BPP Kit Mapping question wise

BPP Kit Mapping question wise

You might also like

- Ifrs & Ias Flow Charts: by Mr. Bilal Khalid Khan (Fca)Document40 pagesIfrs & Ias Flow Charts: by Mr. Bilal Khalid Khan (Fca)Bagas Nurfazar100% (2)

- CMA Part 1 Hock Essay QuestionsDocument74 pagesCMA Part 1 Hock Essay QuestionsAbhishek Goyal100% (5)

- 11-1 Medieval Adventures CompanyDocument8 pages11-1 Medieval Adventures CompanyWei DaiNo ratings yet

- Chris Moon - Business Ethics - Facing Up To The Issues (2001, Bloomberg Press) PDFDocument218 pagesChris Moon - Business Ethics - Facing Up To The Issues (2001, Bloomberg Press) PDFCostache Madalina AlexandraNo ratings yet

- Rev C5Document9 pagesRev C5Richard W YipNo ratings yet

- Advance AccountingDocument12 pagesAdvance AccountingunknownNo ratings yet

- Framework of Accounting (TOA) - ValixDocument42 pagesFramework of Accounting (TOA) - ValixFatima Pasamonte88% (43)

- FSAI EXAM2 Solutions Fraser 10thDocument14 pagesFSAI EXAM2 Solutions Fraser 10thGlaiza Dalayoan Flores0% (1)

- BPP Kit Standard Wise MappingDocument7 pagesBPP Kit Standard Wise Mappingjunk2023No ratings yet

- AuditingDocument22 pagesAuditingawaisNo ratings yet

- Ca Inter Advanced Accounting MCQDocument210 pagesCa Inter Advanced Accounting MCQVikramNo ratings yet

- Accounting Reviewer 1.1Document35 pagesAccounting Reviewer 1.1Ma. Concepcion DesepedaNo ratings yet

- CPA Paper 13Document16 pagesCPA Paper 13sanu sayedNo ratings yet

- CPA Paper 8Document15 pagesCPA Paper 8sanu sayedNo ratings yet

- Framework of Accounting TOA EDITEDDocument48 pagesFramework of Accounting TOA EDITEDMiss A Academic ServicesNo ratings yet

- Corporate GovernanceDocument22 pagesCorporate Governanceroman empireNo ratings yet

- Answer in Assessment (CFAS)Document14 pagesAnswer in Assessment (CFAS)Angelika MoranNo ratings yet

- Which of The Following Is Not A Duty of The International Financial Reporting StandardDocument5 pagesWhich of The Following Is Not A Duty of The International Financial Reporting Standardchristian ReyesNo ratings yet

- Material - Framework of Accounting (Weekend)Document5 pagesMaterial - Framework of Accounting (Weekend)Sharmaine Diane N. CalvaNo ratings yet

- TEST BANK (UCNHS Reviewer For Kingfisher ABM Cup)Document12 pagesTEST BANK (UCNHS Reviewer For Kingfisher ABM Cup)Eya Guerrero Calvarido100% (1)

- Question - September 2018 BackgroundDocument6 pagesQuestion - September 2018 BackgroundAbdullah EjazNo ratings yet

- In-Class Test 2019Document8 pagesIn-Class Test 2019kissmegorgeousNo ratings yet

- Review Questions Financial Accounting and Reporting PART 1Document3 pagesReview Questions Financial Accounting and Reporting PART 1Claire BarbaNo ratings yet

- Training Material of AuditDocument89 pagesTraining Material of AuditNaeem Uddin100% (10)

- Accounting Principles & Procedures MCQs - FPSC Senior Auditor Tests PDFDocument8 pagesAccounting Principles & Procedures MCQs - FPSC Senior Auditor Tests PDFMuhammad TariqNo ratings yet

- Accounting & Finance (SMB108)Document25 pagesAccounting & Finance (SMB108)lravi4uNo ratings yet

- Accounting & Auditing Paper - I (2000)Document13 pagesAccounting & Auditing Paper - I (2000)Sikandar EjazNo ratings yet

- Paper F-1 Fianancial Operation: Syllabus Content Learning Outcome: Hours Quiz/Home AssignmentsDocument5 pagesPaper F-1 Fianancial Operation: Syllabus Content Learning Outcome: Hours Quiz/Home AssignmentsAslam SiddiqNo ratings yet

