Download as pdf or txt

You might also like

- Cash Flow Statement Problems PDFDocument32 pagesCash Flow Statement Problems PDFnsrivastav181% (31)

- Master Test 04 _ Test Solution (Accounting) __ PDF OnlyDocument13 pagesMaster Test 04 _ Test Solution (Accounting) __ PDF Onlytushar singh rajputNo ratings yet

- Cash Flow Statement of AmulDocument6 pagesCash Flow Statement of AmulArav Sarin60% (5)

- 3 Solution Q.5Document4 pages3 Solution Q.5Aayush AgrawalNo ratings yet

- 1 Financial Statements of CompaniesDocument21 pages1 Financial Statements of CompaniesShivaram ShivaramNo ratings yet

- PART-B Analysis Test YtDocument8 pagesPART-B Analysis Test YtRiddhi GuptaNo ratings yet

- Questions Based On Cashflow StatementDocument3 pagesQuestions Based On Cashflow StatementpuxvashuklaNo ratings yet

- Internal ReconstructionDocument26 pagesInternal ReconstructionRajesh NangaliaNo ratings yet

- Revision Questions XiiDocument11 pagesRevision Questions XiiSahej Kaur AroraNo ratings yet

- Dr. CA RAVI AGARWAL FR COMPILER-1315-1334-11Document1 pageDr. CA RAVI AGARWAL FR COMPILER-1315-1334-11shubham sNo ratings yet

- Cash Flow Statement - 2Document9 pagesCash Flow Statement - 2Midhun PerozhiNo ratings yet

- Cash Flow Statement Xtra Qns Raja Ma'am RecDocument8 pagesCash Flow Statement Xtra Qns Raja Ma'am RecReedhima SrivastavaNo ratings yet

- Master Questions, Advance Level Questions and Additional Questions-Chapter 4Document18 pagesMaster Questions, Advance Level Questions and Additional Questions-Chapter 4manmeet0001No ratings yet

- Accountancy Practical 2023-24-1Document2 pagesAccountancy Practical 2023-24-1uzmazeeshan10No ratings yet

- Clavax Power - TAR - 2023 - Provisional - 10.09Document7 pagesClavax Power - TAR - 2023 - Provisional - 10.09Naresh nath MallickNo ratings yet

- Fund Flow Statement-FR FSADocument27 pagesFund Flow Statement-FR FSADãrk LïghtNo ratings yet

- Solution 18preparation of Financial Statements Company Final AccDocument2 pagesSolution 18preparation of Financial Statements Company Final AccKajal BindalNo ratings yet

- AFM Assignment 2021Document7 pagesAFM Assignment 2021NARENDRA PATTELANo ratings yet

- Proposed DividebdDocument34 pagesProposed DividebdPiyush SrivastavaNo ratings yet

- Acc Practical QuestionsDocument6 pagesAcc Practical QuestionsyogochkeNo ratings yet

- Solution:: Equity and LiabilitiesDocument4 pagesSolution:: Equity and LiabilitiesNIMROD MOCHAHARINo ratings yet

- Accounts Important Questions by Rajat Jain SirDocument31 pagesAccounts Important Questions by Rajat Jain SirRajiv JhaNo ratings yet

- Preparation of Financial Statements - QBDocument26 pagesPreparation of Financial Statements - QBHindutav arya100% (1)

- Accountancy Board Practical Paper - 2020-2021 Class - Xii Time: 1 Hour Max. Marks: 12Document3 pagesAccountancy Board Practical Paper - 2020-2021 Class - Xii Time: 1 Hour Max. Marks: 12Kairav KhuranaNo ratings yet

- Accounting MBA Sem I 2018Document4 pagesAccounting MBA Sem I 2018yogeshgharpureNo ratings yet

- CFS 2023 PyqDocument15 pagesCFS 2023 PyqAnshul JainNo ratings yet

- FR (New) A MTP Final Mar 2021Document17 pagesFR (New) A MTP Final Mar 2021ritz meshNo ratings yet

- Important QuestionsDocument3 pagesImportant QuestionsNayan JainNo ratings yet

- Accounts ProjectDocument29 pagesAccounts ProjectazeemNo ratings yet

- Cash Flow Statement Activity Wise 05-02-24Document7 pagesCash Flow Statement Activity Wise 05-02-24navyabindra28No ratings yet

- Adobe Scan 05 Mar 2022Document5 pagesAdobe Scan 05 Mar 2022Titiksha Joshi100% (1)

