Download as xlsx, pdf, or txt

You might also like

- 4 G 69Document18 pages4 G 69dhikomo100% (2)

- Designing Urea ReactorDocument21 pagesDesigning Urea ReactorAdawiyah Al-jufri100% (4)

- Copy of CF Assignment 1(1)Document14 pagesCopy of CF Assignment 1(1)GANVIR NISHIT PRADEEP MBA 2023-25 (Kolkata)No ratings yet

- 17a Charts Histogram V3Document7 pages17a Charts Histogram V3jyotsnaNo ratings yet

- TLKM. Olah Data BaruDocument5 pagesTLKM. Olah Data Barusyahrul oikosNo ratings yet

- SpiceJet SensexDocument985 pagesSpiceJet SensexManvi ParikhNo ratings yet

- Bank Alfala: Date Price Change ReturnsDocument17 pagesBank Alfala: Date Price Change Returnssyed ali mujtabaNo ratings yet

- Stock ValuesDocument12 pagesStock Values可惜可惜No ratings yet

- Frontera Riesgo - Rendimiento Cuervo y LalaDocument8 pagesFrontera Riesgo - Rendimiento Cuervo y LalaTadeo CabreraNo ratings yet

- Return Covariance and Correlation 23 April 2021Document261 pagesReturn Covariance and Correlation 23 April 2021Tushar AroraNo ratings yet

- Cyiet LimitedDocument53 pagesCyiet Limitedsoumya MNo ratings yet

- WMAI AssignmentDocument13 pagesWMAI AssignmentArbaz MalikNo ratings yet

- SM Class 2Document7 pagesSM Class 2Abhishek singhNo ratings yet

- Varianza y CovarianzaDocument4 pagesVarianza y CovarianzaWendy SequeirosNo ratings yet

- Company Name Stock Symbol Average Monthly Return (5 Years) Standard Deviation of Monthly ReturnsDocument8 pagesCompany Name Stock Symbol Average Monthly Return (5 Years) Standard Deviation of Monthly Returnsanon_764902750No ratings yet

- DXY To GOLDDocument12 pagesDXY To GOLDAgrim JainNo ratings yet

- Price Data in %%Document31 pagesPrice Data in %%NISHANTNo ratings yet

- Risk and Return in ExcelDocument7 pagesRisk and Return in ExcelSubashNo ratings yet

- Aliza Bsaf 22 47Document29 pagesAliza Bsaf 22 47Muhammad HasnainNo ratings yet

- Monte CarloDocument428 pagesMonte CarloShruti BindalNo ratings yet

- Initial ExclDocument17 pagesInitial ExclSubrata Chanda UthpalNo ratings yet

- Name Shahzad Kkhan Roll - No 8 Semester BBA (7TH) Submitted To Sir Asif Subject Investment Analysis and Portfolio ManagementDocument3 pagesName Shahzad Kkhan Roll - No 8 Semester BBA (7TH) Submitted To Sir Asif Subject Investment Analysis and Portfolio ManagementSheheryar KhanNo ratings yet

- BSE Post-CovidDocument8 pagesBSE Post-CovidPragyna ThotaNo ratings yet

- Date Adj Close Cisco Adj Close S & P Cisco SP 100Document5 pagesDate Adj Close Cisco Adj Close S & P Cisco SP 100Sabia Gul BalochNo ratings yet

- Capm InfyDocument7 pagesCapm InfySouparno ChaudhuriNo ratings yet

- Date Indiacpi Uscpi Inflation Differential Repoindia UsfedrateDocument7 pagesDate Indiacpi Uscpi Inflation Differential Repoindia UsfedrateRohan ShankpalNo ratings yet

- MC16 Stock TDocument1 pageMC16 Stock Tsivaji_ssNo ratings yet

- CorregidoDocument31 pagesCorregidoEleonor de PortillaNo ratings yet

- Trabajo Listo Carteras ListasDocument49 pagesTrabajo Listo Carteras ListasSantiago SanchezNo ratings yet

- Entrega 1Document35 pagesEntrega 1Nicolas Peralta PaezNo ratings yet

- If Team 02 Excel FileDocument27 pagesIf Team 02 Excel FileWasif MahmudNo ratings yet

