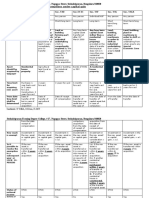

TAX 2 Chapter 3

TAX 2 Chapter 3

You might also like

- Normas NES M1019Document12 pagesNormas NES M1019Margarita Torres FloresNo ratings yet

- MPM TroubleshootingDocument34 pagesMPM TroubleshootingMustafaNo ratings yet

- Topic 8 - Measuring Financial PerformanceDocument60 pagesTopic 8 - Measuring Financial PerformanceThabo ChuchuNo ratings yet

- Chapter 3b - Agriculture AllowanceDocument19 pagesChapter 3b - Agriculture AllowanceNgNo ratings yet

- Chapter 3b - Agriculture AllowanceDocument19 pagesChapter 3b - Agriculture AllowanceNgNo ratings yet

- TAX 467 Topic 4 Capital Allowance - AgricultureDocument11 pagesTAX 467 Topic 4 Capital Allowance - AgricultureAnis RoslanNo ratings yet

- Chapter 3 Agriculture Allowance StudntDocument22 pagesChapter 3 Agriculture Allowance StudntCharmaine Deirdre DaveNo ratings yet

- Agriculture AllowanceDocument17 pagesAgriculture AllowanceKhairun NabilahNo ratings yet

- Sharing Session Agrikultur 15 Desember 2022 UpdateDocument12 pagesSharing Session Agrikultur 15 Desember 2022 UpdateDaniel SinagaNo ratings yet

- Rural & Agri Banking Department, Baroda Sun Tower, 6 Floor, G-Block, Bandra Kurla Complex, Mumbai 400 051, IndiaDocument6 pagesRural & Agri Banking Department, Baroda Sun Tower, 6 Floor, G-Block, Bandra Kurla Complex, Mumbai 400 051, IndiaAnand KumarNo ratings yet

- Capital AllowancesDocument3 pagesCapital AllowancesNurain Nabilah ZakariyaNo ratings yet

- USDA Grain Bin Replacement ProgramDocument2 pagesUSDA Grain Bin Replacement PrograminforumdocsNo ratings yet

- Agricultural Act of 2014Document5 pagesAgricultural Act of 2014Estableciendo el ReinoNo ratings yet

- TOPIC 8 PART 2 Agriculture & ForestDocument44 pagesTOPIC 8 PART 2 Agriculture & Forestanon_171893308No ratings yet

- Agrarian Law Reviewer UNGOS BOOK PDFDocument27 pagesAgrarian Law Reviewer UNGOS BOOK PDFMArk RAy Nicolas Ruma100% (1)

- Agrarian Law Reviewer UNGOS BOOKDocument27 pagesAgrarian Law Reviewer UNGOS BOOKRyan TanamanNo ratings yet

- TAX 2 Chapter 2Document5 pagesTAX 2 Chapter 2dayahdhia24No ratings yet

- Ministry of Agric Farmers AND Ulture Welfare: 1.1. PM Fasal Bima YojanaDocument13 pagesMinistry of Agric Farmers AND Ulture Welfare: 1.1. PM Fasal Bima Yojanamadhuja mukhopadhyayNo ratings yet

- Sacred Heart School - Ateneo de Cebu: High School Social Studies AreaDocument3 pagesSacred Heart School - Ateneo de Cebu: High School Social Studies Area김나연No ratings yet

- Capital Gain ExemptionsDocument2 pagesCapital Gain Exemptions9743081454No ratings yet

- Income Tax Treatment of Agricultural IncomeDocument9 pagesIncome Tax Treatment of Agricultural Incomeprabs2007No ratings yet

- Farming and Farm StockDocument32 pagesFarming and Farm StockMoud KhalfaniNo ratings yet

- Carp Section 1: AGRARIAN LAW - All Laws That Govern and Regulate Rights and RelationshipDocument27 pagesCarp Section 1: AGRARIAN LAW - All Laws That Govern and Regulate Rights and RelationshipEarl Louie MasacayanNo ratings yet

- Tax Unit 1-2 - 1-2Document2 pagesTax Unit 1-2 - 1-2joy BoseNo ratings yet

- CFAS - Biological Assets, Intangibles, and InvestmentsDocument8 pagesCFAS - Biological Assets, Intangibles, and InvestmentsAngelaMariePeñarandaNo ratings yet

