Download as pdf or txt

You might also like

- Ibc ChartsDocument7 pagesIbc Chartspiyush bansalNo ratings yet

- Toy World, Inc - Projected Balance Sheet and Income StatementDocument4 pagesToy World, Inc - Projected Balance Sheet and Income StatementMartin Perrone0% (1)

- Unit 5Document8 pagesUnit 5Aravindhan RavichandranNo ratings yet

- Ch 14 Part a Leverage Risk and ReturnDocument17 pagesCh 14 Part a Leverage Risk and Return55dvir555No ratings yet

- Capital Structure: Financial DistressDocument22 pagesCapital Structure: Financial DistressAniket KaushikNo ratings yet

- Corporate: Restructuring & TurnaroundsDocument15 pagesCorporate: Restructuring & TurnaroundsNathaniel AnumbaNo ratings yet

- 4330 Lecture 28 Financial Stress F10Document19 pages4330 Lecture 28 Financial Stress F10joekamunya63No ratings yet

- C14 External Loss FinancingDocument38 pagesC14 External Loss FinancingPham Hong VanNo ratings yet

- Class Notes - 1Document32 pagesClass Notes - 1ushaNo ratings yet

- Financial Distress - Overview and ModelsDocument20 pagesFinancial Distress - Overview and Modelsfanuel kijojiNo ratings yet

- Financial DistressDocument24 pagesFinancial Distressjahidul.rakib.me1No ratings yet

- Lecture 5: Capital Structure 3 Lecture 5: Capital Structure 3Document10 pagesLecture 5: Capital Structure 3 Lecture 5: Capital Structure 3LIAW ANN YINo ratings yet

- CityU - Chapter 1 Intro To CF - STDDocument34 pagesCityU - Chapter 1 Intro To CF - STDNguyễn Đăng HiếuNo ratings yet

- Ch16 Part B Financal DistressDocument15 pagesCh16 Part B Financal Distress55dvir555No ratings yet

- Business Failure, Reorganization, and LiquidationDocument12 pagesBusiness Failure, Reorganization, and LiquidationApril BoreresNo ratings yet

- Financial Distress (2008)Document24 pagesFinancial Distress (2008)Ira Putri100% (1)

- Debt Restructuring: Alternatives and Implications: On Business EducationDocument6 pagesDebt Restructuring: Alternatives and Implications: On Business Educationkristin_kim_13No ratings yet

- Corporate Finance Cheat SheetDocument3 pagesCorporate Finance Cheat Sheetdiscreetmike50No ratings yet

- Jurnal Al AjmiDocument16 pagesJurnal Al AjmiamandaNo ratings yet

- A Look at Current Financial Reporting Issues: in DepthDocument26 pagesA Look at Current Financial Reporting Issues: in Depthhur hussainNo ratings yet

- ABFL Liquidty Risk Disclosure Dec 2019Document1 pageABFL Liquidty Risk Disclosure Dec 2019lohit22No ratings yet

- Bankruptcy DecisionDocument20 pagesBankruptcy DecisionJeffy JanNo ratings yet

- Chapter 1 (Edited)Document28 pagesChapter 1 (Edited)Hoang Thi Thanh TamNo ratings yet

- MFA (Volume 2) by M. Asif, FCADocument202 pagesMFA (Volume 2) by M. Asif, FCAZubair MalikNo ratings yet

- Leases and Off-Balance Sheet Debt Why Lease ?Document3 pagesLeases and Off-Balance Sheet Debt Why Lease ?Nouman AliNo ratings yet

- Pert 8-Financial DifficultyDocument39 pagesPert 8-Financial DifficultySri AstutiNo ratings yet

- Capital Struchoices (Modified)Document16 pagesCapital Struchoices (Modified)mogibol791No ratings yet

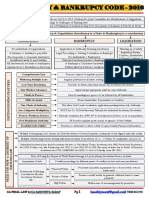

- Ibc 2016Document74 pagesIbc 2016Roshini Chinnappa100% (1)

- Chapter 17 - Bankruptcy and LiquidationDocument9 pagesChapter 17 - Bankruptcy and Liquidation1954032027cucNo ratings yet

- Evolving Landscape of Corporate Stress ResolutionDocument68 pagesEvolving Landscape of Corporate Stress ResolutiongowthampkfNo ratings yet