- Que PaperDocument7 pagesQue PaperaditikaushikNo ratings yet

- Cash Flow Statement: Particular 31-03-2013 31-03-2012Document2 pagesCash Flow Statement: Particular 31-03-2013 31-03-2012bimbee 13No ratings yet

- Q.1) From The Following Balance Sheet of Kiero Ltd. and The Additional Information As On 31-3-2018 Prepare A Cash Flow StatementDocument5 pagesQ.1) From The Following Balance Sheet of Kiero Ltd. and The Additional Information As On 31-3-2018 Prepare A Cash Flow StatementNoor SehgalNo ratings yet

- Cash Flow StatementDocument10 pagesCash Flow Statementvsy9926No ratings yet

- Master of Business Administration (M.B.A.) Semester-I (C.B.C.S.) Examination Accounting For Managers Compulsory Paper-3Document4 pagesMaster of Business Administration (M.B.A.) Semester-I (C.B.C.S.) Examination Accounting For Managers Compulsory Paper-3Namrata RamgadeNo ratings yet

- Class 12 Accountancy CBSE Cash Flow StatementDocument7 pagesClass 12 Accountancy CBSE Cash Flow StatementSarvesh SreedharNo ratings yet

- PA 2_2022_set BDocument4 pagesPA 2_2022_set BPooja PanjwaniNo ratings yet

- Screenshot 2023-09-20 at 11.30.51 AMDocument1 pageScreenshot 2023-09-20 at 11.30.51 AMprince bhatiaNo ratings yet

- Cash Flow StatementDocument13 pagesCash Flow StatementBISHAL ROYNo ratings yet

- FR SaDocument413 pagesFR SaBabu DinakaranNo ratings yet

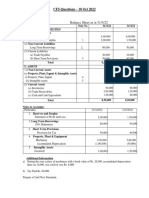

- CFS Questions - 18 - OCT - 2022Document5 pagesCFS Questions - 18 - OCT - 2022Kartik SujanNo ratings yet

- FR Suggested May 2018Document31 pagesFR Suggested May 2018Rahul NandurkarNo ratings yet

- Problem Set of Cash Flow StatementDocument1 pageProblem Set of Cash Flow StatementpriyankaNo ratings yet

- Practice Test (Analysis of Fianacial Statement)Document2 pagesPractice Test (Analysis of Fianacial Statement)j37527802No ratings yet

- CASH FLOW ANALYSIS YTDocument12 pagesCASH FLOW ANALYSIS YTAkashdeep singhNo ratings yet

- Additional Questions 5Document13 pagesAdditional Questions 5Sanjay SiddharthNo ratings yet

- FR - QuestionsDocument8 pagesFR - Questionsrocks007123No ratings yet

- Isc Mock 2Document14 pagesIsc Mock 2anshikajain3474No ratings yet

- Worksheet Tools of Financial Statements of A FirmDocument9 pagesWorksheet Tools of Financial Statements of A FirmpuxvashuklaNo ratings yet

- 9 Consolidated Financial StatementsDocument20 pages9 Consolidated Financial StatementsArpan SinghNo ratings yet

- First Model Test Paper Part - B Time: 40 Minutes Accountancy M.M. 20Document2 pagesFirst Model Test Paper Part - B Time: 40 Minutes Accountancy M.M. 20surbhi singhalNo ratings yet

- Press 'CTRL' + ' (' On The Next Cell For Notes To Accounts: III. Total Revenue (I + II)Document28 pagesPress 'CTRL' + ' (' On The Next Cell For Notes To Accounts: III. Total Revenue (I + II)Anoushka LakhotiaNo ratings yet

- DocumentDocument4 pagesDocumentTûshar ThakúrNo ratings yet

- Xii AccDocument4 pagesXii AccSanjayNo ratings yet

- Question ADV GMDocument11 pagesQuestion ADV GMDharmateja ChakriNo ratings yet

- Andi Woodworks Pvt. Ltd. - 14-15Document17 pagesAndi Woodworks Pvt. Ltd. - 14-15Aayush agarwalNo ratings yet

- Balance Sheet (All Numbers in Thousands) : Break Down 7/30/2020Document16 pagesBalance Sheet (All Numbers in Thousands) : Break Down 7/30/2020Shubham ThakurNo ratings yet

- 027 Practice Test 09 Accounting Test Solution Subjective Udesh RegularDocument6 pages027 Practice Test 09 Accounting Test Solution Subjective Udesh Regulardeathp006No ratings yet