- IAS 16 PPE - LectureDocument11 pagesIAS 16 PPE - LectureBeatrice Ella DomingoNo ratings yet

- (Iv) Income Earned From Carrying Nursery Operations Is Also Considered As Agricultural Income and Hence Exempt From Income TaxDocument6 pages(Iv) Income Earned From Carrying Nursery Operations Is Also Considered As Agricultural Income and Hence Exempt From Income TaxMahima SharmaNo ratings yet

- Carp Section 1: Agrarian LawDocument27 pagesCarp Section 1: Agrarian LawAprilyn CelestialNo ratings yet

- Govacc - Financial Assets and Investments: Katrine Celine C. Gutierrez, CPADocument6 pagesGovacc - Financial Assets and Investments: Katrine Celine C. Gutierrez, CPAbobo kaNo ratings yet

- As 10Document34 pagesAs 10Harsh PatelNo ratings yet

- Farm Vehicles and Fuels 2021Document2 pagesFarm Vehicles and Fuels 2021Finn KevinNo ratings yet

- Account PresentationDocument11 pagesAccount PresentationAtul KhotNo ratings yet

- Agra Reviewer 1 UngosDocument33 pagesAgra Reviewer 1 UngosRenzo JamerNo ratings yet

- Ci Program GuideDocument43 pagesCi Program GuideJohan Sebastian EdbertNo ratings yet

- Ecotax: Subsistence Farming Farm OperatorsDocument3 pagesEcotax: Subsistence Farming Farm OperatorssrdazalNo ratings yet

- Sweet Cherry Pilot Crop Provisions 18 0057 SweetDocument7 pagesSweet Cherry Pilot Crop Provisions 18 0057 SweetvivekNo ratings yet

- Reinvestment Allowance (RA) : SCH 7ADocument39 pagesReinvestment Allowance (RA) : SCH 7AchukanchukanchukanNo ratings yet

- Maroc: Evaluation Financiere Du Pro) Et Oliveraie en Agriculture Pluviale Avec Irrigation D' Appoint AuDocument3 pagesMaroc: Evaluation Financiere Du Pro) Et Oliveraie en Agriculture Pluviale Avec Irrigation D' Appoint AuKamel HebbacheNo ratings yet

- Citrus Pilot Crop Provisions 18 0227Document7 pagesCitrus Pilot Crop Provisions 18 0227vivekNo ratings yet

- South Cotabat Consolidated Rice Production Project 1Document6 pagesSouth Cotabat Consolidated Rice Production Project 1RONALD PACOLNo ratings yet

- Choosing Production LevelsDocument43 pagesChoosing Production LevelsLucky GojeNo ratings yet

- Income From AgricultureDocument19 pagesIncome From AgricultureSourav MahadiNo ratings yet

- Agricultural Land and Capital GainsDocument8 pagesAgricultural Land and Capital Gainsrandhir.sinha1592No ratings yet

- AgricultureDocument3 pagesAgricultureolpccjpianonacademicsprincesskNo ratings yet

- Agricultural IncomeDocument12 pagesAgricultural IncomeDipanshu PathakNo ratings yet

- Factors Affecting Agricultural Production: Annex 11Document5 pagesFactors Affecting Agricultural Production: Annex 11Movita NaraineNo ratings yet

- Lesson 3Document11 pagesLesson 3devravidhan382No ratings yet

- Sweet Cherry Pilot Crop Provisions 16 0057Document7 pagesSweet Cherry Pilot Crop Provisions 16 0057vivekNo ratings yet

- TAX On AgriculturalDocument9 pagesTAX On AgriculturalThoom Srideep RaoNo ratings yet

- Fe412farm Module N Cost BenefitDocument34 pagesFe412farm Module N Cost BenefitYaswanth NaikNo ratings yet

- Capital Gain 040313-1Document49 pagesCapital Gain 040313-1cristeenwolf02No ratings yet

- Property Plant and EquipmentDocument11 pagesProperty Plant and EquipmentRyla DocilNo ratings yet

- AC 2101 - Finals Incomplete PDFDocument10 pagesAC 2101 - Finals Incomplete PDFsarahgywneth15No ratings yet

- Global Best Practices in Agropv For Emerging EconomiesDocument20 pagesGlobal Best Practices in Agropv For Emerging EconomiesROHIT BINAY MAHALINo ratings yet

