Download as pdf or txt

You might also like

- APICS Dictionary 16thDocument216 pagesAPICS Dictionary 16thnbq6x7w2kqNo ratings yet

- A Project On Cost AnalysisDocument80 pagesA Project On Cost Analysisnet635194% (16)

- Distributorship AgreementDocument8 pagesDistributorship AgreementKrisha Fabia100% (4)

- Far (Q)Document14 pagesFar (Q)Jee Pare100% (1)

- Managing Digital TransformationDocument12 pagesManaging Digital Transformationabhijeetbesu7No ratings yet

- Step by Step Configuration of SAP S4HANA-FI-Part 6Document17 pagesStep by Step Configuration of SAP S4HANA-FI-Part 6Billy BmnNo ratings yet

- Full Project KomulDocument106 pagesFull Project Komulmohan ks80% (10)

- Theory Cost and Management AccountingDocument27 pagesTheory Cost and Management AccountingAnkit ShahNo ratings yet

- Cost AccountingDocument31 pagesCost AccountingRayala SaisrinivasNo ratings yet

- Application of Marginal Costing Technique & Its LimitationDocument25 pagesApplication of Marginal Costing Technique & Its LimitationAjayPatilNo ratings yet

- Cost Accounting Importance and Advantages of Cost Accounting PapaDocument14 pagesCost Accounting Importance and Advantages of Cost Accounting PapaCruz MataNo ratings yet

- Cost Accounting As A Tool For ManagementDocument5 pagesCost Accounting As A Tool For ManagementPurva DalviNo ratings yet

- Cost Accounting1Document134 pagesCost Accounting1Ryan Brown100% (1)

- B.Cost - Accounting 1 BBA3Document10 pagesB.Cost - Accounting 1 BBA3Shivam Kumar ThakurNo ratings yet

- SM 26Document16 pagesSM 26ishaisha1940No ratings yet

- 1.4 Chapter 1 Introduction To Cost AccountingDocument16 pages1.4 Chapter 1 Introduction To Cost Accountingshreyam8550No ratings yet

- Basic Cost Concepts: Learning ObjectivesDocument31 pagesBasic Cost Concepts: Learning Objectivesversatile3No ratings yet

- Cost AccountingDocument19 pagesCost Accountingshubham ThakerNo ratings yet

- Chapter - 8Document26 pagesChapter - 8Rathnakar SarmaNo ratings yet

- Accounting For Business II PM Xii Chapter1Document27 pagesAccounting For Business II PM Xii Chapter1Senthil S. VelNo ratings yet

- Chapter 1Document28 pagesChapter 1Rahila RafiqNo ratings yet

- Course Code - 102 Course Title-Accounting For Business Decisions 2. Learning Objectives of The CourseDocument29 pagesCourse Code - 102 Course Title-Accounting For Business Decisions 2. Learning Objectives of The Courseavinash singhNo ratings yet

- Tools and Techniques of Cost ReductionDocument27 pagesTools and Techniques of Cost Reductionপ্রিয়াঙ্কুর ধর100% (2)

- Sat SundayDocument67 pagesSat SundayGöwdrü KîrâñNo ratings yet

- Ii B.com - 3 Sem-Cost-TheoryDocument19 pagesIi B.com - 3 Sem-Cost-TheoryAR Ananth Rohith BhatNo ratings yet

- Cost Assignment SEM 2 - Integrated-And-Non-Integrated-System-Of-AccountingDocument37 pagesCost Assignment SEM 2 - Integrated-And-Non-Integrated-System-Of-AccountingShubashPoojariNo ratings yet

- 2 Overview of Cost AccountingDocument18 pages2 Overview of Cost AccountingHarsh KhatriNo ratings yet

- Management AccountingDocument20 pagesManagement AccountingPraveen KumarNo ratings yet

- Meaningof Cost AccountingDocument13 pagesMeaningof Cost AccountingEthereal DNo ratings yet

- Costing An Overview of Cost and Management Accounting 1 PDFDocument6 pagesCosting An Overview of Cost and Management Accounting 1 PDFkeerthi100% (2)

- Cost and Management AccountingDocument52 pagesCost and Management Accountings.lakshmi narasimhamNo ratings yet

- Cost AccountingDocument9 pagesCost Accountingyaqoob008No ratings yet

- Accounting For Business II PM Xii Chapter1Document27 pagesAccounting For Business II PM Xii Chapter1Anusga RamasamyNo ratings yet

