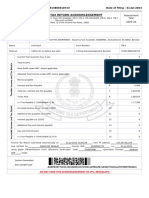

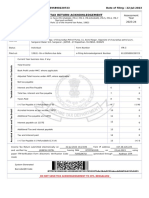

168_36ABUPT4818Q3ZE_VEERASWAMY_THEGULLA_FY_18_19

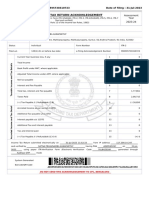

168_36ABUPT4818Q3ZE_VEERASWAMY_THEGULLA_FY_18_19

You might also like

- Bella Frill Dress PDFDocument11 pagesBella Frill Dress PDFChacon R. LastNo ratings yet

- ZF 5hp24Document46 pagesZF 5hp24Davidoff Red100% (1)

- Crime Scene QuizDocument24 pagesCrime Scene Quizjjpietra100% (1)

- Ul 1004-2006Document76 pagesUl 1004-2006Alberto100% (1)

- Ward 20 2 2019-20 07EPCPS5037C1ZZ 0 20240510 031521 820Document11 pagesWard 20 2 2019-20 07EPCPS5037C1ZZ 0 20240510 031521 820Vishal DwivediNo ratings yet

- Shree Suleshvari EnterpriseDocument4 pagesShree Suleshvari EnterpriseDIVISION4 MAHESANANo ratings yet

- Maa Laxmi Hardware 2019-20Document4 pagesMaa Laxmi Hardware 2019-20surendrasharmaofficeNo ratings yet

- Patanjali Arogya Kendra 2018-19Document5 pagesPatanjali Arogya Kendra 2018-19tuensangnagaland2018No ratings yet

- TaxesDocument2 pagesTaxesRameshNadarNo ratings yet

- Digitally Proceedings of P Hanumantharao & Sons 2018-19 S-73Document31 pagesDigitally Proceedings of P Hanumantharao & Sons 2018-19 S-73CTOAUDIT1 BLYNo ratings yet

- REPLYDocument4 pagesREPLYVishal DwivediNo ratings yet

- TYBAF - Indirect Taxation - GST - Set1 - SolutionDocument6 pagesTYBAF - Indirect Taxation - GST - Set1 - Solutionamityadav865783No ratings yet

- VIGHNHARTA LIST FOR INDIRECT TAX MAY-24_240413_192410Document91 pagesVIGHNHARTA LIST FOR INDIRECT TAX MAY-24_240413_192410devikanair482003No ratings yet

- GST Healthcheck Sample Report v1Document148 pagesGST Healthcheck Sample Report v1Gauravkumar KateNo ratings yet

- 22-23 All PagesDocument5 pages22-23 All PagesBulbuli DasNo ratings yet

- GST LatestAmendments Issues 01072023Document85 pagesGST LatestAmendments Issues 01072023Selvakumar MuthurajNo ratings yet

- Page_56Document1 pagePage_56ah94194567No ratings yet

- Annexure To Form GST Drc-07: 21AAVCS9861M1ZF S.N.S. Industrial Works Private LimitedDocument5 pagesAnnexure To Form GST Drc-07: 21AAVCS9861M1ZF S.N.S. Industrial Works Private LimitedBiswajit MishraNo ratings yet

- Mamatha Traders Adjuducation Order Us 73 - CompressedDocument31 pagesMamatha Traders Adjuducation Order Us 73 - Compressedurmilachoudhary1999No ratings yet

- Draft Audit Report XIVDocument11 pagesDraft Audit Report XIVTradingideas2456No ratings yet

- GST ChallanDocument1 pageGST ChallanSanjayThakkarNo ratings yet

- Ranjit ItrrDocument1 pageRanjit ItrrRadha SureshNo ratings yet

- Sri Ram Tech Asmt-10 Cto Sec 2021-22-9Document1 pageSri Ram Tech Asmt-10 Cto Sec 2021-22-9Sunil KumarNo ratings yet