- Chapter 3 Income Exempt From TaxDocument61 pagesChapter 3 Income Exempt From TaxSrishtiNo ratings yet

- Capital Allowances: Zulkhairi@um - Edu. MyDocument35 pagesCapital Allowances: Zulkhairi@um - Edu. MyNero ShaNo ratings yet

- Consultancy - Software DeveloperDocument2 pagesConsultancy - Software DeveloperImadeddinNo ratings yet

- Pengkarya Muda - Aliah BiDocument7 pagesPengkarya Muda - Aliah BiNORHASLIZA BINTI MOHAMAD MoeNo ratings yet

- The Last LessonDocument31 pagesThe Last LessonKanika100% (1)

- Project Summary, WOFDocument2 pagesProject Summary, WOFEsha GargNo ratings yet

- 2020 Msce Practical Questions TargetDocument30 pages2020 Msce Practical Questions TargetspinyblessingNo ratings yet

- Answer KeyDocument21 pagesAnswer KeyJunem S. Beli-otNo ratings yet

- Informative Essays TopicsDocument9 pagesInformative Essays Topicsb725c62j100% (2)

- IPD Rolando AtaDocument2 pagesIPD Rolando AtaMarcela RamosNo ratings yet

- ECON7002: Unemployment and InflationDocument65 pagesECON7002: Unemployment and InflationNima MoaddeliNo ratings yet

- Web-2012-Allison 250-C18 T63-T700 Gas Turbine EngineDocument4 pagesWeb-2012-Allison 250-C18 T63-T700 Gas Turbine Enginekillerghosts666No ratings yet

- Year3 GL Style Maths Practice Paper PrintableDocument4 pagesYear3 GL Style Maths Practice Paper PrintableLolo ImgNo ratings yet

- Security and Privacy Issues: A Survey On Fintech: (Kg71231W, Mqiu, Xs43599N) @pace - EduDocument12 pagesSecurity and Privacy Issues: A Survey On Fintech: (Kg71231W, Mqiu, Xs43599N) @pace - EduthebestNo ratings yet

- Russian General Speaks Out On UFOsDocument7 pagesRussian General Speaks Out On UFOsochaerryNo ratings yet

- Unit 14 - Unemployment and Fiscal Policy - 1.0Document41 pagesUnit 14 - Unemployment and Fiscal Policy - 1.0Georgius Yeremia CandraNo ratings yet

- Phd:304 Lab Report Advanced Mathematical Physics: Sachin Singh Rawat 16PH-06 (Department of Physics)Document12 pagesPhd:304 Lab Report Advanced Mathematical Physics: Sachin Singh Rawat 16PH-06 (Department of Physics)sachin rawatNo ratings yet

- SB KarbonDocument3 pagesSB KarbonAbdul KarimNo ratings yet

- Installation, Operation and Maintenance Manual: Rotoclone LVNDocument23 pagesInstallation, Operation and Maintenance Manual: Rotoclone LVNbertan dağıstanlıNo ratings yet

- Case Digest Extinguishment of ObligationsDocument25 pagesCase Digest Extinguishment of ObligationsLyneth GarciaNo ratings yet

- A320 PedestalDocument14 pagesA320 PedestalAiman ZabadNo ratings yet

- Worksheet 1: The Terms of An AgreementDocument2 pagesWorksheet 1: The Terms of An AgreementJulieta ImbaquingoNo ratings yet

- Legal Reasoning For Seminal U S Texts Constitutional PrinciplesDocument13 pagesLegal Reasoning For Seminal U S Texts Constitutional PrinciplesOlga IgnatyukNo ratings yet

- Week 1 - The Swamp LessonDocument2 pagesWeek 1 - The Swamp LessonEccentricEdwardsNo ratings yet

- Commerce: Paper 7100/01 Multiple ChoiceDocument7 pagesCommerce: Paper 7100/01 Multiple Choicemstudy123456No ratings yet

- PDFDocument86 pagesPDFAnonymous GuMUWwGMNo ratings yet

- Edo Mite GenealogiesDocument23 pagesEdo Mite GenealogiesPeace Matasavaii LeifiNo ratings yet

- Mitc For DisbursementDocument7 pagesMitc For DisbursementMukesh MishraNo ratings yet

- View AnswerDocument112 pagesView Answershiv anantaNo ratings yet

- New Hardcore 3 Month Workout PlanDocument3 pagesNew Hardcore 3 Month Workout PlanCarmen Gonzalez LopezNo ratings yet

