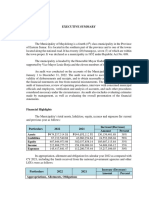

Metropolitan-Naga-Water-District-Camarines-Sur-Executive-Summary-2020

Metropolitan-Naga-Water-District-Camarines-Sur-Executive-Summary-2020

You might also like

- Chinese Creation MythDocument4 pagesChinese Creation MythprominusNo ratings yet

- Strategic Planning & Budget Essentials Part - 2 by GartnerDocument26 pagesStrategic Planning & Budget Essentials Part - 2 by GartnerRavi Teja ChillaraNo ratings yet

- International TradeDocument5 pagesInternational TradeAsif Nawaz ArishNo ratings yet

- Catarman Executive Summary 2019Document7 pagesCatarman Executive Summary 2019Jeanine IlaganNo ratings yet

- General MacArthur Executive Summary 2020Document6 pagesGeneral MacArthur Executive Summary 2020Ma. Danice Angela Balde-BarcomaNo ratings yet

- Bayambang Water District Executive Summary 2020Document5 pagesBayambang Water District Executive Summary 2020Paul De LeonNo ratings yet

- Nueva Vizcaya Executive Summary 2020Document11 pagesNueva Vizcaya Executive Summary 2020Emille MercadoNo ratings yet

- 03-SBMA2020 Executive SummaryDocument7 pages03-SBMA2020 Executive SummaryCharlie Maine TorresNo ratings yet

- Dolores Executive Summary 2020Document6 pagesDolores Executive Summary 2020Ma. Danice Angela Balde-BarcomaNo ratings yet

- Carmen Executive Summary 2020Document8 pagesCarmen Executive Summary 2020Johanna Mae AutidaNo ratings yet

- Matuguinao Samar ES2020Document3 pagesMatuguinao Samar ES2020Desir ArmanNo ratings yet

- Masbate City Executive Summary 2022Document5 pagesMasbate City Executive Summary 2022nicolegardia106No ratings yet

- Maydolong Executive Summary 2022Document4 pagesMaydolong Executive Summary 2022Floydlizamarie PatualNo ratings yet

- PalawanProv ES2019Document11 pagesPalawanProv ES2019Smile Laugh and Be InspiredNo ratings yet

- Caraga State University Executive Summary 2021Document6 pagesCaraga State University Executive Summary 2021Miss_AccountantNo ratings yet

- Tubod Executive SummaryDocument4 pagesTubod Executive SummaryPatrick Lenard Villaluz JaynarioNo ratings yet

- Bayombong Executive Summary 2021Document8 pagesBayombong Executive Summary 2021Aika KimNo ratings yet

- 04-ZCSEZA2021 Executive SummaryDocument5 pages04-ZCSEZA2021 Executive SummaryBaliv MozamNo ratings yet

- Executive Summary: A. IntroductionDocument5 pagesExecutive Summary: A. IntroductionChiara Melanie ButawanNo ratings yet

- Misamis Oriental Executive Summary 2020Document7 pagesMisamis Oriental Executive Summary 2020Sen LinNo ratings yet

- Malaybalay City Water District Executive Summary 2018Document3 pagesMalaybalay City Water District Executive Summary 2018Dindin OrocioIsorenNo ratings yet

- Mayantoc Executive Summary 2022Document8 pagesMayantoc Executive Summary 2022John NicosNo ratings yet

- Calbiga Samar ES2020Document6 pagesCalbiga Samar ES2020Desir ArmanNo ratings yet

- Toledo City Water District Cebu Executive Summary 2020Document5 pagesToledo City Water District Cebu Executive Summary 2020Maria CharessaNo ratings yet

- Binalonan Water District Pangasinan Executive Summary 2022Document5 pagesBinalonan Water District Pangasinan Executive Summary 2022Joseph CajoteNo ratings yet

- Apayao Executive Summary 2020Document5 pagesApayao Executive Summary 2020Franz SyNo ratings yet

- Iba Executive Summary 2022Document8 pagesIba Executive Summary 2022Lance LagundiNo ratings yet

- Masbate-Executive-Summary-2023 SadiasaDocument8 pagesMasbate-Executive-Summary-2023 SadiasaFranz SyNo ratings yet