- GST MDLDocument98 pagesGST MDLIndhuja MNo ratings yet

- PDF 115914800310723Document1 pagePDF 115914800310723jayanto chowdhuryNo ratings yet

- TPEPL-ITR-AY-23-24Document1 pageTPEPL-ITR-AY-23-24Vipasha SanghaviNo ratings yet

- Itr 23Document1 pageItr 23vikash pandeyNo ratings yet

- PDF 990595730310723Document1 pagePDF 990595730310723RaviNo ratings yet

- Amendment Booklet NOV 21 - by CA Yachaa Mutha BhuratDocument46 pagesAmendment Booklet NOV 21 - by CA Yachaa Mutha BhuratSuraj BijlaniNo ratings yet

- Rajesh Bora Itr PLBS 2022Document5 pagesRajesh Bora Itr PLBS 2022ABDUL KHALIKNo ratings yet

- Ack 638167400230723Document1 pageAck 638167400230723gamers SatisfactionNo ratings yet

- ProjectDocument1 pageProjectgaganohri0044No ratings yet

- GyfuDocument5 pagesGyfuVenu KumarNo ratings yet

- Ack 343831860020723Document1 pageAck 343831860020723nikhilNo ratings yet

- ilovepdf_merged (24)_compressed_compressed (1) (1)Document35 pagesilovepdf_merged (24)_compressed_compressed (1) (1)bdsconsultant1313No ratings yet

- ilovepdf_merged (24)Document35 pagesilovepdf_merged (24)bdsconsultant1313No ratings yet

- Atlantic Ro Feb 22Document1 pageAtlantic Ro Feb 22Ambati Madhava ReddyNo ratings yet

- Ram Bai Tor OrpaDocument1 pageRam Bai Tor OrpanandsavghNo ratings yet

- Get HandsDocument1 pageGet HandsGaurav kumarNo ratings yet

- Parmjit Singh Itrv Ay 202324Document1 pageParmjit Singh Itrv Ay 202324SANJEEV KUMARNo ratings yet

- Final New Indirect Tax Laws Test 3 Detailed May Solution 1617180255Document17 pagesFinal New Indirect Tax Laws Test 3 Detailed May Solution 1617180255CAtestseriesNo ratings yet

- 1613200874GST Question Bank - May 2021 (With Solutions) PDFDocument157 pages1613200874GST Question Bank - May 2021 (With Solutions) PDFKhusboo ChowdhuryNo ratings yet

- Ack Aadhn6348f 2022-23 220799250290722Document1 pageAck Aadhn6348f 2022-23 220799250290722Akansha JainNo ratings yet

- GST Automated NoticesDocument6 pagesGST Automated NoticesMaunik ParikhNo ratings yet

- Ack Cdhpa3843f 2022-23 220950670290722Document1 pageAck Cdhpa3843f 2022-23 220950670290722rtaxhelp helpNo ratings yet

- Amendments For NOV 21: Amendment in 1 Min Series Available On InstagramDocument32 pagesAmendments For NOV 21: Amendment in 1 Min Series Available On InstagramAakriti SinghalNo ratings yet

- Ack CKLPR7420J 2022-23 366437070310722Document1 pageAck CKLPR7420J 2022-23 366437070310722manishranjan82710No ratings yet

- ITC Notes Sent To B.COM 2023 BatchDocument40 pagesITC Notes Sent To B.COM 2023 BatchViral OkNo ratings yet

- ACK918293970310723Document1 pageACK918293970310723vikash865138No ratings yet

- Ack Abxpb2604f 2022-23 857058350180722 PDFDocument1 pageAck Abxpb2604f 2022-23 857058350180722 PDFVineet KhuranaNo ratings yet

- GSTR3B 03ajdpk8658g1z5 032023Document4 pagesGSTR3B 03ajdpk8658g1z5 032023SANJEEV KUMARNo ratings yet