Download as docx, pdf, or txt

You might also like

- Normas NES M1019Document12 pagesNormas NES M1019Margarita Torres FloresNo ratings yet

- MPM TroubleshootingDocument34 pagesMPM TroubleshootingMustafaNo ratings yet

- Topic 8 - Measuring Financial PerformanceDocument60 pagesTopic 8 - Measuring Financial PerformanceThabo ChuchuNo ratings yet

- Chapter 3b - Agriculture AllowanceDocument19 pagesChapter 3b - Agriculture AllowanceNgNo ratings yet

- Chapter 3b - Agriculture AllowanceDocument19 pagesChapter 3b - Agriculture AllowanceNgNo ratings yet

- TAX 467 Topic 4 Capital Allowance - AgricultureDocument11 pagesTAX 467 Topic 4 Capital Allowance - AgricultureAnis RoslanNo ratings yet

- Chapter 3 Agriculture Allowance StudntDocument22 pagesChapter 3 Agriculture Allowance StudntCharmaine Deirdre DaveNo ratings yet

- Agriculture AllowanceDocument17 pagesAgriculture AllowanceKhairun NabilahNo ratings yet

- Sharing Session Agrikultur 15 Desember 2022 UpdateDocument12 pagesSharing Session Agrikultur 15 Desember 2022 UpdateDaniel SinagaNo ratings yet

- Rural & Agri Banking Department, Baroda Sun Tower, 6 Floor, G-Block, Bandra Kurla Complex, Mumbai 400 051, IndiaDocument6 pagesRural & Agri Banking Department, Baroda Sun Tower, 6 Floor, G-Block, Bandra Kurla Complex, Mumbai 400 051, IndiaAnand KumarNo ratings yet

- Capital AllowancesDocument3 pagesCapital AllowancesNurain Nabilah ZakariyaNo ratings yet

- USDA Grain Bin Replacement ProgramDocument2 pagesUSDA Grain Bin Replacement PrograminforumdocsNo ratings yet

- Agricultural Act of 2014Document5 pagesAgricultural Act of 2014Estableciendo el ReinoNo ratings yet

- TOPIC 8 PART 2 Agriculture & ForestDocument44 pagesTOPIC 8 PART 2 Agriculture & Forestanon_171893308No ratings yet

- Agrarian Law Reviewer UNGOS BOOK PDFDocument27 pagesAgrarian Law Reviewer UNGOS BOOK PDFMArk RAy Nicolas Ruma100% (1)

- Agrarian Law Reviewer UNGOS BOOKDocument27 pagesAgrarian Law Reviewer UNGOS BOOKRyan TanamanNo ratings yet

- TAX 2 Chapter 2Document5 pagesTAX 2 Chapter 2dayahdhia24No ratings yet

- Ministry of Agric Farmers AND Ulture Welfare: 1.1. PM Fasal Bima YojanaDocument13 pagesMinistry of Agric Farmers AND Ulture Welfare: 1.1. PM Fasal Bima Yojanamadhuja mukhopadhyayNo ratings yet

- Sacred Heart School - Ateneo de Cebu: High School Social Studies AreaDocument3 pagesSacred Heart School - Ateneo de Cebu: High School Social Studies Area김나연No ratings yet

- Capital Gain ExemptionsDocument2 pagesCapital Gain Exemptions9743081454No ratings yet

- Income Tax Treatment of Agricultural IncomeDocument9 pagesIncome Tax Treatment of Agricultural Incomeprabs2007No ratings yet

- Farming and Farm StockDocument32 pagesFarming and Farm StockMoud KhalfaniNo ratings yet

- Carp Section 1: AGRARIAN LAW - All Laws That Govern and Regulate Rights and RelationshipDocument27 pagesCarp Section 1: AGRARIAN LAW - All Laws That Govern and Regulate Rights and RelationshipEarl Louie MasacayanNo ratings yet

- Tax Unit 1-2 - 1-2Document2 pagesTax Unit 1-2 - 1-2joy BoseNo ratings yet

- CFAS - Biological Assets, Intangibles, and InvestmentsDocument8 pagesCFAS - Biological Assets, Intangibles, and InvestmentsAngelaMariePeñarandaNo ratings yet

- IAS 16 PPE - LectureDocument11 pagesIAS 16 PPE - LectureBeatrice Ella DomingoNo ratings yet