- June 2006 Question PaperDocument11 pagesJune 2006 Question PapermanojrkmNo ratings yet

- Unit Ii Short Answer Type QuestionDocument3 pagesUnit Ii Short Answer Type Questionmultanigazal_4254062No ratings yet

- Icaew Diploma in Ifrss Syllabus and Study Guide 811Document11 pagesIcaew Diploma in Ifrss Syllabus and Study Guide 811Muridsultan JanjuaNo ratings yet

- ACCT 621 Practicing 1Document3 pagesACCT 621 Practicing 1Hashitha100% (1)

- SBR Revision NotesDocument294 pagesSBR Revision Notesbubbly100% (2)

- MCQ - BBA III Semester - BBA3B04 - Corporate Accounting - 0Document12 pagesMCQ - BBA III Semester - BBA3B04 - Corporate Accounting - 0sanz81909No ratings yet

- Making A List of IAS and IFRS As Adopted by BangladeshDocument9 pagesMaking A List of IAS and IFRS As Adopted by BangladeshAbir Hasan ApurboNo ratings yet

- Afacr Dec 2023 Attempt QuestionsDocument8 pagesAfacr Dec 2023 Attempt QuestionsShoaib HafeezNo ratings yet

- FAR Dry Run ReviewerDocument5 pagesFAR Dry Run ReviewerJohn Ace MadriagaNo ratings yet

- Accounting Principles and ProceduresDocument8 pagesAccounting Principles and ProceduresAdnan DaniNo ratings yet

- P20 SPM BV PH 2Document9 pagesP20 SPM BV PH 2Shivam GuptaNo ratings yet

- Ca10 0120Document16 pagesCa10 0120Amit KumarNo ratings yet

- Paspt Paper AnalysisDocument15 pagesPaspt Paper Analysisawais mehmoodNo ratings yet

- Basic Acc Quiz1Document4 pagesBasic Acc Quiz1Angel BiernezaNo ratings yet

- SBR-List of Technical ArticlesDocument1 pageSBR-List of Technical ArticleskeishaelinaNo ratings yet

- SBR Revision NotesDocument294 pagesSBR Revision NotesThembisile P ZwaneNo ratings yet

- Accounting & Auditing Mcqs From Past Papers: (C) Lucas PacioliDocument24 pagesAccounting & Auditing Mcqs From Past Papers: (C) Lucas PacioliAssad BilalNo ratings yet

- Accounting MCQDocument15 pagesAccounting MCQFahad RazaNo ratings yet

- Updates in FRS - Midterm Exam With SolutionDocument10 pagesUpdates in FRS - Midterm Exam With Solutionchristian ReyesNo ratings yet

- 7 CPA FINANCIAL REPORTING Paper 7Document13 pages7 CPA FINANCIAL REPORTING Paper 7dennis greenNo ratings yet

- Materials Allowed: Silent, Cordless Calculators (Financial Calculators Are Permitted) Translation DictionariesDocument12 pagesMaterials Allowed: Silent, Cordless Calculators (Financial Calculators Are Permitted) Translation DictionariesMiruna CiteaNo ratings yet

- International Financial Reporting Standards: Presentation and Disclosure Checklist 2007Document160 pagesInternational Financial Reporting Standards: Presentation and Disclosure Checklist 2007Tony PranotoNo ratings yet

- Financial Analysis TestDocument11 pagesFinancial Analysis TestAlaitz GNo ratings yet

- International Accounting and Financial Reporting: Ass. Prof. Mohammed ALASHIDocument16 pagesInternational Accounting and Financial Reporting: Ass. Prof. Mohammed ALASHIOmar YounisNo ratings yet

- CPA Paper 1Document10 pagesCPA Paper 1sanu sayedNo ratings yet

- Conceptual Frame Work QBDocument15 pagesConceptual Frame Work QBnanthini nanthini100% (1)

- ChronologiqueDocument40 pagesChronologiqueSamseer R HNo ratings yet

- Inter Paper12 Revised PDFDocument788 pagesInter Paper12 Revised PDFbhagyashre100% (1)

- 1 Cpa Financial Accounting Paper 1Document20 pages1 Cpa Financial Accounting Paper 1kajalshiroya17No ratings yet

- Acc 416Document7 pagesAcc 4161sirdeeqNo ratings yet

- Prepared By: CA. Abhijeet N. BobadeDocument9 pagesPrepared By: CA. Abhijeet N. Bobadepsawant77No ratings yet