- Santa Maria Executive Summary 2013Document4 pagesSanta Maria Executive Summary 2013kaixuxu2No ratings yet

- Bocaue Executive SummaryDocument6 pagesBocaue Executive SummaryWubba Lubba Dub DubNo ratings yet

- Metro Bangued Water District Abra Executive Summary 2021Document3 pagesMetro Bangued Water District Abra Executive Summary 2021DBM-CAR Feliza AlosNo ratings yet

- Local Water Utilities Administration Executive Summary 2020 PDFDocument6 pagesLocal Water Utilities Administration Executive Summary 2020 PDFJohn Archie SerranoNo ratings yet

- Banga Executive Summary 2018 PDFDocument5 pagesBanga Executive Summary 2018 PDFMohammadNo ratings yet

- Socorro Water District Surigao Del Norte Executive Summary 2021Document4 pagesSocorro Water District Surigao Del Norte Executive Summary 2021Miss_AccountantNo ratings yet

- Pinamalayan Executive Summary 2022Document10 pagesPinamalayan Executive Summary 2022Jean Monique TolentinoNo ratings yet

- Philippine Drug Enforcement Agency Executive Summary 2020Document4 pagesPhilippine Drug Enforcement Agency Executive Summary 2020jancel maeNo ratings yet

- Labason Water District Zamboanga Del Norte Executive Summary 2021Document5 pagesLabason Water District Zamboanga Del Norte Executive Summary 2021Lady Lynn PosadasNo ratings yet

- Visayas State University Executive Summary 2022Document11 pagesVisayas State University Executive Summary 2022gkxmtlemNo ratings yet

- Atok Benguet Source3 PDFDocument4 pagesAtok Benguet Source3 PDFkaye carrancejaNo ratings yet

- Executive Summary 2020Document5 pagesExecutive Summary 2020Marc CabreraNo ratings yet

- San Luis Executive Summary 2020Document5 pagesSan Luis Executive Summary 2020The ApprenticeNo ratings yet

- Salcedo Executive Summary 2015Document7 pagesSalcedo Executive Summary 2015davilaalexamayNo ratings yet

- San Ildefonso Executive Summary 2014Document5 pagesSan Ildefonso Executive Summary 2014Fritz MainarNo ratings yet

- Amulung Water District Cagayan Executive Summary 2021Document5 pagesAmulung Water District Cagayan Executive Summary 2021Okay AkoNo ratings yet

- 04-MunCantilan2019 Executive SummaryDocument7 pages04-MunCantilan2019 Executive Summarysandra bolokNo ratings yet

- Penablanca Water District Cagayan Executive Summary 2022Document5 pagesPenablanca Water District Cagayan Executive Summary 2022Marlon FernandoNo ratings yet

- Nabas Executive Summary 2019Document6 pagesNabas Executive Summary 2019Marlon FernandoNo ratings yet

- Carcar Water District Cebu Executive Summary 2020Document5 pagesCarcar Water District Cebu Executive Summary 2020PatrickNo ratings yet

- 03-Estancia2022 Executive SummaryDocument4 pages03-Estancia2022 Executive SummaryEi Mi SanNo ratings yet

- Zamboanga City Water District 2018 Executive SummaryDocument6 pagesZamboanga City Water District 2018 Executive SummaryBaliv MozamNo ratings yet

- Aborlan Executive Summary 2019Document6 pagesAborlan Executive Summary 2019Arly TolentinoNo ratings yet

- Taytay Water District Executive Summary 2018Document6 pagesTaytay Water District Executive Summary 2018Allan SobrepeñaNo ratings yet

- 03-DRT2019 Executive SummaryDocument6 pages03-DRT2019 Executive SummaryGiovanni MartinNo ratings yet

- Bureau of Local Government Finance Executive Summary 2019Document5 pagesBureau of Local Government Finance Executive Summary 2019renelynarbisNo ratings yet

- Chapter 6 PDFDocument23 pagesChapter 6 PDFreyNo ratings yet

- General Santos City Executive Summary 2019Document5 pagesGeneral Santos City Executive Summary 2019Princess Alyssa AbidNo ratings yet

- Binalonan Water District Executive Summary 2020Document4 pagesBinalonan Water District Executive Summary 2020michelangelo lemonNo ratings yet