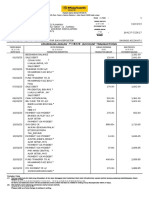

- Bank StatementDocument2 pagesBank Statementjjj81507No ratings yet

- B - Fund - Acc - 1 & 2Document248 pagesB - Fund - Acc - 1 & 2newaybeyene5No ratings yet

- Journal and LedgerDocument23 pagesJournal and Ledgerfarooq.haqiq2012No ratings yet

- Unit 4.2 Partnership LiquidationDocument2 pagesUnit 4.2 Partnership LiquidationBenjamine EscañoNo ratings yet

- Serangoon Broadway Pte. Ltd.Document6 pagesSerangoon Broadway Pte. Ltd.sryxcb5f6zNo ratings yet

- Petty Cash Recon PDFDocument1 pagePetty Cash Recon PDFCristy Martin YumulNo ratings yet

- Ibs TMN Midah, KL 1 31/03/23Document5 pagesIbs TMN Midah, KL 1 31/03/23Nor SharizaNo ratings yet

- Full Download PDF of (Ebook PDF) Cornerstones of Financial Accounting 2nd Canadian Edition All ChapterDocument43 pagesFull Download PDF of (Ebook PDF) Cornerstones of Financial Accounting 2nd Canadian Edition All Chapterphakhijayahr100% (7)

- General Guidelines For Spreading Financial StatementsDocument8 pagesGeneral Guidelines For Spreading Financial StatementsChandan Kumar ShawNo ratings yet

- Find Question 3Document2 pagesFind Question 3hasgonde123No ratings yet

- 03 Partnership Dissolution ANSWERDocument4 pages03 Partnership Dissolution ANSWERKrizza Mae MendozaNo ratings yet

- CH 5Document58 pagesCH 5marwan2004acctNo ratings yet

- Investment in Equity Securities 2Document6 pagesInvestment in Equity Securities 2RomeNo ratings yet

- Makalah Teori Akuntansi - Kelompok 6 - Kelas EDocument28 pagesMakalah Teori Akuntansi - Kelompok 6 - Kelas EBintang Anggara76No ratings yet

- 11th Accountancy EM Book Back 1 Mark Questions 1 English Medium PDF DownloadDocument38 pages11th Accountancy EM Book Back 1 Mark Questions 1 English Medium PDF Downloadlnandhini023No ratings yet

- VCCEdge Fin-TechDocument7 pagesVCCEdge Fin-TechsahilsushilboharaNo ratings yet

- Chapter 4 Investments in Debt Securities and Other Long Term InvestmentDocument30 pagesChapter 4 Investments in Debt Securities and Other Long Term InvestmentAngelica Joy ManaoisNo ratings yet

- Orbis BrochureDocument15 pagesOrbis BrochureBalakrishnan IyerNo ratings yet

- PPT5-Allocation and Depreciation of Differences Between Implied and Book ValuesDocument51 pagesPPT5-Allocation and Depreciation of Differences Between Implied and Book ValuesRifdah SaphiraNo ratings yet

- Illustrative Problems With Solution Problem 1 To 7Document10 pagesIllustrative Problems With Solution Problem 1 To 7Viky Rose EballeNo ratings yet

- Investment Analysis 1Document48 pagesInvestment Analysis 1yonasteweldebrhan87No ratings yet

- Documents Required For Company Registration - Taxguru - inDocument6 pagesDocuments Required For Company Registration - Taxguru - inVyom RajNo ratings yet

- Financial Information Act Return 20140331Document188 pagesFinancial Information Act Return 20140331Mukarom AlatasNo ratings yet

- Finman Pre Mid NotesDocument25 pagesFinman Pre Mid NotesFor ProjectsNo ratings yet

- 2022 Quiz 2 (Solved)Document3 pages2022 Quiz 2 (Solved)Anshuman GuptaNo ratings yet

- Introduction To Financial Statements 18032024 013947pmDocument29 pagesIntroduction To Financial Statements 18032024 013947pmAbdul hanan MalikNo ratings yet

- Speciality ChemicalsDocument32 pagesSpeciality ChemicalsKeshav KhetanNo ratings yet

- Assignment 3 1Document6 pagesAssignment 3 1Siying GuNo ratings yet

- Ass. Chapter 11 Shareholders Equity (Part 2)Document12 pagesAss. Chapter 11 Shareholders Equity (Part 2)Jea Ann CariñozaNo ratings yet

- CH 13 DissolutionDocument25 pagesCH 13 DissolutionRishty PydegaduNo ratings yet