- Accounts ImpDocument24 pagesAccounts ImphamzafarooqNo ratings yet

- An Introduction International Financial Reporting Standards (IFRS)Document34 pagesAn Introduction International Financial Reporting Standards (IFRS)EshetieNo ratings yet

- Understanding IFRS Fundamentals: International Financial Reporting StandardsFrom EverandUnderstanding IFRS Fundamentals: International Financial Reporting StandardsNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionNo ratings yet

- Part - A: (Financial Accounting - I)Document16 pagesPart - A: (Financial Accounting - I)Adit Bohra VIII BNo ratings yet

- Balance Sheet ProvisionalDocument2 pagesBalance Sheet ProvisionalRaja AdhikariNo ratings yet

- Fixed Assest Management-UltratechDocument6 pagesFixed Assest Management-UltratechMr SmartNo ratings yet

- Consolidations - Subsequent To The Date of Acquisition: Multiple Choice QuestionsDocument290 pagesConsolidations - Subsequent To The Date of Acquisition: Multiple Choice QuestionsKim FloresNo ratings yet

- Chapter 11 - Ho Branch - MillanDocument34 pagesChapter 11 - Ho Branch - MillanAngelica Cerio100% (1)

- Indirect and Mutual HoldingsDocument36 pagesIndirect and Mutual HoldingssiwiNo ratings yet

- Methods For Patent Valuation PDFDocument11 pagesMethods For Patent Valuation PDFSantosh PatiNo ratings yet

- Business Combination Lecture Notes. ACC 401Document4 pagesBusiness Combination Lecture Notes. ACC 401Ugbah Chidinma LilianNo ratings yet

- AC2091 ZB Final For UoLDocument16 pagesAC2091 ZB Final For UoLkikiNo ratings yet

- Depreciation: Disposal of Fixed AssetsDocument13 pagesDepreciation: Disposal of Fixed AssetsHassan AliNo ratings yet

- Sir Mac Book SolmanDocument10 pagesSir Mac Book SolmanJAY AUBREY PINEDANo ratings yet

- Q4-31-03-2022 TMBDocument67 pagesQ4-31-03-2022 TMBDhanush Kumar RamanNo ratings yet

- Accounting For Management Question PaperDocument3 pagesAccounting For Management Question PaperVINOD KUMARNo ratings yet

- DepreciationDocument13 pagesDepreciationHarshitPalNo ratings yet

- Financial Reporting Strathmore University Notes and Revision KitDocument551 pagesFinancial Reporting Strathmore University Notes and Revision KitLazarus AmaniNo ratings yet

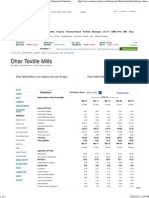

- Dhar Textile Mills Balance Sheet, Dhar Textile Mills Financial Statement & AccountsDocument3 pagesDhar Textile Mills Balance Sheet, Dhar Textile Mills Financial Statement & AccountsAkshay BhattNo ratings yet

- Mini MBA B10 - 01 Financial Management - Day 01Document41 pagesMini MBA B10 - 01 Financial Management - Day 01Reza MonoarfaNo ratings yet

- Montajes - Joelyn Grace 117848 Seatwork 2Document9 pagesMontajes - Joelyn Grace 117848 Seatwork 2Joelyn Grace MontajesNo ratings yet

- ERP Operations: SAP Standard ReportsDocument10 pagesERP Operations: SAP Standard ReportsAnkur RastogiNo ratings yet

- Dabur Financial Modeling-Live Project.Document47 pagesDabur Financial Modeling-Live Project.rahul1094No ratings yet

- Interlocal Agreement 8-2-99Document2 pagesInterlocal Agreement 8-2-99williamblueNo ratings yet

- (ESP Merit and Needs Based Scholarship Program) : Instructions For Filling Out The Scholarship Application FormDocument9 pages(ESP Merit and Needs Based Scholarship Program) : Instructions For Filling Out The Scholarship Application FormIffatNo ratings yet

- Amalgamation NotesDocument28 pagesAmalgamation NotesADARSH MISHRANo ratings yet

- Acc311 2021Document4 pagesAcc311 2021hoghidan1No ratings yet

- ACCT 100-Principles of Financial Accounting - Omair HaroonDocument7 pagesACCT 100-Principles of Financial Accounting - Omair HaroonUmar FarooqNo ratings yet