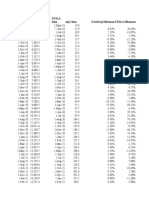

- Regression Beta of TeslaDocument5 pagesRegression Beta of TeslaNikhil AnantNo ratings yet

- 4-Petra - 770 South HarborDocument302 pages4-Petra - 770 South HarborJNo ratings yet

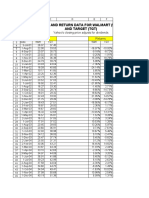

- Price and Return Data For Walmart (WMT) and Target (TGT) : Prices Returns Yahoo's Closing Price Adjusts For DividendsDocument13 pagesPrice and Return Data For Walmart (WMT) and Target (TGT) : Prices Returns Yahoo's Closing Price Adjusts For DividendsArisha KhanNo ratings yet

- Beta Less Than OneDocument11 pagesBeta Less Than OneAmi DuttaNo ratings yet

- Tinangis Farm: January 12, 2024Document46 pagesTinangis Farm: January 12, 2024suarezrichard005No ratings yet

- Date Sale RP RP-RP' (RP-RP') 2 Semi Variance IndexDocument3 pagesDate Sale RP RP-RP' (RP-RP') 2 Semi Variance IndexAbdul NaveedNo ratings yet

- Dự Báo Định Lượng - Tuần 2 - Ví DụDocument18 pagesDự Báo Định Lượng - Tuần 2 - Ví Dụphanngocduy2004.2019No ratings yet

- Pgp32345 - FM Axis Bank BetaDocument57 pagesPgp32345 - FM Axis Bank BetaVivek AnandanNo ratings yet

- Project Meal IngDocument21 pagesProject Meal Ingsimply_alNo ratings yet

- Al CompresiónDocument17 pagesAl CompresiónBelinda ZuñigaNo ratings yet

- Stock TempDocument1 pageStock TempFachransjah AliunirNo ratings yet

- Ashok LeylandDocument13 pagesAshok LeylandAditya NainNo ratings yet

- Capm - STKDocument54 pagesCapm - STKduaenguyen1102No ratings yet

- 3.2.2b Tính Beta Và Chi Phi Von ChuDocument10 pages3.2.2b Tính Beta Và Chi Phi Von ChuLê TiếnNo ratings yet

- Price and Return Data For Walmart (WMT) and Target (TGT) : Prices Returns Yahoo's Closing Price Adjusts For DividendsDocument19 pagesPrice and Return Data For Walmart (WMT) and Target (TGT) : Prices Returns Yahoo's Closing Price Adjusts For DividendsSyed Ameer Ali ShahNo ratings yet

- Risk Management VarsityDocument26 pagesRisk Management VarsityaadishNo ratings yet

- NEDL Appraisal RatioDocument64 pagesNEDL Appraisal RatioSrinivasa PanglossNo ratings yet

- Turkey CanadaDocument6 pagesTurkey CanadaSimraNo ratings yet

- Var of Tata ElxsiDocument160 pagesVar of Tata Elxsifarazahmadas6No ratings yet

- Nifty: Date Rel Nav Sahara NavDocument8 pagesNifty: Date Rel Nav Sahara Navmayankco84No ratings yet

- Lab Poa WinterDocument12 pagesLab Poa WinterHanif Cesario AbdullahNo ratings yet

- Taller 12 ExcelCMVNDocument3 pagesTaller 12 ExcelCMVNcarlos MiguelNo ratings yet

- Airline WACC ExampleDocument6 pagesAirline WACC ExampleSritam DasNo ratings yet

- A10 - Atividade Sobre Beta e CAPMDocument6 pagesA10 - Atividade Sobre Beta e CAPMKaren RauaneNo ratings yet

- Kohinoor TextileDocument90 pagesKohinoor TextileRameen AliNo ratings yet

- Report Spotspeed Volume v2Document20 pagesReport Spotspeed Volume v2Muhd Shahrulazmi HashimNo ratings yet

- Simulador de Créditos: Producto Importe en Plazo en Tasa Efectiva Día de Pago Fecha CuotaDocument13 pagesSimulador de Créditos: Producto Importe en Plazo en Tasa Efectiva Día de Pago Fecha Cuotadiana cuevaNo ratings yet