- Management Accounting IIDocument48 pagesManagement Accounting IIAnonymous Nx2mIiH3sJNo ratings yet

- Cost AccountingDocument35 pagesCost Accountingfaisalkazi2467% (3)

- Nutan Cost AnalysisDocument76 pagesNutan Cost AnalysisBhushan NagalkarNo ratings yet

- Unit 1-IntroductionDocument13 pagesUnit 1-Introductionavinal malikNo ratings yet

- MODULE - 6B Elementary Cost Accounting NotesDocument7 pagesMODULE - 6B Elementary Cost Accounting Noteskatojunior1No ratings yet

- Cost Accounting AssignmentDocument5 pagesCost Accounting AssignmentMargie Therese SanchezNo ratings yet

- Theory Cost AccountingDocument11 pagesTheory Cost AccountingMrinmoy SahaNo ratings yet

- Dbm-215 Cost AccountingDocument116 pagesDbm-215 Cost AccountingJuweriya SolankiNo ratings yet

- Cost AccountancyDocument197 pagesCost AccountancymirjapurNo ratings yet

- Accounting Complte ModuleDocument88 pagesAccounting Complte Modulest0195461No ratings yet

- Defination of Cost AccountingDocument5 pagesDefination of Cost AccountingYaseen Saleem100% (1)

- Unit I Cost Accounting NotesDocument27 pagesUnit I Cost Accounting NotesParmeet KaurNo ratings yet

- UNIT IDocument20 pagesUNIT Ikumaresan palanisamyNo ratings yet

- Cost A:c & BankingDocument130 pagesCost A:c & BankingAbu anas100% (1)

- Module 1 PDFDocument13 pagesModule 1 PDFWaridi GroupNo ratings yet

- ESSAY: This Will Help You Express Your Understanding of The Concept. Answer Each Item Briefly in Complete SentencesDocument6 pagesESSAY: This Will Help You Express Your Understanding of The Concept. Answer Each Item Briefly in Complete Sentencesjustin morenoNo ratings yet

- CH 1 IntroductionDocument20 pagesCH 1 IntroductionKashish BhutadaNo ratings yet

- UNit Costing Study MaterialDocument42 pagesUNit Costing Study MaterialChetana SoniNo ratings yet

- Project (Cost Structure)Document24 pagesProject (Cost Structure)Suvi TRNo ratings yet

- Notes PDFDocument80 pagesNotes PDFRahila Rafiq100% (5)

- Cost Accounting Literature ReviewDocument4 pagesCost Accounting Literature Reviewafmzsawcpkjfzj100% (1)

- Course Title: Cost & Management Accounting Course Code:ACC 205Document37 pagesCourse Title: Cost & Management Accounting Course Code:ACC 205Ishita GuptaNo ratings yet

- Cost AccountingDocument64 pagesCost Accountingningegowda100% (1)

- Introduction To Cost AccountingDocument17 pagesIntroduction To Cost AccountingShadrack KazunguNo ratings yet

- Chapter-1 2022Document36 pagesChapter-1 2022Makai CunananNo ratings yet

- Introduction To Cost AccountingDocument48 pagesIntroduction To Cost AccountingsajjadNo ratings yet

- Bba201 Management & Cost Accounting Unit 2Document24 pagesBba201 Management & Cost Accounting Unit 2Divya MishraNo ratings yet

- The Balanced Scorecard: Turn your data into a roadmap to successFrom EverandThe Balanced Scorecard: Turn your data into a roadmap to successRating: 3.5 out of 5 stars3.5/5 (4)

- "The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"From Everand"The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"No ratings yet

- Cost Reduction Strategies for the Manufacturing Sector With Application of Microsoft ExcelFrom EverandCost Reduction Strategies for the Manufacturing Sector With Application of Microsoft ExcelNo ratings yet

- ENTREPRENEURSHIP AND SMALL BUSINESS - 2023 FINAL NOTEDocument46 pagesENTREPRENEURSHIP AND SMALL BUSINESS - 2023 FINAL NOTEOwusu Agyapong StephenNo ratings yet

- How To Decide Whether Your Group Should IncorporateDocument10 pagesHow To Decide Whether Your Group Should IncorporateOwusu Agyapong StephenNo ratings yet