Download as pdf or txt

You might also like

- Ifrs & Ias Flow Charts: by Mr. Bilal Khalid Khan (Fca)Document40 pagesIfrs & Ias Flow Charts: by Mr. Bilal Khalid Khan (Fca)Bagas Nurfazar100% (2)

- CMA Part 1 Hock Essay QuestionsDocument74 pagesCMA Part 1 Hock Essay QuestionsAbhishek Goyal100% (5)

- 11-1 Medieval Adventures CompanyDocument8 pages11-1 Medieval Adventures CompanyWei DaiNo ratings yet

- Chris Moon - Business Ethics - Facing Up To The Issues (2001, Bloomberg Press) PDFDocument218 pagesChris Moon - Business Ethics - Facing Up To The Issues (2001, Bloomberg Press) PDFCostache Madalina AlexandraNo ratings yet

- Rev C5Document9 pagesRev C5Richard W YipNo ratings yet

- Advance AccountingDocument12 pagesAdvance AccountingunknownNo ratings yet

- Framework of Accounting (TOA) - ValixDocument42 pagesFramework of Accounting (TOA) - ValixFatima Pasamonte88% (43)

- FSAI EXAM2 Solutions Fraser 10thDocument14 pagesFSAI EXAM2 Solutions Fraser 10thGlaiza Dalayoan Flores0% (1)

- BPP Kit Standard Wise MappingDocument7 pagesBPP Kit Standard Wise Mappingjunk2023No ratings yet

- AuditingDocument22 pagesAuditingawaisNo ratings yet

- Ca Inter Advanced Accounting MCQDocument210 pagesCa Inter Advanced Accounting MCQVikramNo ratings yet

- Accounting Reviewer 1.1Document35 pagesAccounting Reviewer 1.1Ma. Concepcion DesepedaNo ratings yet

- CPA Paper 13Document16 pagesCPA Paper 13sanu sayedNo ratings yet

- CPA Paper 8Document15 pagesCPA Paper 8sanu sayedNo ratings yet

- Framework of Accounting TOA EDITEDDocument48 pagesFramework of Accounting TOA EDITEDMiss A Academic ServicesNo ratings yet

- Corporate GovernanceDocument22 pagesCorporate Governanceroman empireNo ratings yet

- Answer in Assessment (CFAS)Document14 pagesAnswer in Assessment (CFAS)Angelika MoranNo ratings yet

- Which of The Following Is Not A Duty of The International Financial Reporting StandardDocument5 pagesWhich of The Following Is Not A Duty of The International Financial Reporting Standardchristian ReyesNo ratings yet

- Material - Framework of Accounting (Weekend)Document5 pagesMaterial - Framework of Accounting (Weekend)Sharmaine Diane N. CalvaNo ratings yet

- TEST BANK (UCNHS Reviewer For Kingfisher ABM Cup)Document12 pagesTEST BANK (UCNHS Reviewer For Kingfisher ABM Cup)Eya Guerrero Calvarido100% (1)

- Question - September 2018 BackgroundDocument6 pagesQuestion - September 2018 BackgroundAbdullah EjazNo ratings yet

- In-Class Test 2019Document8 pagesIn-Class Test 2019kissmegorgeousNo ratings yet

- Review Questions Financial Accounting and Reporting PART 1Document3 pagesReview Questions Financial Accounting and Reporting PART 1Claire BarbaNo ratings yet

- Training Material of AuditDocument89 pagesTraining Material of AuditNaeem Uddin100% (10)

- Accounting Principles & Procedures MCQs - FPSC Senior Auditor Tests PDFDocument8 pagesAccounting Principles & Procedures MCQs - FPSC Senior Auditor Tests PDFMuhammad TariqNo ratings yet

- Accounting & Finance (SMB108)Document25 pagesAccounting & Finance (SMB108)lravi4uNo ratings yet

- Accounting & Auditing Paper - I (2000)Document13 pagesAccounting & Auditing Paper - I (2000)Sikandar EjazNo ratings yet

- Paper F-1 Fianancial Operation: Syllabus Content Learning Outcome: Hours Quiz/Home AssignmentsDocument5 pagesPaper F-1 Fianancial Operation: Syllabus Content Learning Outcome: Hours Quiz/Home AssignmentsAslam SiddiqNo ratings yet

