter's Bank 158 Scra 626Jo DevisNo ratings yet

- Customs Duty Calculation FormulaDocument4 pagesCustoms Duty Calculation Formulabibhas1No ratings yet

- Vijaya Po 2Document1 pageVijaya Po 2adrijaswiagenciesNo ratings yet

- Thomas Co LTD Payroll 2019Document2 pagesThomas Co LTD Payroll 2019MaxineNo ratings yet

- Commissioner v. Burroughs, 142 SCRA 324 (1986) PDFDocument4 pagesCommissioner v. Burroughs, 142 SCRA 324 (1986) PDFHazel FernandezNo ratings yet

- Classification of TaxesDocument2 pagesClassification of TaxesJoliza CalingacionNo ratings yet

- Balochistan Sales Tax Special Procedure (Transportation or Carriage of Petroleum Oils Through Oil Tankers) Rules, 2019Document8 pagesBalochistan Sales Tax Special Procedure (Transportation or Carriage of Petroleum Oils Through Oil Tankers) Rules, 2019Tax PerceptionNo ratings yet

- Bipard Prashichhan (Gaya) - 87-2023 2ndDocument2 pagesBipard Prashichhan (Gaya) - 87-2023 2ndtinkulal91No ratings yet

- Form16 (2020-2021)Document2 pagesForm16 (2020-2021)P v v RaoNo ratings yet

- Spectra Notes Tax Law 2 Compilation PDFDocument197 pagesSpectra Notes Tax Law 2 Compilation PDFKriziaItao100% (1)

- LLPCollegeDocument25 pagesLLPCollegeKeshavNo ratings yet

- Name: Waleed Zahid Roll No: F18-1010 BS Accounting&Finance 6 Assignment No 1 Submitted To: Sir Atif Attique SiddiquiDocument5 pagesName: Waleed Zahid Roll No: F18-1010 BS Accounting&Finance 6 Assignment No 1 Submitted To: Sir Atif Attique SiddiquiFurqan AhmedNo ratings yet

- Black MoneyDocument22 pagesBlack MoneyManish JainNo ratings yet