- La Paz Executive Summary 2021Document5 pagesLa Paz Executive Summary 2021Jeffrey RiveraNo ratings yet

- 03-MWSS2018 Executive SummaryDocument4 pages03-MWSS2018 Executive SummaryEljoe VinluanNo ratings yet

- Surigao Del Norte State University Executive Summary 2022Document8 pagesSurigao Del Norte State University Executive Summary 2022Noli BenongoNo ratings yet

- Cagayan Executive Summary 2022Document5 pagesCagayan Executive Summary 2022Arjimar BaloyoNo ratings yet

- San Isidro Executive Summary 2022Document13 pagesSan Isidro Executive Summary 2022Ronel CadelinoNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- Northern Christian College: The Institution For Better LifeDocument22 pagesNorthern Christian College: The Institution For Better Lifenananana123No ratings yet

- Bell Atlantic Corp v. TwomblyDocument4 pagesBell Atlantic Corp v. Twomblylfei1216No ratings yet

- Thermae RomaeDocument11 pagesThermae RomaeBerenice RamírezNo ratings yet

- CV Sample FormatDocument6 pagesCV Sample FormatVijay MindfireNo ratings yet

- Brochure FDP On 5G Wireless CommunicationsDocument2 pagesBrochure FDP On 5G Wireless CommunicationsevolvingsatNo ratings yet

- Pts B.ing 21-22Document5 pagesPts B.ing 21-22YantisYtNo ratings yet

- S.Shiva Enterprises: Jagat AutomobilesDocument2 pagesS.Shiva Enterprises: Jagat AutomobilesS.SHIVA ENTERPRISESNo ratings yet

- Literature Review of Service Quality in RestaurantsDocument7 pagesLiterature Review of Service Quality in RestaurantsuifjzvrifNo ratings yet

- A Quick Guide To The Employment Rights Act: OcumentationDocument4 pagesA Quick Guide To The Employment Rights Act: OcumentationGeorgia SimmsNo ratings yet

- Mudarabah by Sheikh Muhammad Taqi UsmaniDocument5 pagesMudarabah by Sheikh Muhammad Taqi UsmaniMUSALMAN BHAINo ratings yet

- Simulacro 3 GildaDocument27 pagesSimulacro 3 GildamauricioNo ratings yet

- 13mar2020 Week11Document16 pages13mar2020 Week11cerejagroselhaNo ratings yet

- Get Set Case - WeRock - IIM KozhikodeDocument7 pagesGet Set Case - WeRock - IIM KozhikodeKESHAV RATHI 01No ratings yet

- Bear Stearns and The Seeds of Its DemiseDocument15 pagesBear Stearns and The Seeds of Its DemiseJaja JANo ratings yet

- 101-98-Magazine For The Month of March-2022-FinalDocument138 pages101-98-Magazine For The Month of March-2022-FinalPratyush BalNo ratings yet

- KAPILA User Guide 2023-24Document12 pagesKAPILA User Guide 2023-24SUTHANRAJ K SEC 2020No ratings yet

- Artiste List CompleteDocument165 pagesArtiste List CompleteDorego TaofeeqNo ratings yet

- Energy Management in An Automated Solar Powered Irrigation SystemDocument6 pagesEnergy Management in An Automated Solar Powered Irrigation Systemdivya1587No ratings yet

- Velcan Energy Company Profile Dec 2015Document22 pagesVelcan Energy Company Profile Dec 2015filipandNo ratings yet

- Businessline 1101Document32 pagesBusinessline 1101Seok Jun YoonNo ratings yet

- Brochure Final PDFDocument2 pagesBrochure Final PDFCarl Warren RodriguezNo ratings yet

- Human Action: A Treatise On Economics by Ludwig Von MisesDocument6 pagesHuman Action: A Treatise On Economics by Ludwig Von MisesHospodar VibescuNo ratings yet

- Tajweed TerminologyDocument2 pagesTajweed TerminologyJawedsIslamicLibraryNo ratings yet

- Lesson Plan in Teaching Mapeh 8Document9 pagesLesson Plan in Teaching Mapeh 8Kimverly zhaira DomaganNo ratings yet

- English Core 5Document14 pagesEnglish Core 5Tanu Singh100% (1)

- Quita v. Court of AppealsDocument6 pagesQuita v. Court of AppealsShairaCamilleGarciaNo ratings yet