- June 2006 Question PaperDocument11 pagesJune 2006 Question PapermanojrkmNo ratings yet

- Unit Ii Short Answer Type QuestionDocument3 pagesUnit Ii Short Answer Type Questionmultanigazal_4254062No ratings yet

- Icaew Diploma in Ifrss Syllabus and Study Guide 811Document11 pagesIcaew Diploma in Ifrss Syllabus and Study Guide 811Muridsultan JanjuaNo ratings yet

- ACCT 621 Practicing 1Document3 pagesACCT 621 Practicing 1Hashitha100% (1)

- SBR Revision NotesDocument294 pagesSBR Revision Notesbubbly100% (2)

- MCQ - BBA III Semester - BBA3B04 - Corporate Accounting - 0Document12 pagesMCQ - BBA III Semester - BBA3B04 - Corporate Accounting - 0sanz81909No ratings yet

- Making A List of IAS and IFRS As Adopted by BangladeshDocument9 pagesMaking A List of IAS and IFRS As Adopted by BangladeshAbir Hasan ApurboNo ratings yet

- Afacr Dec 2023 Attempt QuestionsDocument8 pagesAfacr Dec 2023 Attempt QuestionsShoaib HafeezNo ratings yet

- FAR Dry Run ReviewerDocument5 pagesFAR Dry Run ReviewerJohn Ace MadriagaNo ratings yet

- Accounting Principles and ProceduresDocument8 pagesAccounting Principles and ProceduresAdnan DaniNo ratings yet

- P20 SPM BV PH 2Document9 pagesP20 SPM BV PH 2Shivam GuptaNo ratings yet

- Ca10 0120Document16 pagesCa10 0120Amit KumarNo ratings yet

- Paspt Paper AnalysisDocument15 pagesPaspt Paper Analysisawais mehmoodNo ratings yet

- Basic Acc Quiz1Document4 pagesBasic Acc Quiz1Angel BiernezaNo ratings yet

- SBR-List of Technical ArticlesDocument1 pageSBR-List of Technical ArticleskeishaelinaNo ratings yet

- SBR Revision NotesDocument294 pagesSBR Revision NotesThembisile P ZwaneNo ratings yet

- Accounting & Auditing Mcqs From Past Papers: (C) Lucas PacioliDocument24 pagesAccounting & Auditing Mcqs From Past Papers: (C) Lucas PacioliAssad BilalNo ratings yet

- Accounting MCQDocument15 pagesAccounting MCQFahad RazaNo ratings yet

- Updates in FRS - Midterm Exam With SolutionDocument10 pagesUpdates in FRS - Midterm Exam With Solutionchristian ReyesNo ratings yet

- 7 CPA FINANCIAL REPORTING Paper 7Document13 pages7 CPA FINANCIAL REPORTING Paper 7dennis greenNo ratings yet

- Materials Allowed: Silent, Cordless Calculators (Financial Calculators Are Permitted) Translation DictionariesDocument12 pagesMaterials Allowed: Silent, Cordless Calculators (Financial Calculators Are Permitted) Translation DictionariesMiruna CiteaNo ratings yet

- International Financial Reporting Standards: Presentation and Disclosure Checklist 2007Document160 pagesInternational Financial Reporting Standards: Presentation and Disclosure Checklist 2007Tony PranotoNo ratings yet

- Financial Analysis TestDocument11 pagesFinancial Analysis TestAlaitz GNo ratings yet

- International Accounting and Financial Reporting: Ass. Prof. Mohammed ALASHIDocument16 pagesInternational Accounting and Financial Reporting: Ass. Prof. Mohammed ALASHIOmar YounisNo ratings yet

- CPA Paper 1Document10 pagesCPA Paper 1sanu sayedNo ratings yet

- Conceptual Frame Work QBDocument15 pagesConceptual Frame Work QBnanthini nanthini100% (1)

- ChronologiqueDocument40 pagesChronologiqueSamseer R HNo ratings yet

- Inter Paper12 Revised PDFDocument788 pagesInter Paper12 Revised PDFbhagyashre100% (1)

- 1 Cpa Financial Accounting Paper 1Document20 pages1 Cpa Financial Accounting Paper 1kajalshiroya17No ratings yet

- Acc 416Document7 pagesAcc 4161sirdeeqNo ratings yet

- Prepared By: CA. Abhijeet N. BobadeDocument9 pagesPrepared By: CA. Abhijeet N. Bobadepsawant77No ratings yet