- Adobe Scan 15 Dec 2023Document1 pageAdobe Scan 15 Dec 2023gandhipl74No ratings yet

- ACK638391570230723Document1 pageACK638391570230723salveakshay1000No ratings yet

- Form No. 16A: From ToDocument2 pagesForm No. 16A: From ToNanu PatelNo ratings yet

- Form16 PDFDocument9 pagesForm16 PDFHarish KumarNo ratings yet

- Form16 (2021-2022)Document2 pagesForm16 (2021-2022)Anushka PoddarNo ratings yet

- Atul Saini 22Document1 pageAtul Saini 22Fascino WhiteNo ratings yet

- Recent Developments in GSTDocument27 pagesRecent Developments in GSTAravindNo ratings yet

- Nation: MarketDocument9 pagesNation: MarketDebashis MitraNo ratings yet

- Indian Income Tax Return Acknowledgement: Acknowledgement Number:611395890220723 Date of Filing: 22-Jul-2023Document1 pageIndian Income Tax Return Acknowledgement: Acknowledgement Number:611395890220723 Date of Filing: 22-Jul-2023Respect InfinityNo ratings yet

- VineetDocument1 pageVineetRiaZ MoHamMaDNo ratings yet

- 23CAYPD4777M1ZX_GSTR3B_Feb2024Document3 pages23CAYPD4777M1ZX_GSTR3B_Feb2024kunalladji158No ratings yet

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisFrom EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisNo ratings yet

- Direct Tax Rulings in 2023 Taxmann Com Research 1704341933Document31 pagesDirect Tax Rulings in 2023 Taxmann Com Research 1704341933funny todaysNo ratings yet

- FCS ModelaDocument3 pagesFCS Modelafunny todaysNo ratings yet

- Electricity BillsDocument15 pagesElectricity Billsfunny todaysNo ratings yet

- FCS SingaraipetDocument14 pagesFCS Singaraipetfunny todaysNo ratings yet

- Book Num 3 CAF DT Regular Batch November 2021Document358 pagesBook Num 3 CAF DT Regular Batch November 2021funny todaysNo ratings yet

- CSI Wildlife: Analyzing Genetic Evidence: Click & Learn Student WorksheetDocument4 pagesCSI Wildlife: Analyzing Genetic Evidence: Click & Learn Student Worksheeta RockaNo ratings yet

- Adobe Scan 22-Aug-2023Document1 pageAdobe Scan 22-Aug-2023Er. Sakshi ChauhanNo ratings yet

- Appointment Letter FormatDocument9 pagesAppointment Letter FormatNiraliNo ratings yet

- BBCG3103 AkhirDocument5 pagesBBCG3103 AkhirTengku Zulhilmi Al HajNo ratings yet

- MR Roshan Ramchandra Patil X 3 PDFDocument2 pagesMR Roshan Ramchandra Patil X 3 PDFVishesh DaveNo ratings yet

- Sex HD MOBILE Pics Ann Angel XXX Ann Angel Ideal Booty Playmate 5Document1 pageSex HD MOBILE Pics Ann Angel XXX Ann Angel Ideal Booty Playmate 5mariawalker47kNo ratings yet

- IbDocument2 pagesIbSrinivasa Reddy KarriNo ratings yet

- Aed NotesDocument83 pagesAed NotesAnnapoornam KNo ratings yet

- Jamuna BankDocument35 pagesJamuna BankMd ShahnewazNo ratings yet

- General Lazaro CardenasDocument6 pagesGeneral Lazaro CardenasDanielZepedaPereaNo ratings yet

- Certification Process GSAustDocument7 pagesCertification Process GSAustBai HuNo ratings yet

- G12 Hello Unit 1 Longman Revision Mr. Mohamed El-SheikhDocument7 pagesG12 Hello Unit 1 Longman Revision Mr. Mohamed El-SheikhMohamed RafatNo ratings yet