- Directors' Duties and Liabilities in Financial Distress During Covid-19Document13 pagesDirectors' Duties and Liabilities in Financial Distress During Covid-19jshfjksNo ratings yet

- Workflow OptimizationDocument14 pagesWorkflow OptimizationSandro ChanelNo ratings yet

- For Help With IFRS 9 Compliance, Contact Us At:: WWW - Principa.co - ZaDocument6 pagesFor Help With IFRS 9 Compliance, Contact Us At:: WWW - Principa.co - ZaHafeel MohamedNo ratings yet

- Ch11 SCC Longterm LiabilitiesDocument49 pagesCh11 SCC Longterm Liabilitiesfathiah nur afifiNo ratings yet

- Ibc 2016Document102 pagesIbc 2016Suhas TelangNo ratings yet

- HRM129 Module No. 1Document3 pagesHRM129 Module No. 1Kim B. CalcetaNo ratings yet

- Applied Corporate FinanceDocument258 pagesApplied Corporate Financesirkoywayo6628No ratings yet

- Web Appendix 7BDocument7 pagesWeb Appendix 7Bempor1001No ratings yet

- Financial Distress: Group 5 ACT 4611 Seminar in AccountingsDocument38 pagesFinancial Distress: Group 5 ACT 4611 Seminar in AccountingsPj SornNo ratings yet

- Concept of Insolvency and BankruptcyDocument68 pagesConcept of Insolvency and BankruptcyNavin Man Singh ShresthaNo ratings yet

- Big Picture of Finance: What Is Finance? The Science of Managing MoneyDocument22 pagesBig Picture of Finance: What Is Finance? The Science of Managing MoneyJiyaad NaeemNo ratings yet

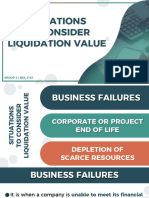

- Situations-to-Consider-Liquidation-ValueDocument17 pagesSituations-to-Consider-Liquidation-Valueherrera.angelaNo ratings yet

- Applying IFRS 9 To Related Company Loans - 2022 2023Document47 pagesApplying IFRS 9 To Related Company Loans - 2022 2023Mohammad IslamNo ratings yet

- SignificantcreditriskDocument8 pagesSignificantcreditriskHamza AmiriNo ratings yet

- Risk Management TechniquesDocument16 pagesRisk Management Techniquesyoshiharu.harano1726No ratings yet

- High Yield Covenants - Merrill Lynch - Oct 2005Document21 pagesHigh Yield Covenants - Merrill Lynch - Oct 2005fi5hyNo ratings yet

- Alliotts Bankruptcy Article Retention AgreementsDocument2 pagesAlliotts Bankruptcy Article Retention Agreementstheoaklandjournal@gmail.comNo ratings yet

- Credit Analysis and Distress PredictionDocument57 pagesCredit Analysis and Distress Predictionrizki nurNo ratings yet

- BIWS LBO Quick ReferenceDocument24 pagesBIWS LBO Quick Referenceallrightsreserved21No ratings yet

- Finance FunctionDocument26 pagesFinance FunctionAyushi KeshriNo ratings yet

- Corporate Insolvency Resolution Procedure Under Indian Insolvency and Bankruptcy Code, 2016: A Comparative PerspectiveDocument8 pagesCorporate Insolvency Resolution Procedure Under Indian Insolvency and Bankruptcy Code, 2016: A Comparative PerspectiveDeva SharmaNo ratings yet

- Chapter 3-Financial Statement AnalysisDocument25 pagesChapter 3-Financial Statement AnalysisThị Duyên Hải PhạmNo ratings yet

- Demergers and Reverse Mergers-An Insightful StudyDocument11 pagesDemergers and Reverse Mergers-An Insightful StudymaithNo ratings yet

- Olympus RVPDocument27 pagesOlympus RVPTan Mark AndrewNo ratings yet

- Learn and Go This New Formula of Cost of Equity:: JMD TUTORIAL'S-Question BankDocument12 pagesLearn and Go This New Formula of Cost of Equity:: JMD TUTORIAL'S-Question BankSnehal PatelNo ratings yet

- Accounting For Directors Loans Under FRS 102 FAQsDocument7 pagesAccounting For Directors Loans Under FRS 102 FAQswattersed1711No ratings yet