- John Read Middle School - Class of 2011Document1 pageJohn Read Middle School - Class of 2011Hersam AcornNo ratings yet

Download as pdf or txt

You might also like

- Chinese Creation MythDocument4 pagesChinese Creation MythprominusNo ratings yet

- Strategic Planning & Budget Essentials Part - 2 by GartnerDocument26 pagesStrategic Planning & Budget Essentials Part - 2 by GartnerRavi Teja ChillaraNo ratings yet

- International TradeDocument5 pagesInternational TradeAsif Nawaz ArishNo ratings yet

- Catarman Executive Summary 2019Document7 pagesCatarman Executive Summary 2019Jeanine IlaganNo ratings yet

- General MacArthur Executive Summary 2020Document6 pagesGeneral MacArthur Executive Summary 2020Ma. Danice Angela Balde-BarcomaNo ratings yet

- Bayambang Water District Executive Summary 2020Document5 pagesBayambang Water District Executive Summary 2020Paul De LeonNo ratings yet

- Nueva Vizcaya Executive Summary 2020Document11 pagesNueva Vizcaya Executive Summary 2020Emille MercadoNo ratings yet

- 03-SBMA2020 Executive SummaryDocument7 pages03-SBMA2020 Executive SummaryCharlie Maine TorresNo ratings yet

- Dolores Executive Summary 2020Document6 pagesDolores Executive Summary 2020Ma. Danice Angela Balde-BarcomaNo ratings yet

- Carmen Executive Summary 2020Document8 pagesCarmen Executive Summary 2020Johanna Mae AutidaNo ratings yet

- Matuguinao Samar ES2020Document3 pagesMatuguinao Samar ES2020Desir ArmanNo ratings yet

- Masbate City Executive Summary 2022Document5 pagesMasbate City Executive Summary 2022nicolegardia106No ratings yet

- Maydolong Executive Summary 2022Document4 pagesMaydolong Executive Summary 2022Floydlizamarie PatualNo ratings yet

- PalawanProv ES2019Document11 pagesPalawanProv ES2019Smile Laugh and Be InspiredNo ratings yet

- Caraga State University Executive Summary 2021Document6 pagesCaraga State University Executive Summary 2021Miss_AccountantNo ratings yet

- Tubod Executive SummaryDocument4 pagesTubod Executive SummaryPatrick Lenard Villaluz JaynarioNo ratings yet

- Bayombong Executive Summary 2021Document8 pagesBayombong Executive Summary 2021Aika KimNo ratings yet

- 04-ZCSEZA2021 Executive SummaryDocument5 pages04-ZCSEZA2021 Executive SummaryBaliv MozamNo ratings yet

- Executive Summary: A. IntroductionDocument5 pagesExecutive Summary: A. IntroductionChiara Melanie ButawanNo ratings yet

- Misamis Oriental Executive Summary 2020Document7 pagesMisamis Oriental Executive Summary 2020Sen LinNo ratings yet

- Malaybalay City Water District Executive Summary 2018Document3 pagesMalaybalay City Water District Executive Summary 2018Dindin OrocioIsorenNo ratings yet

- Mayantoc Executive Summary 2022Document8 pagesMayantoc Executive Summary 2022John NicosNo ratings yet

- Calbiga Samar ES2020Document6 pagesCalbiga Samar ES2020Desir ArmanNo ratings yet

- Toledo City Water District Cebu Executive Summary 2020Document5 pagesToledo City Water District Cebu Executive Summary 2020Maria CharessaNo ratings yet

- Binalonan Water District Pangasinan Executive Summary 2022Document5 pagesBinalonan Water District Pangasinan Executive Summary 2022Joseph CajoteNo ratings yet

- Apayao Executive Summary 2020Document5 pagesApayao Executive Summary 2020Franz SyNo ratings yet

- Iba Executive Summary 2022Document8 pagesIba Executive Summary 2022Lance LagundiNo ratings yet

- Masbate-Executive-Summary-2023 SadiasaDocument8 pagesMasbate-Executive-Summary-2023 SadiasaFranz SyNo ratings yet

- Santa Maria Executive Summary 2013Document4 pagesSanta Maria Executive Summary 2013kaixuxu2No ratings yet