- Filipino Citizenship SynthesisDocument17 pagesFilipino Citizenship SynthesisColee StiflerNo ratings yet

- ADCRs NotificationDocument4 pagesADCRs NotificationKhan XadaNo ratings yet

- John Deere Backhoes Dozers Excavators Mini Excavators Skid Steers Wheel Loaders Manuals 6gb DVDDocument24 pagesJohn Deere Backhoes Dozers Excavators Mini Excavators Skid Steers Wheel Loaders Manuals 6gb DVDchristyross211089ntz100% (143)

- Ethical PrinciplesDocument88 pagesEthical PrinciplesMaica QuilangNo ratings yet

- American ExpressDocument2 pagesAmerican Expressshankesh singhNo ratings yet

- Schwarz Dieter-Freemasonry, 1944Document70 pagesSchwarz Dieter-Freemasonry, 1944nicolasflo100% (1)

- Auto ID Generation in T24Document12 pagesAuto ID Generation in T24laksNo ratings yet

- Chapter 1 PA IDocument71 pagesChapter 1 PA Ibeshahashenafe20No ratings yet

- Module 6 - Theo 5Document19 pagesModule 6 - Theo 5Claire G. MagluyanNo ratings yet

- Mind Map For Prophet's Life - TaskadeDocument7 pagesMind Map For Prophet's Life - TaskadeUniba WajidNo ratings yet

- CA San BernardinoDocument6 pagesCA San BernardinotressanavaltaNo ratings yet

- Arti Dixit v. Sushil Kumar Mishra, 2023 SCC OnLine SC 649Document18 pagesArti Dixit v. Sushil Kumar Mishra, 2023 SCC OnLine SC 649Kashish JumaniNo ratings yet

- Why Ferdinand E. Marcos Should Not Be Buried at The Libingan NG Mga Bayani by National Historical Commission of The PhilippinesDocument32 pagesWhy Ferdinand E. Marcos Should Not Be Buried at The Libingan NG Mga Bayani by National Historical Commission of The PhilippinesLittle PakersNo ratings yet

- New Jersey Superior Court Denies AppealDocument26 pagesNew Jersey Superior Court Denies AppealThe TrentonianNo ratings yet

Download as pdf or txt

You might also like

- Bella Frill Dress PDFDocument11 pagesBella Frill Dress PDFChacon R. LastNo ratings yet

- ZF 5hp24Document46 pagesZF 5hp24Davidoff Red100% (1)

- Crime Scene QuizDocument24 pagesCrime Scene Quizjjpietra100% (1)

- Ul 1004-2006Document76 pagesUl 1004-2006Alberto100% (1)

- Ward 20 2 2019-20 07EPCPS5037C1ZZ 0 20240510 031521 820Document11 pagesWard 20 2 2019-20 07EPCPS5037C1ZZ 0 20240510 031521 820Vishal DwivediNo ratings yet

- Shree Suleshvari EnterpriseDocument4 pagesShree Suleshvari EnterpriseDIVISION4 MAHESANANo ratings yet

- Maa Laxmi Hardware 2019-20Document4 pagesMaa Laxmi Hardware 2019-20surendrasharmaofficeNo ratings yet

- Patanjali Arogya Kendra 2018-19Document5 pagesPatanjali Arogya Kendra 2018-19tuensangnagaland2018No ratings yet

- TaxesDocument2 pagesTaxesRameshNadarNo ratings yet

- Digitally Proceedings of P Hanumantharao & Sons 2018-19 S-73Document31 pagesDigitally Proceedings of P Hanumantharao & Sons 2018-19 S-73CTOAUDIT1 BLYNo ratings yet

- REPLYDocument4 pagesREPLYVishal DwivediNo ratings yet

- TYBAF - Indirect Taxation - GST - Set1 - SolutionDocument6 pagesTYBAF - Indirect Taxation - GST - Set1 - Solutionamityadav865783No ratings yet