- ANIM3 BetaDocument23 pagesANIM3 BetaFlathon CardosoNo ratings yet

- Sumativa 1 Exp 2 FinDocument14 pagesSumativa 1 Exp 2 FinRoger Danilo Lujan ArmasNo ratings yet

- Procter & Gamble Co.: Tasas Mensuales de RetornoDocument7 pagesProcter & Gamble Co.: Tasas Mensuales de RetornoCELESTENo ratings yet

- EE364a Homework 4 SolutionsDocument21 pagesEE364a Homework 4 SolutionsSakshi SharmaNo ratings yet

- Vinay Sharma - inDocument3 pagesVinay Sharma - inVinay SharmaNo ratings yet

- Q170MCPU Motion Controller User's ManualDocument274 pagesQ170MCPU Motion Controller User's ManualAbdNo ratings yet

- Geotech Quiz 3 For CTRL FDocument19 pagesGeotech Quiz 3 For CTRL FkbgainsanNo ratings yet

- Physics ProposalDocument8 pagesPhysics Proposalrairaicute100% (2)

- IEEE Standards 1585Document23 pagesIEEE Standards 1585pcsen95No ratings yet

- HIPOTERMIA EN TCE. Estudio POLAR 2018Document15 pagesHIPOTERMIA EN TCE. Estudio POLAR 2018Miguel Angel Velaz DomínguezNo ratings yet

- Project Report On Tpms DeviceDocument12 pagesProject Report On Tpms DeviceVikas KumarNo ratings yet

- 4x4 MIMO Boosts 4G and Gives Consumers A Taste of The Gigabit ExperienceDocument26 pages4x4 MIMO Boosts 4G and Gives Consumers A Taste of The Gigabit ExperiencemathNo ratings yet

- Astm C796Document6 pagesAstm C796Abel ClarosNo ratings yet

- The Use of Hec-Ras Modelling in Flood Risk Analysis PDFDocument8 pagesThe Use of Hec-Ras Modelling in Flood Risk Analysis PDFaNo ratings yet

- Gonzalez Gar Zon Miguel Angel 2017Document288 pagesGonzalez Gar Zon Miguel Angel 2017Wilmar LlhNo ratings yet

- Chapter 10Document27 pagesChapter 10Yash GandhiNo ratings yet

- Chem7a BSN-1-J Module2 Group5 DapulaseDocument4 pagesChem7a BSN-1-J Module2 Group5 DapulaseKiana JezalynNo ratings yet

- Actchem 85 85 RST 8-15Document1 pageActchem 85 85 RST 8-15rivrsideNo ratings yet

- 001 - SerQual ParasuramanDocument29 pages001 - SerQual Parasuramanfenilia15No ratings yet

- Expt 8 EDC-2Document8 pagesExpt 8 EDC-2samarthNo ratings yet

- Common Bridge RectifiersDocument6 pagesCommon Bridge RectifiersAsghar AliNo ratings yet

- AC TO DC CONVERTERS Paper 1 PDFDocument3 pagesAC TO DC CONVERTERS Paper 1 PDFDonigoNo ratings yet

- Introduction To Experimental Archaeology - Outram PDFDocument7 pagesIntroduction To Experimental Archaeology - Outram PDFDasRakeshKumarDasNo ratings yet

- Difference Between RAM and ROMDocument7 pagesDifference Between RAM and ROMJan Carlo Balatan Pablo100% (2)

- Motor Data For 32038Document1 pageMotor Data For 32038zo-kaNo ratings yet

- Criotom Server Manual PDFDocument282 pagesCriotom Server Manual PDFAlex RaileanNo ratings yet

- MPR TMN NetworkingDocument91 pagesMPR TMN Networkingkazi_hoque5729No ratings yet

- Lesson 2Document7 pagesLesson 2maria genioNo ratings yet

- Huawei S6720-HI Series Switches DatasheetDocument25 pagesHuawei S6720-HI Series Switches DatasheetAbdelhafid LarouiNo ratings yet

- Assignment 2Document4 pagesAssignment 2kalana chamodNo ratings yet

- 1 BoardCompanion Physics PDFDocument61 pages1 BoardCompanion Physics PDFSrn YuvaneshNo ratings yet