- Accounts ImpDocument24 pagesAccounts ImphamzafarooqNo ratings yet

- An Introduction International Financial Reporting Standards (IFRS)Document34 pagesAn Introduction International Financial Reporting Standards (IFRS)EshetieNo ratings yet

- Understanding IFRS Fundamentals: International Financial Reporting StandardsFrom EverandUnderstanding IFRS Fundamentals: International Financial Reporting StandardsNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionNo ratings yet

- Part - A: (Financial Accounting - I)Document16 pagesPart - A: (Financial Accounting - I)Adit Bohra VIII BNo ratings yet

- Balance Sheet ProvisionalDocument2 pagesBalance Sheet ProvisionalRaja AdhikariNo ratings yet

- Fixed Assest Management-UltratechDocument6 pagesFixed Assest Management-UltratechMr SmartNo ratings yet

- Consolidations - Subsequent To The Date of Acquisition: Multiple Choice QuestionsDocument290 pagesConsolidations - Subsequent To The Date of Acquisition: Multiple Choice QuestionsKim FloresNo ratings yet

- Chapter 11 - Ho Branch - MillanDocument34 pagesChapter 11 - Ho Branch - MillanAngelica Cerio100% (1)

- Indirect and Mutual HoldingsDocument36 pagesIndirect and Mutual HoldingssiwiNo ratings yet

- Methods For Patent Valuation PDFDocument11 pagesMethods For Patent Valuation PDFSantosh PatiNo ratings yet

- Business Combination Lecture Notes. ACC 401Document4 pagesBusiness Combination Lecture Notes. ACC 401Ugbah Chidinma LilianNo ratings yet

- AC2091 ZB Final For UoLDocument16 pagesAC2091 ZB Final For UoLkikiNo ratings yet

- Depreciation: Disposal of Fixed AssetsDocument13 pagesDepreciation: Disposal of Fixed AssetsHassan AliNo ratings yet

- Sir Mac Book SolmanDocument10 pagesSir Mac Book SolmanJAY AUBREY PINEDANo ratings yet

- Q4-31-03-2022 TMBDocument67 pagesQ4-31-03-2022 TMBDhanush Kumar RamanNo ratings yet

- Accounting For Management Question PaperDocument3 pagesAccounting For Management Question PaperVINOD KUMARNo ratings yet

- DepreciationDocument13 pagesDepreciationHarshitPalNo ratings yet

- Financial Reporting Strathmore University Notes and Revision KitDocument551 pagesFinancial Reporting Strathmore University Notes and Revision KitLazarus AmaniNo ratings yet

- Dhar Textile Mills Balance Sheet, Dhar Textile Mills Financial Statement & AccountsDocument3 pagesDhar Textile Mills Balance Sheet, Dhar Textile Mills Financial Statement & AccountsAkshay BhattNo ratings yet

- Mini MBA B10 - 01 Financial Management - Day 01Document41 pagesMini MBA B10 - 01 Financial Management - Day 01Reza MonoarfaNo ratings yet

- Montajes - Joelyn Grace 117848 Seatwork 2Document9 pagesMontajes - Joelyn Grace 117848 Seatwork 2Joelyn Grace MontajesNo ratings yet

- ERP Operations: SAP Standard ReportsDocument10 pagesERP Operations: SAP Standard ReportsAnkur RastogiNo ratings yet

- Dabur Financial Modeling-Live Project.Document47 pagesDabur Financial Modeling-Live Project.rahul1094No ratings yet

- Interlocal Agreement 8-2-99Document2 pagesInterlocal Agreement 8-2-99williamblueNo ratings yet

- (ESP Merit and Needs Based Scholarship Program) : Instructions For Filling Out The Scholarship Application FormDocument9 pages(ESP Merit and Needs Based Scholarship Program) : Instructions For Filling Out The Scholarship Application FormIffatNo ratings yet

- Amalgamation NotesDocument28 pagesAmalgamation NotesADARSH MISHRANo ratings yet

- Acc311 2021Document4 pagesAcc311 2021hoghidan1No ratings yet

- ACCT 100-Principles of Financial Accounting - Omair HaroonDocument7 pagesACCT 100-Principles of Financial Accounting - Omair HaroonUmar FarooqNo ratings yet