- Bocaue Executive SummaryDocument6 pagesBocaue Executive SummaryWubba Lubba Dub DubNo ratings yet

- Metro Bangued Water District Abra Executive Summary 2021Document3 pagesMetro Bangued Water District Abra Executive Summary 2021DBM-CAR Feliza AlosNo ratings yet

- Local Water Utilities Administration Executive Summary 2020 PDFDocument6 pagesLocal Water Utilities Administration Executive Summary 2020 PDFJohn Archie SerranoNo ratings yet

- Banga Executive Summary 2018 PDFDocument5 pagesBanga Executive Summary 2018 PDFMohammadNo ratings yet

- Socorro Water District Surigao Del Norte Executive Summary 2021Document4 pagesSocorro Water District Surigao Del Norte Executive Summary 2021Miss_AccountantNo ratings yet

- Pinamalayan Executive Summary 2022Document10 pagesPinamalayan Executive Summary 2022Jean Monique TolentinoNo ratings yet

- Philippine Drug Enforcement Agency Executive Summary 2020Document4 pagesPhilippine Drug Enforcement Agency Executive Summary 2020jancel maeNo ratings yet

- Labason Water District Zamboanga Del Norte Executive Summary 2021Document5 pagesLabason Water District Zamboanga Del Norte Executive Summary 2021Lady Lynn PosadasNo ratings yet

- Visayas State University Executive Summary 2022Document11 pagesVisayas State University Executive Summary 2022gkxmtlemNo ratings yet

- Atok Benguet Source3 PDFDocument4 pagesAtok Benguet Source3 PDFkaye carrancejaNo ratings yet

- Executive Summary 2020Document5 pagesExecutive Summary 2020Marc CabreraNo ratings yet

- San Luis Executive Summary 2020Document5 pagesSan Luis Executive Summary 2020The ApprenticeNo ratings yet

- Salcedo Executive Summary 2015Document7 pagesSalcedo Executive Summary 2015davilaalexamayNo ratings yet

- San Ildefonso Executive Summary 2014Document5 pagesSan Ildefonso Executive Summary 2014Fritz MainarNo ratings yet

- Amulung Water District Cagayan Executive Summary 2021Document5 pagesAmulung Water District Cagayan Executive Summary 2021Okay AkoNo ratings yet

- 04-MunCantilan2019 Executive SummaryDocument7 pages04-MunCantilan2019 Executive Summarysandra bolokNo ratings yet

- Penablanca Water District Cagayan Executive Summary 2022Document5 pagesPenablanca Water District Cagayan Executive Summary 2022Marlon FernandoNo ratings yet

- Nabas Executive Summary 2019Document6 pagesNabas Executive Summary 2019Marlon FernandoNo ratings yet

- Carcar Water District Cebu Executive Summary 2020Document5 pagesCarcar Water District Cebu Executive Summary 2020PatrickNo ratings yet

- 03-Estancia2022 Executive SummaryDocument4 pages03-Estancia2022 Executive SummaryEi Mi SanNo ratings yet

- Zamboanga City Water District 2018 Executive SummaryDocument6 pagesZamboanga City Water District 2018 Executive SummaryBaliv MozamNo ratings yet

- Aborlan Executive Summary 2019Document6 pagesAborlan Executive Summary 2019Arly TolentinoNo ratings yet

- Taytay Water District Executive Summary 2018Document6 pagesTaytay Water District Executive Summary 2018Allan SobrepeñaNo ratings yet

- 03-DRT2019 Executive SummaryDocument6 pages03-DRT2019 Executive SummaryGiovanni MartinNo ratings yet

- Bureau of Local Government Finance Executive Summary 2019Document5 pagesBureau of Local Government Finance Executive Summary 2019renelynarbisNo ratings yet

- Chapter 6 PDFDocument23 pagesChapter 6 PDFreyNo ratings yet

- General Santos City Executive Summary 2019Document5 pagesGeneral Santos City Executive Summary 2019Princess Alyssa AbidNo ratings yet

- Binalonan Water District Executive Summary 2020Document4 pagesBinalonan Water District Executive Summary 2020michelangelo lemonNo ratings yet

- La Paz Executive Summary 2021Document5 pagesLa Paz Executive Summary 2021Jeffrey RiveraNo ratings yet