- (Iv) Income Earned From Carrying Nursery Operations Is Also Considered As Agricultural Income and Hence Exempt From Income TaxDocument6 pages(Iv) Income Earned From Carrying Nursery Operations Is Also Considered As Agricultural Income and Hence Exempt From Income TaxMahima SharmaNo ratings yet

- Carp Section 1: Agrarian LawDocument27 pagesCarp Section 1: Agrarian LawAprilyn CelestialNo ratings yet

- Govacc - Financial Assets and Investments: Katrine Celine C. Gutierrez, CPADocument6 pagesGovacc - Financial Assets and Investments: Katrine Celine C. Gutierrez, CPAbobo kaNo ratings yet

- As 10Document34 pagesAs 10Harsh PatelNo ratings yet

- Farm Vehicles and Fuels 2021Document2 pagesFarm Vehicles and Fuels 2021Finn KevinNo ratings yet

- Account PresentationDocument11 pagesAccount PresentationAtul KhotNo ratings yet

- Agra Reviewer 1 UngosDocument33 pagesAgra Reviewer 1 UngosRenzo JamerNo ratings yet

- Ci Program GuideDocument43 pagesCi Program GuideJohan Sebastian EdbertNo ratings yet

- Ecotax: Subsistence Farming Farm OperatorsDocument3 pagesEcotax: Subsistence Farming Farm OperatorssrdazalNo ratings yet

- Sweet Cherry Pilot Crop Provisions 18 0057 SweetDocument7 pagesSweet Cherry Pilot Crop Provisions 18 0057 SweetvivekNo ratings yet

- Reinvestment Allowance (RA) : SCH 7ADocument39 pagesReinvestment Allowance (RA) : SCH 7AchukanchukanchukanNo ratings yet

- Maroc: Evaluation Financiere Du Pro) Et Oliveraie en Agriculture Pluviale Avec Irrigation D' Appoint AuDocument3 pagesMaroc: Evaluation Financiere Du Pro) Et Oliveraie en Agriculture Pluviale Avec Irrigation D' Appoint AuKamel HebbacheNo ratings yet

- Citrus Pilot Crop Provisions 18 0227Document7 pagesCitrus Pilot Crop Provisions 18 0227vivekNo ratings yet

- South Cotabat Consolidated Rice Production Project 1Document6 pagesSouth Cotabat Consolidated Rice Production Project 1RONALD PACOLNo ratings yet

- Choosing Production LevelsDocument43 pagesChoosing Production LevelsLucky GojeNo ratings yet

- Income From AgricultureDocument19 pagesIncome From AgricultureSourav MahadiNo ratings yet

- Agricultural Land and Capital GainsDocument8 pagesAgricultural Land and Capital Gainsrandhir.sinha1592No ratings yet

- AgricultureDocument3 pagesAgricultureolpccjpianonacademicsprincesskNo ratings yet

- Agricultural IncomeDocument12 pagesAgricultural IncomeDipanshu PathakNo ratings yet

- Factors Affecting Agricultural Production: Annex 11Document5 pagesFactors Affecting Agricultural Production: Annex 11Movita NaraineNo ratings yet

- Lesson 3Document11 pagesLesson 3devravidhan382No ratings yet

- Sweet Cherry Pilot Crop Provisions 16 0057Document7 pagesSweet Cherry Pilot Crop Provisions 16 0057vivekNo ratings yet

- TAX On AgriculturalDocument9 pagesTAX On AgriculturalThoom Srideep RaoNo ratings yet

- Fe412farm Module N Cost BenefitDocument34 pagesFe412farm Module N Cost BenefitYaswanth NaikNo ratings yet

- Capital Gain 040313-1Document49 pagesCapital Gain 040313-1cristeenwolf02No ratings yet

- Property Plant and EquipmentDocument11 pagesProperty Plant and EquipmentRyla DocilNo ratings yet

- AC 2101 - Finals Incomplete PDFDocument10 pagesAC 2101 - Finals Incomplete PDFsarahgywneth15No ratings yet

- Global Best Practices in Agropv For Emerging EconomiesDocument20 pagesGlobal Best Practices in Agropv For Emerging EconomiesROHIT BINAY MAHALINo ratings yet

- Chapter 3 Income Exempt From TaxDocument61 pagesChapter 3 Income Exempt From TaxSrishtiNo ratings yet