- VIGHNHARTA LIST FOR INDIRECT TAX MAY-24_240413_192410Document91 pagesVIGHNHARTA LIST FOR INDIRECT TAX MAY-24_240413_192410devikanair482003No ratings yet

- GST Healthcheck Sample Report v1Document148 pagesGST Healthcheck Sample Report v1Gauravkumar KateNo ratings yet

- 22-23 All PagesDocument5 pages22-23 All PagesBulbuli DasNo ratings yet

- GST LatestAmendments Issues 01072023Document85 pagesGST LatestAmendments Issues 01072023Selvakumar MuthurajNo ratings yet

- Page_56Document1 pagePage_56ah94194567No ratings yet

- Annexure To Form GST Drc-07: 21AAVCS9861M1ZF S.N.S. Industrial Works Private LimitedDocument5 pagesAnnexure To Form GST Drc-07: 21AAVCS9861M1ZF S.N.S. Industrial Works Private LimitedBiswajit MishraNo ratings yet

- Mamatha Traders Adjuducation Order Us 73 - CompressedDocument31 pagesMamatha Traders Adjuducation Order Us 73 - Compressedurmilachoudhary1999No ratings yet

- Draft Audit Report XIVDocument11 pagesDraft Audit Report XIVTradingideas2456No ratings yet

- GST ChallanDocument1 pageGST ChallanSanjayThakkarNo ratings yet

- Ranjit ItrrDocument1 pageRanjit ItrrRadha SureshNo ratings yet

- Sri Ram Tech Asmt-10 Cto Sec 2021-22-9Document1 pageSri Ram Tech Asmt-10 Cto Sec 2021-22-9Sunil KumarNo ratings yet

- GST MDLDocument98 pagesGST MDLIndhuja MNo ratings yet

- PDF 115914800310723Document1 pagePDF 115914800310723jayanto chowdhuryNo ratings yet

- TPEPL-ITR-AY-23-24Document1 pageTPEPL-ITR-AY-23-24Vipasha SanghaviNo ratings yet

- Itr 23Document1 pageItr 23vikash pandeyNo ratings yet

- PDF 990595730310723Document1 pagePDF 990595730310723RaviNo ratings yet

- Amendment Booklet NOV 21 - by CA Yachaa Mutha BhuratDocument46 pagesAmendment Booklet NOV 21 - by CA Yachaa Mutha BhuratSuraj BijlaniNo ratings yet

- Rajesh Bora Itr PLBS 2022Document5 pagesRajesh Bora Itr PLBS 2022ABDUL KHALIKNo ratings yet

- Ack 638167400230723Document1 pageAck 638167400230723gamers SatisfactionNo ratings yet

- ProjectDocument1 pageProjectgaganohri0044No ratings yet

- GyfuDocument5 pagesGyfuVenu KumarNo ratings yet

- Ack 343831860020723Document1 pageAck 343831860020723nikhilNo ratings yet

- ilovepdf_merged (24)_compressed_compressed (1) (1)Document35 pagesilovepdf_merged (24)_compressed_compressed (1) (1)bdsconsultant1313No ratings yet

- ilovepdf_merged (24)Document35 pagesilovepdf_merged (24)bdsconsultant1313No ratings yet

- Atlantic Ro Feb 22Document1 pageAtlantic Ro Feb 22Ambati Madhava ReddyNo ratings yet

- Ram Bai Tor OrpaDocument1 pageRam Bai Tor OrpanandsavghNo ratings yet

- Get HandsDocument1 pageGet HandsGaurav kumarNo ratings yet

- Parmjit Singh Itrv Ay 202324Document1 pageParmjit Singh Itrv Ay 202324SANJEEV KUMARNo ratings yet

- Final New Indirect Tax Laws Test 3 Detailed May Solution 1617180255Document17 pagesFinal New Indirect Tax Laws Test 3 Detailed May Solution 1617180255CAtestseriesNo ratings yet