- 03-MWSS2018 Executive SummaryDocument4 pages03-MWSS2018 Executive SummaryEljoe VinluanNo ratings yet

- Surigao Del Norte State University Executive Summary 2022Document8 pagesSurigao Del Norte State University Executive Summary 2022Noli BenongoNo ratings yet

- Cagayan Executive Summary 2022Document5 pagesCagayan Executive Summary 2022Arjimar BaloyoNo ratings yet

- San Isidro Executive Summary 2022Document13 pagesSan Isidro Executive Summary 2022Ronel CadelinoNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- Northern Christian College: The Institution For Better LifeDocument22 pagesNorthern Christian College: The Institution For Better Lifenananana123No ratings yet

- Bell Atlantic Corp v. TwomblyDocument4 pagesBell Atlantic Corp v. Twomblylfei1216No ratings yet

- Thermae RomaeDocument11 pagesThermae RomaeBerenice RamírezNo ratings yet

- CV Sample FormatDocument6 pagesCV Sample FormatVijay MindfireNo ratings yet

- Brochure FDP On 5G Wireless CommunicationsDocument2 pagesBrochure FDP On 5G Wireless CommunicationsevolvingsatNo ratings yet

- Pts B.ing 21-22Document5 pagesPts B.ing 21-22YantisYtNo ratings yet

- S.Shiva Enterprises: Jagat AutomobilesDocument2 pagesS.Shiva Enterprises: Jagat AutomobilesS.SHIVA ENTERPRISESNo ratings yet

- Literature Review of Service Quality in RestaurantsDocument7 pagesLiterature Review of Service Quality in RestaurantsuifjzvrifNo ratings yet

- A Quick Guide To The Employment Rights Act: OcumentationDocument4 pagesA Quick Guide To The Employment Rights Act: OcumentationGeorgia SimmsNo ratings yet

- Mudarabah by Sheikh Muhammad Taqi UsmaniDocument5 pagesMudarabah by Sheikh Muhammad Taqi UsmaniMUSALMAN BHAINo ratings yet

- Simulacro 3 GildaDocument27 pagesSimulacro 3 GildamauricioNo ratings yet

- 13mar2020 Week11Document16 pages13mar2020 Week11cerejagroselhaNo ratings yet

- Get Set Case - WeRock - IIM KozhikodeDocument7 pagesGet Set Case - WeRock - IIM KozhikodeKESHAV RATHI 01No ratings yet

- Bear Stearns and The Seeds of Its DemiseDocument15 pagesBear Stearns and The Seeds of Its DemiseJaja JANo ratings yet

- 101-98-Magazine For The Month of March-2022-FinalDocument138 pages101-98-Magazine For The Month of March-2022-FinalPratyush BalNo ratings yet

- KAPILA User Guide 2023-24Document12 pagesKAPILA User Guide 2023-24SUTHANRAJ K SEC 2020No ratings yet

- Artiste List CompleteDocument165 pagesArtiste List CompleteDorego TaofeeqNo ratings yet

- Energy Management in An Automated Solar Powered Irrigation SystemDocument6 pagesEnergy Management in An Automated Solar Powered Irrigation Systemdivya1587No ratings yet

- Velcan Energy Company Profile Dec 2015Document22 pagesVelcan Energy Company Profile Dec 2015filipandNo ratings yet

- Businessline 1101Document32 pagesBusinessline 1101Seok Jun YoonNo ratings yet

- Brochure Final PDFDocument2 pagesBrochure Final PDFCarl Warren RodriguezNo ratings yet

- Human Action: A Treatise On Economics by Ludwig Von MisesDocument6 pagesHuman Action: A Treatise On Economics by Ludwig Von MisesHospodar VibescuNo ratings yet

- Tajweed TerminologyDocument2 pagesTajweed TerminologyJawedsIslamicLibraryNo ratings yet

- Lesson Plan in Teaching Mapeh 8Document9 pagesLesson Plan in Teaching Mapeh 8Kimverly zhaira DomaganNo ratings yet

- English Core 5Document14 pagesEnglish Core 5Tanu Singh100% (1)

- Quita v. Court of AppealsDocument6 pagesQuita v. Court of AppealsShairaCamilleGarciaNo ratings yet

- John Read Middle School - Class of 2011Document1 pageJohn Read Middle School - Class of 2011Hersam AcornNo ratings yet