- Capital Allowances: Zulkhairi@um - Edu. MyDocument35 pagesCapital Allowances: Zulkhairi@um - Edu. MyNero ShaNo ratings yet

- Consultancy - Software DeveloperDocument2 pagesConsultancy - Software DeveloperImadeddinNo ratings yet

- Pengkarya Muda - Aliah BiDocument7 pagesPengkarya Muda - Aliah BiNORHASLIZA BINTI MOHAMAD MoeNo ratings yet

- The Last LessonDocument31 pagesThe Last LessonKanika100% (1)

- Project Summary, WOFDocument2 pagesProject Summary, WOFEsha GargNo ratings yet

- 2020 Msce Practical Questions TargetDocument30 pages2020 Msce Practical Questions TargetspinyblessingNo ratings yet

- Answer KeyDocument21 pagesAnswer KeyJunem S. Beli-otNo ratings yet

- Informative Essays TopicsDocument9 pagesInformative Essays Topicsb725c62j100% (2)

- IPD Rolando AtaDocument2 pagesIPD Rolando AtaMarcela RamosNo ratings yet

- ECON7002: Unemployment and InflationDocument65 pagesECON7002: Unemployment and InflationNima MoaddeliNo ratings yet

- Web-2012-Allison 250-C18 T63-T700 Gas Turbine EngineDocument4 pagesWeb-2012-Allison 250-C18 T63-T700 Gas Turbine Enginekillerghosts666No ratings yet

- Year3 GL Style Maths Practice Paper PrintableDocument4 pagesYear3 GL Style Maths Practice Paper PrintableLolo ImgNo ratings yet

- Security and Privacy Issues: A Survey On Fintech: (Kg71231W, Mqiu, Xs43599N) @pace - EduDocument12 pagesSecurity and Privacy Issues: A Survey On Fintech: (Kg71231W, Mqiu, Xs43599N) @pace - EduthebestNo ratings yet

- Russian General Speaks Out On UFOsDocument7 pagesRussian General Speaks Out On UFOsochaerryNo ratings yet

- Unit 14 - Unemployment and Fiscal Policy - 1.0Document41 pagesUnit 14 - Unemployment and Fiscal Policy - 1.0Georgius Yeremia CandraNo ratings yet

- Phd:304 Lab Report Advanced Mathematical Physics: Sachin Singh Rawat 16PH-06 (Department of Physics)Document12 pagesPhd:304 Lab Report Advanced Mathematical Physics: Sachin Singh Rawat 16PH-06 (Department of Physics)sachin rawatNo ratings yet

- SB KarbonDocument3 pagesSB KarbonAbdul KarimNo ratings yet

- Installation, Operation and Maintenance Manual: Rotoclone LVNDocument23 pagesInstallation, Operation and Maintenance Manual: Rotoclone LVNbertan dağıstanlıNo ratings yet

- Case Digest Extinguishment of ObligationsDocument25 pagesCase Digest Extinguishment of ObligationsLyneth GarciaNo ratings yet

- A320 PedestalDocument14 pagesA320 PedestalAiman ZabadNo ratings yet

- Worksheet 1: The Terms of An AgreementDocument2 pagesWorksheet 1: The Terms of An AgreementJulieta ImbaquingoNo ratings yet

- Legal Reasoning For Seminal U S Texts Constitutional PrinciplesDocument13 pagesLegal Reasoning For Seminal U S Texts Constitutional PrinciplesOlga IgnatyukNo ratings yet

- Week 1 - The Swamp LessonDocument2 pagesWeek 1 - The Swamp LessonEccentricEdwardsNo ratings yet

- Commerce: Paper 7100/01 Multiple ChoiceDocument7 pagesCommerce: Paper 7100/01 Multiple Choicemstudy123456No ratings yet

- PDFDocument86 pagesPDFAnonymous GuMUWwGMNo ratings yet

- Edo Mite GenealogiesDocument23 pagesEdo Mite GenealogiesPeace Matasavaii LeifiNo ratings yet

- Mitc For DisbursementDocument7 pagesMitc For DisbursementMukesh MishraNo ratings yet

- View AnswerDocument112 pagesView Answershiv anantaNo ratings yet

- New Hardcore 3 Month Workout PlanDocument3 pagesNew Hardcore 3 Month Workout PlanCarmen Gonzalez LopezNo ratings yet