- 1613200874GST Question Bank - May 2021 (With Solutions) PDFDocument157 pages1613200874GST Question Bank - May 2021 (With Solutions) PDFKhusboo ChowdhuryNo ratings yet

- Ack Aadhn6348f 2022-23 220799250290722Document1 pageAck Aadhn6348f 2022-23 220799250290722Akansha JainNo ratings yet

- GST Automated NoticesDocument6 pagesGST Automated NoticesMaunik ParikhNo ratings yet

- Ack Cdhpa3843f 2022-23 220950670290722Document1 pageAck Cdhpa3843f 2022-23 220950670290722rtaxhelp helpNo ratings yet

- Amendments For NOV 21: Amendment in 1 Min Series Available On InstagramDocument32 pagesAmendments For NOV 21: Amendment in 1 Min Series Available On InstagramAakriti SinghalNo ratings yet

- Ack CKLPR7420J 2022-23 366437070310722Document1 pageAck CKLPR7420J 2022-23 366437070310722manishranjan82710No ratings yet

- ITC Notes Sent To B.COM 2023 BatchDocument40 pagesITC Notes Sent To B.COM 2023 BatchViral OkNo ratings yet

- ACK918293970310723Document1 pageACK918293970310723vikash865138No ratings yet

- Ack Abxpb2604f 2022-23 857058350180722 PDFDocument1 pageAck Abxpb2604f 2022-23 857058350180722 PDFVineet KhuranaNo ratings yet

- GSTR3B 03ajdpk8658g1z5 032023Document4 pagesGSTR3B 03ajdpk8658g1z5 032023SANJEEV KUMARNo ratings yet

- Adobe Scan 15 Dec 2023Document1 pageAdobe Scan 15 Dec 2023gandhipl74No ratings yet

- ACK638391570230723Document1 pageACK638391570230723salveakshay1000No ratings yet

- Form No. 16A: From ToDocument2 pagesForm No. 16A: From ToNanu PatelNo ratings yet

- Form16 PDFDocument9 pagesForm16 PDFHarish KumarNo ratings yet

- Form16 (2021-2022)Document2 pagesForm16 (2021-2022)Anushka PoddarNo ratings yet

- Atul Saini 22Document1 pageAtul Saini 22Fascino WhiteNo ratings yet

- Recent Developments in GSTDocument27 pagesRecent Developments in GSTAravindNo ratings yet

- Nation: MarketDocument9 pagesNation: MarketDebashis MitraNo ratings yet

- Indian Income Tax Return Acknowledgement: Acknowledgement Number:611395890220723 Date of Filing: 22-Jul-2023Document1 pageIndian Income Tax Return Acknowledgement: Acknowledgement Number:611395890220723 Date of Filing: 22-Jul-2023Respect InfinityNo ratings yet

- VineetDocument1 pageVineetRiaZ MoHamMaDNo ratings yet

- 23CAYPD4777M1ZX_GSTR3B_Feb2024Document3 pages23CAYPD4777M1ZX_GSTR3B_Feb2024kunalladji158No ratings yet

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisFrom EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisNo ratings yet

- Direct Tax Rulings in 2023 Taxmann Com Research 1704341933Document31 pagesDirect Tax Rulings in 2023 Taxmann Com Research 1704341933funny todaysNo ratings yet

- FCS ModelaDocument3 pagesFCS Modelafunny todaysNo ratings yet

- Electricity BillsDocument15 pagesElectricity Billsfunny todaysNo ratings yet

- FCS SingaraipetDocument14 pagesFCS Singaraipetfunny todaysNo ratings yet

- Book Num 3 CAF DT Regular Batch November 2021Document358 pagesBook Num 3 CAF DT Regular Batch November 2021funny todaysNo ratings yet