- Bailouts and Bankruptcies - Corporate Distress, Troubled Debt Restructurings and Equity StrippingDocument61 pagesBailouts and Bankruptcies - Corporate Distress, Troubled Debt Restructurings and Equity StrippingjeganrajrajNo ratings yet

- Lecture 1 - The Financial Manager and The Firm (Student Version)Document18 pagesLecture 1 - The Financial Manager and The Firm (Student Version)Jason LuximonNo ratings yet

- 402 - FSV - Suggested Solutions - 2020 MayDocument18 pages402 - FSV - Suggested Solutions - 2020 MayThema ThushsNo ratings yet

- 02 Financial Statements Case StudyDocument3 pages02 Financial Statements Case StudyanitalauymNo ratings yet

- Chapter 19 Business Finance Needs and SourcesDocument5 pagesChapter 19 Business Finance Needs and SourcesSol CarvajalNo ratings yet

- Cooperative Banking in Kerala Revamping The Role of Kerala BankDocument96 pagesCooperative Banking in Kerala Revamping The Role of Kerala Banksuryanellikkunnam2No ratings yet

- Application For Other Savings For The Computation of Income Tax For The YearDocument2 pagesApplication For Other Savings For The Computation of Income Tax For The YearSr DEE G MLDT OFFICENo ratings yet

- GPF CPS FormatDocument6 pagesGPF CPS FormatSuganya LokeshNo ratings yet

- Credit Reports and Scores Note Taking Guide 2 6 1 l1Document4 pagesCredit Reports and Scores Note Taking Guide 2 6 1 l1api-26818659550% (2)

- How To Build Credit Score QuicklyDocument2 pagesHow To Build Credit Score QuicklyCharles0% (1)

- Investor Presentation - June23Document24 pagesInvestor Presentation - June23ivanpushkarevNo ratings yet

- Cps ClarificationDocument4 pagesCps ClarificationgcrajasekaranNo ratings yet

- Current Account Statement: Dear CustomerDocument15 pagesCurrent Account Statement: Dear Customersk1internationalsk1No ratings yet

- Form Reimbursement Boy (Bali 14-20 May)Document10 pagesForm Reimbursement Boy (Bali 14-20 May)David ValentinoNo ratings yet

- Finance Group Assignment Week 13Document3 pagesFinance Group Assignment Week 13Rahman Armenzaria100% (1)

- Test - CH 5 & 6Document4 pagesTest - CH 5 & 6luvkumar3532No ratings yet

- Tri LegalDocument4 pagesTri LegalShreyashkarNo ratings yet

- EY IBC ReportDocument40 pagesEY IBC ReportShushrut KhannaNo ratings yet

- Daily Cash Position FormDocument15 pagesDaily Cash Position FormJERRY PRINTSHOPNo ratings yet

- DRE Broker Compliance Short GuideDocument28 pagesDRE Broker Compliance Short GuideScott RoyvalNo ratings yet

- Types of Pension PlansDocument46 pagesTypes of Pension PlansAasthaNo ratings yet

- Acca FINC 406 Financial Markets ModeratedDocument6 pagesAcca FINC 406 Financial Markets Moderatedcaleb smithNo ratings yet

- Fact Sheet Fha 203bDocument10 pagesFact Sheet Fha 203bmptacly9152No ratings yet

- Salary SlipDocument1 pageSalary Sliprichard parkerNo ratings yet

- PayslipDocument3 pagesPayslipDurga raniNo ratings yet

- The Mortgage Markets: Quantitative ProblemsDocument10 pagesThe Mortgage Markets: Quantitative ProblemsMai AnhNo ratings yet

- Benefits. by of Sales: 2020. SuperannuationDocument1 pageBenefits. by of Sales: 2020. SuperannuationArya RoshanNo ratings yet

- Key BtapDocument11 pagesKey BtapViệt Phương NguyễnNo ratings yet

- Form - 6251Document2 pagesForm - 6251Anonymous JqimV1ENo ratings yet

- Promissory NoteDocument2 pagesPromissory NoteRoselyn IgartaNo ratings yet

- Practice ProblemsDocument1 pagePractice ProblemsYss CastañedaNo ratings yet

- Form PDF 648514400190719Document6 pagesForm PDF 648514400190719RebornNo ratings yet