- Tax InterviewDocument1 pageTax InterviewOwusu Agyapong StephenNo ratings yet

- The Ultimate Guide To Choosing Your Life Partner - Tips and Tricks For Finding The OneDocument3 pagesThe Ultimate Guide To Choosing Your Life Partner - Tips and Tricks For Finding The OneOwusu Agyapong StephenNo ratings yet

- Preboards Exam Part I Answer Key 2Document9 pagesPreboards Exam Part I Answer Key 2Peter ian AutenticoNo ratings yet

- Satisfaction: (Mcdonald'S) : Total Quality Management and How It's Impact On CustomerDocument83 pagesSatisfaction: (Mcdonald'S) : Total Quality Management and How It's Impact On CustomerArchana.p PandeyNo ratings yet

- Managing Current Asset Ch.8Document34 pagesManaging Current Asset Ch.8AimanNo ratings yet

- sl2023 745Document2 pagessl2023 745iodinecoil02No ratings yet

- Funnel Process & SMM: Septian EP, S.PD., M.EngDocument16 pagesFunnel Process & SMM: Septian EP, S.PD., M.Engriski septianingrumNo ratings yet

- How To Start Grow Your Own Law Firm 1700546198Document118 pagesHow To Start Grow Your Own Law Firm 1700546198Farhana SuderNo ratings yet

- Analyzing Marketing Environment of Vietnam AirlinesDocument17 pagesAnalyzing Marketing Environment of Vietnam AirlinesMình Trung Trần VănNo ratings yet

- How Much Cash Does Your Company NeedDocument8 pagesHow Much Cash Does Your Company NeedSairam PrakashNo ratings yet

- Customer Satisfaction Towards JioDocument29 pagesCustomer Satisfaction Towards JioAshwin RNo ratings yet

- Patterns of Entrepreneurship Management 4th Edition Kaplan Test BankDocument7 pagesPatterns of Entrepreneurship Management 4th Edition Kaplan Test Bankcarolaveryygjmztsdix100% (17)

- Example 1 The - Graduate - Employment - Market - and - Emerging - TrendsDocument6 pagesExample 1 The - Graduate - Employment - Market - and - Emerging - Trendsjule160606No ratings yet

- A Strategy Implementation PlanDocument6 pagesA Strategy Implementation Planaran singhNo ratings yet

- Air Deccan: Revolutionizing The Indian SkiesDocument20 pagesAir Deccan: Revolutionizing The Indian Skiessaroj aashmanfoundationNo ratings yet

- Consultancy Project Final Thesis Tootle NepalDocument94 pagesConsultancy Project Final Thesis Tootle NepalJenishNo ratings yet

- The Corporation ReviewDocument2 pagesThe Corporation ReviewMau PeñaNo ratings yet

- Imogyzstan: Introduction To CyberpreneurshipDocument14 pagesImogyzstan: Introduction To CyberpreneurshipsueernNo ratings yet

- Individual Assignment Ibm641Document12 pagesIndividual Assignment Ibm641Cik NoraziemahNo ratings yet

- The Rise and Fall of Fabmart Indias First E CommerceDocument10 pagesThe Rise and Fall of Fabmart Indias First E CommerceJeanus AroraNo ratings yet

- Content SMM Assessment Task 2 - Project Template 2018 (T4-20)Document7 pagesContent SMM Assessment Task 2 - Project Template 2018 (T4-20)elenay0418No ratings yet

- SAP MM-Automatic Creation of Intercompany PO and Billing-2Document26 pagesSAP MM-Automatic Creation of Intercompany PO and Billing-2Rahul PillaiNo ratings yet

- Investable Entrepreneur James Church PDFDocument238 pagesInvestable Entrepreneur James Church PDFAkram HamamNo ratings yet

- Network Design in The Supply Chain 2Document12 pagesNetwork Design in The Supply Chain 2Isaac JebNo ratings yet

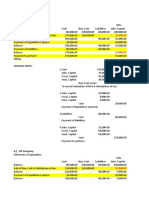

- Solution QUIZ Partnership LiquidationDocument6 pagesSolution QUIZ Partnership Liquidationchezyl cadinongNo ratings yet

- BURATDocument19 pagesBURATLucas MenteNo ratings yet

- 2024 Edelman Trust Barometer Special Report Brands and Politics FinalDocument57 pages2024 Edelman Trust Barometer Special Report Brands and Politics Finaltitusgroan73No ratings yet