- CSI Wildlife: Analyzing Genetic Evidence: Click & Learn Student WorksheetDocument4 pagesCSI Wildlife: Analyzing Genetic Evidence: Click & Learn Student Worksheeta RockaNo ratings yet

- Adobe Scan 22-Aug-2023Document1 pageAdobe Scan 22-Aug-2023Er. Sakshi ChauhanNo ratings yet

- Appointment Letter FormatDocument9 pagesAppointment Letter FormatNiraliNo ratings yet

- BBCG3103 AkhirDocument5 pagesBBCG3103 AkhirTengku Zulhilmi Al HajNo ratings yet

- MR Roshan Ramchandra Patil X 3 PDFDocument2 pagesMR Roshan Ramchandra Patil X 3 PDFVishesh DaveNo ratings yet

- Sex HD MOBILE Pics Ann Angel XXX Ann Angel Ideal Booty Playmate 5Document1 pageSex HD MOBILE Pics Ann Angel XXX Ann Angel Ideal Booty Playmate 5mariawalker47kNo ratings yet

- IbDocument2 pagesIbSrinivasa Reddy KarriNo ratings yet

- Aed NotesDocument83 pagesAed NotesAnnapoornam KNo ratings yet

- Jamuna BankDocument35 pagesJamuna BankMd ShahnewazNo ratings yet

- General Lazaro CardenasDocument6 pagesGeneral Lazaro CardenasDanielZepedaPereaNo ratings yet

- Certification Process GSAustDocument7 pagesCertification Process GSAustBai HuNo ratings yet

- G12 Hello Unit 1 Longman Revision Mr. Mohamed El-SheikhDocument7 pagesG12 Hello Unit 1 Longman Revision Mr. Mohamed El-SheikhMohamed RafatNo ratings yet

- Filipino Citizenship SynthesisDocument17 pagesFilipino Citizenship SynthesisColee StiflerNo ratings yet

- ADCRs NotificationDocument4 pagesADCRs NotificationKhan XadaNo ratings yet

- John Deere Backhoes Dozers Excavators Mini Excavators Skid Steers Wheel Loaders Manuals 6gb DVDDocument24 pagesJohn Deere Backhoes Dozers Excavators Mini Excavators Skid Steers Wheel Loaders Manuals 6gb DVDchristyross211089ntz100% (143)

- Ethical PrinciplesDocument88 pagesEthical PrinciplesMaica QuilangNo ratings yet

- American ExpressDocument2 pagesAmerican Expressshankesh singhNo ratings yet

- Schwarz Dieter-Freemasonry, 1944Document70 pagesSchwarz Dieter-Freemasonry, 1944nicolasflo100% (1)

- Auto ID Generation in T24Document12 pagesAuto ID Generation in T24laksNo ratings yet

- Chapter 1 PA IDocument71 pagesChapter 1 PA Ibeshahashenafe20No ratings yet

- Module 6 - Theo 5Document19 pagesModule 6 - Theo 5Claire G. MagluyanNo ratings yet

- Mind Map For Prophet's Life - TaskadeDocument7 pagesMind Map For Prophet's Life - TaskadeUniba WajidNo ratings yet

- CA San BernardinoDocument6 pagesCA San BernardinotressanavaltaNo ratings yet

- Arti Dixit v. Sushil Kumar Mishra, 2023 SCC OnLine SC 649Document18 pagesArti Dixit v. Sushil Kumar Mishra, 2023 SCC OnLine SC 649Kashish JumaniNo ratings yet

- Why Ferdinand E. Marcos Should Not Be Buried at The Libingan NG Mga Bayani by National Historical Commission of The PhilippinesDocument32 pagesWhy Ferdinand E. Marcos Should Not Be Buried at The Libingan NG Mga Bayani by National Historical Commission of The PhilippinesLittle PakersNo ratings yet

- New Jersey Superior Court Denies AppealDocument26 pagesNew Jersey Superior Court Denies AppealThe TrentonianNo ratings yet